Temporary setbacks can prevent you from being able to make your mortgage payments for a couple of months. In the wake of unexpected events such as COVID-19, a flood or other natural disasters, many Americans face unemployment, furloughs, illness and the death of family members. This challenging time may heavily impact your finances, and you may be wondering what to do if you can’t pay your mortgage.

While many homeowners may expect that an inability to make a monthly mortgage payment will immediately result in a default on the mortgage loan or foreclosure on their property, the reality is not so cut and dried. Fortunately, another possibility is mortgage forbearance.

What Is Mortgage Forbearance?

Mortgage forbearance refers to an agreement between you and your mortgage servicer to temporarily reduce or suspend your mortgage payments for a specific period. The option of mortgage forbearance can allow you to cope with your short-term financial difficulties by giving you some time to recover after a hardship. In some cases, there is government mortgage relief, and in others, the servicer may offer a special program of mortgage forbearance.

As part of this agreement, you agree to a plan for your mortgage that will bring you up-to-date on your payments over a set time. Essentially, you will need to repay these paused or lowered payments down the road after the temporary hardship has ended.

If you are dealing with a temporary hardship or are behind on your monthly mortgage payments or may soon miss a payment, mortgage forbearance may be an option for you.

Benefits of Mortgage Forbearance

What benefits can mortgage forbearance offer you during a time of temporary hardship? The following are a few of the benefits of mortgage forbearance:

- Suspends or lowers your monthly mortgage payment temporarily

- Allows you to avoid foreclosure or damage to your credit score

- Enables you to remain in your home

- Gives you time to get back on your feet and improve your current financial situation

Mortgage forbearance, then, is essentially pausing your payments. If you have been dealing with hardships due to COVID-19 and you can’t pay the mortgage this month, you may be able to pursue mortgage forbearance.

Frequently Asked Questions About Mortgage Forbearance

Here are a few of the frequently asked questions we receive about mortgage forbearance from homeowners:

- Do I have to repay missed payments? If your mortgage is in forbearance, you must repay your missed payments. Forbearance delays your payments, rather than forgiving them.

- Will interest on my mortgage continue accruing? Yes, interest on your mortgage will likely continue accruing while your mortgage is in forbearance, though this varies by

- Will mortgage forbearance affect my credit? No, opting for mortgage forbearance is unlikely to adversely impact your credit score unless your servicer reports it to a credit bureau. However, you may have trouble getting approved if you try to refinance your mortgage shortly afterward. Also, it’s a good idea to check your credit report each month to quickly resolve any issues that could arise.

- Can I pay my missed payments whenever I want? No, you cannot repay your missed mortgage payments whenever you want. Servicers handle mortgage modifications differently, so you may have to pay all of your missed payments in a lump sum or add them to the end of your loan term.

- Where should I apply for forbearance? You should apply for mortgage forbearance where you currently make monthly payments.

Mortgage forbearance is for homeowners who are dealing with a situation that causes financial hardships. In uncertain times, you may be worried about making your monthly mortgage payments, but before you stress, you should reach out to your servicer to discuss your options.

How Does Mortgage Forbearance Work?

To request mortgage forbearance, you should first contact your servicer. The exact specifics of how mortgage forbearance works depend on a few factors, such as your servicer, the type of mortgage you have, the underlying circumstances and how long you have been making monthly mortgage payments. Most terms for mortgage forbearance fall under one of two agreements.

- Suspended payments: Your servicer will agree to a mortgage pause for a specific period.

- Lowered payments: Your servicer will reduce your monthly mortgage payments, but you’ll need to pay them on the same schedule.

The goal of these agreements is to keep the bank from foreclosing on your home if you’re temporarily incapable of paying your monthly mortgage payments in full.

Mortgage Forbearance Terms

If you are eligible for mortgage forbearance, you and your servicer will discuss the terms, such as:

- The length of time your mortgage forbearance will last

- How you will repay your payments to your servicer after your mortgage forbearance ends

- Your reduced mortgage amount if you need to keep making monthly payments

- Whether your servicer will report your mortgage forbearance to credit bureaus

Speak with your servicer to determine how these terms will affect your monthly payments and total mortgage amount.

How Long Mortgage Forbearance Lasts

The length of the forbearance period depends on the amount of time you and your servicer agree upon, as well as what caused the setback and your likelihood of being able to return to making your full monthly mortgage payments. As such, a mortgage forbearance period may last for a couple of months or up to a year. Since the goal of mortgage forbearance is to provide relief to homeowners with short-term financial difficulties, it usually does not last for more than a year.

Your servicer may also ask you to provide updates during your mortgage forbearance period. If it seems like you’ll need a different type of assistance or an extension on your forbearance, you can speak to them and discuss your options.

Mortgage Forbearance Repayment Options

While your mortgage is in forbearance, your loan will likely continue accruing interest. After your mortgage forbearance period ends, you must repay the reduced or suspended amount. You will repay your servicer according to the forbearance terms you previously arranged.

