Key Takeaways

- FHA loans accept lower credit scores with a 3.5% minimum down for mid-high scores or 10% for lower scores, while conventional loans require higher credit scores.

- FHA loans mandate mortgage insurance (both upfront and annual premiums) for the entire loan term, whereas conventional loans only require optional annual PMI when the down payment is under 20%.

- FHA loans are limited by county median home prices and require fixed rates with strict property standards, while conventional loans offer more flexibility in loan amounts and rate options.

No, it’s not just you. Understanding conventional versus Federal Housing Administration (FHA) loans can feel like learning another language. Throw in terms like private mortgage insurance, debt-to-income ratios, interest accrual and insurance premiums and suddenly you feel like calling to give Fannie and Freddie a piece of your mind.

Understanding these two home mortgage options is key to making an informed decision. Let’s break down the ins and outs of conventional versus FHA loans so you can feel empowered in choosing the right loan for your financial health.

- What Are FHA Loans?

- What Are FHA Loan Requirements?

- Other Questions to Consider Before Getting an FHA Loan

- Are There Any Purchasing Restrictions or Limitations on FHA Loans?

- Who Is an FHA Loan Best For?

- Who Should Not Get an FHA Loan?

- What Is a Conventional Loan?

- Conventional Mortgage Requirements

- How Do Purchasing Restrictions and Limitations Compare to FHA Loans?

- Other Questions to Consider Before Getting a Conventional Mortgage

- Comparing FHA Versus Conventional Loans Limitations

- Comparing Credit Score Requirements for FHA Versus Conventional Loans

- Are Down Payments Different for Conventional Loans Versus FHA Loans?

- How to Choose the Right Mortgage for You

What Are FHA Loans?

Federal Housing Administration (FHA) loans are home mortgages insured by the federal government. Generally speaking, it’s a mortgage type allowing those with lower credit scores, smaller down payments and modest incomes to still qualify for loans. For this reason, FHA loans tend to be popular with first-time homebuyers.

The goal of FHA mortgages is to broaden access to homeownership for the American public. While FHA loans are insured by the federal agency with which it shares its name, you still work with an FHA-approved private lender to procure this mortgage type.

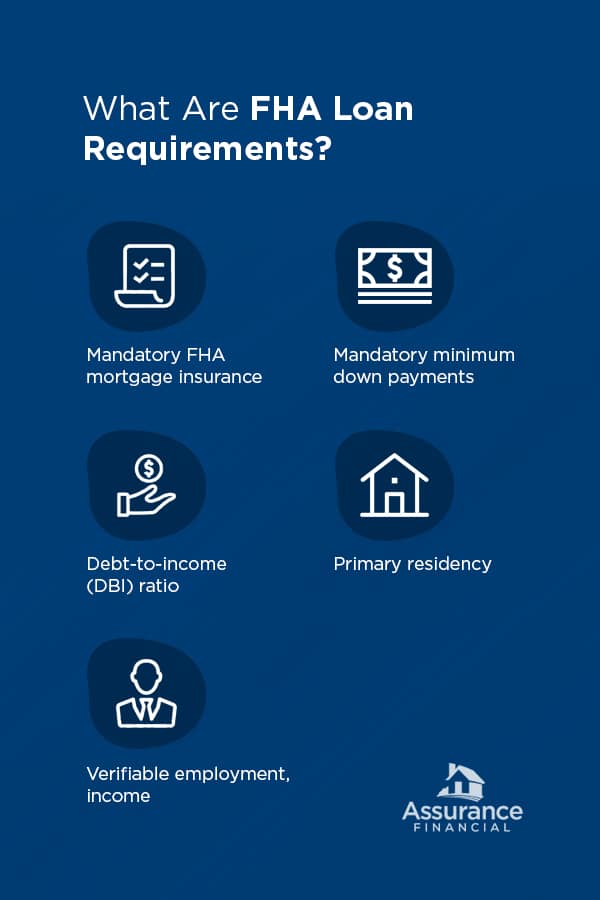

What Are FHA Loan Requirements?

Every year, the Federal Housing Administration, along with a slew of assisting government agencies, publishes their 1,000-plus-page FHA loan handbook.

If federal loan manuals (or should we say manifestos) don’t make your reading list cut, no problem. We’ve summed up the top FHA loan requirements applicable to today’s prospective home buyers:

- Mandatory FHA mortgage insurance: Borrowers with FHA loans must also pay FHA mortgage insurance. With conventional loans, mortgage insurance is optional and only mandatory when your down payment is less than 20 percent of the home’s value. However, this rule is less of a “gotcha” tactic and more of a market stabilizer, since FHA mortgage insurance covers your lender if you end up defaulting on your loan.

