To get certain types of loans, such as a mortgage, you need to have a good or excellent credit score and a strong credit report to qualify for the best terms possible. But it can be difficult to build a good credit history or establish your credit score without having any loans.

If you’re wondering how you can build your credit score, the good news is that there are several options available to help you establish credit and get on the path toward homeownership. Learn more about what mortgage lenders are looking for in a credit report and what you can do to make your credit score and history look attractive.

Table of Contents

- Credit 101

- How to Build Credit to Get a House

- How to Practice Good Credit Habits

- Benefits of Building Credit

- Boost Your Credit With Assurance Financial

Credit 101

Credit lets you borrow money to purchase items you can’t afford to pay for in full upfront. For example, it allows people to pay for cars, education and houses. When a lender extends credit to you, they expect you to pay back what you borrow, plus interest, usually on a set schedule. Lenders who issue credit can’t simply trust their gut when deciding whether or not to lend money to a person. They usually check that person’s credit report to see whether they have a history of paying on time or missed payments.

The longer a person’s credit history, the more information a lender has to go on. For example, if someone opened their first credit card 20 years ago, the lender can see whether they have made consistent and timely payments over the years. The more varied someone’s credit history is, the more the lender has to judge whether or not an individual would be able to handle repaying another loan. The amount a person has borrowed also plays a part in influencing a lender’s decision about whether or not to give that person another loan.

While it can be relatively easy to get approval for some types of loans, others have more stringent lending requirements and might require a person to have a stronger credit history. If buying a house is in your future plans, it can be worthwhile to focus on building credit — making you a more attractive borrower to lenders and helping you get the best terms and conditions possible on your home loan.

How to Build Credit to Get a House

If you’re starting from scratch and don’t have a credit history at all, you have several options for building up your credit and making yourself a more attractive borrower to lenders.

1. Consider a Secured Loan

Several types of loans are available for people who want to improve or establish their credit. Both types require you to make a deposit that acts as collateral, but how the loans go about doing that is slightly different.

For example, you first need to put down a deposit if you open a secured credit card. The deposit acts as the collateral on the card, reducing the risk to the lender if you can’t make payments on the card. Usually, the amount of your deposit serves as the card’s limit. If you open a card with a security deposit of $500, you can charge up to $500 on the card. Once you pay off the full balance, you can charge up to $500 once again.

One thing to understand about a secured credit card is that your deposit won’t count toward your payments on the card. If you use the card to purchase things, you need to pay it by the due date to avoid late fees and other penalties.

[download_section]

Secured credit cards tend to have higher interest rates than other types of credit cards, making it worth your while to pay your balance in full before the due date rather than pay only the minimums. In addition, many cards will convert to an unsecured version after a year or so, meaning you get the amount of your deposit back. Depending on the terms of the credit card, you might need to ask the card company to convert the card to an unsecured one, or the conversion might be automatic.

Another option for people with limited credit histories is a credit-builder loan. Credit-builder loans work differently from other loan types. When a person applies for a credit-builder loan, a lender deposits the amount of the loan, such as $1,000, into an account. The borrower then makes payments to the lender, such as $75 per month, plus interest. When the borrower makes payments, the lender transfers that amount of the loan into the borrower’s account. The lender also reports the borrower’s payments to the three credit reporting bureaus, helping people build their credit to purchase a home.

A study from the Consumer Financial Protection Bureau found that nearly one-quarter of people who didn’t previously have credit were able to establish a credit history after they got a credit-builder loan. The average credit score increased by 60 points after individuals opened a credit-builder loan.

2. Get a Credit Card

You might not have to apply for a secured credit card to start building credit. Several “starter” cards are available that let you build your credit history without putting down a deposit. Often, starter cards are targeted at students, meaning you might have to be in college to qualify for the card. There are some cards that are designed for adults who aren’t in school, though.

When you get your first credit card, keep in mind that it might have a high interest rate and a low credit limit. A credit card company might be willing to issue you a card, but it is also likely to take steps to minimize its risks. A higher-than-average interest rate is one way to do so, as is limiting the amount you can borrow. There are a few things you can do to make the most of your new credit card:

- Only buy things you can afford: Use your card for purchases you would make anyway, such as groceries. That way, you won’t run the risk of charging more than you can afford to pay back on the card.

