Need a Little More Room to Roam?

A USDA RD Loan is designed to enhance the quality of life for Americans in designed rural and suburban areas. It’s perfect for low- and moderate-income borrowers because it offers flexible credit and underwriting terms and 100% financing. Other benefits include:

![]() No down payment required

No down payment required

![]() Not limited to first-time homebuyers

Not limited to first-time homebuyers

![]() 30-year fixed rate terms

30-year fixed rate terms

![]() Allows seller contribution to closing costs

Allows seller contribution to closing costs

Find out more about this program and eligibility from your Assurance Financial Loan Officer.

RESOURCES

Downloadable Guides

We’ve created these guides to be a valuable resource to walk you step-by-step through your next adventure.

-

First-Time Homebuyer Guide

4.6 MiB

Thanks for your interest in learning more about your mortgage options! We hope you find this information helpful. If you have more questions, please feel free to contact us anytime.

Click here to download the file -

Refinance Guide

4.35 MiB

Thanks for your interest in learning more about your mortgage options! We hope you find this information helpful. If you have more questions, please feel free to contact us anytime.

Click here to download the file

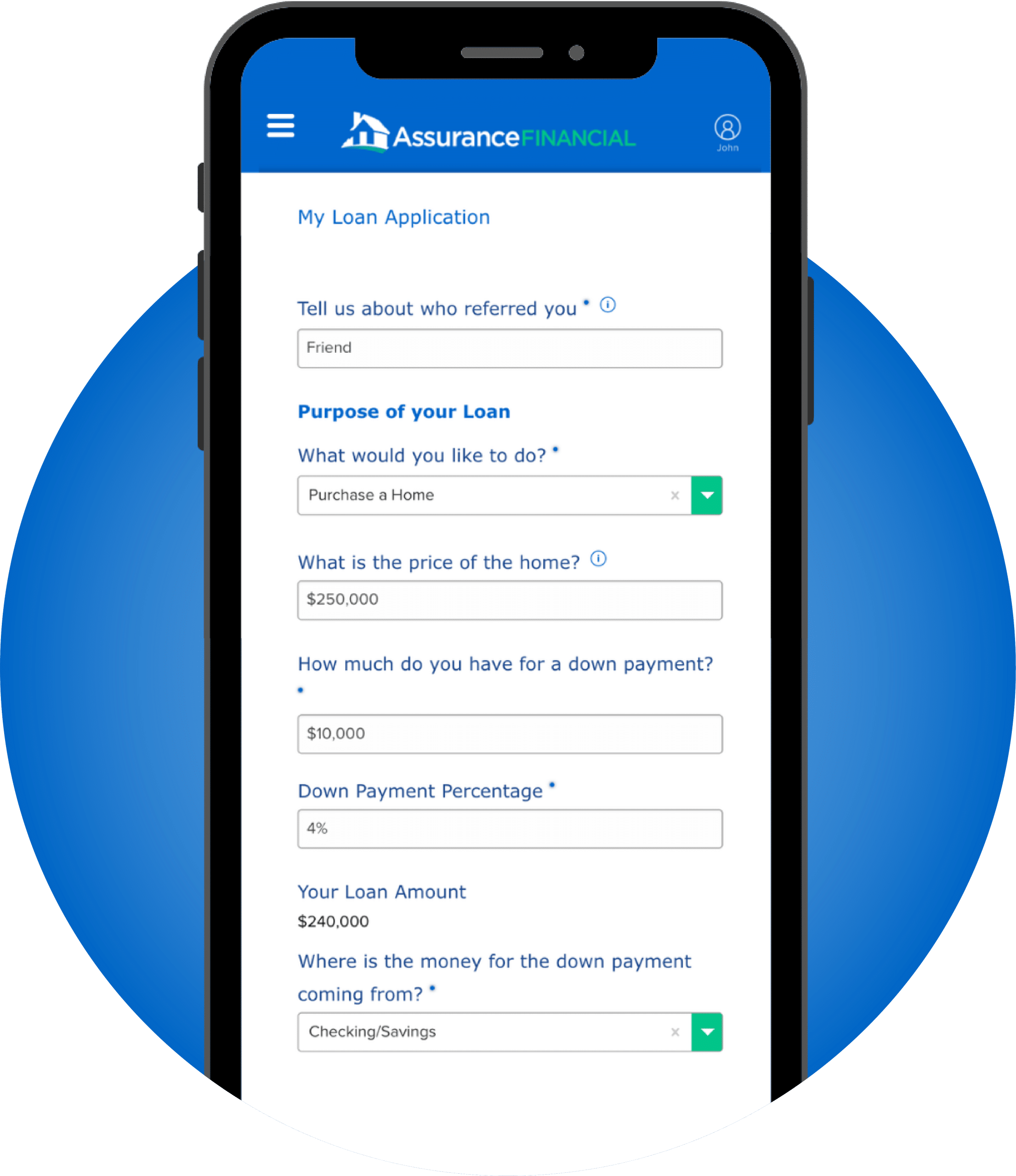

How to Get Started

There are several ways to begin the loan process.

Explore all the loans we provide

Need help with your application? We're here to lend a hand.

Our easy digital application walks you through every step of the process in terms you can actually understand. Plus, we’re always a phone call away if you get stuck.

start your application

Speak with an expert!