- Mandatory minimum down payments: FHA loan qualifiers pay down payments partially dictated by credit score. Credit scores on the lower end of the spectrum typically require a 10 percent down payment. Mid-range to high credit scores typically are able to put down around 3.5 percent.

- Debt-to-income (DTI) ratio: DTIs calculate the amount of money you spend every month on outstanding debts compared to your total income. To secure an FHA loan, qualifiers typically have a DTI of 30 to 50 percent. Generally, the lower the DTI, the more competitive the borrower.

- Primary residency: All properties a buyer intends to use their FHA loan on must be considered their primary place of residence, not a vacation or rental property.

- Verifiable employment, income: Like most loan types, you must provide a minimum of two years of employment history or verifiable income to qualify for an FHA loan. (Think pay stubs, federal tax returns or bank statements to name a few.)

Note: FHA’s mandatory mortgage insurance requires borrowers to pay not one but two mortgage insurance premiums: Upfront premiums and annual premiums.

- Upfront mortgage insurance premium: Currently, upfront insurance premiums for FHA loans are a small percentage of the total loan amount. It is paid as soon as the borrower receives their loan.

- Annual mortgage insurance premium: Like upfront mortgage insurance premiums, annual mortgage insurance premiums are calculated based off of a small percentage of the total loan amount.However, variables like loan terms (15 or 30 years) also influence rates. This premium is paid monthly, with installments calculated by taking the premium rate and dividing it by 12 months.

Other Questions to Consider Before Getting an FHA Loan

FHA loans are designed to be a more generous pathway to homeownership. Its underwriting standards are geared toward buyers who may not have traditionally lender-attractive credit scores or incomes but can still prove limited liability.

With that said, there are a handful of questions to ask before securing an FHA mortgage.

1. Are There Any Purchasing Restrictions or Limitations on FHA Loans?

Yes. Your FHA loan terms will maintain the following stipulations:

- Loan amounts: FHA loan amounts are dictated by a county’s median home price. While some exceptions exist, your qualifying FHA loan amount will fall near that median county value, known as its floor or ceiling amount. Also note: For the majority of U.S. home markets, FHA loans have limits on the cost of the home purchased — making a home outside this price range generally unattainable.

- Fixed interest rates: FHA loans only carry fixed, not variable, interest rates.

- Premiums: Remember those two types of FHA mortgage insurance premiums described earlier? Annual premiums can be refinanced, but only by turning the loan into a non-FHA mortgage or after you sell your home.

2. Who Is an FHA Loan Best For?

Since FHA mortgages are easier to qualify for, they’re particularly attractive for individuals in the following circumstances:

- Young or first-time homebuyers: Over 80 percent of all FHA loans lent in the past two years have been to first-time homeowners.

- Househunters with smaller savings: FHA loans statistically court lower down payments. Buyers with less competitive down payment capabilities may find FHA terms more favorable.

- Househunters with modest or variable income: The lower interest rates on most FHA loans can provide breathing room for buyers with tighter budgets or variable income, including freelancers or those who are self-employed.

3. Who Should Not Get an FHA Loan?

Borrowers turned off by the loan limit may find FHA mortgages too restrictive.

Likewise, most lenders recommend your monthly mortgage payments should not exceed 31 percent of your gross monthly income. Some private lenders offering FHA loans may allow up to 40 percent. If either of those rates proves to siphon too much of your monthly income, an FHA loan still may not be right for you.

FHA Loan Benefits

FHA loans carry several unique advantages.

1. Thoroughness of Property Appraisals

Property appraisals for FHA loans are extensive. Compared to conventional loan property assessments, inspectors will conduct a detailed analysis of the safety, structural integrity, design, HUD property guideline alignment and true value of your desired home, as well as compliance with local ordinances and standards.

2. Easier Approval

FHA-approval standards involve lower credit scores and more forgiving debt-to-income ratio allowances. Data from the Department of Housing and Urban Development show that a significant portion of FHA qualifiers maintain average credit scores or above.

3. Fixed Interest Rates

When it comes to fixed versus variable interest rates, one isn’t necessarily superior to the other. Depending on your financial situation and general risk tolerance, though, the fixed interest rates of most FHA loans may provide more budget stability than fluctuating ones.

4. Closing Costs

FHA loans typically have lower closing costs due to restrictions on the amount the lender can charge. This restriction works as a cost control for new home buyers.

What Is a Conventional Loan?

Conventional loans are mortgages issued through private lending institutions, such as banks and mortgage lenders.

Unlike FHAs, conventional loans are not insured by the federal government. They also can have fixed or variable interest rates, higher qualifying credit scores and more competitive down payment amounts affecting those interest rates.

