A mortgage usually lasts for 15 or 30 years, but that doesn’t mean you have to have the same home loan for several decades. Some people choose to refinance their mortgage at some point, either to take advantage of lower interest rates or change the loan length. Some take out home equity loans or lines of credit, which let them borrow against the value of their home. With a home equity loan and a primary mortgage, you effectively have two loans on your home.

Mortgage consolidation gives you the option of merging multiple loans into one. It’s a good way for some people to save money or get a little more breathing room in their monthly payments. Learn more about the mortgage consolidation process and see if it’s right for you.

Table of Contents

- What Does it Mean to Consolidate Mortgages?

- Should You Combine Two Mortgages?

- How to Combine Two Mortgages

- Benefits of a Consolidated Home Mortgage

- Refinance with Assurance Financial

What Does It Mean to Consolidate Mortgages?

Debt consolidation merges multiple debts into a single loan. When someone decides to consolidate their debt, they apply for a new loan and use the principal to pay off the remaining balances on their existing loans. Once the existing loans are paid in full, the borrower is left with only the consolidation loan.

When someone decides to consolidate mortgage debt, they are usually doing one of two things. In some cases, consolidating mortgages means refinancing an existing home loan and using it to pay off a primary mortgage and a home equity loan or second mortgage.

Another option is for a person to refinance their current mortgage and use the new home loan to pay off their current mortgage and other types of debt, such as a car loan or credit card debt. If someone decides to do that, they can apply for a cash-out refinance.

With a cash-out refinance, the borrower applies for a new mortgage for an amount that is more than what they currently owe. For example, someone who currently owes $100,000 on a mortgage for a house worth $200,000 can apply for a cash-out refinance of $150,000. The first $100,000 pays off the balance on their existing mortgage. They can use the remaining $50,000 to pay off other debts.

While consolidating debt by refinancing or combining two mortgages into one can be the right option for some borrowers, there are some risks to consider. For instance, when you use the proceeds from a consolidation refinance to pay off unsecured debt, such as a credit card, you are putting your home on the line. If you have difficulty repaying the new mortgage, you could lose your home.

Mortgage consolidation isn’t free, either. Just as you paid closing costs when you purchased the home initially, you’ll need to pay more fees when you refinance.

Should You Combine Two Mortgages Into One?

