When it comes to renting vs. buying a home, many people may feel overwhelmed by how to make the best decision for themselves. Is it better to rent or get a mortgage? Are there situations when it’s better to rent?

Ultimately, the decision to rent or buy is a personal one and is a question that you may answer differently at various stages of your life. If you’re trying to decide whether to rent or buy, you’ll want to base your decision on your finances, your lifestyle, your location and your goals. In this article, we’ll cover renting vs. buying pros and cons as well as reasons to buy or rent.

- When You Should Buy vs. When You Should Rent

- When to Buy

- When to Rent

- Reasons to Buy a Home

- Types of Loans That Make Sense

- Great Buying Locations

- Reasons to Rent

- Locations That Are Better for Renting Longer

- Securing a Home Mortgage With Assurance Financial

When You Should Buy vs. When You Should Rent

Whether you rent or buy is a personal choice. There’s no right answer that’s best for everyone, and the choice can change for a person throughout their life. Renting may be the right option for you right now, and owning a home may be the right option for you in three years. If you’ve taken a job in another state, renting might be the best option for you until you find a home to buy in your new area. Maybe you live in an area where it makes more sense financially to buy than rent.

Whatever your situation may be, there are a few key factors that can help you determine when you should consider paying a mortgage vs. paying rent.

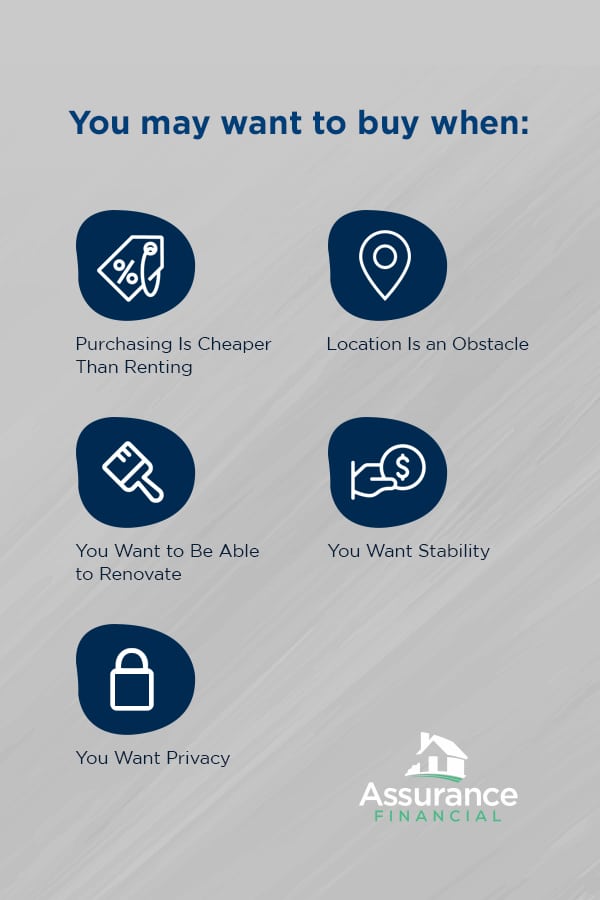

When to Buy

If any of these apply to you, you may want to consider buying.

1. Purchasing Is Cheaper Than Renting

You can use an online calculator to play with the numbers and discover which may be the better financial option for you. Generally, rent may be the better financial option in the short-term, but buying is usually cheaper over the course of a few years.

For example, if you stay in your home for two years, buying a $100,000 home with a 20% down payment of $20,000, at an interest rate of 3.75% over a 30-year loan term, is cheaper than renting a home for $800 a month. If you only stay for one year, renting is cheaper.

If you pay $200,000 for a home with a 20% down payment of $40,000 with the same interest rate and loan term, you would have to stay in your home for five years for buying to be cheaper than a monthly rent of $800. At a rent of $500 a month, however, buying is never cheaper than renting, though the savings between them does become quite minuscule.

2. Location Is an Obstacle

In some areas, there simply may not be any properties for rent. If your heart is set on a certain location, then your only viable option may be buying a home.

3. You Want to Be Able to Renovate

When you rent, you can’t change anything about your home without permission from the owner. If you enjoy decorating and making a space your own, you may feel restricted when renting a home that you can change only with your landlord’s permission.

4. You Want Stability

When you’re not tied to a lease and beholden to a landlord, you get to choose when you move. With the right loan, you’ll also get the financial predictability of a consistent monthly mortgage payment.

