Key Takeaways

- 15-year fixed mortgages lock in constant interest rates, typically lower than 30-year loans, providing payment predictability throughout the loan term.

- Monthly payments include principal, interest, homeowner’s insurance, property taxes, and potentially private mortgage insurance if the down payment is under 20%.

- Understanding how 15-year loans affect total costs requires requesting loan estimates, comparing options, and preparing for closing.

You plan on buying a house in the near future, and you know you’ll need a mortgage to do so. The question is, which type of mortgage may be best for you? Mortgages vary in term length, type of interest rate and the amount of interest charged. One available option is a 15-year, fixed-rate mortgage.

Apply NowStill have questions or need more information? Below is an overview of what this article covers!

Topics Covered

Frequently Asked Questions

- What Is a 15-Year Fixed Mortgage?

- How Does a 15-Year Fixed-Rate Mortgage Work?

- What Makes up Your Mortgage Payment?

- How Much Can You Afford to Borrow?

- Is a 15-Year Fixed Mortgage Right for Me?

- Apply for a Home Loan Online

As you weigh your mortgage options, it’s important to understand how getting a 15-year home loan will affect your monthly payments and how much you end up paying for your home over the long run. It’s also important to understand how a fixed interest rate differs from an adjustable rate. Get all the details on a 15-year fixed mortgage so you can determine if it’s the right option for you.

What Is a 15-Year Fixed Mortgage?

A 15-year fixed mortgage is a loan with a repayment period of 15 years and an interest rate that remains the same throughout the life of the loan. Like other types of mortgages, you use a 15-year, fixed-rate mortgage to buy property. Many people obtain a mortgage to buy their primary residence, while others obtain a mortgage to buy a vacation home or property to rent out to others.

To understand what a 15-year fixed mortgage is, it helps to break down some commonly used terms in the mortgage business:

- Term: The mortgage term is the length of time you have to repay the loan. At the end of the term, the entire loan needs to be repaid to the lender. The length of the term influences the size of the monthly payments, as well as the interest charged on the loan. Mortgages with shorter terms, like a 15-year home loan, are considered less risky to the lender, so they often have slightly lower interest rates compared to longer-term mortgages, like a 30-year loan.

- Interest: Interest is the price you pay to borrow money, usually a percentage of the loan, such as 3% or 4%. A lender determines your interest rate based on factors such as your credit score, income, the loan term and the market. The type of interest rate — whether it’s fixed or adjustable — also plays a part in determining when you pay.

- Fixed-rate: Some mortgages have a fixed interest rate. With a fixed-rate mortgage, you pay the same interest rate throughout the life of your loan. For example, a 15-year mortgage with a 5% fixed rate will have a 5% rate until the borrower pays off the mortgage or refinances. One advantage of a fixed-rate mortgage is that it allows you to lock in a rate when they are low. You can rest assured that your mortgage principal and interest payment will stay the same month after month, no matter what happens in the market. On the flip side, if you get a fixed-rate home loan when rates are high, you could be stuck paying a high interest rate for years.

- Adjustable-rate: Unlike a fixed-rate home loan, the interest rate on an adjustable-rate mortgage (ARM) changes at various points throughout the repayment period. Often, an ARM may have an introductory rate. The introductory rate tends to be lower than the interest rate available on a fixed-rate loan. After the introductory period ends, the rate may change based on whatever is going on in the market. It can go up, meaning your monthly payments may go up. It can also drop, meaning you may pay less each month. Some borrowers take out an ARM initially and later refinance to a fixed-rate loan.

- Principal: The principal is the amount of money you’ve borrowed to buy your home. If you purchase a $250,000 house, pay a 10% down payment of $25,000 and borrow $225,000, the $225,000 would be the loan’s principal. If you can pay extra against the principal as you pay down your mortgage, you can shorten the length of time it takes to pay off the loan completely.

- Mortgage insurance: Depending on the size of your down payment, you may have to pay mortgage insurance on top of the principal and interest charged on the loan. Mortgage insurance offers an additional layer of protection to the lender, in case the borrower struggles to make payments. It is usually required when a person makes a down payment under 20% of the home’s value. You can cancel the mortgage insurance payment once you have paid off enough of the principal to have 20% equity in your home.

How Does a 15-Year Fixed-Rate Mortgage Work?

A 15-year fixed-rate mortgage works similarly to other types of mortgages. You apply for the loan by providing proof of income, employment, assets and your credit history. If approved, you put down a certain amount of money, then make payments on the loan each month until it is paid off. The amount you can afford to borrow when you apply for a 15-year fixed mortgage depends on a variety of factors.

