When you’re shopping for a home, you want to do as much as possible to show sellers you’re serious and make yourself stand out in a crowded field. That’s particularly true when you’re looking to buy in a seller’s market. In a seller’s market, there are more people trying to buy homes than properties available.

One way to make yourself stand out is to get a pre-approval from a lender. With a mortgage pre-approval letter in hand, you demonstrate to sellers that you’re ready to buy and likely have the loan to back you up.

Before you get a pre-approval, you might wonder about its impact on your credit score and report. However, for the most part, getting pre-approved will only help you. Read on to have your questions about pre-approval answered.

What Is a Pre-Approval?

A mortgage pre-approval is essentially a stamp of approval from a lender. It’s very similar to the process of applying for a mortgage loan. A lender will review your documents and history during the pre-approval process to determine your interest rate and how much you can comfortably borrow.

Mortgage pre-approval is sometimes confused with pre-qualification, but there are distinct differences. A pre-qualification is generally less serious than a pre-approval. It’s like a rough sketch. When pre-qualifying you, a lender might look at your income and ask about your credit history, but they won’t dig very deep.

A pre-qualification can be valuable when you’re in the early stages of home buying. For example, pre-qualification can give you some general guidance if you’re about to dip your toes in and aren’t sure how much you can afford to buy or if you’d even be eligible for a mortgage. It’s an estimate regarding what you can afford and whether you’re likely to qualify for a loan.

A pre-approval comes after the pre-qualification once you know that you want to buy a home and are ready to jump in with a real estate agent. To get a pre-approval, you need to provide the lender with some documentation and evidence of your financial status.

During the pre-approval process, a lender will look at documents that verify your income, such as income tax returns or paystubs. They might also ask you to provide copies of bank statements to show how much money you have available and what you’ve saved for a down payment.

Crucially, a pre-approval involves a credit check. The lender will review your credit history during the credit check, looking for concerns such as missing or late payments. They might also look for bankruptcies and other signs that you’ve had trouble with loans in the past. They’ll get your credit score, too.

A pre-approval doesn’t always guarantee that you’ll get final approval for a mortgage. There can be circumstances that stand in the way of getting approved, such as an issue with the property’s title or a home appraised at less than the sale price. Changes in your financial situation between the time you get pre-approved and when you’re ready to apply for the actual mortgage can also affect the process.

Why Get a Pre-Approval?

Although a pre-approval isn’t a 100% guarantee that you’ll get a mortgage, it’s an excellent first step. It makes you look more attractive as a buyer to sellers. When someone is selling a property, they want to work with buyers who will provide the smoothest experience possible. Someone who’s got a mortgage lender behind them and who’s taken the time to go through the pre-approval process is more likely to commit to the home buying process.

Getting pre-approved also helps you narrow down your options. For example, a lender might pre-approve you for a $250,000 loan. With that information in hand, you know where you can set your budget.

Going through the pre-approval process also allows you to shop around and see what different lenders can offer you. You’ll be more likely to get a mortgage that works for your budget and financial situation if you have a chance to shop around.

How to Get Pre-Approved

One way to look at the pre-approval process is as a dress rehearsal for an actual mortgage application. You’ll need to give the lender certain documents, and they’ll review your financial information to determine the following:

- How much you can borrow

- What interest rate you’ll pay

- The mortgage term

To start the pre-approval process, your lender will most likely ask you to provide:

- Proof of income: Depending on how you earn income, your proof can be paystubs or tax returns. Self-employed individuals usually provide tax returns, while employed people can provide paystubs.

- Proof of assets: A lender might also request bank statements or other documents that verify how much you have saved or invested. Some lenders will only verify that you have enough for the down payment and closing costs. Others will want to see evidence of cash reserves and savings beyond what you need for closing costs and down payment.

- Employment verification: You will most likely need to verify that you’re still employed or still have a source of income. You can ask your employer for an employment letter, or the lender might call your employer to see if you’re still working there.

- Identification: A lender will need to verify your identity to run the credit check and confirm that you’re who you claim to be. Besides providing your social security number, you’ll also have to provide a photo ID, such as a passport or driver’s license.

- Information about other debts: Your other debt obligations can affect whether you get approved for a mortgage or not or how much you’re approved to borrow. A lender will likely ask you to provide information about any other debts, including the monthly payments and the total amount owed.

