If you’re wondering when you should downsize your home, understand that it may be a lengthy process. While everyone’s timeline looks different based on their situation, downsizing involves a multistep process:

- Downsizing your possessions

- Preparing your home to sell

- Selling your home

- Finding and moving into a new house

If you have more space than you need, would like to save some money or plan to travel more, downsizing could be a great step to help you reach your goals. Discover the reasons and benefits of downsizing your home.

Should I Downsize My Home?

If you’re considering downsizing your home, you may be committing to a large, long-term project. Even if you have a short timeline — whether due to a sudden move or retirement — be sure to take the time to ensure downsizing is right for you. Reflect on why you want to downsize and what the process will involve realistically.

Some questions you may want to consider before downsizing your home include:

- What are my motivations for downsizing? If you want to downsize because you’re looking for a different layout for your home or to have different amenities, consider whether it might make more sense to reorganize or renovate your current home. Many homeowners whose needs change often decide to take out a second mortgage to fund their renovations.

- What do you love about your current home? During the process of buying a new home, you may be tempted to focus on the negatives of your current space. Instead, consider the aspects of your current house you love and use, and add those to your must-have list.

- What will my family or I gain from downsizing? Think about the activities and projects you will be able to accomplish with a smaller home. Perhaps it will allow you to travel more, or mean a safer environment for the children and older adults in your family.

- What are my primary concerns about downsizing? Most people’s main concern with downsizing is budget. You might also worry about missing out on storage, outside space and other amenities you enjoy in your current house.

- What is my timeline? Consider when you’d like to start your downsizing process, how long you want to take and when you ultimately want to complete the process and be in your new space.

- What are my current and future needs? When considering downsizing, think about what you need right now and how your needs might change in the future. Will you have kids moving out, parents moving in or other considerations you’ll want to account for in the downsizing process?

Reasons to Downsize Your Home

Everyone’s reasoning for downsizing will be unique to them, but there are a few important reasons many people choose to downsize. Most of these have to do with a person’s budget, living situation or dreams for the future. Take a look at six reasons why you should downsize your home:

1. Maintenance Costs

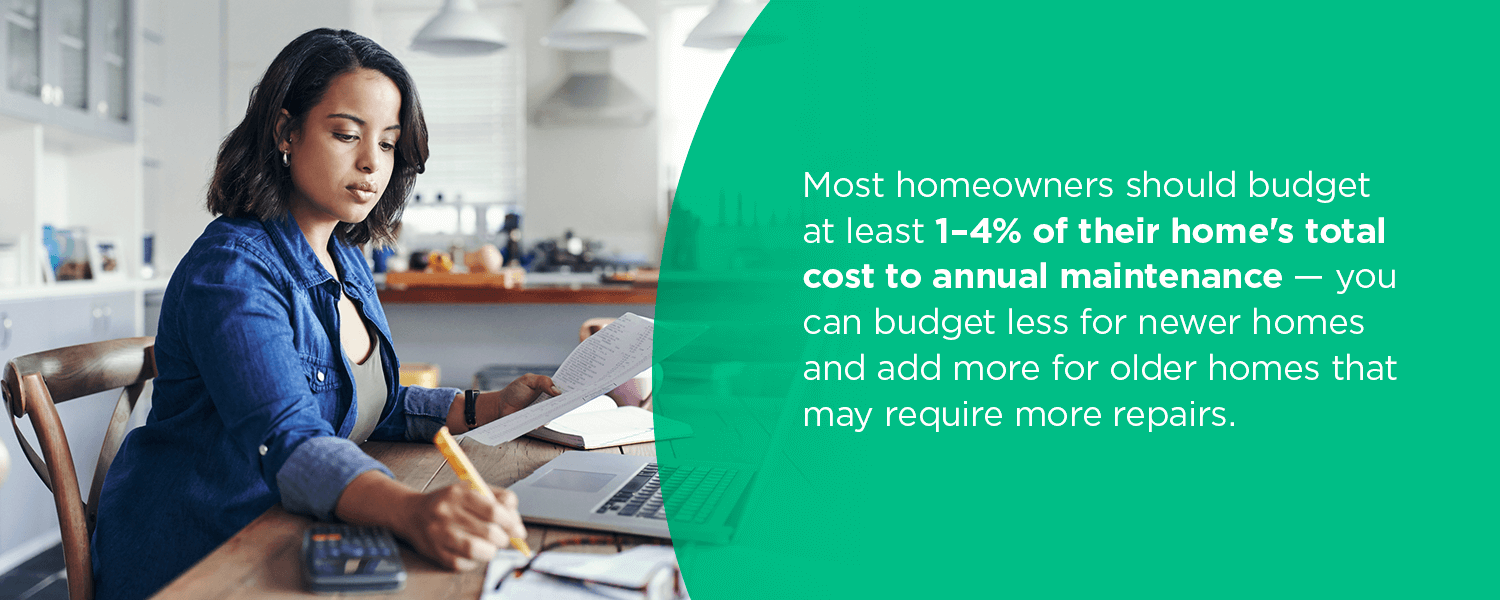

With larger homes and larger yards, you’ll confront higher costs of maintaining your spaces. Most homeowners should budget at least 1-4% of their home’s total cost to annual maintenance — you can budget less for newer homes and add more for older homes that may require more repairs. That means a 20-year-old house that originally cost $500,000 might need a budget of $20,000 each year, while a house for the same price that’s brand new may only need $5,000 for incidental maintenance and upkeep.

Smaller homes have lower price points in many cases, so the cost of maintaining them yearly is much less. With less square footage, you’ll spend less on things like flooring, roofing and heating and cooling costs. Downsizing also might mean a smaller or no outside space, resulting in little to no cost to maintain your yard.

2. Retirement

Most people begin thinking about downsizing while considering retirement. With a little more time on their hands, many envision traveling and participating in activities that make keeping up with a large home more difficult. When you reach retirement age, you may also begin thinking about the future and the potential challenges your current space might incur as you age.

