Key Takeaways

- Critical questions include: Can I afford the down payment and closing costs? Am I financially stable? How much house can I afford? Can I secure a good mortgage rate? How long do I plan to stay? Am I ready for homeownership challenges? And what do I want in a home?

- These foundational questions guide financial planning and ensure realistic homebuying decisions.

- Detailed answers to these questions determine whether homeownership is feasible and appropriate for your situation.

For many in the U.S., home buying is an essential component of the American dream. A home is also one of the most significant investments you’ll make during your lifetime, and isn’t a decision to make hastily. If you’re feeling overwhelmed at the idea of buying a home, you’re not alone. At Assurance Financial, we know how stressful the process of home buying can initially seem, and we want to make this exciting step in your life as easy and enjoyable as possible.

Before buying a home, there are a few external factors you’ll want to consider, questions you’ll want to ask yourself to determine whether you’re ready to purchase a home and pros and cons you’ll want to weigh when you find a house you’re interested in. Once you’ve run through your checklist of what to ask when buying a house and what to know before making an offer on a house, we can help you acquire your dream mortgage.

- Can I Afford the Down Payment?

- Am I Financially Stable?

- How Much House Can I Afford?

- Can I Secure a Good Mortgage Rate?

- How Long Do I Plan to Stay Here?

- Am I Ready for the Challenges of Owning a Home?

- What Do I Want in a Home?

External Factors in The Home Buying process

Outside of your financial situation, there may be external factors to consider before you decide to buy a home. What are the market’s current interest rates? How is the economy performing? How has nature affected the market? These are all things you should look into before buying a home.

1. Interest Rates

The economy, politics and banks can influence interest rates. The Federal Reserve also regulates these rates in part, though human control of interest rates can sometimes spell trouble for the housing market.

2. The Economy

Various factors, such as politics, employment levels and consumer confidence, compose the economy. When looking for a home in a specific region, you’ll want to look at the market nationally, as well as regionally. The real estate market and economy in Texas may be quite a bit different from the market in Maine, for example. The market may even vary between cities in the same state, so it can be beneficial to do some research into your potential home’s area before jumping in.

3. Impacts of Nature

Natural disasters can significantly affect the real estate market. A devastating storm can cause a thriving market to completely turn around in a matter of days. People may abandon the area, and homeowners may become renters. Listings may increase, but prices may drop and it could take quite some time for the market to rebound.

Plenty of factors from your situation come into play when looking to buy a house, but be sure you don’t overlook external factors such as interest rates, the economy and the impacts of nature when making your decision about when to enter the market.

Questions to Ask Before Buying a House

Before choosing to buy a home, there are a few questions you may want to ask yourself to determine whether homeownership is the right next step for you. Here are seven of these to get you started.

1. Can I Afford the Down Payment & Closing Costs?

The standard rule of thumb when it comes to a down payment on a home is 20%. However, you can also put a down payment of as low as 10% for a conventional loan and 3.5% for a Federal Housing Administration loan. Depending on the type of loan you’re looking to get, do you have enough money to make the down payment? You’ll also need to factor in closing costs, which can cost between 2 and 5% of the home’s value. Though the seller may sometimes contribute to these closing costs depending on the deal you get and the state of the market, you may still want to ensure you’ve saved up enough to cover these costs.