Once you’ve given all your details to the lender, they’ll run your credit score and review the information to determine a maximum loan amount and your interest rate. The higher your income and credit score, the more you can borrow and the lower your rate. Whether it’s 15 or 30-years, the length of your mortgage term will also affect your loan amount and interest rate.

If you get the pre-approval, the lender will give you a letter detailing how much you can borrow and the interest rate. When you make an offer on a home, you submit a copy of the pre-approval letter to the seller.

Usually, a pre-approval locks in the interest rate for a limited period, such as 90 days. That means you should find and buy a house within that period to get the rate. Otherwise, you might have to start the pre-approval process over again.

What’s in Your Credit Score?

Your credit score plays a significant role during the mortgage approval process. Your score affects the type of mortgage you qualify for and the interest rate you pay. Your score can affect whether you get approved or not. Some mortgage programs, such as FHA loans, are designed to help borrowers who might not have the credit score needed to qualify for a conventional loan.

The companies that calculate credit scores use secret formulas to come up with the three-digit numbers. While the companies keep their exact formulas under wraps, they have detailed the factors that contribute to your overall score:

- Total amount of debt: The total amount is how much you’ve borrowed at the moment.

- Payment history: Your payment history details whether you pay on time or have a history of paying 30 or more days late.

- Age of credit accounts: The age of your credit accounts refers to how long you’ve had a credit history, dating from the time you opened your first currently active credit account.

- Number and type of accounts: The number of accounts refers to how many credit cards or loans you have open. The type refers to whether those accounts are secured loans, credit cards or other types of unsecured loans.

- How much credit you use: How much credit you use refers to the amount you’ve borrowed compared to how much you can borrow. For example, you have a credit utilization ratio of 10% if you have a $1,000 balance on a credit card with a $10,000 limit.

- Recent credit applications: Recent credit applications refers to how many accounts you’ve applied for in the past couple of years. Any recent mortgage pre-approvals or credit card applications will show up here.

Each factor has a different impact on your score. For example, payment history typically has the most considerable effect, while credit applications and types of accounts have less of an impact.

Does Getting Pre-Approved Hurt Your Credit?

In short, yes, getting pre-approved for a mortgage can affect your credit score. But the impact is likely to be less than you expect and shouldn’t stand in the way of you getting final approval for a mortgage.

What Happens to Your Credit Score After a Pre-Approval

When a lender checks your credit for a mortgage pre-approval, they run a hard inquiry. A hard inquiry can cause your score to dip slightly. The impact on your credit will be minimal. The small credit score change after pre-approval won’t cause the lender to change their mind when it comes time to apply for a mortgage.

The drop is temporary. If you continue to pay your bills on time and are punctual with your mortgage payments once you receive one, your credit score will soon recover.

What Are Different Types of Credit Inquiries?

There are two ways of checking credit. A lender might run a soft or hard inquiry, depending on the situation. Each type of credit inquiry has a different impact on your credit score.

Hard Credit Inquiries

When lenders perform the pre-approval process, they run a hard credit inquiry. A hard credit inquiry is like a large flag that tells other lenders you’re in the process of applying for a loan.

A hard credit inquiry affects your credit score, as it signals that you’ve recently applied for credit. If you have several new credit applications on your credit report within a short period, such as within a few months, a lender might see that as a red flag or a sign that you’re having financial difficulties. Usually, the more hard inquiries you have in a limited period, the more significant the impact on your score.

For that reason, it’s usually recommended that you do not apply for a car loan, credit card or other types of loan while you’re applying for a mortgage.

It’s important to understand that although a hard inquiry often causes a score to drop, hard inquiries in and of themselves aren’t necessarily bad things. You need a hard inquiry to get any type of loan.

Soft Credit Inquiries

A soft credit inquiry doesn’t have an impact on your credit score. A soft inquiry occurs whenever you check your credit report. A lender won’t be able to see that you’ve run a credit check on yourself.

If a lender wants to pre-approve you for a credit card, they’ll also run a soft inquiry on your credit. The lender uses the information they get to put together a credit card pre-approval offer to send you. Other examples of a soft inquiry include when a utility company checks your credit before opening a new account or when an employer runs a credit screening before hiring you.

Does Getting Multiple Pre-Approvals Hurt Your Credit Score?