When you apply for a 15-year fixed-rate mortgage, you will typically take the following steps:

- Request a loan estimate from a lender: A loan estimate lets you know how much you can borrow, the interest rate and the anticipated closing costs. You can request estimates from multiple lenders to get a sense of what’s available.

- Indicate your intent to proceed: If you decide to move forward with one lender, you need to let them know. Lenders must honor the estimate for 10 business days, so you should decide if you’re moving forward within that time.

- Begin the application process: After you tell the lender you want to go ahead with the mortgage, you’ll need to submit documents, such as proof of income and bank statements, to start the formal application process.

- Prepare for closing: If all goes well with the application, home inspection and process as a whole, you can get ready for the closing date. It’s important to keep things moving as scheduled, as a delay in closing can mean you lose the rate you locked in or that you have to start over.

What Makes up Your Mortgage Payment?

One miscalculation many aspiring homebuyers make is to assume their monthly mortgage payment only includes the principal and interest. In reality, your mortgage payment includes multiple components. When you take out a 15-year home loan, your monthly payments can be divvied up in the following ways:

- Principal payment: This portion of your monthly payment goes toward the amount you’ve borrowed. As you pay down your mortgage, you’ll likely see the amount of your payment that goes to the principal increases while the amount you pay in interest decreases. Many lenders also let you pay additional amounts toward the principal to help pay off your mortgage more quickly. Paying more than the minimum due toward the principal monthly can help you get out of debt sooner.

- Interest: Think of the interest rate on your mortgage as the money you pay the lender in order to use their service. The lower your interest rate, the more affordable the loan is. As you pay down the principal, the amount you pay in interest each month shrinks.

- Homeowner’s insurance premiums: Your lender may also collect your homeowner’s insurance premiums and put them in an escrow account to be paid to your insurer. The size of your premiums depends on the value of your house and the amount of insurance you buy.

- Property taxes: Your lender may also collect your property tax payments and put them in an account to be paid to your local government by the due date each year. Property tax amounts vary widely from location to location.

- Private mortgage insurance: If you put down less than 20%, your lender may require private mortgage insurance. The amount varies based on the size of your down payment. The more you put down, the lower the insurance premium. Once you’ve made enough payments to equal 20% of the value of your home, you can ask the lender to remove the insurance.

How Much Can You Afford to Borrow?

You want to have a sense of how much you can afford to borrow before you start looking for a home and applying for a mortgage. Usually, since you pay off a 15-year home loan in half the time it takes to pay off a 30-year loan, the amount you can afford to borrow is less. You might be able to purchase a $200,000 home by putting 20% down if you apply for a 30-year loan. Since the monthly payments on a 15-year loan are often about twice as much as those on a 30-year loan, you might be able to purchase a $150,000 home with a 15-year loan.

You can use a mortgage calculator to compare the monthly payments on a 15-year versus a 30-year mortgage.

To determine how much you can borrow with a 15-year mortgage, pay attention to how much you can afford to pay each month. Look at your total debt compared to your total income. When getting a mortgage, your ideal housing ratio, also known as a front-end debt-to-income ratio, is 28%. With insurance and property taxes included, your housing payments should be within 28% of your total income.

Lenders also use the back-end ratio, which is all your debts compared to your income. An ideal back-end ratio is 36%. If you have other significant debts, such as student loans or car loans, your ideal monthly mortgage payment can end up being much lower than 28% of your total income.

