Key Takeaways

- FHA loans are government-insured mortgages created in 1934, requiring as little as 3.5% down with credit scores over 580, or 10% down for scores 500-579, making them ideal for first-time buyers and people with imperfect credit.

- However, mortgage insurance (1.75% upfront plus ongoing monthly payments) is required for the entire loan term and rates are higher than conventional loans.

- Must-wait periods apply: 1-2 years after bankruptcy or 3 years after foreclosure.

You may have heard about FHA loans but wondered what they were. Federal Housing Administration loans help people buy houses when they may not be able to borrow enough through other means. This article covers what you need to know about who can use these types of loans and what you need for the FHA approval process. Get the answers to all your FHA loans questions here.

What Is an FHA Loan and Why Does It Exist?

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA). The FHA was created in 1934 as a result of the National Housing Act. This division of the government was established to increase home construction, reduce unemployment and operate various loan insurance programs.

The FHA is not a loan lender, nor does it plan or build houses. Instead, it acts as the insurer on thousands of loans for Americans who might not otherwise be able to afford or qualify for a home loan. Since the FHA is not a mortgage lender, only approved lenders provide these loans.

Pros and Cons of FHA Loans?

Like all loans, you will have benefits and drawbacks when you get an FHA loan. Before deciding if you should apply, weigh the pros and cons to see how well you can accept the negative aspects of the loan in light of the positive side of having one of these means of borrowing money for your home.

1. Pros

Many people look for FHA loans because they allow those with less-than-perfect credit or first-time buyers to become homeowners. Compared to other financing options, these allow lower down payments for the home. If you have moderately good credit, with a FICO score over 580, you may only pay 3.5 percent of the home’s value for a down payment. Scores below that will require a 10% down payment. This down payment is much lower than the traditional 20 percent needed by other home loans.

2. Cons

Unlike with conventional loans, borrowers with FHA loans pay for mortgage insurance to protect the lender from a loss if the borrower defaults on the loan. You must pay an insurance down payment followed by monthly payments.

The first part you pay will be the upfront mortgage payment premium, which is typically about 1.75 percent of the home’s price. If you cannot afford it immediately, you may be able to have it financed into your mortgage. After paying this amount, you will still need to pay toward the mortgage insurance each month.

Monthly payments come from an annual mortgage payment based on your home’s value and loan term. You will have lower monthly payments for shorter loan terms or for loans that cover less than 95 percent of the home’s value.

Compared to a conventional loan, where you only pay mortgage insurance until your home’s value builds up liquidity, you must pay FHA mortgage insurance, however, for as long as you make mortgage installments.

The FHA mortgage itself tends to have a higher interest rate compared to conventional loans, meaning you pay more for your home than if you had a traditional loan that required higher down payment.

Who Should Use an FHA Loan?

The FHA loan program offers a unique opportunity for those with less-than-perfect credit to get approved in situations they otherwise wouldn’t.

Minimum credit scores for FHA loans depend upon the type of loan the borrower needs. However, in general, to get a mortgage with a down payment of around 3.5 percent, the borrower will likely need a credit score of at least 580 or higher. Borrowers with scores between 500 and 579 are likely to need a down payment of at least 10 percent. Borrowers with credit scores under 500 are usually ineligible for FHA loans, but the FHA will make exceptions for people with “nontraditional credit history” or “insufficient credit.”

Due to the mortgage insurance on FHA loans, lenders can — and do — offer these loans at attractive interest rates. FHA guarantees 30-year fixed-rate mortgages with as little as 3.5 percent down payment — plus borrowers can apply a seller’s credit or family gift towards closing costs. And if you would prefer a loan with an adjustable-rate, our FHA adjustable-rate mortgages (ARMs) can help you get into the home of your dreams, with a low initial interest rate.

The FHA also has a unique loan program for borrowers who need some extra cash to complete repairs on their homes. The most notable advantage of these loans is that the loan amount is based upon the value of your home after you’ve finished your repairs rather than its current value.