With a mortgage forbearance, you may be able to choose from the following repayment options.

- Reinstatement: One of your repayment options is a one-time lump sum payment for your reduced or suspended amount.

- Added amount to subsequent mortgage payments: Another option for repayment is adding a specific amount to each of your monthly payments until you have repaid the full forbearance amount.

- Tack on missed payments: Finally, you may also be able to add the amount of your repayment to the end of your loan. Doing so will lengthen the term of your mortgage.

You may also be able to modify your past-due mortgage amount, which will change the terms of your loan so your payments can be more manageable. Modification is an option may be available to you if you do not have the funds to cover a repayment plan or reinstatement or if your financial hardship continues for a longer period than initially anticipated.

To qualify for mortgage forbearance, you may have to pay a higher interest rate on your monthly payments once they resume, or you may have to pay a one-time fee.

How to Apply for Mortgage Forbearance

As soon as you realize you are in danger of missing a mortgage payment, you may want to reach out to your mortgage servicer, which is the company you send your monthly mortgage payments to. If you are unsure who services your mortgage, you can find the company’s contact information on your mortgage statement.

Events like natural disasters may have time limitations related to initiating a mortgage forbearance, so you may want to contact your servicer as soon as possible. When you do so, keep in mind that during unpredictable times, servicers will be dealing with a high call volume and may also be struggling with upheaval.

When you reach out to your servicer, prepare to discuss the following.

- The event that led to the request: You will likely discuss with your servicer what event or circumstances caused you to request mortgage forbearance.

- Length of inconvenience: You may also discuss with your servicer whether you expect the problem to be short- or long-term.

- Actions you have taken: Another point of discussion may be what you have already done to rectify or avoid this situation.

It may be helpful to request that your servicer note your history of on-time payments. Aim to continue making your monthly payments while you are waiting for a decision from your servicer on mortgage forbearance.

While a bank does not have to approve your request for mortgage forbearance, during a time of nationwide difficulty, a servicer may be more inclined to help with your mortgage payments and approve your application so you can keep your home.

Who Qualifies for Mortgage Relief?

How do you know if you are an ideal candidate for mortgage relief programs? Though eligibility requirements for mortgage forbearance depend on the servicer, you will most likely start your request for mortgage forbearance by filling out an application. Depending on the servicer, you may apply online or by calling.

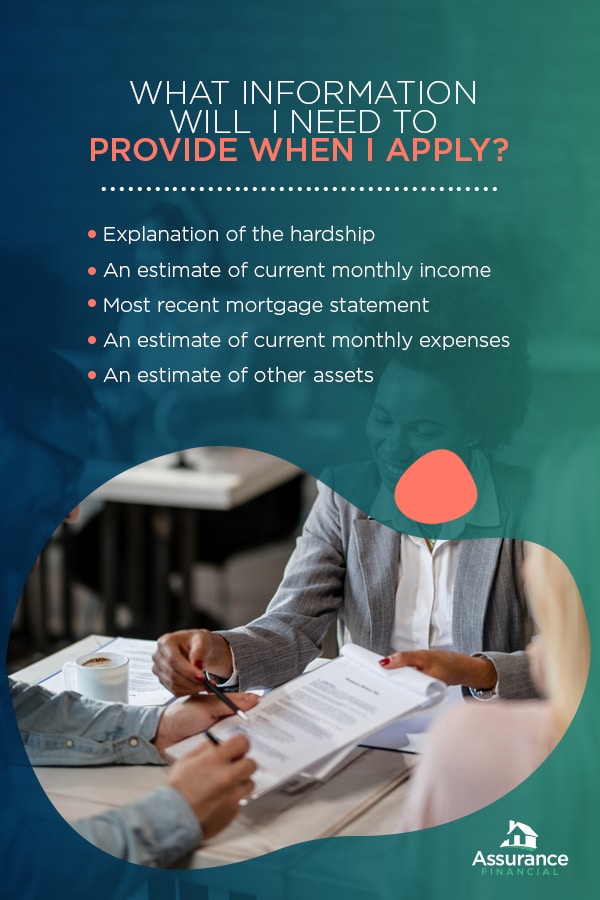

What Information Will I Need to Provide When I Apply?

When you fill out your online application or call your servicer, you may want to have the following information on hand.

- Explanation of the hardship: When you apply online or call your servicer, you may need to explain the hardship you are facing. If possible, you may also need to supply documentation that can substantiate your claim.

- An estimate of current monthly income: You may need to supply an estimate of your monthly income when you apply online or call your servicer. To demonstrate your income, you may need to provide your servicer with your income tax returns and paystubs.

- Most recent mortgage statement: When you call or apply, you may need to provide the most recent statement from your mortgage payments.

- An estimate of current monthly expenses: Along with your monthly income, you may also need to provide your servicer with an estimate of your monthly expenses, which include your monthly debt payments, such as student loans, car loans or credit card payments.

- An estimate of other assets: You may also need to provide your servicer with information about your other assets, such as how much cash you have in the bank.