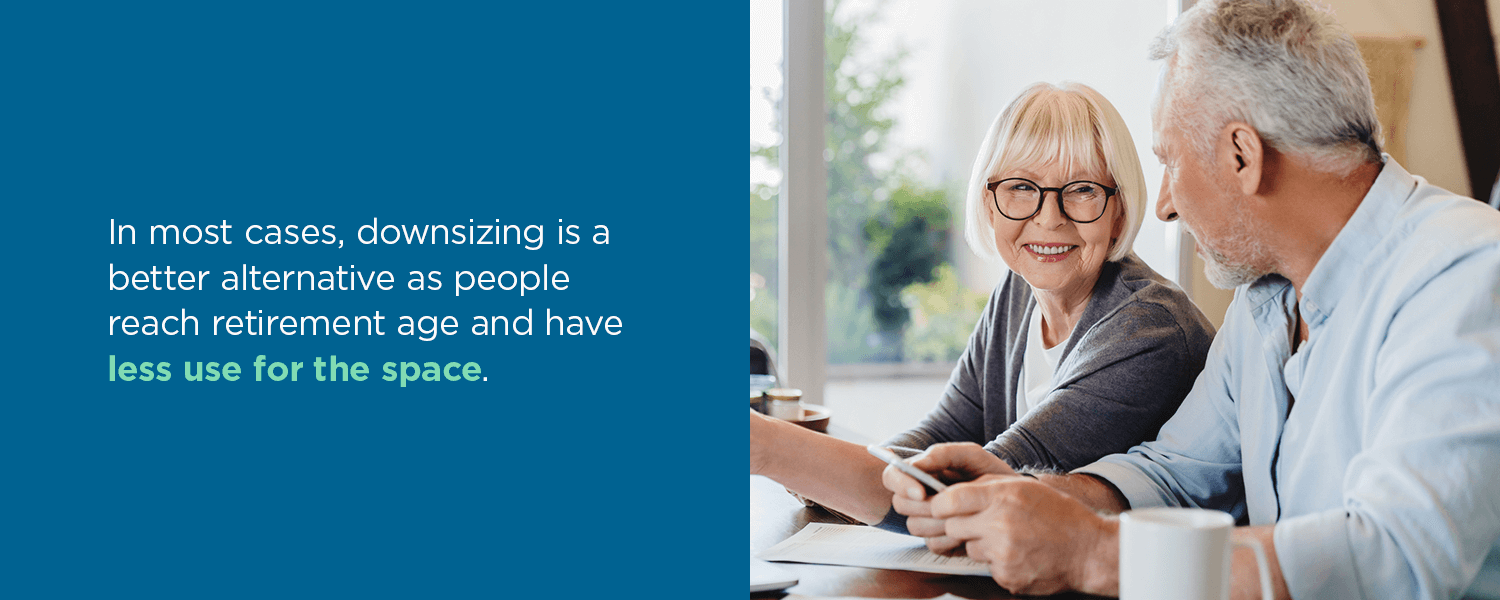

Large homes with steps, steep driveways and other mobility challenges can be dangerous for older adults. Modifications, such as stairlifts, ramps and railings, may be simple and affordable to add to existing homes, but tasks like widening doorways, adjusting counter heights, leveling flooring and remodeling the shower or tub may prove more expensive than they’re worth. In most cases, downsizing is a better alternative as people reach retirement age and have less use for the space.

For many retired individuals and couples, condos and townhomes are attractive options when thinking about downsizing. They often provide on-site maintenance with staff handling outside work as well. Secondly, they also provide a community for older adults to gather together, a service that becomes incredibly important given the increased rates of loneliness in retired adults.

3. Unused Space

If you find you’re leaving entire rooms or wings of your house vacant for extended periods of time, it may be a sign to consider downsizing. When initially purchasing a home, it can be tempting to go with an option that has more rooms and closets than you need. However, having extra, unused space may seem wasteful if your family doesn’t use it as time passes.

Many parents find they have a lot of unused space in their homes after their children move out for college and job opportunities. With whole rooms and bathrooms suddenly out of use, downsizing becomes an attractive idea. In addition to spending less time on upkeep — unused rooms still need vacuuming and dusting, after all — downsizing can provide opportunities for people to start saving for retirement.

4. Travel

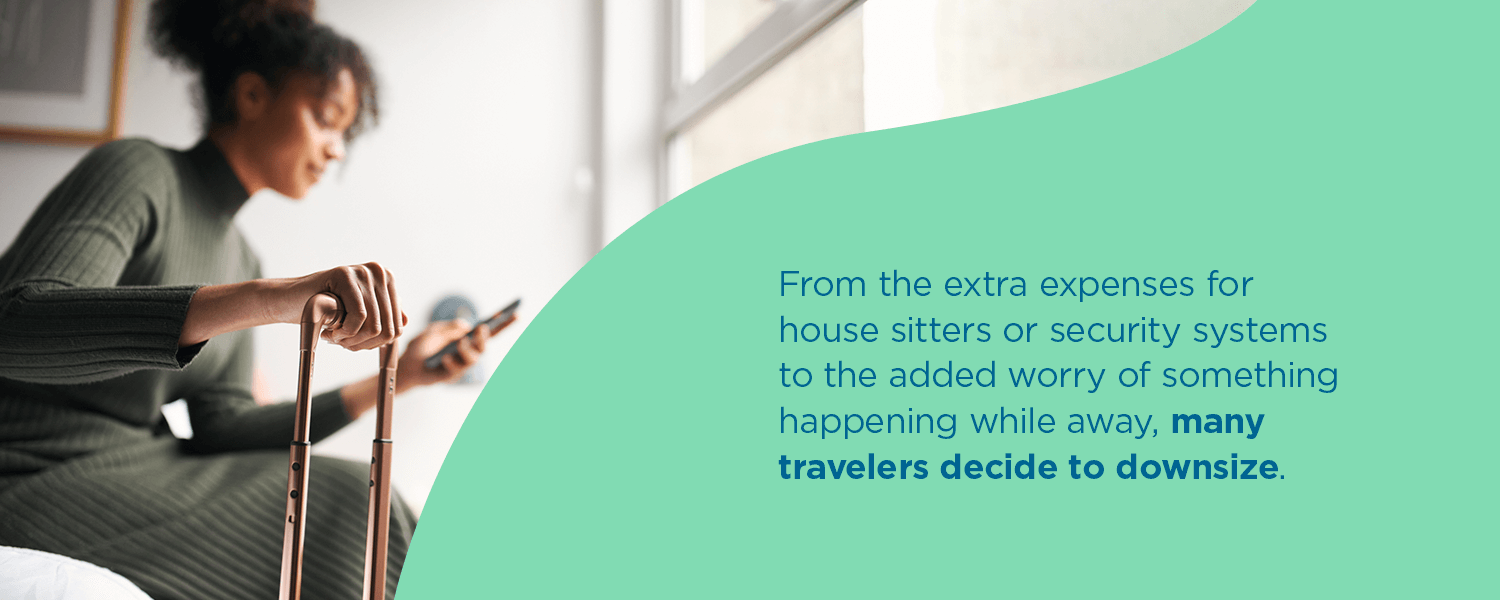

Traveling can be a wonderful experience that broadens your mind and introduces you to new experiences. Many who travel frequently find keeping up with their home while away is difficult. From the extra expenses for house sitters or security systems to the added worry of something happening while away, many travelers decide to downsize.