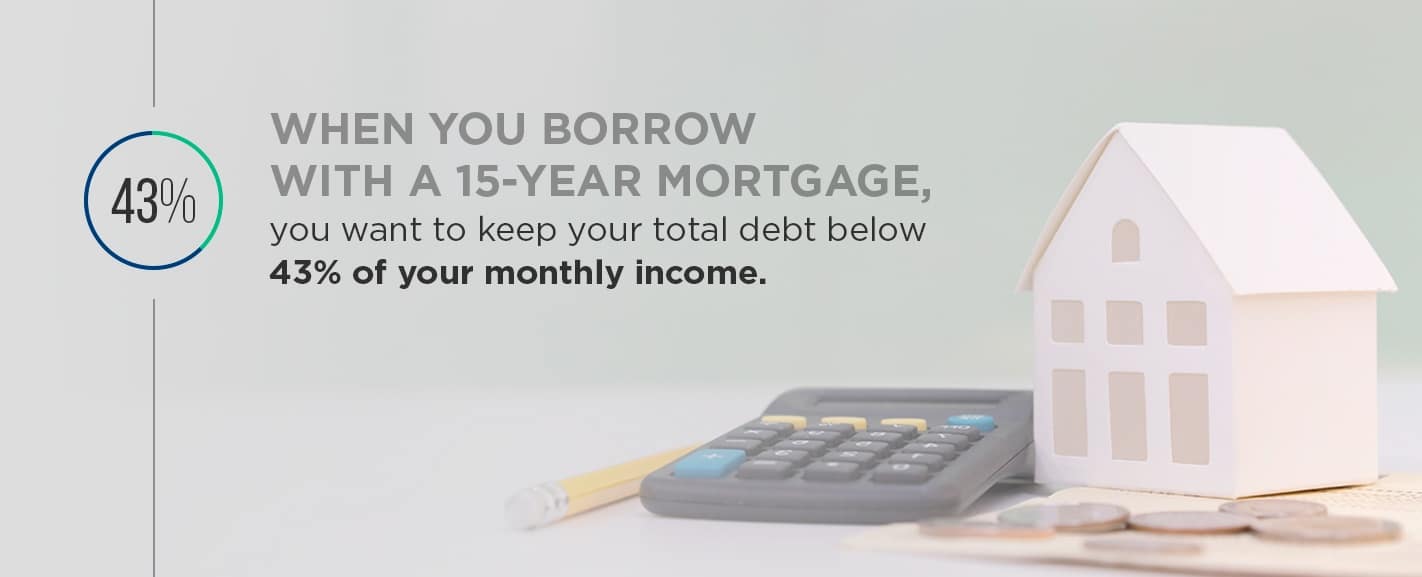

While the 28 and 36% ratios are ideal, lenders understand that life can be complicated. Depending on your income or credit score, you might be able to borrow as much as 43% of your monthly income.

To get your monthly payments under the desired percentage of your income, you may need to either pay off some debts before applying for your mortgage or find a way to increase your earnings.

Is a 15-Year Fixed Mortgage Right for Me?

Paying off your mortgage in half the time can seem pretty appealing. Before you decide to apply for a home loan with a 15-year term instead of a 30-year term, it’s important to consider your personal situation. You’ll pay the loan off sooner, but that usually means a higher monthly payment or buying a less expensive house. Some things to consider before applying for a 15-year fixed-rate home loan include:

- Your income stability: Since a 15-year mortgage typically means higher monthly payments compared to a 30-year home loan, it’s vital that you have the income needed to afford those payments. It’s also helpful if you have a steady record of earning either the same amount or increasing amounts of income each year. If there’s a lot of up-and-down in terms of what you bring in or if you aren’t sure how long your current employment and income situation may last, it may not be the right time to get a 15-year mortgage.

- Current interest rates: Take a look at the current interest rates. If they are low, getting a mortgage with a fixed rate is likely to be in your favor, as you’ll get to keep that rate for years to come. If rates are on the high side, you might consider an ARM instead. When it comes time for the rate on your loan to adjust, you can refinance to a fixed-rate loan or keep the ARM.

- Your age: Your age or season in life can help you determine if a 15- or 30-year loan makes more sense. If you are older and approaching retirement, a longer term may have you making payments on your loan after you’re no longer working. If you don’t want to have a mortgage throughout retirement, choosing one with a shorter term can make more sense.

- Your other financial goals: Consider your other financial goals in light of your mortgage. If you are trying to save for retirement or save for your child’s education, you may not want to pay a considerable amount of your monthly income toward your home. On the other hand, if you have already achieved other financial goals or have a high amount of disposable income each month, putting that toward your housing payment can be a good move.

- The price of homes in your area: The average price of houses in your area may influence whether you can afford a 15-year mortgage or not. The more expensive homes are, the higher your payment may be. But if homes are relatively affordable, getting a 15-year loan can help you own your home outright in less time and for less money.

[download_section]

Pros of a 15-Year Fixed-Rate Mortgage

If you’re still not sure if a 15-year fixed-rate mortgage is right for you, it helps to look at a few advantages of this type of home loan:

- You build up equity more quickly: Equity is the difference between the value of your home and the amount you still owe on the mortgage. Having equity in your home gives you leverage. When you sell the home, you get more money from the sale if you have more equity in it. You can also use equity to borrow against your home to cover the cost of renovations or other repairs.

- You own your home faster: With a 15-year mortgage, you can own your home completely in half the time it would take if you were to get a 30-year loan. Once your home is fully paid off, your cost of living can drop significantly.

- You pay less in interest: Since you have a 15-year mortgage for less time than a 30-year loan, you usually end up paying considerably less in interest. More of your monthly payment goes toward the principal sooner. Although you have bigger monthly payments, the total cost of a 15-year loan is often much less than the cost of a longer mortgage.

- You might get a better interest rate: The less time you need to pay off a loan, the less of a risk you are in the eyes of a lender. Depending on other factors, many lenders are likely to offer lower interest rates on 15-year mortgages compared to 30-year loans.