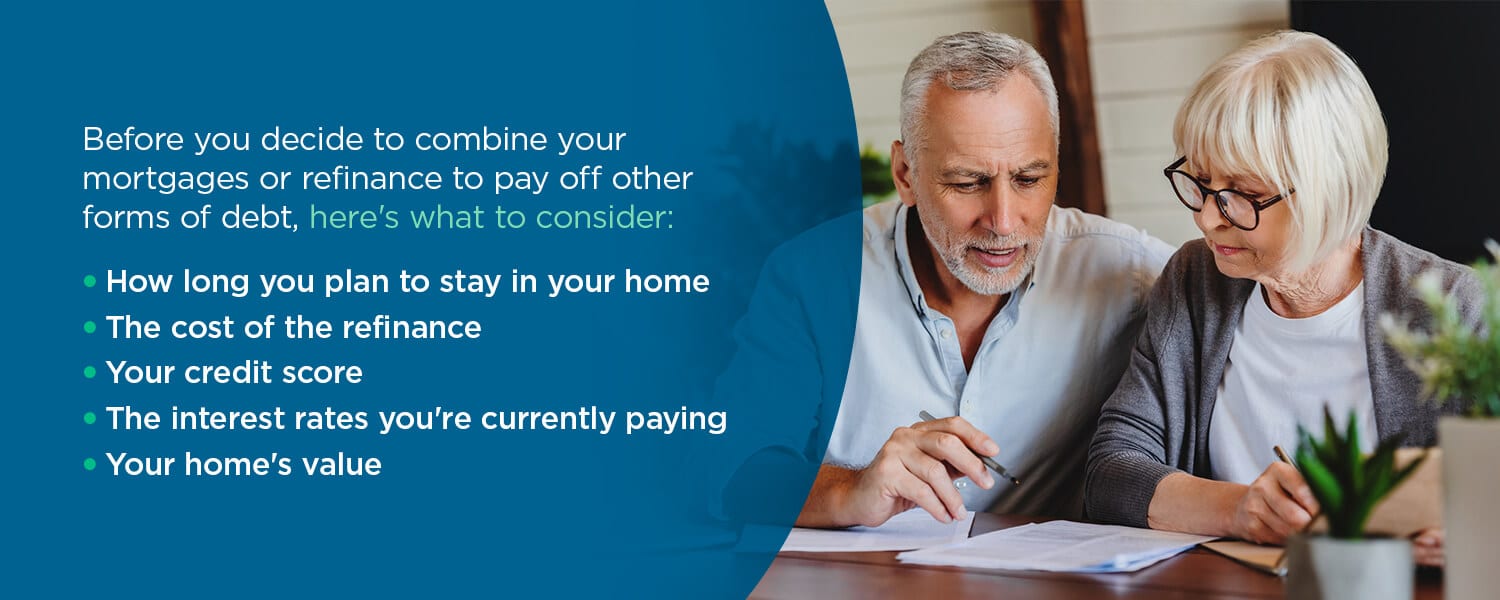

Before you decide to combine your mortgages or refinance to pay off other forms of debt, here’s what to consider:

- How long you plan to stay in your home: The longer you plan to live in your current home, the more sense a consolidation refinance makes. If you refinance now but plan on moving in a year or two, you risk not recouping the refinance costs. Before choosing to refinance and consolidate, use a calculator to figure out your breakeven point and to see how much you could save if you go forward.

- The cost of the refinance: Another thing to consider when consolidating home loans is the total cost of the refinance. Exact costs vary based on the location and your home’s value, but they tend to average around $5,000. You’ll need to have that money upfront when you close on the loan unless you decide to roll it into the interest rate you pay, which might defeat the purpose of refinancing.

- Your credit score: Just as the lender checked your credit before approving you for the first mortgage, they’ll check your credit again when you refinance. The higher your score, the better the terms you’ll get on a refinance loan. If you’ve had difficulty paying your loans since taking out your first mortgage, that can affect your eligibility for the best terms on a consolidation loan. Depending on your situation, you might need to focus on improving your score before you can refinance. You can improve your score by reducing your total debt and by getting current on your payments if you’ve fallen behind.

- The interest rates you’re currently paying: It’s a good idea to be sure you’ll actually save money by consolidating your mortgages or other debts. Take a look at the interest rates on your existing loans and compare them to the rates a lender is likely to offer you. Ideally, the new rates will be lower than your current rates. If not, consolidation probably doesn’t make sense for you.

- Your home’s value: The value of your home determines how much you can borrow and whether you can borrow enough to pay off your other debts. Ideally, your home will have increased in value since you bought it, meaning you owe significantly less on it than it’s worth. For consolidation to work, the home’s value must be more than what you owe on the primary mortgage and what you owe on a second mortgage or other debts. An appraisal is part of the refinancing process. If the appraiser doesn’t value the house high enough, refinancing is off the table.

Keep in mind that other debt consolidation options don’t require you to refinance your mortgage. If you’re looking to get a better rate on high-interest credit card debt, you might be eligible for a balance transfer card with a 0% introductory rate. A consolidation loan that doesn’t involve merging your other debts with your home loan is another possibility.

[download_section]

How to Combine Two Mortgages

The process of consolidating your home loans or refinancing to consolidate other forms of debt will be very similar to getting a mortgage for the first time. Shop around for the best loan options and make sure you put your best application forward:

1. Review Your Refinance Options

Before you start the consolidation process, read up on the different refinancing options available. Generally, there are two categories of refinancing. The first is a rate and term refinance. When you apply for a rate and term refinance, you change either the interest rate or the length of the mortgage, or in some cases, both. You can take advantage of a lower interest rate, which usually means lower monthly payments.