Shopping around for a mortgage is often recommended to people looking to buy a home. But, if getting pre-approved for a mortgage requires a hard inquiry on your credit report, won’t getting several pre-approvals create several hard inquiries, increasing the damage to your credit score?

Fortunately, the impact several pre-approvals have on your credit score is minimal. When you get pre-approvals for multiple lenders, the credit bureaus typically lump them together as a single hard inquiry. Bureaus understand it’s common to shop for a mortgage. Borrowers who get pre-approvals from multiple lenders aren’t penalized for trying to get the best offer possible.

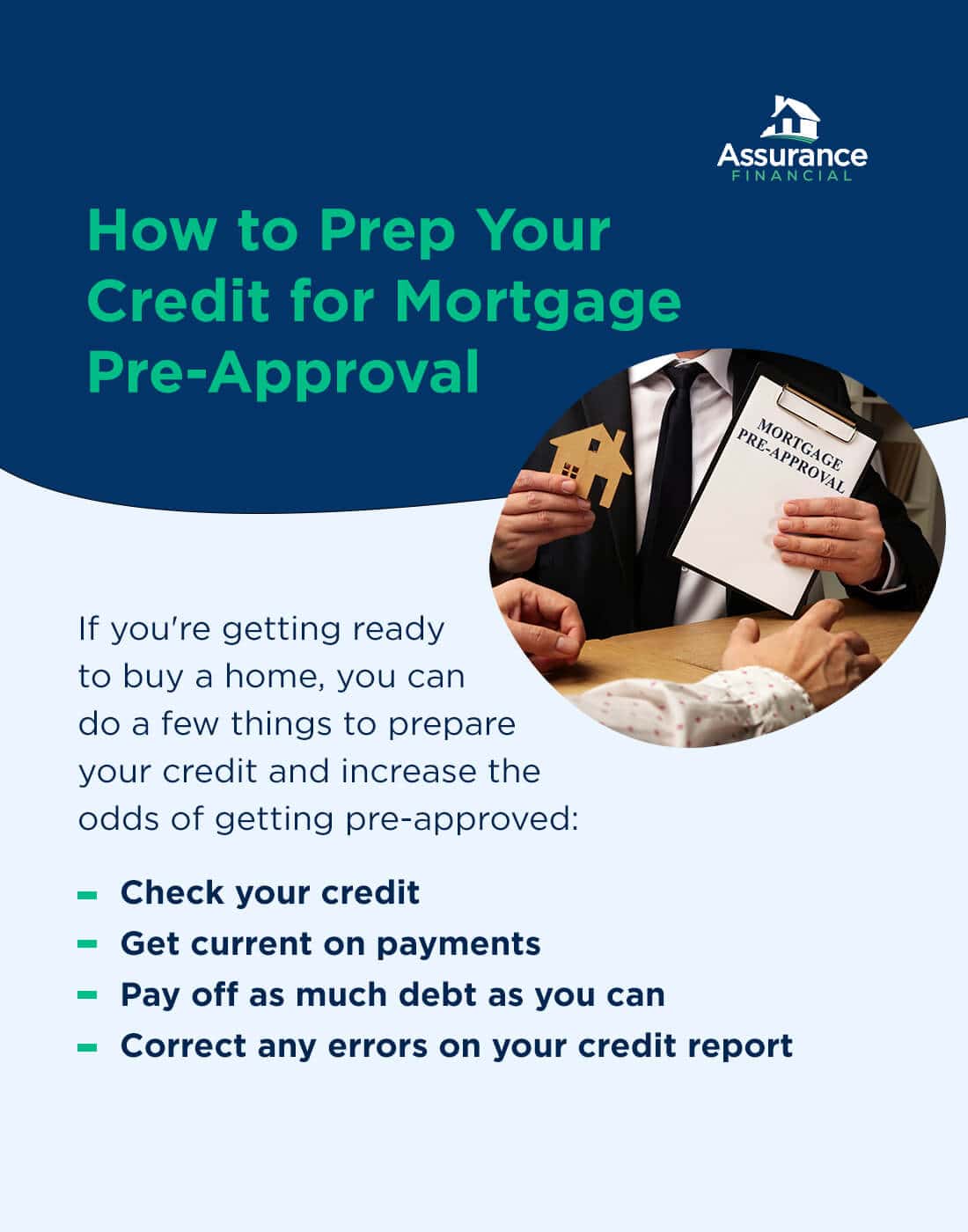

How to Prep Your Credit for Mortgage Pre-Approval

If you’re getting ready to buy a home, you can do a few things to prepare your credit and increase the odds of getting pre-approved:

- Check your credit: Checking your credit creates a soft inquiry, which doesn’t affect your score. It’s a good idea to check your credit for at least several months or even up to a full year before you start looking for homes. Checking in advance gives you plenty of time to take action to improve your history and score if needed.