- Pay the balance in full each month: Pay the full amount of the balance by the due date to avoid having to pay interest on the things you’ve charged. Paying in full by the due date also helps you avoid late fees and keeps your payment history positive.

- Keep spending on the card to less than 10% of the limit:How much you’ve borrowed compared to your credit limit affects your credit score and history. To boost your score, keep your spending on the card below 10% of the limit. That means if you have a $1,000 limit, don’t charge more than $100 at a time.

3. Get Installment Loans

Your credit mix plays a part in determining your credit score. The more varied the history on your credit report, the more reliable you might appear as a borrower. Along with considering revolving credit in the form of credit cards, it’s a good idea to add an installment loan or two to your credit mix. While revolving loans let you pay off your balance and borrow more, installment loans are issued in a lump sum. You then pay them back with interest in monthly installments. How long it takes to repay the loan depends on its term.

A mortgage is an example of an installment loan, as are student loans and car loans. If you’re looking to build credit, getting a student loan or car loan is likely going to be easier than getting a mortgage. Some types of student loans, notably federal student loans, don’t require a credit check first, making them easy to get, even if you have no credit at all. Some car loans are also available to people with minimal credit histories.

As with any type of loan, it’s important you make sure you can repay your installment loan based on its terms. You can take out several student loans without a credit check and borrow thousands of dollars to pay for school, but for the sake of your future credit, it’s important you can afford the monthly payments on those loans after you graduate.

If you’re considering a car loan, also be sure you can afford the monthly payment. You might consider making a larger down payment or buying a cheaper car to be absolutely certain you’ll be able to repay the loan without paying late or missing payments.

4. Ask Someone to Be a Co-Signer for You

If you’re having difficulty getting approved for a loan or credit card, one option is to find someone who can be a co-signer. A co-signer is usually someone with an established history of good credit, such as a parent, spouse or older sibling. When they co-sign a loan with you, they agree to take on responsibility for it. The loan will appear on their credit report, and they will be expected to pay it if you stop making payments or otherwise fall behind.

Being a co-signer is a major act of trust on the part of the person who co-signs. If you fall behind on payments, their credit is on the line, too. Before you ask someone to co-sign for you, be clear about your plans for the loan. Your co-signer might want to set up rules about the repayment process or otherwise verify you can make the payments. Good communication is key to protecting each person’s credit and preserving your relationship.

A slightly less risky option for a person with established credit is to add you as an authorized user on an existing account, such as a credit card. Some credit cards let account holders add others as authorized users, meaning a person gets a credit card in their name and is put on the account. The authorized user doesn’t own the account and isn’t fully responsible for making payments.

In many cases, the credit card appears on the authorized user’s credit report, helping them establish credit. You don’t have to use the card you’re an authorized user on. Simply having it appear on your report can be enough to improve or establish credit. The trick is to make sure the person who owns the card pays it as agreed and doesn’t pay late.

5. Make Sure Your Loans Get Reported

Three credit reporting bureaus exist that compile all the details about your loans and credit card accounts. Mortgage lenders use the information on the credit bureau’s reports to calculate your credit score. For an account to “count” toward your score, it needs to show up on your credit report.

For the most part, credit card companies and lenders will report your information to the appropriate credit bureaus. But it’s still a good idea to double-check and make sure your account details are going to show up on your credit history. If you’re completely new to building credit, another option is to have your rental payments and utility bills show on your reports. Some lenders will use that information when making a decision about you, and others won’t. If you have a good history of paying your rent and utility bills on time, it can be a useful thing to have show up on your credit report.