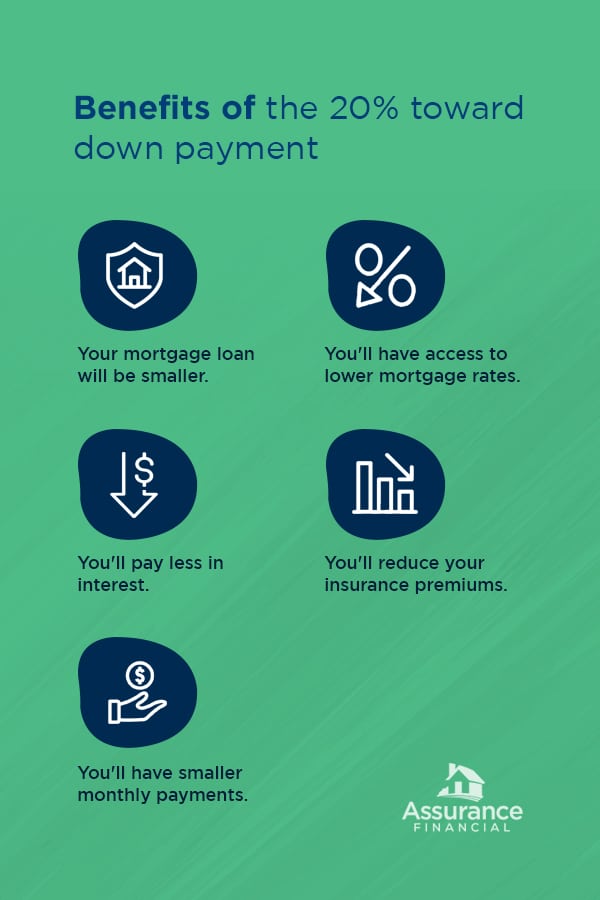

Putting a down payment of 20% toward your house can offer a range of benefits:

- Your mortgage loan will be smaller.

- You’ll have access to lower mortgage rates.

- You’ll pay less in interest.

- You’ll reduce your homeowner insurance premiums.

- You’ll have smaller monthly payments.

The more you can put down on your house up front, the more money you’ll save in the long run.

2. Am I Financially Stable?

Are you currently able to meet your other financial obligations and goals? Are you paying your bills on time every month? Are you consistently achieving your goal for retirement savings? Do you have an emergency fund? Before introducing a mortgage into the mix, you’ll want to ensure you’re covering all your other financial goals and obligations. If you’re able to say you do meet all of your other financial obligations, you may be able to comfortably fit a house into your budget.

A mortgage is a long financial commitment. Even most shorter-term mortgages are at least 10 years. The standard mortgage term is 30 years, so ideally, you’ll want to be financially stable for the duration of your mortgage, which could be several decades. Job security and a steady income are great ways to ensure financial stability, but since job loss can happen to anyone, you’ll want to ensure you can continue paying your mortgage even in the face of losing your source of income.

To prepare for this possibility, you may want to save several months’ worth of living expenses to cover you during your gap in employment. If you work in a field with high demand and you can reasonably expect to get hired in a short amount of time, you may only plan to save up for three to four months of living expenses. If you don’t work in a field with high demand and you anticipate a job loss may leave you unemployed for several months, consider saving up an emergency fund of six to 12 months of living expenses. That way, even if you remain unemployed for an entire year, you won’t have to worry about making the payments on your mortgage and bills every month.

3. How Much House Can I Afford?

Take your existing budget and input the new monthly expenses you can expect after you acquire a mortgage. You’ll want to estimate your principal, interest, taxes and insurance to plug into your budget.

Use a Mortgage Calculator

To determine the numbers for your principal and interest, you can use an online mortgage calculator. Experiment to see how much you could comfortably fit into your budget and what amounts would be stretching your budget uncomfortably thin. You can also look at the current rates from a lender like Assurance Financial for different types of loan terms, such as 15-year versus 30-year or conventional versus FHA. Try out of our Assurance Financial mortgage calculators today! Several payoff calculators also exist on many real estate websites. This can help with long-term planning which could help you avoid mistakes.

Taxes and Homeowner Insurance

To determine the approximate cost of your property taxes, you can look online for homes for sale in the area you’re interested in and find examples of what the approximate taxes might be. Usually the home you are purchasing includes historical property tax information as part of the buying process. Estimating your homeowner insurance may be a little trickier without an address to give your insurance company, but they may still be able to provide you a with reasonable estimate or range. We also recommend looking into past insurance claims on the home. Understanding the history of past insurance can open your eyes to a wealth of information on your potential new home, and may give you the information needed to change your total budget requirements.