- You don’t have to worry about interest rates changing: With a fixed-rate loan, the rate you pay on day one is the same as the rate you pay on day 5,000. You don’t have to worry that your payment may suddenly balloon or that you’ll be left with an unexpectedly high mortgage bill.

- You have the same payment month after month: A 15-year, fixed-rate mortgage eliminates one uncertainty from your life: How much your housing payment will be. When you rent, your monthly obligation can increase from year to year if your landlord decides to raise the rent. With an ARM, your payment can go up, as well. Your fixed-rate mortgage payment stays the same year after year, even if you begin to earn more money or other costs increase.

- You might be able to make a larger down payment: Since the price of the home you can buy with a 15-year mortgage could be lower than what you can afford with a 30-year mortgage, you may be able to put down more upfront — potentially saving you the cost of private mortgage insurance. For example, if you can afford a $200,000 home with a 30-year mortgage and have $30,000 to put down, your down payment would be 15% and you’ll have to pay mortgage insurance. If you can afford a $150,000 home with a 15-year mortgage and put $30,000 down, your down payment is 20%. Putting down 20% upfront can also make you more likely to get a lower interest rate, helping you save even more.

Cons of a 15-Year Fixed-Rate Mortgage

While a 15-year fixed-rate mortgage can have several benefits for the right borrower, there are also some potential drawbacks to consider:

- You have a higher monthly payment: Usually, the monthly payment required on a 15-year mortgage is higher than that required by a 30-year mortgage since you are paying the loan in half the time. If your income is high enough and you have enough financial stability, the extra monthly payment in exchange for saving more overall might not be a concern. But if you struggle to make ends meet each month or have other financial obligations, a high mortgage payment can be a challenge.

- You could end up “house poor”: You build up equity more quickly with a 15-year loan. This can also mean you end up house poor, meaning most of your net worth is tied up in your home. Day-to-day, that might not be an issue. But if you need cash quickly and don’t have a lot of savings or liquidity, it can pose a problem.

- You might have to buy a less expensive house: Depending on where you live, you might not be able to afford to buy a house with a 15-year mortgage. If housing prices are high, a 30-year loan might be a necessity to keep your monthly payment within reach. Another option may be to buy a smaller, less expensive home, such as a two-bedroom instead of a three-bedroom or a house in a neighborhood that offers fewer amenities.

- You might get stuck with a high interest rate: Interest rates fluctuate from year to year, so depending on when you buy your home, you may end up getting a higher rate compared to someone with similar income or credit who buys a home a year before or after you. Since the interest rate on a fixed-rate mortgage is the same for the life of the loan, you could be stuck with a high rate unless you refinance.

Apply for a Home Loan Online

Assurance Financial aims to help people achieve the American dream of homeownership. If you’re ready to make the first step towards buying your home, we’re here to help. Abby, our online mortgage assistant, can walk you through the process of putting together your application.

You can get started today or set up an appointment to put together your application at a time that works for you. If you’d rather talk to a representative right away, you can connect with a loan advisor in your state who can help you review your mortgage options and choose the one that works for you.

Sources

- https://assurancemortgage.com/purchase-your-home/

- https://www.consumerfinance.gov/ask-cfpb/on-a-mortgage-whats-the-difference-between-my-principal-and-interest-payment-and-my-total-monthly-payment-en-1941/

- https://www.lendingtree.com/home/mortgage/common-mortgage-terms/

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-debt-to-income-ratio-why-is-the-43-debt-to-income-ratio-important-en-1791/

- https://www.phila.gov/services/property-lots-housing/property-taxes/real-estate-tax/

- https://www.mortgageloan.com/why-you-should-and-shouldnt-get-a-15-year-mortgage

- https://www.credit.com/blog/can-you-qualify-for-a-15-year-mortgage-113487/

- https://www.bankrate.com/calculators/mortgages/mortgage-calculator.aspx

- https://www.nerdwallet.com/mortgages/mortgage-calculator/calculate-mortgage-payment

- https://www.bankrate.com/mortgages/arm-vs-fixed-rate/

- https://www.rocketmortgage.com/learn/15-vs-30-year-mortgage

- https://www.fool.com/mortgages/4-reasons-to-get-a-15-year-mortgage.aspx

- https://www.bankrate.com/finance/mortgages/fixed-rate-mortgages-1.aspx

- https://www.quickenloans.com/learn/home-equity-and-how-to-use-it

- https://www.nerdwallet.com/article/mortgages/pros-cons-15-year-mortgage

- https://www.daveramsey.com/blog/what-is-a-15-year-fixed-rate-mortgage

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/find-a-loan-officer/