5. You Want Privacy

When renting, you may also have less privacy than you would if you owned a home. Generally, landlords must give notice before they’ll be entering a tenant’s home, but in an emergency, the landlord may come in unannounced.

When to Rent

On the other hand, you may want to rent if any of these describe your situation.

1. You Can’t Afford the Upfront Costs

If you don’t have enough savings to cover the transaction costs of purchasing a house, then you may want to rent. Buying a home can bring with it some hefty initial costs, such as inspection fees and a down payment. A down payment alone can be as much as 20% of your home’s cost depending on the type of mortgage loan you secure. You may also have to deal with other fees that can amount to thousands of dollars, including closing costs that can be as much as 3 to 5% of the loan amount.

2. You Won’t Be Able to Cover Unexpected Maintenance Expenses

If you don’t have extra savings set aside to pay for unexpected maintenance costs or the financial ability to save up and pay for those major repairs, then it may not be the right time for you to buy a home.

3. You Aren’t Comfortable With Risk

Homeownership can also be riskier than renting. Your home is an asset and could be at risk for expensive damages, especially any damages not covered by insurance that then become a financial burden you have to shoulder alone.

4. You Don’t Want to Deal With or Pay for Home Maintenance

If you don’t have the desire to maintain a home, then owning may not be the right option for you. Homes require a fair bit of maintenance and upkeep, such as mowing the lawn, cleaning the gutters and keeping appliances in working order. This maintenance can cost you either time if you perform the tasks yourself or money if you choose to outsource the job to someone else.

Reasons to Buy a Home

In many cases, it’s usually better to buy a home rather than rent one. Here are a few reasons you should buy a home:

1. You Will Eventually Pay off Your Mortgage

The main difference between rent and a mortgage is that, when you buy a home, you eventually will no longer have a mortgage on your house. Then, you’ll only be responsible for paying your taxes, insurance and maintenance costs. When you rent, those rental payments never stop as long as you continue living in that home.

Some may argue that when you’re renting, you don’t have to worry about paying taxes, insurance or maintenance costs, but that’s exactly where your rent money is going –– to cover the property’s expenses and then some so the owner can make a profit. When you’re renting, you simply don’t know how much of your rent is going toward those costs and how much is going straight to the owner’s pocket.

APPLY TODAY2. Your Monthly Payments for Owning Might Be Cheaper Than Renting

In some areas, renting a place may be several hundred dollars more a month than your monthly cost of owning a home. Even when taking into consideration taxes, insurance and maintenance, your monthly cost for owning a home can save you money, especially over the course of a few years. Even renting a much smaller property may be more expensive than purchasing a home.

How long you have to own your house for it to be cheaper than renting depends on how much your home costs, how much you put down and how much you would’ve been paying for rent. Owning a home may take five years to be cheaper than renting, or it might be the cheaper option immediately.

3. Your Home Is an Asset

The real estate market does see fluctuations in home values, but historically, home values have appreciated over time. You can also build equity in your home, which you can’t do while renting. Additionally, you can borrow against your home equity if you’re hit with an unexpected expense or when you want to work toward another financial goal, such as upgrading your home or paying for a child’s college tuition.

4. You Can Make Financial Plans for the Long-Term

If you’re renting and your lease ends in a year, you don’t necessarily know what the future holds for the cost of your living situation after the end of your lease. Your landlord may also have the option of ending your lease early, so you may not know what the cost of living will be for you at that time.

When you own a home, you can make your financial plans for the long-term. If you have a fixed-rate 30-year mortgage, you’ll know what your living costs will be over that length of time. Knowing what your living situation is going to cost you in the long run makes it much easier for you to plan for your financial future.

5. Your Space Is Entirely Your Own

When you purchase a home, you decide whether you want to make changes to the space. You can renovate, repaint or redecorate. You may have some limitations if you have a strict homeowners’ association, especially on the outside of your property, but otherwise, you should have mostly free rein and certainly more freedom than as a renter. A home you own is a place to build a life and make memories for you and your family, so it also brings with it a personal value that can’t be quantified in dollars.

Types of Loans That Make Sense

If you want to buy a home, you may now be wondering how you can choose the right mortgage loan for you. To make your decision, you’ll want to look at all your options. The easiest way to make your decision may be to quickly eliminate the loans you know won’t work for you. Here are a few of the more common loan types that may make sense for you:

1. 30-year Fixed Mortgage

A 30-year fixed mortgage is a loan in which the interest rate and mortgage payments stay consistent for 30 years. After 30 years, you will have repaid your loan. This mortgage type is an excellent option if you prefer the stability of a fixed monthly expense and plan on living in your home for at least 10 years. This is generally considered a mostly risk-free mortgage option.

