Go Ahead - Think Bigger - Apply for a Jumbo loan

Whether you’re in one of the nation’s highest pricing markets, or your dream home exceeds a conforming loan limit, financing a loan that is larger than conforming limits is one of our specialties. As a private bank, we may be able to offer more.

![]() Fixed or adjustable rates (ARM)

Fixed or adjustable rates (ARM)

![]() Can be used to purchase, refinance and cash-out

Can be used to purchase, refinance and cash-out

![]() Available for owner-occupied, second homes, and investment properties

Available for owner-occupied, second homes, and investment properties

![]() Financing for almost all types of properties, from single- and multi-family homes to condominiums and even manufactured homes.

Financing for almost all types of properties, from single- and multi-family homes to condominiums and even manufactured homes.

Find out more about this program and eligibility from your Assurance Financial Loan Officer.

RESOURCES

Downloadable Guides

We’ve created these guides to be a valuable resource to walk you step-by-step through your next adventure.

-

First-Time Homebuyer Guide

4.6 MiB

Thanks for your interest in learning more about your mortgage options! We hope you find this information helpful. If you have more questions, please feel free to contact us anytime.

Click here to download the file -

Refinance Guide

4.35 MiB

Thanks for your interest in learning more about your mortgage options! We hope you find this information helpful. If you have more questions, please feel free to contact us anytime.

Click here to download the file

How to Get Started

There are several ways to begin the loan process.

Explore all the loans we provide

Need help with your application? We're here to lend a hand.

Our easy digital application walks you through every step of the process in terms you can actually understand. Plus, we’re always a phone call away if you get stuck.

start your application

Speak with an expert!

We have friendly experts to answer your questions. Find a loan officer licensed in your state.

Find A Loan Officer

Did we miss anything?

You still have questions, we still have answers. Take a look at what other people have been asking.

Read FAQs

Sometimes, your dreams of homeownership are big. When your ideal home exceeds the conforming limit established by government agencies, jumbo loans may be able to help you buy the property.

What Is a Jumbo Loan?

The Federal Housing Finance Agency (FHFA) sets certain limits for mortgage sizes. In addition, a conforming loan must abide by rules established by Fannie Mae or Freddie Mac, both of which are government-controlled agencies. When a home loan exceeds the limits set by these bodies, you need a jumbo home loan.

What constitutes a jumbo loan? These mortgages are conventional nonconforming loans that are not backed by any government agency or by Freddie Mac or Fannie Mae.

The limit of mortgage you can have before you need a jumbo loan changes and varies by location, but as of 2020, the jumbo mortgage limit in most of the country is $510,400. The limit varies depending on the markets in high-cost areas. Any loans exceeding the jumbo limit require a jumbo loan.

The limit for a one-unit property in a high-cost area is $765,600. These are the 2020 limits, and we will be keeping track of updates on loan limits in 2021. Review FHFA’s conforming loan limits map for more information on your location’s loan limit.

Like many mortgages, jumbo loans come in many forms, so you can choose the type of financing that suits your needs. You can get a fixed rate or an adjustable rate if you do not plan on being in your home for very long. You can also choose different terms.

You may wish to use calculators to determine the most affordable monthly payments and interest rate for your loan. Since a jumbo loan involves a large sum of money, small variances in rates and terms can have a significant impact on your monthly payment.

A jumbo loan is ideal for an experienced homebuyer who may have considerable assets but who may not necessarily have liquid assets that can be used to purchase a property. A jumbo loan may also be the right option for a higher-income earner who has not yet accumulated significant assets but who has the income to take out bigger loans.

Jumbo Loan Requirements

Since more money is involved with jumbo mortgages and since there isn’t an agency guaranteeing the loan, a lender faces more risk. As a result, the requirements for a jumbo loan are stricter in comparison to conventional conforming home mortgages. To qualify for a jumbo loan, you will need:

- A good down payment: You may need 10% or more of the home’s asking price as a down payment. Depending on your situation and your lender, you may also be asked to supply a 20% or even 30% down payment.