Many avid travelers downsize to condos and townhomes or smaller homes — some even turn to tiny homes — to reduce the cost and hassle of keeping up with a larger home. Whether you travel for fun or work, having less space to manage can give you peace of mind while away. Some also find that downsizing makes funds available to embark on the adventures they’ve always wanted to go on.

[download_section]

Benefits of Downsizing Your Home

If you’re on the fence about whether downsizing is right for you, consider all the benefits that come with enjoying a smaller living space. Many people have concerns about storage, sleeping space and privacy when moving to smaller homes, condos or townhomes, but the following are some amazing benefits you can reap when downsizing your space:

More Time

Many homeowners feel the time they spend on household chores interferes with their ability to spend time with their family and friends. Some time-consuming household tasks include:

- Yardwork

- Floor cleaning

- Laundry

- Dishes

However, there are hundreds of other tasks that require the homeowner’s attention. This time can double if something breaks down or malfunctions, and you have to make time to call a repair technician, schedule an appointment and find an alternative solution until the problem is fixed.

With a smaller home, you have less space to maintain, meaning tasks like vacuuming, mopping and deep cleaning take less time. Downsizing might also mean reducing the volume of clothes and the number of appliances you own, drastically reducing laundry time and potential maintenance issues.

Less Debt and More Savings

In most cases, moving into a smaller home means the actual cost of the home is much less, in addition to lower maintenance and upkeep costs. If you have a good real estate agent and time your home sale optimally, you could get up to full or more than the asking price for your home. This can set you up with more money to spend on your new home mortgage and even free up some extra funds to put toward paying off any debt.

If you have a few acres on your larger property, you might rely on a yard service to maintain your lawn — when you move to a smaller place with a smaller yard, you can likely do the yard work yourself, or at least pay less for the service to maintain your yard. You’ll also have less furniture, decorations and supplies to buy for the smaller space.

Simplicity

Some people find downsizing is great for their mental health and emotional well-being. Psychologists have found that living in cluttered living spaces can contribute to heightened levels of anxiety and can even lead to a phenomenon called “mental clutter.” When you have a lot of space, your tendency may be to fill it up — which often happens when people have plenty of storage space to keep things they don’t use every day.

Having less space and fewer things to fill it with can lead to a simpler life. Certain life philosophies and approaches advocate for reducing your possessions and keeping only the essential items for your life. In doing so, people can experience a more fulfilling life.

Reduced Energy Costs

On average, most households spend over $2,000 on utility bills each year. For larger houses, you might spend more — but downsizing means your utility costs could lower. That can leave more money in your budget each month for things like groceries and mortgage payments, or you can save that money for a special trip or another investment.

Urban Living

If you downsize, it can open up more possibilities as to where you can live. Many families with young children in school find life simpler in the suburbs. With more space to spread out, families enjoy the safety and familiarity of wide-open neighborhoods. However, when kids move out or the time comes to downsize, urban living becomes a possibility.