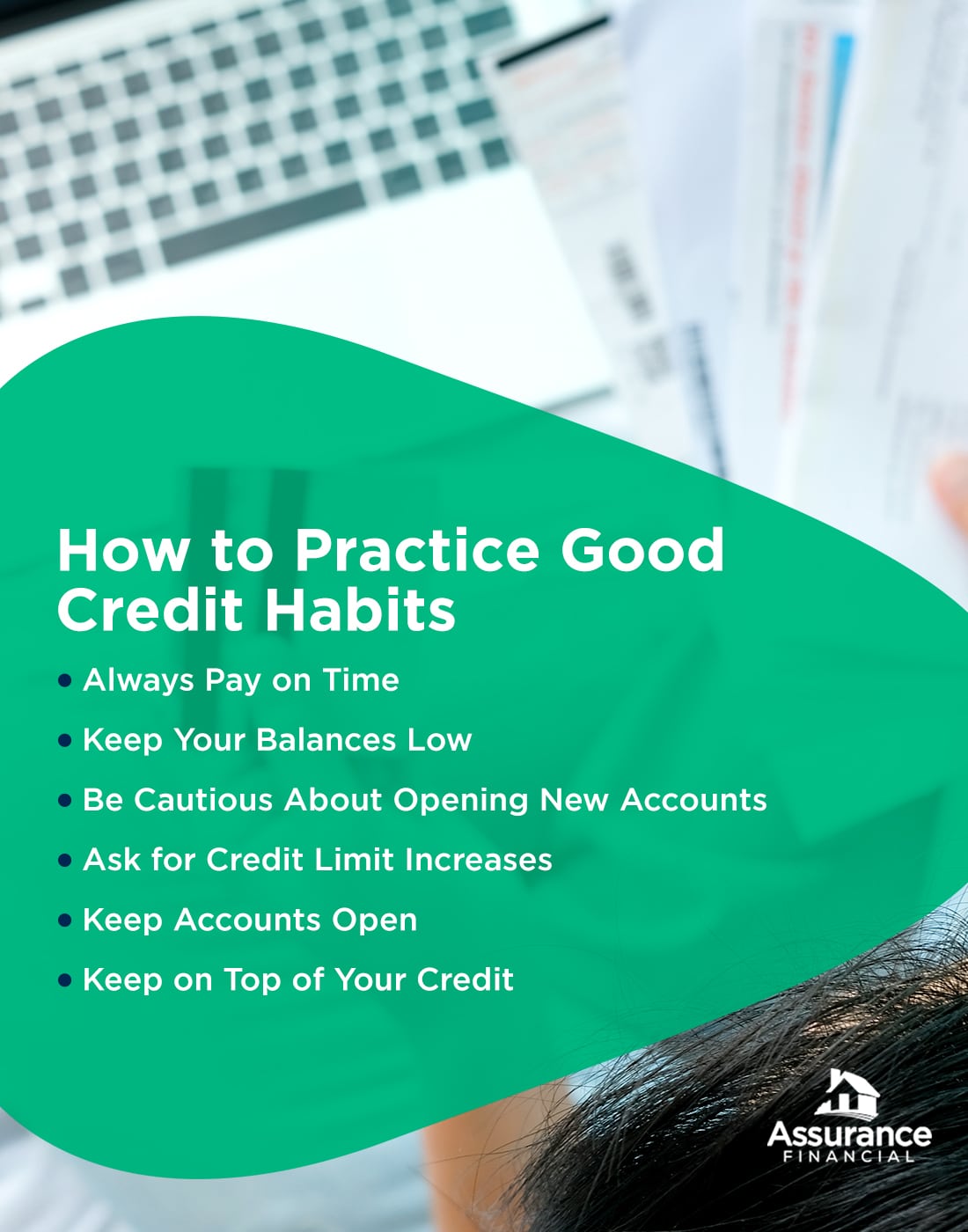

How to Practice Good Credit Habits

After you’ve established a credit history, there are some best practices to follow to help keep your score high and make you an attractive borrower to lenders. Here’s what you can do to build and boost your credit:

1. Always Pay on Time

Your payment history makes up 35% of your credit score, making it the most important factor when it comes to determining your credit. Make sure you always pay your bills on or before the due date and always pay at least the minimum owed. You can pay more than the minimum if you prefer. In fact, paying as much as you can is also good for your credit, as it helps to reduce the total amount you owe.