- Low debt: Lenders may wish to see debt-to-income (DTI) under 43% or close to 36%. You can use a calculator for jumbo loans to determine whether you qualify.

- Proof of income: You will need to supply W2 tax forms and pay stubs that date back two years and 30 days, respectively. You will also need at least 60 days of bank statements and two years of tax returns if you are self-employed. Additionally, you may be required to show paperwork proving any liquid and non-liquid assets. Your liquid assets may need to be significant enough to cover six months of home loan monthly payments.

What Credit Score Do I Need for a Jumbo Loan?

In general, you may need to have a credit score of 700-720. Depending on your specific situation and the loan you are applying for, you may need a credit score that exceeds this range. Additionally, having a higher credit score than the required minimum could help you receive the best possible jumbo loan mortgage rates.

To determine what requirements you may need for your specific circumstances, such as your credit score, you can speak with one of our loan officers.

How to Get the Best Jumbo Loan Mortgage Rates

If you are eligible for a jumbo loan and are looking to finance your dream home, it’s not enough to meet conventional jumbo loan requirements. Of course, you also want the best terms possible.

To get the best rates, there are a few things you can do:

- Increase the size of your down payment: In the past, these mortgages required down payments of 30%, and while you may qualify for a home with a smaller down payment, paying more upfront reduces the risk for jumbo loan lenders. Paying a larger down payment can also help you reduce your monthly payments and can encourage your lender to give you a more attractive rate.

- Improve your credit score: Even with a credit score of 700, you may want to consider trying to increase your score so you qualify for the best rate. Paying down your debts and paying your bills on time can help. You can automate your payments so none of your payments are late.

- Talk to a lender: A mortgage expert at Assurance Financial can review your homeownership goals and discuss different types of loan products. Assurance Financial can also offer you a free, no-obligation quote. If you realize you want a lower rate, a member of our team can discuss your options with you so you understand what you can do to get the best rate possible.

- Pay down your debts: Paying down your debts lowers your debt-to-income ratio, and the closer your DTI is to 36%, the better the chances are of getting approved for a loan. You can also improve the odds of a good rate by lowering your debt overall.

- Work on improving your financial life: The lower a risk you are to lenders, the more willing they may be to give you an excellent rate. You can improve your finances by taking on a better job, getting promoted and finding ways to make more money. Staying with your current job and working to show employment stability can also help.

Many assume that because a jumbo loan carries more risk than a conforming loan, lenders charge higher interest rates. However, data shows that jumbo loan rates are competitive with market rates. In recent years, these rates have dropped to a historic low. Additionally, some of the interest on your mortgage may also be tax-deductible.

Today, the difference in interest rates between a conforming loan and a jumbo loan is minimal. Some jumbo loans even have lower rates than other types of mortgage loans. As of 2020, the Federal Reserve cut interest rates to 1% in March, then to 0.25%. In October, the rate was 0.09%.

Though the Federal Reserve does not set mortgage rates directly, its actions have an effect on the market. After the first interest rate cut, the average rate was 3.29% for a 30-year fixed mortgage. In September 2020, the average mortgage interest rate was 2.89%.

Apply for a Jumbo Loan Online Today

If you’ve found your dream home, but it is above the limits that have been set by FHFA, you may want to consider applying for a jumbo loan. Fortunately, Assurance Financial can make the process of applying for a mortgage simpler.