A Quick Note On Homeowners’ Association Dues and Other Expenses

Other costs potential homeowners may overlook include fees for a homeowners’ association, an alarm system, condo fees or utilities. To get estimates for these services, especially homeowners’ association dues, you can research what residents in the area tend to pay for these expenses or contact the utility company to ask about the costs in that specific neighborhood or area. If you’re upscaling from a small apartment to a larger space, you may also want to increase other living costs that tend to go up when you have more space, like furniture, decor and property maintenance.

4. Can I Secure a Good Mortgage Rate?

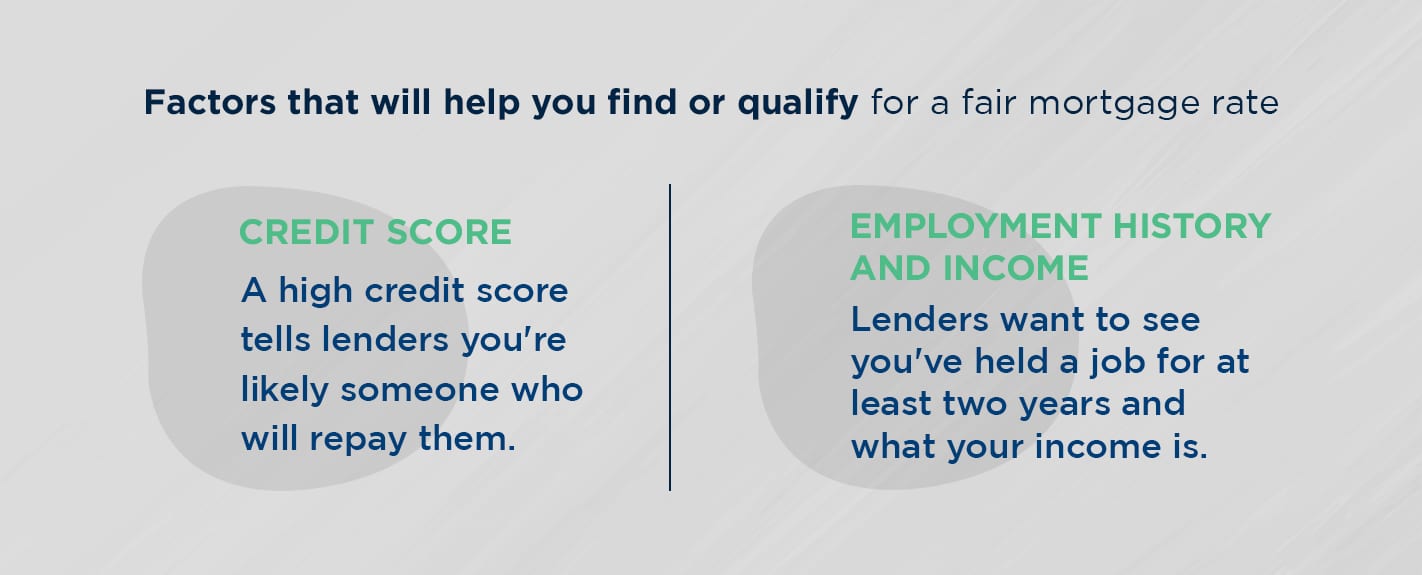

First, do you know what you should consider to be a good mortgage rate? In short, a reasonable rate is one you can afford and that works with your budget. Here’s a closer look at the factors that will help you find or qualify for a fair mortgage rate.

- Credit score: Your credit score is probably the most critical factor when it comes to securing a mortgage. A high credit score tells lenders you’re likely someone who will repay them. Lenders will look at your credit history to determine whether you’ll be able to afford your mortgage and consistently make your payments. Higher scores generally result in the lowest rates, but you’re also likely to qualify for a favorable rate with a score in the mid-range. However, if you want to secure an FHA loan, you could get a mortgage with a lower score. You can request a free credit report every year from the three major credit bureaus. Choose from TransUnion, Equifax and Experian to request your credit report to determine whether your credit score could already secure you a good mortgage rate. You may find you need to do a little more improvement before applying for a mortgage.