If you change the term, you can either get lower monthly payments if you extend from a 15-year to a 30-year mortgage, or higher payments, if you switch from a 30-year to a 15-year loan. Usually, a rate and term loan won’t pay out enough for you to use it to consolidate multiple mortgages or other debts.

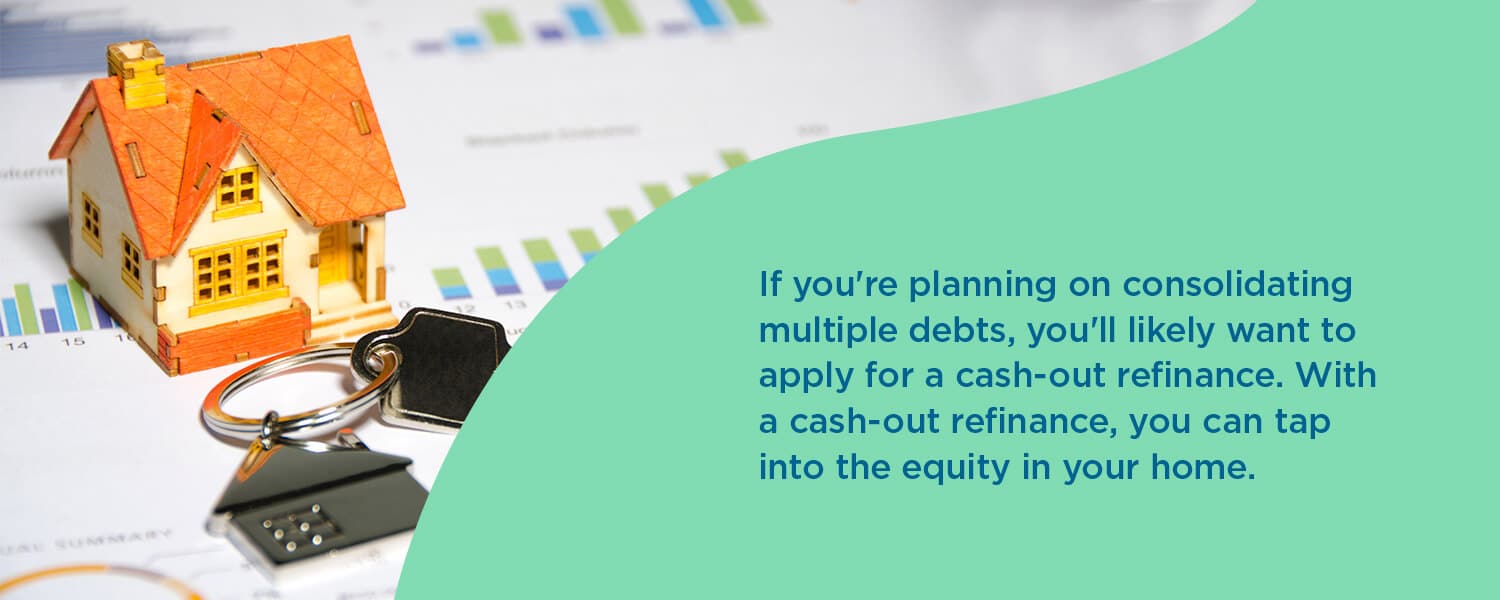

If you’re planning on consolidating multiple debts, you’ll likely want to apply for a cash-out refinance. With a cash-out refinance, you can tap into the equity in your home. The amount of a cash-out refinance is higher than what you owe on the current mortgage, so you can use the extra money to pay off other loans.

To get a cash-out to refinance, you need to have a certain amount of equity in the home. Usually, a lender won’t agree to lend you more than 80% of the home’s value. So if you currently owe 80% or more on your home — for example, you owe $180,000 on a home worth $200,000 — a cash-out refinance is most likely not an option.