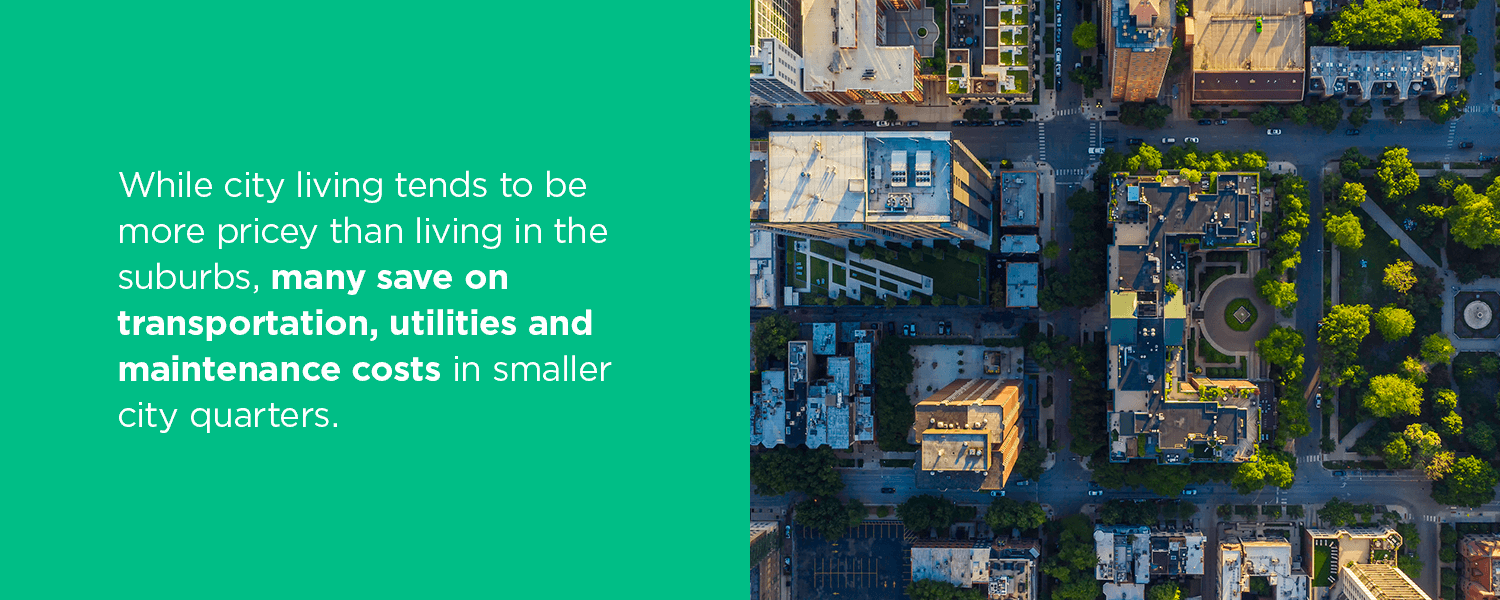

With almost everything you could need within a few steps from your front door, living in the middle of a big city is extremely attractive to some people. The bustle of city life and the cultural diversity can make every day an adventure. While city living tends to be more pricey than living in the suburbs, many save on transportation, utilities and maintenance costs in smaller city quarters. Living in a city might also make travel more accessible due to access to airports and train stations.

How to Downsize Your House

If you’ve decided downsizing is right for you and your family, the next step is actually doing it. While planning can help immensely with the process, there are a few processes that can help.

Timing Is Everything

When planning to downsize, knowing the housing market situation is essential. If you can time your home sale during a period where there are more buyers than supply, you’ll get the best price for your home. This seller’s market means you will have more power in selling your current home. Some buyers may even waive inspections and offer more than the asking price.

When you have more money from the sale of your current home, you can put that towards a down payment on your smaller home or condo. In most cases, this means you may be able to afford a nicer home or one in a more expensive area. You might also choose to offer a larger down payment to reduce the amount you’ll have to pay each month.

You might also want to time your downsizing with a buyer’s market when there’s plenty of supply and little demand, making it more likely you’ll get a great deal when purchasing your new home. If you plan to downsize significantly, this approach could be a great idea. Even if you may lose a little on the sale of your larger place, you’ll still have plenty to put toward your smaller place.

Methods of Downsizing Your Possessions

When planning to move somewhere smaller, one of your first thoughts is likely, “Okay, but what do I do with all this stuff?” If you’ve been in your current space for a while, you’ve likely amassed a sizable collection of clothing, toys, furniture and other items you may not be able to take to your new place. Before you begin preparing your home for sale, start downsizing your possessions.

Starting with this makes the moving process easier and also gives you a good idea of how much storage and space you’ll need in your new place. You can also do this even if you’re still on the fence about downsizing to a new home. Many people like to do small clear-outs seasonally, often in spring, to rid their closet of clothes they haven’t worn in a year or two. However, the type of clean-out you’ll need to do for downsizing will likely be more intense.