Keep in mind that to qualify, you may need to put in your request for mortgage forbearance within a specific period after the natural disaster or change in circumstances. For example, your servicer may mandate that you request mortgage payment assistance within a month of filing for unemployment.

What If My Mortgage Forbearance Request Gets Denied?

If your servicer denies your application for mortgage forbearance, you may be able to appeal the decision. When you do so, a different loan officer who was not involved in the original decision will review the application you submitted. After this person goes over your application, you will receive an updated decision.

If you are still facing difficulty in reaching an agreement with your loan servicer, you may be able to find help elsewhere.

- Housing counselors approved by HUD: You may be able to discuss your situation with a housing counselor who has received approval from the U.S. Department of Housing and Urban Development. A housing counselor may discuss your options with you, such as a modified payment program.

- Lawyers: One option you may want to consider is reaching out to an attorney who may be able to provide you with legal resources and assistance.

- Credit counselors: If you are struggling to come to an agreement with your servicer, you may want to contact a credit counselor. Counselors typically work for nonprofit organizations and can advise you on your debts, money and budget. You may also receive assistance in negotiating with creditors.

During times of worldwide uncertainty, business shutdowns and staggering unemployment rates, you should pursue every option at your disposal for mortgage relief.

What Mortgages Qualify?

Which types of loans can you use mortgage forbearance for? To qualify for forbearance, mortgages must have backing from a federal agency or be federally owned. The new federal law known as the Coronavirus Aid, Relief and Economic Security Act, abbreviate as the CARES Act, has put new protections in place for homeowners who have federally backed mortgages. These protections are:

- A right to mortgage forbearance for the homeowners who are dealing with financial hardship as a result of COVID-19

- A foreclosure moratorium

If you are unsure who backs or owns your mortgage, you can take action using the following methods.

- Contact your loan servicer: You can ask the servicer of your mortgage about who backs your loan. Your servicer may be able to provide you with the name, address and contact information of the agency that owns your mortgage loan.

- Check online: You can use a lookup tool online via Fannie Mae or Freddie Mac to determine if one of these entities is backing your mortgage.

Government-Backed Mortgages

One of the following federal agencies may back mortgages that qualify for mortgage forbearance:

- Fannie Mae or Freddie Mac

- The U.S. Department of Veterans Affairs for VA loans

- The Federal Housing Administration for FHA loans

- The U.S. Department of Agriculture for USDA Rural loans

- The U.S. Department of Housing and Urban Development, also known as HUD

Mortgages the Government Doesn’t Back

What if you don’t have a federal agency backing your mortgage? Although the CARES Act may not require private servicers to offer relief, you may still be able to successfully apply for mortgage forbearance.

In the case of a natural disaster or national uncertainty, private mortgage servicers may adopt similar policies to those of federally backed loans. If a federal agency doesn’t back your loan, you can contact your servicer to ask what home loan relief programs they have available.

Similarly to a federally backed loan, if you and your servicer agree to mortgage forbearance or a loan modification, your bank will probably not report your paused or reduced payments to the credit bureaus.

Requesting Mortgage Forbearance or Relief

Under the CARES Act, you may have two relief options for a federally backed mortgage. Beginning March 18, 2020, the law has prohibited your servicer from foreclosing on your home for 60 days. If you are experiencing financial hardship as a result of COVID-19, you have the right to put in a request for mortgage forbearance for up to 180 days.

Beyond the scheduled amounts, you will not need to worry about penalties or additional interest or fees. The CARES Act also does not require you to submit additional documentation to your servicer to qualify for mortgage forbearance, other than your claim of financial hardship related to the pandemic.

You may also have other mortgage relief options from your state. Several states are considering or are implementing various options for home loan relief, so check your state’s website for further details.

What should you do after you have received mortgage forbearance or another mortgage relief option? Consider doing the following to further protect yourself.

- Monitor your mortgage statement: Monitor your mortgage statements every month to determine whether there are any errors.

- Store your written documentation: In case any errors arise on your mortgage statements, you may want to keep the written documentation available.

- Pay attention to your credit: You may also want to pay attention to your credit score to ensure that are no inaccuracies or errors.

- Contact your servicer once your income returns to normal: When your mortgage is in forbearance, you will need to pay your missed payments. However, with fewer missed payments, you will owe less later, so you should let your servicer know as soon as your income levels get back to normal.

If you can save money now, you may want to consider putting it away for later, when your payments are due.

Learn More About Mortgage Forbearance From Assurance Financial

At Assurance Financial, we can assist you with all of your mortgage needs. We use the technology that can help you get the mortgage loan you need as soon as possible, and we will provide you with end-to-end support so you can go through the entire process of applying for a mortgage loan under a single roof.

During times of global uncertainty, we still strive to provide you with stability and missed payment forgiveness. Our loan officers at Assurance Financial have a presence across the nation in 28 states and can assist you with any of your mortgage needs. To learn more about mortgage forbearance, reach out to a local loan officer or contact us at Assurance Financial.

Sources