2. Apply for the Refinance Loan

Once your credit is where you want it to be, you’ve chosen the type of loan you want and you’ve found a lender who’s giving you the best rate, it’s time to finalize the application. Applying for a refinancing or consolidation loan may be a lot like applying for a mortgage the first time around. Your lender will want to see proof of income, assets and employment. They are likely to call you to verify information or to ask for additional documentation as needed. They might also call your employer to confirm your employment history.

3. Get an Appraisal

An appraisal is usually part of the refinancing process. During it, a third-party appraiser will visit your home to determine how much it is worth. The appraiser will look at the price of similar homes that sold recently and evaluate your home’s overall condition. Ideally, they will determine that your home is worth much more than you plan to borrow. If the home appraises low, you might not be able to refinance.

4. Close on the New Loan

The closing process when you refinance is also similar to the closing process when you got your mortgage the first time around. You’ll need to bring a cashier’s check or wire the closing costs to the lender. You’ll sign a lot of documents, agreeing to the new mortgage.

If you’ve got a cash-out refinance at the end of the process, your lender might present you with a check for the amount that’s above what you owed on the first mortgage. You can use the money to pay off a home equity loan, line of credit or otherwise pay off your debt. Now, you’ll just have the single mortgage payment to focus on monthly.

Benefits of a Consolidated Home Mortgage

Consolidating mortgages or other loans can seem like a lot of work. You might be wondering if it’s worth the time and effort. While everyone’s situation is different, there usually are several benefits to consolidating your mortgage, including:

1. Lower Interest Rate

Depending on when you took out your first mortgage and when you applied for a home equity loan or line of credit, you might be paying interest rates that are considerably higher than what’s available now.

For example, if you bought your home in September 2008, your interest rate might be hovering around 6%. If you got a home equity loan a decade later, in 2018, you might be paying a rate of around 4.5%. If you refinance in 2021, you can get a rate just under 3%, which will lower your interest costs on both loans considerably and can help you pay off the loans more quickly.

If you’re going to consolidate other forms of debt with higher rates, you stand to save even more. For example, a credit card might charge 20% or so in interest. Using a cash-out refinance to pay off that card and getting a rate around 3% or 4% can mean significant savings on your part.

The change in interest rate doesn’t need to be dramatic to benefit you. Even a 1% change can mean major savings on your end when you refinance and consolidate your loans.

2. Switch From ARM to Fixed-Rate

Two types of interest rates are available when you take out a mortgage or home equity loan. A fixed interest rate stays the same throughout the loan’s term. If the rate is 3% on the first day, it’s 3% on the last day. A fixed-rate mortgage offers you predictability and stability.

An adjustable-rate mortgage has an interest rate that can change over time. Often, the rate is the same throughout an introductory period, such as five or seven years. When the introductory phase ends, the rate adjusts based on the market and current conditions. It can skyrocket, bringing your monthly payment up with it. The only way to get out of an adjustable rate is to refinance to a loan with a fixed rate.

There are some reasons to consider taking out a mortgage with an adjustable rate, such as a lower initial interest rate. Taking advantage of the lower rate initially, then refinancing just before it adjusts, can help you save money.

3. Shorter Loan Term

How long you have to pay back your mortgage influences a few factors. Shorter-term mortgages, such as a 15-year loan, often have lower interest rates than longer-term home loans. A lender takes on less risk when someone agrees to pay back their loan in 15 years versus 30 years.

The term of the mortgage also determines the monthly payment. A 15-year loan has a higher monthly payment than a 30-year loan since you’re paying the mortgage down in half the time. The advantage is that you pay less in interest, and you get out of debt sooner. If you can afford a higher monthly payment and want to be debt-free earlier, it can make sense to consolidate your loans in a mortgage with a shorter term.