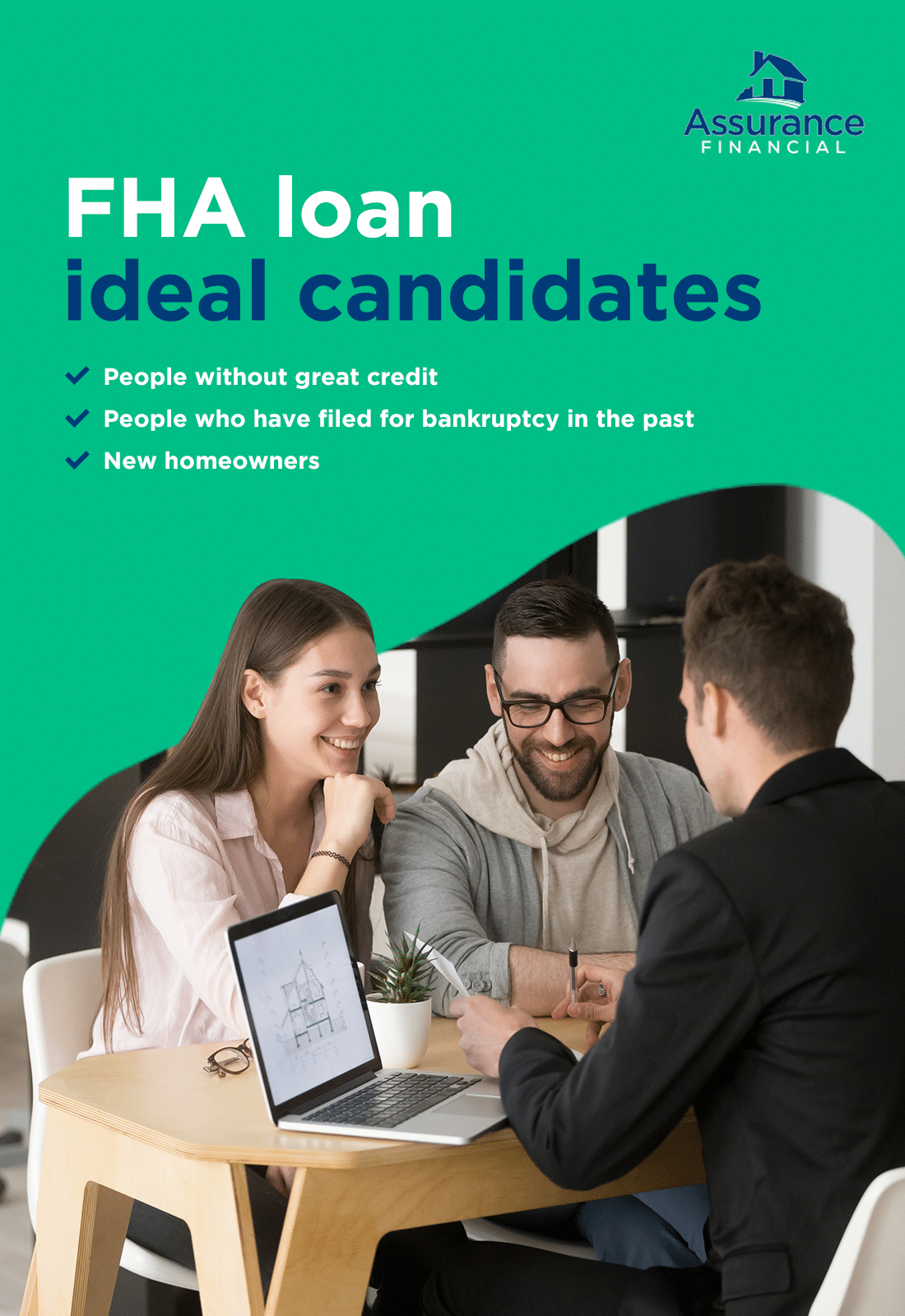

If you’re wondering who should apply for an FHA loan, the following groups are ideal candidates for these homebuying financial helpers.

- People without great credit: Most lenders look for credit scores higher than 660, but FHA loans allow approval with credit scores as low as 500. Your history will, however, affect your interest rate and down payment. FHA loans frequently have a smaller down payment — depending on your credit — to allow lower-income borrowers to enter the market.

- People who have filed for bankruptcy in the past: One of the most significant benefits of an FHA loan is its lenient approval process. By having the mortgage insured through the FHA, lenders are more likely to agree to a loan in situations they otherwise wouldn’t.

- New homeowners: For most new homebuyers, an FHA loan provides them with an accessible route to financing their homes. New homebuyers usually are just getting on their feet financially, and the low-down payments of an FHA loan are the most attractive benefit.

Who Guarantees FHA Loans?