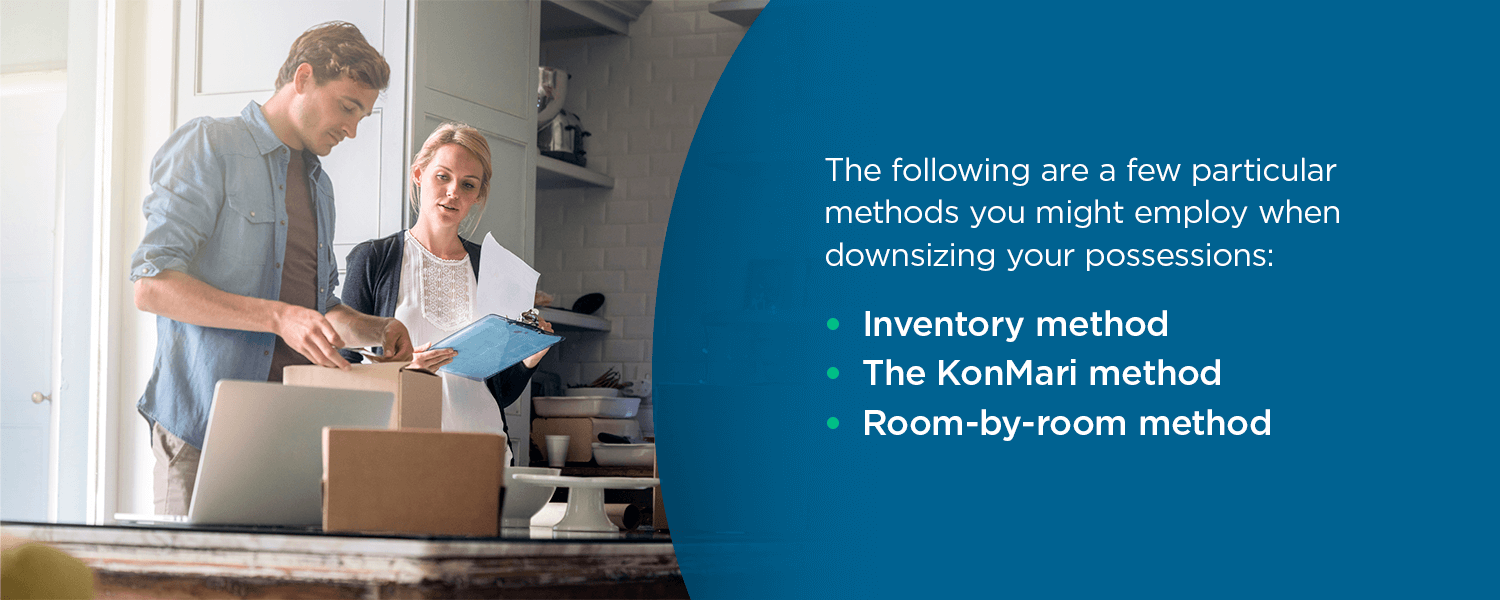

Go through every room and take a close look at everything you own. Most people use a three-pile method — keep, donate, toss — to sort through items, but this method can be overwhelming when looking at all your possessions at once. The following are a few particular methods you might employ when downsizing your possessions:

- Inventory method: If you’re a lover of spreadsheets, this might be the method for you. Take inventory of all your belongings by categorizing them into certain groups, such as clothing, appliances, kitchen tools and toys. Seeing all your items laid out visually on a screen or piece of paper will help you realize how much you have. As you clean out items from your home, remove them from your list until you have a manageable number.

- The KonMari method: The KonMari method focuses on items that “bring joy” and approaches tidying and downsizing as a process of ensuring you surround yourself with things you love and use. For this method, you’ll divide your possessions based on categories and sort through them. If they do not “spark joy,” it’s time to give them up.

- Room-by-room method: Taking your house room by room, you’ll completely sort each one before moving on to another. Many people start with the toughest room first, which often is a garage, attic or basement. This method can help compartmentalize your clearing out, especially if a busy schedule means you can’t upend your entire house all at once.

