There are many factors to consider when selling a home, and you may be wondering what happens to your mortgage when you move. After all, the 2018 American Community Survey found that the median length of time homeowners stayed in their homes was 13 years, a shorter length of time than most mortgage terms.

Recent data from the Pew Research Center found that at the end of the fourth quarter of 2020, the rate of American households that owned their own home increased to around 65.8%. With so much homeownership throughout the country, mortgages are an imperative topic. If you’re one of the many Americans that own a home with a mortgage, you should know your options when it comes time to sell.

Here’s a comprehensive guide to what happens if you sell your house and still owe money.

Topics Covered

- Should I Pay Off My Mortgage Before Selling My House?

- What Happens to My Mortgage When I Sell My House?

- Selling Your Current Home Before Buying Another

- Buying a New Home Before Selling Your Current One

- How to Get a Mortgage on a New Home

Should I Pay Off My Mortgage Before Selling My House?

If you plan to move and already have a mortgage on your current home, your first thought may be to pay off your mortgage early, so you’re free of your monthly payments. Though it isn’t necessary to pay off a mortgage before you sell your house, it may be a viable option depending on your situation. This option requires some planning, but you can make it happen.

There are several benefits to paying off a mortgage early:

- Saves interest fees: Over the life of a 15- or 30-year loan, interest can stack up and sometimes double what homeowners pay, despite their original loan amount. When homeowners decide to pay their loan off early, they get to eliminate some of the interest they would pay in the future and save themselves years of payments.

- Frees up monthly funds: This process also opens up more funds in your monthly budget, giving you greater flexibility with that cash later in life. When your mortgage payments are gone, you could contribute that money into your emergency fund, retirement account or other investments, or save up for that vacation you always planned.

Many variables can factor into your decision, so it’s essential to crunch the numbers and examine your financial situation individually.

Here are two of the most common strategies to pay off your mortgage early:

1. Higher or More Frequent Payments

One of the simplest ways to decrease the life of your mortgage is to make payments more often. Although bi-monthly payments will cost the same amount as your previous mortgage payments, they’ll use the weeks of the year to give you an additional annual payment. When multiplied over several years, one extra yearly deposit can lead to a considerable amount of savings.

Consider increasing your monthly payments, consistently paying more on your mortgage than the minimum requirement. Manually adding extra is a flexible option that allows you to contribute any amount you choose. Add $100 more, $50 more or any variable amount you decide to contribute over your loan’s life.

2. Refinancing

Some homeowners choose to fix their loan for 30 or 40 years but may later decide to pay it off sooner. By refinancing your mortgage, you can refigure your loan for a shorter timeframe, increasing your monthly payments and decreasing your interest.

However, refinancing may not be the best idea when you’re looking to move. Some homeowners may want to refinance to put the money they would have spent on interest payments toward their savings for a down payment. If your savings don’t add up before your planned move, a refinance could cost you more money than it’s worth. Use Assurance Financial’s refinance calculator to determine whether a refinance is right for you.

Ultimately, choosing to pay off a mortgage before you move may not be your best option. Depending on your timeframe and your other investment opportunities, you may decide to keep that cash and set it aside for a new down payment. Whatever you choose, weigh your choices and consider which is in your best interest.

What Happens to My Mortgage When I Sell My House?

According to Freddie Mac, almost 90% of American homeowners finance their homes with a 30-year mortgage. Still, many homeowners will move to another house before that timeframe ends. This situation is common, so you can follow standard practices for selling a home with a mortgage attached.

If you’re selling your house before the mortgage term is up, you can take one of two avenues:

1. Traditional Home Sale

In a traditional home sale, the seller lists the house for a price that will cover the following costs:

- The mortgage’s remaining costs

- Existing home equity loans or home equity lines of credit (HELOCs), if applicable

- Mortgage prepayment penalties, if applicable

- Closing costs, including agent commissions, taxes and other fees

After taking care of the above expenses, whatever amount is left over is the seller’s profit. To pay for the rest of the mortgage, the closing manager sets up an escrow account into which the buyer will deposit their payment. Then, the title company will distribute the final mortgage payment to the lender. As a result, the seller no longer has that mortgage.