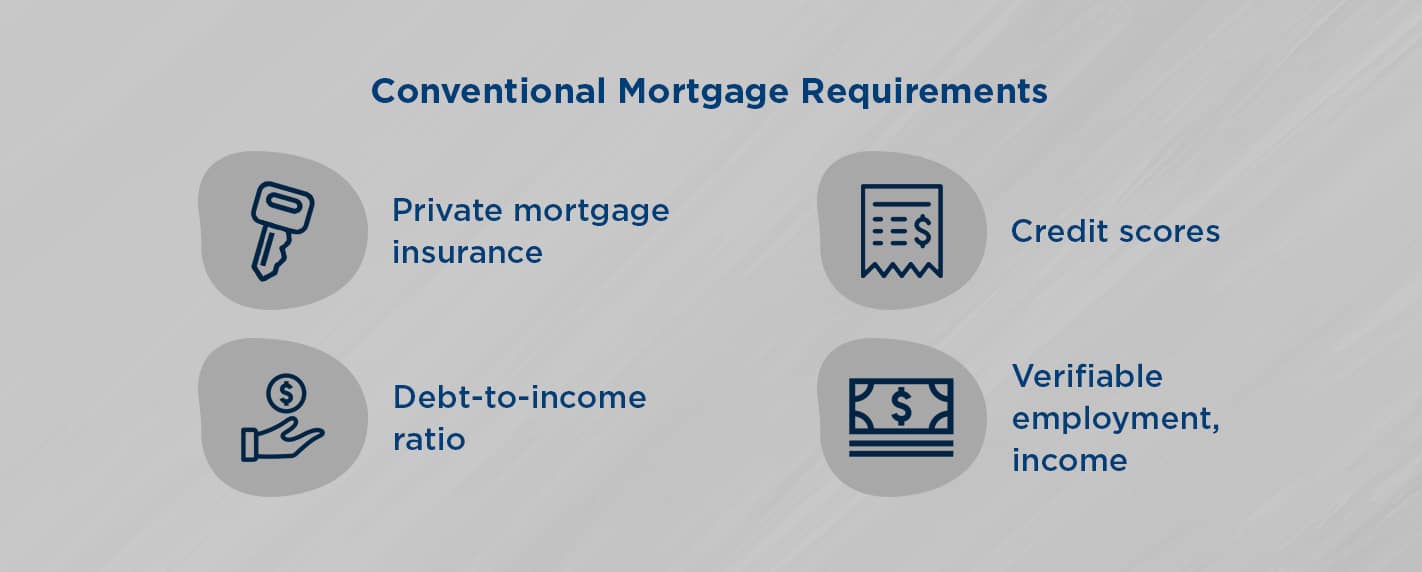

Conventional Mortgage Requirements

Borrowers considering conventional loans have stricter qualifications to meet private lender requirements. Some of these qualifications include:

- Private mortgage insurance: If a borrower provides a down payment of less than 20 percent, then they must additionally purchase mortgage insurance paid in monthly installments. However, down payments higher than 20 percent do not require private mortgage insurance.

- Credit scores: Most private lenders require a minimum credit score to be an attractive loan candidate.

- Debt-to-income ratio: Conventional lenders look favorably on lower DTIs. Conventional loan DTIs are also capped at a moderate or mid-range credit score, though exceptions exist for those with credit scores higher than 700, though exceptions may exist for borrowers with very high or even perfect credit.

- Verifiable employment, income: Like FHA loans, borrowers must provide proof of steady income and employment to qualify for a conventional mortgage. After-tax income requirements may be higher as well, depending on the lending institution.

How Do Purchasing Restrictions and Limitations Compare to FHA Loans?

Generally speaking, conventional mortgages carry more restrictions than their FHA counterparts. Private mortgages tend to require:

- Higher credit scores

- Higher monthly income

- Higher down payment amounts, namely to access lower interest rates

It’s important to remember that one mortgage type is not better than the other. Rather, FHA and conventional loans fit particular situations that are always best reviewed with a local loan officer.

Other Questions to Consider Before Getting a Conventional Mortgage

Conventional mortgages do involve several unique processes, both before qualifying and after you’ve been approved. Consider the following questions if weighing a conventional loan against an FHA mortgage.

1. Who Is a Conventional Loan Best For?

Conventional loans work best for people in the following circumstances:

- People with high credit scores: If your credit score is 640 or above, conventional loans are advantageous.

- People house-hunting for vacation or rental properties: Conventional loans can be used on secondary properties or homes the owner does not occupy.

- People with a 20 percent down payment: Generally, putting down at least 20 percent lets you avoid private mortgage insurance — and the thousands of dollars PMI can cost over the course of your loan.