To ensure homebuyers pay their loans, the FHA guarantees lenders full payment. For homebuyers, this means paying for mortgage insurance in addition to their home payments. The amount in insurance you pay depends on your loan term and the mortgage amount. For instance, your mortgage insurance premiums could range from 0.45 percent to 1.05 percent of the home’s cost after paying a 1.75 percent upfront premium.

By having the FHA guarantee, or insure, the loans, if you don’t pay the lender, the FHA offers several ways to avoid foreclosure.

- Home Affordable Refinance Program (HARP): With HARP, you can refinance to a stable mortgage if you’ve made regular payments on your existing loan and your home has lost value.

- Home Affordable Unemployment Program (UP): If you lose your job and cannot make your FHA loan payments, you may qualify for a suspension or reduction in payments for up to one year.

- Home Affordable Foreclosure Alternatives (HAFA): You may be able to transition to more affordable housing if you cannot pay for your current mortgage. Through HAFA, you may be able to get a deed-in-lieu of foreclosure or a short sale.

How Do You Get Started?

If you think you may qualify for an FHA loan, you need to gather some information to prove your income and employment. This data will help your lender determine if you qualify and what your rates and term will be.

1. Process of Buying a Home With an FHA Loan

You must show the lender that you have an established record of paying your bills. Gather this information to show your financial state when you talk to a lender:

- Bank accounts

- Tax returns from the last two years

- Pay stubs, 1099s and W-2s

- Bank statements

- Retirement account statements

- Credit card bills

- Investments

- Bankruptcy information

2. What Homes Qualify and How Much Can I Buy?

The FHA establishes baseline minimum and maximum amounts for loans each year. Some parts of the country may have different floors and ceilings, as the FHA calls these low and high amounts. In 2019, the floor was $314,827 while the ceiling was $729,525. Always talk to your lender about specific limits in your area.

FHA loans must accompany homes that an FHA appraiser has evaluated. The inspection sees if the home will meet Housing and Urban Development (HUD) standards. If the home does not adhere to HUD property guidelines, you will not be able to get an FHA loan for it.

3. What Are Limitations on the FHA Loan?

The FHA loan has some limitations. You will need to wait three years following a foreclosure before applying for an FHA loan. If you’ve ever filed for bankruptcy, you cannot apply for an FHA loan for one to two years, depending on the lender.

You also must have established employment for the last two years. If you have been self-employed, you must provide information from the last three years of your work to show employment.

4. What Is the FHA Loan Approval Process?

The process for loan approval happens after you submit the required information to the lender for pre-approval. Once you have this pre-approval, you can show the seller the information to indicate you will complete the process for a loan. You need to have found a home you want to purchase to complete the next form.

The next form is the Fannie Mae form 1003, also known as the Uniform Residential Loan Application. You need to include the address of the home you want to buy on this form in addition to supplying all necessary documents to show your income and employment.

With the address on file, the lender can send an FHA-approved home appraiser to assess the property’s value. If the property value falls within the mortgage requirements and the home meets HUD guidelines, you can move forward. If the home has a value too high or too low for the mortgage, you may not have it approved.

After the appraisal, your lender will examine your finances to determine if you qualify for the loan. Once you get the lender to underwrite your home loan, you have approval for your home loan and can continue to the closing process.

What Can I Use the Loan for? Can I Build a House With an FHA Loan?

When purchasing a new home with an FHA loan, you usually must have a pre-built home in mind that an appraiser will look at before you get loan approval. However, you can find FHA loans to allow you to build your home in addition to financing existing homes.

1. What Types of Homes Qualify for FHA Loans?

Homes that qualify for FHA loans must meet HUD home building guidelines. Additionally, the home value must be above the floor and under the ceiling loan amounts. These amounts change each year as the FHA evaluates changes in home prices across the country.

2. Can an FHA Loan Be Used for New Construction?

Loans insured by the FHA can cover new construction. The type of loan you will want for building a new home is a one-time close mortgage. For this option, you will not make mortgage payments until construction finishes, making it a better option for those without a lot of extra cash than taking out a construction loan and separate mortgage. Ceiling limits for built homes apply to FHA loans for construction, as well. Keep this in mind when working with the builder on specs for the home.

If you want new construction, the lender determines whether it will allow you to take a loan out for that home. For example, some lenders don’t allow one-time close mortgages for modular homes while others will only loan on modular homes and not site-built constructions. Always consult with your lender about specific home types the loan covers if you want to build a home with an FHA loan.