If you’re unable to sell your home for enough money to cover the associated costs, you’ll have to pay them out of pocket, wait until you can sell the house for more or request a short sale. In an ideal situation, the seller can cover the remaining balance of their loan, pay for closing costs and put a down payment on their next home from the sale price. This scenario requires good home equity — which is the homeowner’s financial stake in their house — to warrant a high enough price.

A home’s equity is comprised of the following elements:

- The original down payment

- The home’s gains in market value

- Mortgage principal payments

- The cost of renovations or improvements the seller made to the house

Getting a quote for your mortgage payoff when selling your house helps determine the price you need to sell your home. A mortgage payoff shows you the total amount you need to pay to settle your mortgage debt, including your interest and other unpaid fees. If you tell your lender about your plan to sell your home, they’ll provide you with a mortgage payoff quote.

2. Short Sale

When your house has too little equity to pay for your mortgage, it has negative equity. Without enough cash to cover your remaining mortgage balance, plus the closing costs, a short sale may be your only option. In a short sale, the buyer purchases the home for less than the seller’s debt against the property. These sales require approval from your lender because they leave the mortgage company at a financial loss.

The approval process for a short sale usually takes longer than for a traditional sale since the seller has to convince the lender they can’t pay off their loan. To convince the lender, the seller must either show that the housing market dropped, so their home is worth less than their debt, or prove they’re incapable of keeping up with their payments. Because the lender is trying to recoup as much of their losses as they can, the process may take a while.

Another negative aspect of short sales is they remove the seller’s negotiating power. This entire process depends on the lender’s approval, including the sale of the house. Even when the buyer and seller agree on a price, the lender may end up declining the buyer’s offer to hold out for a higher one. Ultimately, short sales negatively affect a seller’s credit score and make it more challenging to get a home in the future.

Selling Your Current Home Before Buying Another

If you’ve examined all of your options and want to go ahead with the sale of your home, you may want to know whether you should sell it before or after buying a new one. This answer could be as simple as establishing how much you have in savings to spend on a down payment. Most sellers find that selling their current home opens up their home’s equity so they can use that profit for their next home.

Pros of Selling First

By selling first, you can enjoy the following benefits:

- More negotiating power: When you buy a new house before selling your current one, you put more pressure on yourself to sell quickly and at a high price. Depending on what strategy you use to purchase a new home while still responsible for an old one, you may feel compelled to accept the first offer you receive. However, selling first allows you to negotiate with buyers and wait to sell until you get the offer you want.

- Less pressure: Buying a new home before someone purchases your old one puts you on a crunched timeline to get rid of your current home as fast as possible. Waiting for the right buyer while paying for two properties can be a lot to handle. If you sell first, you can take your time considering sales strategies and making any renovations or repairs.

- Total equity for future purchases: Perhaps one of the most compelling reasons to sell before buying another house is the potential to tap into your current home’s equity when you make your next purchase. If you pocket a considerable profit, you may be able to pay a larger down payment and take out a smaller mortgage on your next home. With a high enough profit, you may even be able to offer cash, which is very appealing to sellers.

For the above reasons, selling a current home before buying another is usually the most straightforward course to take. When stepping into the market to purchase a new home, the lack of pressure on your time and funds can help you make the best decision regarding a sale and give you more money to put toward your next home.

If you’re in a seller’s market, selling before buying can be even more profitable. In a seller’s market, sellers have the upper hand in negotiations because there are fewer homes than potential buyers. This situation gives sellers the ability to keep their asking price high or even raise it. Because there’s such high demand, homes usually sell quickly in a seller’s market.

Cons of Selling First

However, selling before buying could also cause some logistical concerns. If you sell your home quickly, you might have to find temporary housing before purchasing your new home. When there’s a lot of competition in the housing market, a seller could reject your offer, and the property could go to another buyer. Should that happen unexpectedly, you might need to move your belongings into a rental unit or pay for storage until you can move somewhere else.