- Employment history and income: Lenders also look at your employment history. They want to see you’ve held a job for at least two years and what your income is. If you are not employed, you’re unlikely to get a mortgage at all, let alone a mortgage with a good rate. Lenders may also look at your debt-to-income ratio and your assets. They want to feel confident you have the means to pay them back the money you’re borrowing.

5. How Long Do I Plan to Stay Here?

If you aren’t planning on staying in an area for long, buying a home may not the best option for you. Generally, it’s best to buy a house only if you plan on staying in it for at least five years. This length of time allows you to build up equity in your home and make up for the costs that went into buying, selling and moving.

If you plan on moving within a few years, you may want to consider an ARM — adjustable-rate mortgage — which have rates that adjust every year, unlike fixed-rate mortgages. If market conditions are optimal and rates are consistently dropping, an ARM may be the right option for you in a relatively short-term living situation.

6. Am I Ready for the Challenges of Owning a Home?

A significant difference between owning and renting is that when you own a home, you’re entirely responsible for everything inside it. When the refrigerator stops working or the air conditioning system fails, the cost of making these repairs comes out of your pocket. Before buying a home, you may want to have money set aside in anticipation of property and household damages.

The cost of a home isn’t only what you pay up front, but your continued maintenance and upkeep as well. Yard and outdoor maintenance can include mowing the lawn, raking leaves, clearing debris, cleaning out the gutters, power washing the house or resealing the deck. You may need to worry about paying an exterminator to remove bugs or rodents that enter your house. It’s also smart to get your air conditioning and heating systems inspected at least once a year, along with changing air filters a few times throughout the year. These costs are ongoing, so you’ll want to keep these in mind as you make your yearly or multi-year budget.