About Federal Housing Administration Mortgage Insurance

Mortgage insurance protects the lender if you cannot make your payments. If you have an FHA loan, you must have mortgage insurance. Even with a traditional home loan, if you cannot pay the standard 20 percent down payment, you will also need to pay for insurance.

1. What Are PMIs?

PMI stands for private mortgage insurance. This type of coverage differs in many ways from the mortgage insurance you take out for FHA loans. However, if you have a home loan, you will likely need PMI or FHA mortgage insurance.

First, PMIs must only last until you have paid off 20 percent of the home’s value through mortgage payments. At this point, you may request the PMI stop coverage. Some lenders, however, require PMI to last for a specified time, regardless of how much you have paid on your home. With FHA loans, you pay mortgage insurance for the entire life of the home loan.

The interest rates can differ between PMIs and FHA mortgage insurance. For PMIs, the interest rates typically range from 0.5 percent to 1 percent of the home’s value annually. FHA insurance requires a 1.75 percent of the home’s value for a down payment on the coverage plus an extra 0.45 percent to 1.05 percent annually.

If you can cover the 20 percent down payment to avoid paying the extra PMI, you will save money doing so. However, sometimes, life situations do not allow you to wait that long to save up such an amount. Because you may not have the cash on hand for a large down payment, you can still get a home loan if you are willing to pay the extra mortgage insurance with it.

2. Can You Pay That Off?

How you pay off your mortgage insurance depends on the type of coverage you have. Some lenders may allow you to end PMI coverage once your home has built enough equity. While you pay PMI, you have three methods of payment:

- Monthly payments: The most common way to pay off PMI is through monthly premiums added to your mortgage payment.

- Up front: You may need to pay the premium in full at closing. You may not get a refund if you refinance or move.

- Both: Some lenders may offer you to pay your PMI with both an up-front and monthly payments.

If you have FHA mortgage insurance, you must make both an upfront payment and monthly payments as long as you have the home loan, regardless of the equity in the home.

3. Can You Refinance Later?

If you choose to refinance into a conventional loan from an FHA loan, you can get rid of FHA mortgage insurance premiums. This method and selling your home are the only ways to rid yourself of FHA coverage premiums until you have paid off the home.

For PMIs, if you made an up-front payment and refinance your home, you may not be able to get your down payment back.

What Are the FHA Closing Costs?

After going through the approval process, you finally reach the closing. You will need to cover several closing costs to seal the deal, including your down payment on the house, mortgage premium and fees.

1. How Do FHA Closing Costs Differ From Conventional Loans?

Compared to conventional loans, FHA loans require an upfront mortgage insurance premium, and appraisal fees often cost $50 more. The upfront payment for your FHA mortgage insurance will equal 1.75 percent of the home’s value. Depending on the type of loan and lender, you may not need to make a mortgage insurance upfront payment with a conventional loan. Don’t worry if you cannot pay these closing costs. You have options to help.

2. Seller Assist and Other Sources to Help Cover Closing Costs

You have several sources of assistance with covering the closing costs. You may get seller assist, which has the seller pay your closing costs in return for you paying an equivalent amount on the home’s price.

If you have friends or family members who will gift you the down payment, you can use that to help with the FHA closing costs. You must have documentation showing the money was a gift without you intending to repay it. Account information from you and the giver also will prove the money came from the giver.

Some lenders also help you cover closing costs by offering higher home loan rates. Depending on how quickly you can pay off the home loan, you may benefit from these. Talk to your lender about your personal situation to see if this option will work for you.

[download_section]

Calculating Your FHA Loan Payment

When it comes to calculating your FHA loan payment, you must consider the length of the loan you have and the interest rate for both the loan and mortgage insurance. It’s best to talk to your lender to determine your loan rate and term.

Not all lenders offer the same interest rates for FHA home loans. You need to shop around to find the best rates from trusted lenders to get the loan you need.

Ready for the Next Step? Apply With Assurance Financial

Should you feel that it’s an appropriate time to become a homebuyer, but don’t have the best credit or have never bought a house before, let us know. You may qualify for an FHA loan. If you think you may be a candidate for an FHA loan, contact us at Assurance Financial. Our loan advisors can help you to get through the approval process. You can pre-qualify in 15 minutes and get a free, no-obligation quote. Trust us to help you. We’re the people people with technology!