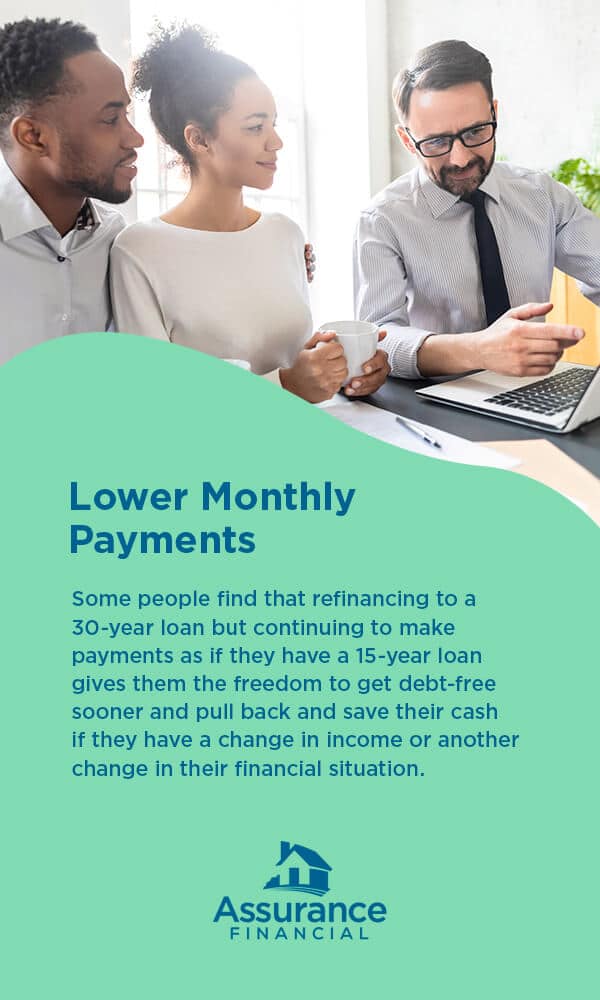

4. Lower Monthly Payments

It could be the case that you took out a 15-year mortgage and a home equity loan and now find the monthly payments to be a bit higher than you’re comfortable with. You’re not struggling to make the payments, but you would like some more wiggle room in your budget. In that situation, it can make sense to switch from a 15-year loan to a 30-year loan. You’ll have more time to pay back the mortgage and will end up paying more in the long run.

You’ll also have more cash in your bank account each month since you’ll owe less. You can use the savings to establish an emergency fund, save more for retirement or save for your children’s education. You also have the option of paying more toward your mortgage debt monthly.

Some people find that refinancing to a 30-year loan but continuing to make payments as if they have a 15-year loan gives them the freedom to get debt-free sooner and pull back and save their cash if they have a change in income or another change in their financial situation.

5. Simpler Payments

Variety might be the spice of life, but you really can’t put a price tag on simplicity. When you refinance your home loan and use the cash to consolidate your loans, you end up with one monthly payment. You don’t have to worry about juggling due dates or making sure all your bills get paid on time. You only have to make a single payment and only to one lender.

When you simplify your payments, you reduce the chance of missing bills, which can help you boost your credit. You also get more time in your schedule to focus on the things that matter to you.

Finally, simplifying your debt payments can help to improve your stress levels. You won’t have to worry about whether you scheduled a payment or missed a deadline. When you streamline your debt payments, you can focus more on other financial issues and goals, such as saving for the future.

6. Gets Rid of Private Mortgage Insurance

Depending on the type of home loan you have and how much you put down when you borrowed, you might have private mortgage insurance payments (PMI) to pay each month. If you have an FHA loan, those payments are for the life of the mortgage, meaning you can get rid of them if you refinance. Eliminating PMI can reduce your monthly payments and help you get out of debt sooner.

Refinance or Consolidate With Assurance Financial

Is a cash-out refinance right for you? If you’d like to consolidate a home equity loan and a primary mortgage or have other debts you’d like to roll into your mortgage payment, refinancing can be the right call. Assurance Financial makes it easy to see if refinancing is a good option for you. You can start the application process with Abby, our virtual assistant, in just 15 minutes. Apply today and take the first steps toward simplifying your financial life.

Linked Sources:

https://assurancemortgage.com/refinance-your-home/

https://assurancemortgage.com/calculators/should-i-refinance-my-mortgage/

https://myhome.freddiemac.com/refinancing/costs-of-refinancing.html