2. Who Should Not Go With a Conventional Loan?

Prospective homeowners with variable income or low debt-to-income ratios tend to have a harder time securing a conventional loan with favorable terms. Low debt-to-income ratios — meaning your monthly debt payments eat a larger portion of your income — make it particularly difficult to present as an attractive borrower to private lending institutions.

Conventional Loan Benefits

Borrowers who qualify for conventional mortgages experience several advantages:

1. No Upfront PMI, Optional Annual PMI

Conventional loans do not require upfront mortgage insurance. What’s more, annual PMI is not typically required if you meet the minimum down payment requirements, and in most situations PMI falls off your loan once you have paid off a certain percentage of the loan.

2. Flexible Loan Terms

Not only are conventional loans granted in higher values, but they come in more flexible timelines, too. Homebuyers can negotiate 10, 15, 20, 25 and 30-year conventional loans. Plus, any private mortgage insurance the buyer did take cancels once the loan’s total value (LTV) is 78 percent or less of the current value of the property.

3. Higher Loan Values

Private, conventional loans have higher ceilings than FHA loans. Mortgages backed by Fannie Mae and Freddie Mac can be secured a single-family home and reach up to higher amounts in higher housing markets.

Comparing FHA Versus Conventional Loans Limitations

There are a few major takeaways when comparing conventional loans versus FHA loans’ uses and restrictions.

- Owner Occupation: Conventional loans do not require the borrower to live in the property. FHA mortgages do.

- Refinancing: Refinancing is available for both FHA and conventional loans. However, conventional loans’ refinancing is more detailed, requiring a credit check, home reappraisal, income verification and more.

- High-cost and low-cost areas affecting loan values: Both FHA and conventional mortgages have loan floors and ceilings, i.e., the minimum and maximum values you can receive. FHA loans are determined by the median home value in a county. Conventional loans vary by county, state and lender but will generally follow Fannie Mae and Freddy Mac protection standards.

- Debt-to-income ratios: The lower your debt-to-income ratio (a.k.a. the closer the two numbers), the harder it will be to secure a conventional loan. Conventional loans typically accept DTIs in the 30-43 percent range; FHA mortgages can go up to 50 percent.

Comparing Credit Score Requirements for FHA Versus Conventional Loans

Credit scores are instrumental when determining loan eligibility for both types of mortgages.

- FHA loans generally accept modest credit scores: Borrowers with lower credit scores or credit challenges are frequently approved.

- Conventional loans generally favor higher credit scores: Borrowers tend to need moderate to high credit scores to receive opportune loan terms and rates.

Do remember, though, that for both types of mortgages, the lower your credit score, the higher your interest rates will be.

Are Down Payments Different for Conventional Loans Versus FHA Loans?

Yes. Conventional loans allow down payments of anywhere from 3-20 percent, with those above 20 percent receiving more favorable interest rates and no mortgage insurance.

FHA loans allow lower down payments for borrowers who meet credit requirements

How to Choose the Right Mortgage for You

There is no single “best” type of mortgage. Instead, prospective homebuyers should review their complete finance portrait to get an accurate representation of their homeownership maturity, then begin determining loan type from there.

- Know your credit score: Don’t beat yourself up if the number you discover isn’t where you want it to be. There are plenty of ways to raise your credit score and open the doors to more competitive mortgaging options.

- Be realistic about your down and monthly payment capabilities: Whether you rent or own, the budgeting golden rule is that your housing costs shouldn’t exceed 30 percent of your income. As you home shop, be realistic about what you can genuinely afford to spend on monthly mortgage payments as well as that initial down payment. Make calculations and set an actionable budget. This is one of the most important steps to take not only when house hunting but also when choosing a loan type for that home.

- Do your housing market research: FHA and conventional loan values are tied to their immediate markets. Familiarize yourself with the pricing structures and values of neighborhoods you’re considering before contacting a loan agent.

- Calculate the total cost of ownership: Consider the “hidden” costs associated with the mortgage and homebuying process, including insurance, fees, closing costs and mandatory premium payments. When tallied, these add considerably to your total monthly housing expenditures. It can also mean the loan offer with the lower interest rate might not be the savviest option in the long term.

- Consider consulting a mortgage broker or loan officers: These are individuals who have made a career navigating the complexities of the mortgage world. If you have questions, they’ll have answers.

The Bottom Line?

Buying a home is one of life’s greatest achievements — but for many, it’s also one of its most daunting.

Don’t be intimidated! Choosing between an FHA or conventional loan is a significant process but one with many options for guidance and assistance.

If you’re looking into getting a mortgage, reach out. Assurance Financial supports online applications for both FHA and conventional loans and has loan officers on staff who are ready to walk you through every step of the process.

Popular Loan Types

- First Time Home Buyer Loans

- FHA Loans

- Conventional Loans

- Construction Loans

- VA Loans

- Jumbo Loans

- Refinancing