Before deciding when to sell, calculate the costs involved and whether you may experience a time crunch when going to buy. There may be a situation where timing forces you to move in with a friend or sublet an apartment for a while. That said, the cost of moving twice and storing your furniture and belongings until you buy a new house generally won’t outweigh the benefits of selling before buying a new home.

[download_section]

Buying a New Home Before Selling Your Current One

Sometimes, buying first can be appealing when you can afford to buy without recovering the equity in your old home or you’re in a buyer’s market and have negotiated an excellent deal for a house. This option may require some extra steps and additional help with financing the purchase. If you’re unable to pay for a new home out of pocket, you have several options for financing:

1. Home Sale Contingency

A home sale contingency is a clause you can include in your offer to purchase a house. This clause tells the seller you need to find a buyer for your own home before closing on the purchase. A sale and settlement contingency gives you the legal right to exit a contract if you don’t receive an offer for your current home in time. A settlement contingency protects you if an offer on your old home falls through.

A significant drawback to a home sale contingency is that it could make your offer less competitive to sellers. If the seller sees you can’t make a firm offer, they could pass over you in favor of a committed buyer when negotiating a deal. If you’re only able to make less competitive offers, buying a home could take longer. However, if the seller accepts your offer, you’ll be able to keep the home you want under contract while you wait for a buyer.

2. Bridge Loan

Another option for financing a purchase is taking out a bridge loan. These are short-term loans designed to bridge the time between when a homebuyer needs financing and when it becomes available. With a bridge loan, you can access the resources you need to pay for your current mortgage and make a down payment toward your new house.

These loans can be a simple way to get financing quickly. Note that you’ll need to make monthly payments on the bridge loan while also paying for your existing mortgage. However, when you sell the old home, you can use your profit to pay off the bridge loan. If your home takes a while to sell, you could be paying two mortgages on top of the bridge loan payments as you wait.

3. Two Mortgages

If you can afford it, carrying two mortgages may be the least complicated option for financing a home. Maintaining two mortgages while you wait for your old house to sell can keep you from entering into another loan like a bridge loan.

However, carrying two mortgages at once probably doesn’t sound enjoyable. The cost of two mortgages can become steep, so you may not be interested. Still, it could give you greater freedom to make an offer without being tied to a home sale contingency.

How to Get a Mortgage on a New Home

Whether you’ve already sold your old home or are just beginning the house-hunting process, you’ll need a mortgage before closing on a new house. Here are the steps you need to take to be ready to make that purchase and move into your next home.

1. Save for a Down Payment

The down payment may look different depending on whether you’ve already sold your old home. With the profits from your old home in your pocket, you can use it for a down payment along with any other funds you saved. Because a larger down payment means a smaller loan size, choosing to save the money you would have spent on your morning later can go a long way.

If you’re buying a home without the benefit of your previous home’s equity, you may qualify for a conventional loan with a down payment of only 3-10%. There are also mortgage programs that require as little as 0% down, like United States Department of Agriculture (USDA) loans and Veterans Affairs (VA) mortgages. With certain qualifications, you can reduce the amount you need for a down payment and avoid paying for private mortgage insurance.

2. Explore Mortgage Options

Before applying for a loan, consider which loan types are most beneficial for you in your financial situation. Some homebuyers choose to go with a conventional mortgage with 15-, 20- or 30-year loan terms. Special considerations — such as your credit score, veteran status or location — can qualify you for other loan types. With some careful research and the help of our dependable loan advisors, you can find the best mortgage type for your needs.

Also, think about what features you want in a house and what you’re willing to sacrifice. It may be best to buy a smaller or less updated home to keep your mortgage debt lower or concentrate your monthly debt payment on loans with higher interest rates, such as school or credit card payments. On the other hand, you may be comfortable buying at the higher end of your price range if you have few or no other debts.