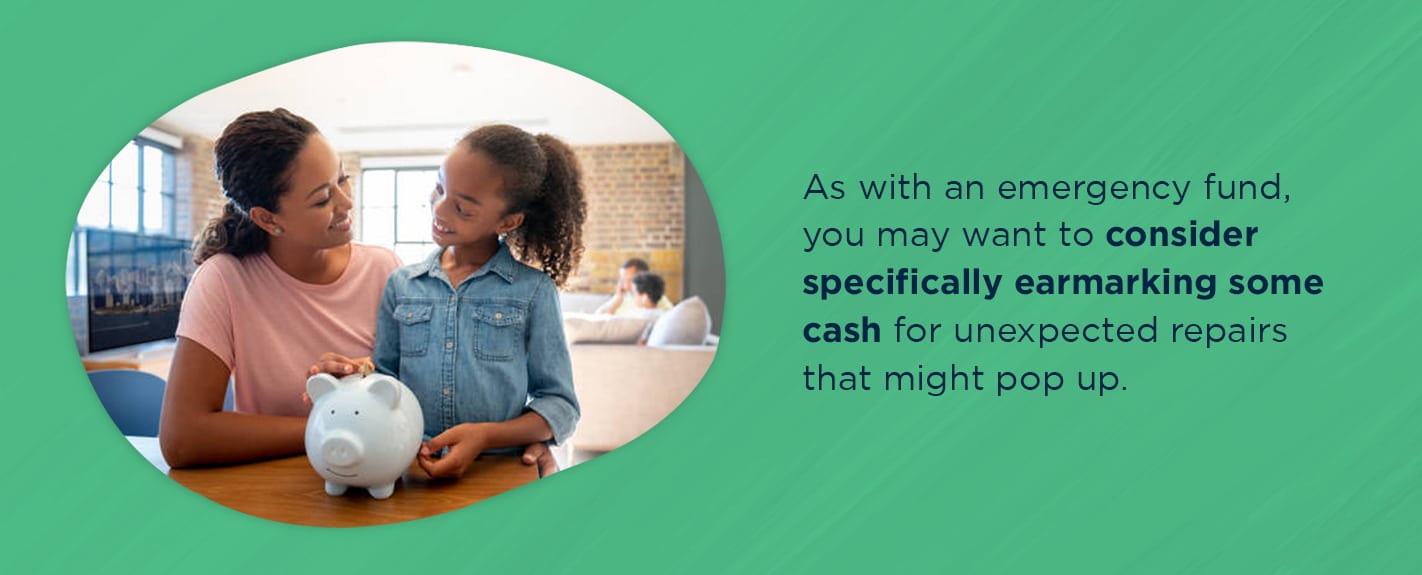

As with an emergency fund, you may want to consider specifically earmarking some cash for unexpected repairs that might pop up. You may want to follow one of two rules of thumb when deciding how to save up for these potential expenses.

- Save $1 per square foot: Every year, set aside $1 for every square foot of your house. If your home is 2,500 square feet, for example, you should save $2,500 every year.

- Save 1% of the sales price of the house. This percentage is not the amount of your mortgage, but the value of the home if you put it on the market today. If your home is currently worth $500,000, that means you would save $5,000.

If you want to save the minimum toward home repairs every year, you may follow the first rule of thumb. If you’d rather err on the side of caution, you may want to follow the second rule of thumb.

7. What Do I Want in a Home?

When compiling your list of questions to ask when buying a home, don’t forget to ask yourself what qualities you find desirable in a house. Make a list of your potential home’s must-haves, what you would like it to have and what your dealbreakers might be.

Your must-haves are any factors your home needs to have for you to buy it. Maybe on your must-haves list, you want central heat and air, rather than having to maintain separate heating and A/C units for each room. Or, perhaps your home needs to be one-story so you don’t need to deal with as much daily upkeep and cleaning. Many parents prioritize finding homes in a good school district to benefit their children. Being in a good school district not only improved your child’s education, but also makes for a better long-term investment. Most real estate websites, such as Zillow and Realtor.com, include school district and rating with each home listing.

Regardless of what you put on your list, you won’t buy a home lacking any of these items.

Your nice-to-haves are perks you would enjoy, but aren’t crucial enough that you would turn down a home that doesn’t have them. These might include a two-car garage or a nice view from the property or new appliances and major systems. If the home does not have these qualities, you’ll still consider purchasing it if it checks all the boxes on your must-have list.

Your list of dealbreakers is anything that would make you not want to buy a home. If you live with multiple people, for example, a dealbreaker for you may be a house with fewer than two bathrooms. Or, maybe you can’t stand the idea of living on a loud, busy street.

If you’ve answered positively to most of these questions, you may be ready to buy a home.

What to Consider Before Making an Offer on a House

Before making an offer on a home, there may be a few factors specific to that house to consider. These factors can include a home inspection, other offers and any work you need to get done based on the condition of the home. Here’s what to know before making an offer on a house.

1. Home Inspection

When you’ve found a house and you want to put an offer in, you will need to get it inspected. Typically, you can take advantage of a 10-day inspection period by bringing in a home inspector to assess the house. You may also want to consider hiring people who work in other trades, such as roofing, plumbing and electricity. A home inspector may not be able to catch everything. Bring in someone who is licensed in a specific profession and who will know what to check in a house before buying, tell you what might be wrong with the system and estimate how much it would cost to fix it. We also recommend using your own home inspector, and not one that your real estate agent works with. Can friends and family for recommendations. When negotiating the sales price of your home with the seller, having this information can work well in your favor.