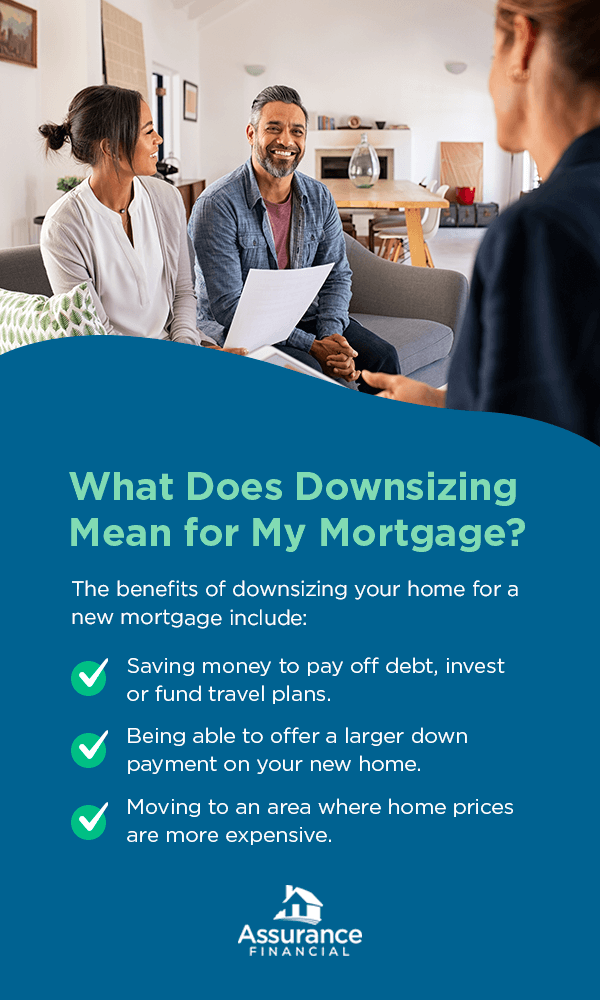

What Does Downsizing Mean for My Mortgage?

Whenever you sell your home, your mortgage will likely change. When downsizing, this often means your current mortgage is more than your new one will be. If you own your home outright, you can sell the old one and pocket the difference. However, most people still own at least some of their mortgage when they decide to sell and downsize to a smaller home.

The benefits of downsizing your home for a new mortgage may include:

- Saving money to pay off debt, invest or fund travel plans.

- Being able to offer a larger down payment on your new home.

- Moving to an area where home prices are more expensive.

A potential challenge you might face is that your current home may not be worth as much as you think. Homes tend to depreciate no matter what, but you can counteract this by investing a little in your home to bring important features up to date. Things like kitchens and bathrooms can be expensive remodels, but it often pays off when it comes to selling your home, especially in a competitive market.

When you sell your home, you will likely have a sizable amount of equity to cash in on. The buyer’s money will go toward paying off the rest of the mortgage and the sale’s closing costs. However, if you have a more valuable home than the one you’re buying, you can pocket the difference as profit.

What Kind of Mortgage Should I Get After Downsizing?

After you downsize and sell your home, you’ll be looking for a new mortgage. The most common mortgage options are 10, 20, 15 and 30-year mortgages. For first-time home-buyers, usually young people or young families, a 30-year mortgage is a great option to get lower monthly payments and put less money down.

However, if you’re downsizing into a new home, especially if you’ve retired, a 15-year mortgage is a great option. Some of the benefits of a 15-year mortgage might include:

- Lower interest rates.

- Equity builds more quickly.

- Lower overall cost due to interest savings.

Apply for a Mortgage With Assurance Financial

There’s a lot to consider when you decide to downsize your home. Thinking about selling your home and purchasing a new one can be an overwhelming prospect, but working with a qualified financial partner can help make the process much smoother.

Assurance Financial makes applying for a mortgage simple and straightforward. We offer every type of loan available on the market and are committed to offering competitive rates and superior customer service. You can apply online in 15 minutes with our digital assistant, Abbey, or speak with a licensed loan officer.

Linked sources:

- https://assurancemortgage.com/second-mortgage-vs-refinance/

- https://www.forbes.com/sites/juliadellitt/2018/06/20/why-you-need-to-adjust-your-monthly-budget-for-home-maintenance/?sh=610b6db934a0

- https://assurancemortgage.com/tiny-home-mortgages-explained/

- https://www.psychologytoday.com/us/blog/fulfillment-any-age/201705/5-reasons-why-clutter-disrupts-mental-health

- https://www.energystar.gov/products/ask-the-expert/breaking-down-the-typical-utility-bill

- https://assurancemortgage.com/buyers-vs-sellers-market/

- https://assurancemortgage.com/15-vs-30-year-mortgages/

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/find-a-loan-officer/