3. Complete an Application

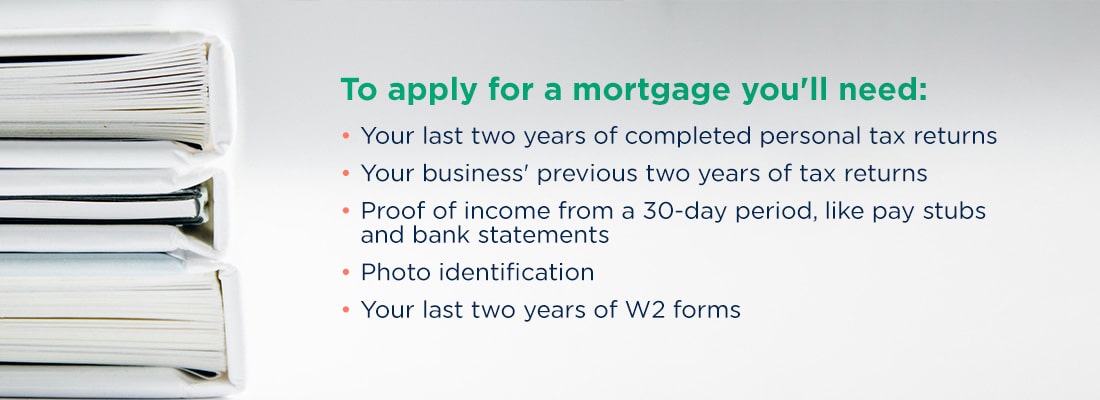

Once you’re ready, you’ll want to apply for the mortgage of your choice. To apply, you’ll need some paperwork, including:

- Your last two years of completed personal tax returns

- Your business’ previous two years of tax returns, if applicable

- Proof of income from a 30-day period, like pay stubs and bank statements

- Photo identification like a driver’s license

- Your last two years of W2 forms

Once you have your forms in order, you can apply online, and your lender will look over your financial information to give you an estimated interest rate. With the online application at Assurance Financial, you can submit all of this documentation in as little as 15 minutes and get pre-qualified for a loan within 24 hours.

4. Wait for Processing and Underwriting

Once you’ve found the home you want and the seller has accepted your offer, your lender sends your financial information over to a loan processor, who double-checks all of the details and will contact you if they need any clarification.

After processing, your lender will likely order a home appraisal to determine the value of the property you intend to buy. Once an appraiser looks over your home, a loan underwriter will review your credit score and application once more to make the final approval. This stage finalizes the amount of your loan and your interest rate.

5. Head to Closing

When your loan is cleared, you can begin the final steps in your journey to homeownership. The title company will set up a closing day with you, and you can sign many of your closing documents online beforehand.

On closing day, you’ll bring your down payment in the form of a cashier’s check, plus any other fees and closing costs you may be required to pay. Alternatively, you can choose to set up a wire transfer for the funds. After you sign the last bit of paperwork, you’ll get the keys to your new home.

Get Started With Assurance Financial

If you’re looking to get a mortgage for your new home or refinance an old mortgage, Assurance Financial is ready to help. We provide complete support at every step of your loan application, and our licensed loan officers are experts at getting the home loan that best suits your needs. With a variety of loan types and competitive rates, we provide mortgage solutions for homebuyers at any stage of life.

At Assurance Financial, we understand you want a smooth mortgage process that leads you to your dream home. To get started and discuss your mortgage options, find a loan officer today and see why Assurance Financial stands out from other online mortgage lenders.

Linked Sources:

- https://assurancemortgage.com/paying-off-mortgage-early/

- https://assurancemortgage.com/calculators/should-i-refinance-my-mortgage/

- https://myhome.freddiemac.com/blog/homeownership/20190815-mortgage-options

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-payoff-amount-is-my-payoff-amount-the-same-as-my-current-balance-en-205/

- https://assurancemortgage.com/everything-you-need-to-know-about-usda-rural-loans/

- https://assurancemortgage.com/5-things-know-va-loans/

- https://assurancemortgage.com/what-is-a-conventional-mortgage/

- https://assurancemortgage.com/apply/

- https://data.census.gov/cedsci/table?q=duration%20of%20homeownership%202018&tid=ACSDP1Y2018.DP04

- https://www.pewresearch.org/fact-tank/2021/03/08/amid-a-pandemic-and-a-recession-americans-go-on-a-near-record-homebuying-spree/