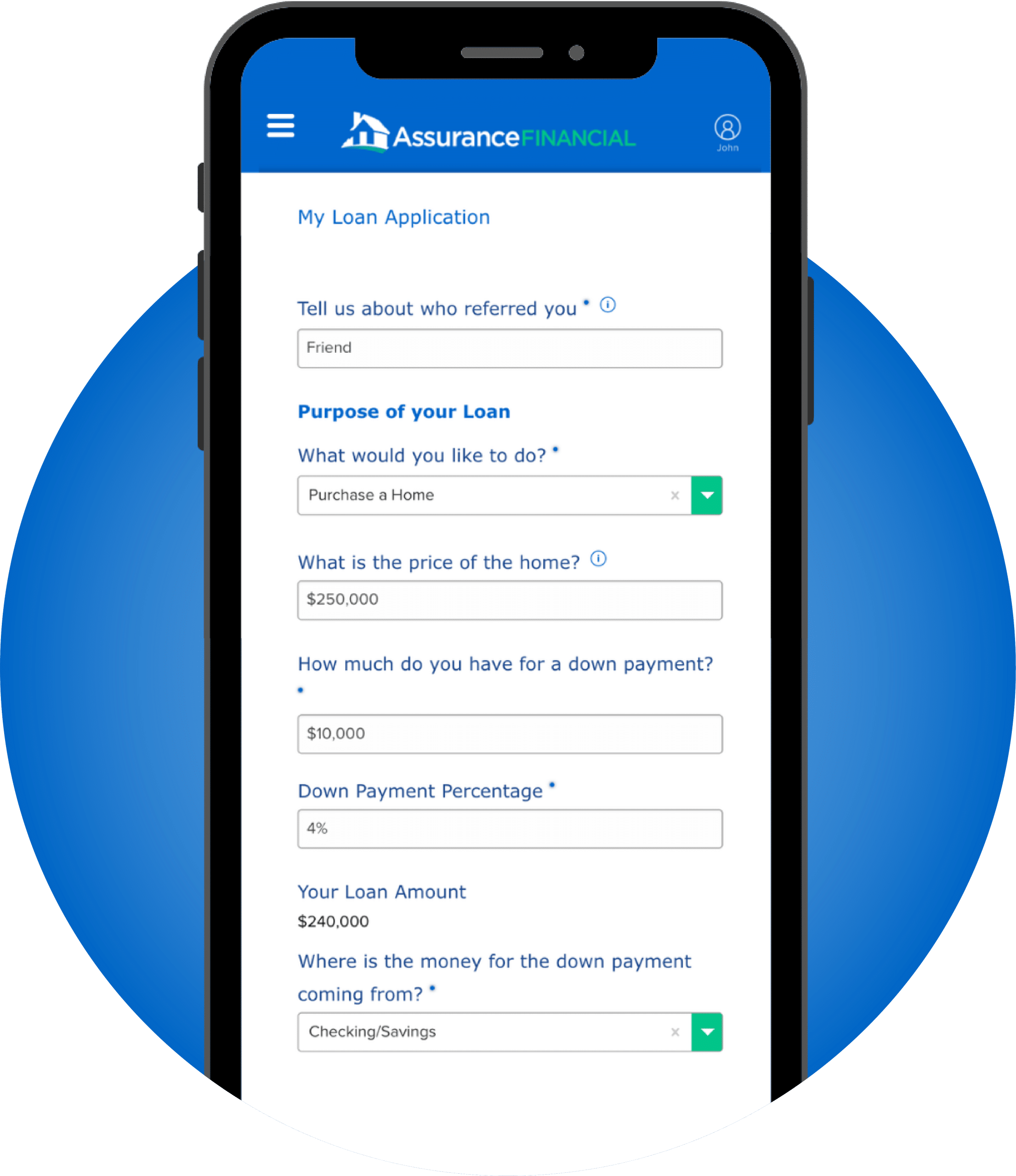

At Assurance Financial, you can be pre-qualified online in as little as 15 minutes. We don’t even require you to fax over documents. Our virtual assistant will walk you through the application and how to verify your information with payroll and banking. You can also choose to apply with a mortgage expert.

Once we have looked at your initial application, we can offer a free, no-obligation mortgage quote, so you can see how much you may pay in interest. If you find your dream home and decide to apply, you can fill out the longer application form and submit the required documentation. Our mortgage experts can help you at every stage of the process.

Once we have your application, we handle all processing in-house, including the underwriting. Once appraisal and underwriting are complete, we may be able to approve your loan. At that stage, the loan is closed and funded after a signature with a notary is secured. Then, you can work on moving and interior decoration.

Of course, if you have any questions or need help, our loan officers are there to address any concerns and to help you.

If you’re ready to stop dreaming about your home and start living in it, get started on the path to homeownership with a mortgage. You can contact a local loan officer to speak to another person.