We have friendly experts to answer your questions. Find a loan officer licensed in your state.

Find A Loan Officer

Did we miss anything?

You still have questions, we still have answers. Take a look at what other people have been asking.

Read FAQs

If you live in a suburban or rural area, you may have more options for home loans than you realize. Government-backed mortgages called USDA loans may allow you to buy a home or even a farm.

What Is a USDA Home Loan?

The U.S. Department of Agriculture (USDA) mortgage program, sometimes also referred to as the USDA Rural Development Guaranteed Housing Loan Program, insures home loans. Loans guaranteed in this way allow eligible borrowers to enjoy great rates and other benefits.

The USDA loan program is designed to improve quality of life for low- and medium-income Americans living in designated suburban and rural areas. USDA financing may allow you to buy property with zero down. In fact, you may even be able to roll closing costs into your USDA mortgage, which truly makes this home loan one of the few that allows for 100% financing of your home.

Another benefit is that this form of financing has one of the lowest mortgage insurance rates in the industry — only VA loans for veterans have lower mortgage insurance. You can also avoid having to pay mortgage insurance entirely by making a larger down payment.

If you’re asking “what is a USDA loan?” you may be interested to learn there are three USDA programs for home loans:

- Guaranteed loans: You can get this loan through a traditional lender, and the USDA guarantees it. Since there is less risk for the lender, you enjoy low interest rates on your loan, and you may not need to have a down payment at all.

- Home improvement loans: You can get grants and loans to improve your home or upgrade it, up to a set limit.

- Direct loans: For those with a very low income, the USDA directly issues loans. The exact income requirements vary by area. In addition to the loans, homebuyers may qualify for subsidies that can lower interest rates to 1%.

Do I Qualify for a USDA Home Loan?

If you do not qualify for a traditional home loan and are challenged by having to save up for a down payment on a rural property, USDA mortgage loans may be an option for you. These loans are specifically designed to be affordable and accessible.

Contrary to what you may think, you do not have to be a farmer or interested in farming to get a USDA loan. While you can use this type of loan to buy a farm, you can also use it to buy any residential, owner-occupied home in any rural and some suburban areas. Even if you have no interest in growing crops or anything else, you can use a USDA loan to buy a home in any eligible area, as long as you meet income and other requirements.

If you’re wondering how to get a USDA loan or whether you qualify, you may wish to contact Assurance Financial to find out more about requirements in your area. Reach out to a loan officer near your location to speak to a live person about your situation.

USDA Home Loan Requirements

If you’re wondering how to qualify for a USDA loan, you need to meet these requirements:

- Citizenship: You must have U.S. permanent residency or citizenship.

- Income: You must meet certain income requirements, meaning you cannot be earning more than a specific amount. The income limits vary by region.

- Type of property: The property you are buying with your USDA financing must be your primary residence and must be owner-occupied. You cannot use this loan to buy a vacation home, rental property or income property.

- A debt ratio of 41% or less: If your credit score is 680 or less, your monthly payment for the loan must be no more than 29% of your income each month. Your debt ratio cannot be higher than 41% unless you have a credit score over 680, but speak with one of our licensed loan officers to best understand your options.

- Income: You must show you have had reliable income for at least the past two years.

- Property location: Rural development lenders offering this type of financing offer loans in rural and some suburban area. Talk to a lender or the USDA to determine which areas of your region qualify.

- Credit history: While credit requirements for a USDA rural development loan are not as strict as they are for convention loans, your credit score still matters. You must not have had any collection over the past year, and your credit must be reasonable. If your credit has some challenges, you may still qualify if you can prove exceptional circumstances caused the credit problems. In general, if your credit score is 680 or higher, you may qualify for streamlined processing of your loan, although having a lower score may not prevent you from getting a mortgage.

Our USDA Loan Process

Assurance Financial understands it can be daunting to apply for a home loan — especially if you have never applied before, or if you have been rejected for financing in the past. Fortunately, USDA loans can be easier to qualify for.

If you like the idea of living on a farm or in a more rural area and would be interested in applying for a loan backed by the USDA, Assurance Financial may be able to help. With us, you can apply online for a quote on a mortgage in just 15 minutes or you can apply by speaking to a person. We can pre-qualify you by looking at your credit score and other details.

When you find a rural property you like, you can fill out a full loan application with Assurance Financial. We are USDA mortgage and construction loan lenders who can handle your application from start to finish in-house. We do not outsource underwriting and other processes.

Processing your application involves appraisal and underwriting. We then make a decision about your application. If you are eligible for a mortgage and we can fund your mortgage, the next phase of the process involves signing with a notary and funding and closing the mortgage. At that point, you can start planning your move and packing your boxes.

Assurance Financial is made up of people people. At every step, we answer your questions and help you understand exactly what you need to do to apply. We also offer a wide range of loans, so whether you want to buy a farm or a home or build or renovate a property, we have the resources and loan products to help.

Contact Assurance Financial Today to Learn More About USDA Financing

USDA financing can offer hope to rural residents and would-be rural homeowners who might not qualify for a mortgage with a conventional home loan. For those with a modest income and desire to live the American dream by owning a home, this form of financing is one option.

Are you curious to learn more? Assurance Financial is eager to give you details. You can contact a local loan officer to speak to a mortgage expert.