- Get current on payments: If you have a history of paying late on any of your loans, make an effort to get current on your payments. Pay off any late fees and back-due amounts. Then, commit to paying your loans by the due date every month. You can set up a payment reminder or schedule automatic payments to ensure you don’t forget.

- Pay off as much debt as you can: How much debt you have or the amount of debt compared to your income can affect your credit score and eligibility for a mortgage. If you have a lot of debt, try to pay some off before applying for a home loan.

- Correct any errors on your credit report: The credit bureaus can make mistakes. Let the agency know if you notice anything strange or incorrect on your credit report. Common errors include accounts that belong to someone else — usually someone with a similar name — or accounts you’ve closed still showing as open. </span >In some cases, errors in your credit report can be a sign of identity theft or fraud.

[download_section]

Do’s and Don’ts After Getting a Mortgage Pre-Approval

Once you have the pre-approval, you’re ready to roll and can put in an offer on a home. Remember that getting pre-approved doesn’t mean you’ll necessarily get fully approved for a mortgage. Certain actions between the pre-approval and final approval can affect your credit and interfere with the mortgage process. Here’s what to do and not do when you’re in the home stretch of getting a mortgage.

Do: Continue to Pay Off Other Debts

If you have other debts, keep making payments on them while looking for a home and going through the mortgage process. Any change in your payment history can impact your credit score, causing a lender to reconsider approving you for a mortgage.

Don’t: Apply for New Credit

While credit bureaus group several mortgage pre-approvals together and count them as a single hard inquiry, the bureaus won’t group other loan applications with your mortgage pre-approval. Several other hard inquiries can affect your credit score, such as a credit card application or personal loan application.

Applying for new credit while shopping for a home can also raise alarm bells for your mortgage lender. They might wonder why you’re applying for multiple loans while you’re trying to buy a home. To keep your lender calm and increase your odds of approval for a home loan, wait until after closing to apply for other types of credit.

Do: Shop for a Home

Pre-approvals don’t last forever, so it’s a good idea to get out there and start looking for your dream home once you have the pre-approval letter in hand. Usually, your pre-approval will be valid for several months, so don’t panic if you don’t find your home immediately.

Contact your lender if you don’t find the right home before the pre-approval expires. Some are willing to extend the offer beyond the initial period without making you go through the entire credit check and application process again.

Don’t: Make Other Big Purchases

If possible, try not to make big purchases between getting pre-approved, putting an offer in on a home and closing. Buying a new car or new furniture can affect your cash reserves, which might make a lender reconsider approving you for a mortgage. Using a credit card to buy furniture will increase the amount of debt used, affecting your credit score.

It’s better to wait until you’ve closed on your home to purchase furnishing for it or before making any other large purchases.

Do: Keep Your Lender Up-to-Date on Any Life Changes

Depending on how long it takes to find a home and put in an offer, you might experience some life changes between getting pre-approved and closing on your home. Let your lender know whether it’s a change in income, a new family member or getting an inheritance. Changes in your financial status can affect your mortgage eligibility.

Don’t: Quit or Change Jobs

A history of steady employment is very attractive to mortgage lenders, as it suggests that you’ll continue to have the means to pay your mortgage for years to come. While your job status might be out of your control in some cases, if possible, wait until you’ve closed on the home before quitting your current gig or finding a new job.

Becoming unemployed before you have final mortgage approval affects the process. The same is true if you change jobs and accept a lower-paying position.

Get Pre-Approved With Assurance Financial Today

The first step to getting a mortgage is getting pre-approved. Apply today or contact a loan officer.

Linked Sources:

- https://assurancemortgage.com/buyers-vs-sellers-market/

- https://assurancemortgage.com/15-vs-30-year-mortgages/

- https://assurancemortgage.com/important-credit-score-for-home-loan/

- https://assurancemortgage.com/fha-loans/

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/how-to-get-a-mortgage-loan/

- https://assurancemortgage.com/apply/