2. Other Offers

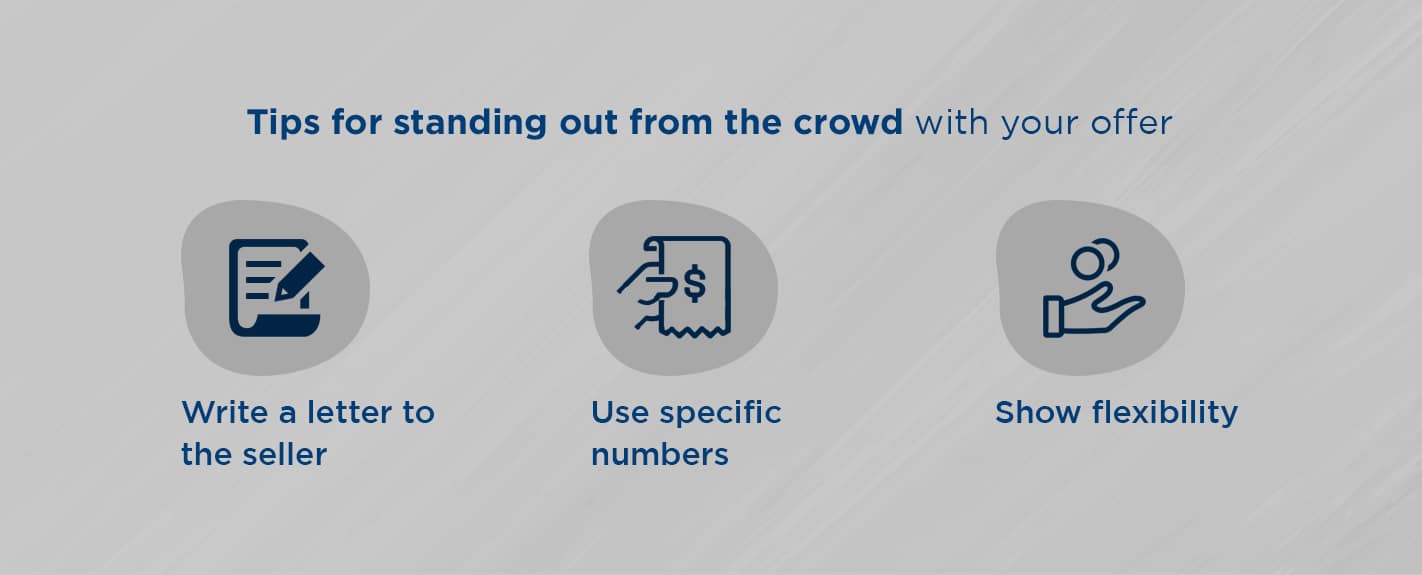

Competition for a home can strike fear into the hearts of homebuyers, especially those who are entering the market for the first time. They worry about offering more than they can reasonably afford or missing out on their dream home. Here are a few tips for standing out from the crowd with your offer.

- Write a letter to the seller: A personal letter may help you be more memorable as a potential buyer. Selling a home can be a stressful and highly emotional time, and a letter with sentimental value can push you over the edge into their favor.

- Use specific numbers: Specific, rather than round, numbers will stick out more in a seller’s mind and may also put your offer just ahead of other buyers, even if only by a couple hundred dollars.

- Show flexibility: Develop your offer around the seller’s specific needs. A seller moving out of the state may want a sooner closing date, so being flexible with the seller may earn you the bonus points that get you the home of your dreams.

Remember, even if you lose out on a bid, you’ll eventually find the right house at the right time with the right bid, and making an offer doesn’t cost anything.

3. Necessary Home Improvements

If you need to do work or make improvements to the home, you’ll want to consider whether the costs of these improvements can fit into your budget. If you anticipate the costs will be too high, you may want to reconsider purchasing the house. On the other hand, if the improvements are minor and the costs can reasonably fit into your budget, you may want to move forward with purchasing. Replacing the roof, for example, could be a pricey home improvement. In contrast, painting a few rooms or installing a new faucet might be a remodeling project that’s within your budget.

Find Your Financing With Assurance Financial

At Assurance Financial, we want to help you achieve your American dream of homeownership. With us, you can find the home of your dreams with the ideal mortgage terms. Buying a house doesn’t have to be overwhelming when you work with the Assurance Financial team.

When applying for a mortgage, you’ll want to have a licensed loan officer to help you through the process. Our application technology and end-to-end processing under one roof will make your loan process quick and straightforward.

Find a loan officer near you today at Assurance Financial to get started, and discover why we’re one of the best lenders for financing a home mortgage.