If you’re worried about missing payments or paying late, you have a few options. You can set up calendar reminders so you get a notification just before the due date. Another option is to automate your payments using a bill-paying service. Some credit cards let you set up automatic payments, so your cards get paid off each month without you having to check a calendar.

2. Keep Your Balances Low

The amount you owe also plays a big part in determining your credit score. The less you owe, particularly in comparison to the amount you can borrow, the better your score. Even if you have a high limit on your credit card, keep your balance well below it. It’s easier to repay your debts when you don’t borrow too much. You also look more reliable to lenders when your balances stay low.

3. Be Cautious About Opening New Accounts

Although you need to have credit accounts to establish a credit history and start building your score, it’s possible to have too much of a good thing. New credit affects your score, and every time you open a new account, your score drops a bit. If you go out to the mall and open several new store credit cards in a day, that can have a notable impact on your credit. Opening several new credit cards at once can be a red flag for a lender. They might look at your new accounts and wonder if you’re experiencing financial difficulties, which would make it challenging for you to repay a new loan.

If you’re in the process of applying for a mortgage, it’s critical you avoid opening new accounts, at least until you have final approval on the mortgage and have closed on your home. Opening a new credit card or taking out a car loan while your mortgage is in the underwriting process can sound like a warning bell to the lender, causing them to press pause on the proceedings.

4. Ask for Credit Limit Increases

Your credit utilization ratio affects your credit score. The ratio compares how much credit you have available vs. how much you have used. For example, if you have a credit card with a $1,000 limit and a balance of $100, your credit utilization ratio is 10%. The lower the ratio, the better for your credit. Keeping your balances low is one way to keep your ratio low. Another way is to increase your credit limit. For instance, you can ask the credit card company to raise your $1,000 limit to $2,000.

Credit card companies might be willing to increase your limit in several cases. If you have a history of paying on time, the company might see you as a lower-risk borrower and agree to increase your limit. An improvement in your credit score or an increase in your household income can also convince a credit card company that you’re a good candidate for a limit increase.

5. Keep Accounts Open

The longer your credit history is, the better it looks to lenders. A person with a 20-year history has more to show than someone with a five-year history. When possible, keep your credit accounts open to maximize the length of your history. For example, if you have a credit card that you no longer use, it’s still a good idea to keep the account open.

Another reason to keep credit card accounts open is that doing so helps your credit utilization ratio. If you have three credit cards that each have a $5,000 limit, your available credit is $15,000. Close one of those cards, and your available credit drops to $10,000.

6. Keep on Top of Your Credit

Everyone makes mistakes, including the credit reporting agencies. Whether you plan on applying for a mortgage soon or in the distant future, it’s a good idea to keep a close eye on your credit reports, so you can detect and fix any issues that come up. Possible mistakes include incorrectly reported payments, accounts that don’t belong to you and outdated information. If you see a mistake on your report, you can let the credit bureau know, and it will take action to correct it.

The Benefits of Building Credit

Having a solid credit history can help you in many areas. With a strong credit score, you can get the best rates on a mortgage or construction loan. Your credit also plays a role in helping you qualify for other loans and can let you get a better rate on insurance. Some employers also check credit when making hiring decisions.

That can mean the sooner you start building credit, the better. Even if buying a house seems like it’s years in the future, laying the groundwork today could mean a lower interest rate and better terms later on.

Boost Your Credit With a Mortgage From Assurance Financial

When you buy a home, getting a mortgage could help your credit. Once you’re approved for the home loan and make regular payments on it, you’re likely to see your score improve. Assurance Financial has simplified the mortgage application process, making it easier for you to become a homeowner and start living your dreams. Start your application with us online today.

Linked Sources:

- https://files.consumerfinance.gov/f/documents/cfpb_targeting-credit-builder-loans_report_2020-07.pdf

- https://www.myfico.com/credit-education/whats-in-your-credit-score

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/how-to-get-a-mortgage-loan/

- https://assurancemortgage.com/important-credit-score-home-loan/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/credit-score-determined