2. 15-year Fixed Mortgage

A 15-year fixed mortgage is much like a 30-year fixed mortgage except the loan is paid off in half the time. Payments and interest stay the same month to month, and this loan type generally offers the lowest fixed rates. However, it also tends to require high monthly payments since you’re paying off the loan in half the time.

This option is great for someone who wants to build equity quickly and can afford higher monthly payments.

3. Adjustable-Rate Mortgage

Also known as an ARM, an adjustable-rate mortgage is a loan in which the interest rate adjusts during a predetermined time and frequency. Typically, this loan type offers an initial lower rate than that of a 30-year fixed mortgage and interest rates adjust with the market. If interest rates in the market lower, your interest rate will lower. If interest rates increase, so will your mortgage’s interest rate. When your ARM adjusts, you may end up paying more or less than you did at your initial rate.

This option is great for someone who may plan on selling their home well before 30 years. For example, if you’re planning on selling the home in five years, and you secure a loan with an adjustment period of 5 years, you won’t have to worry about a payment increase. By paying an initial low interest rate, you can save the extra cash at your disposal every month or use it to make high-yield investments.

Reasons to Rent

In some cases, you may prefer renting over buying. Here are a few financial and lifestyle reasons for renting:

1. You Won’t Have to Pay for Maintenance Expenses

When the air conditioning fails, the refrigerator breaks or the roof starts leaking, the cost of that repair will fall to your landlord, not you. Since maintenance costs can range from a few hundred to tens of thousands of dollars, this could be a major expense that you won’t have to worry about, though it is possible that your landlord has built the cost of these unexpected repairs into your monthly rent.

2. You Have More Mobility

Once your lease is up, you can pick up and move without worrying about renting out or selling the property. If you want to live in different places or move frequently, renting may be a better option for you than owning a home.

However, most leases do last for several months or up to a year, so you don’t necessarily have the freedom to move whenever you want.

3. You Can Usually Find Cheaper Rent

Though this isn’t always necessarily true, you’ll likely be able to find cheaper monthly rent than the cost of a house. This does tend to vary by location, however.

In some cities where the cost of homes is astronomical, renting may be the best financial option for you. Maybe the location you want to move to simply doesn’t have homes for sale or the homes for sale are well out of your price range but an apartment rental isn’t. If you want to move to a certain area because it’s a good neighborhood or because of its culture, then renting may be your only affordable choice.

You’ll also want to keep in mind what living situation you’re seeking and the properties you’re comparing. Renting a one-bedroom apartment should be cheaper than buying a three-bedroom house, but maybe you’re not willing to live in a one-bedroom apartment. A better comparison would be to compare renting a three-bedroom apartment to buying a three-bedroom house to see which is actually the more affordable option.

4. You Won’t Have to Worry About the Home Depreciating in Value

Because houses are assets, they can appreciate or depreciate in value. If you buy a home and it depreciates, you may lose money if you try to sell it. If you’re renting, you don’t have to worry about the home’s value depreciating.

5. Smaller Spaces Are Cheaper to Decorate and Furnish

Though the American Dream often includes owning a large home, a smaller living space is generally cheaper to decorate, furnish and maintain. If you buy a home with more rooms and more space, you’ll want to fill those walls and empty space with decorations, larger couches, bigger tables and more. On the lifestyle side of things, when you rent a smaller space, you’ll also probably spend less time cleaning and performing minor home repairs than you would for a bigger house.

You also may not have to worry about the general upkeep of the property, such as mowing the lawn or cleaning out the gutters, since that may be something the landlord takes care of or outsources to someone. However, this isn’t always true. Some landlords may require the tenant to mow their own yard, especially if they’re renting an entire house.

Locations That Are Better for Renting Longer

In some cities throughout the nation, the increase in home prices has rapidly outpaced the increase in rent costs. In these areas, renting may make more financial sense or even be the only available option:

- San Francisco, California: The market in this city is staggering. The median home price? $1.4 million. The median monthly rent? $4,500.

- San Jose, California: Other cities in California are not far behind. The median home price in San Jose is $950,000, and the median monthly rent is $3,290.

- San Diego, California: The median price of a home in this city is $645,000 and the median rent is $2,850.

- Seattle, Washington: In this city, the median listing price of a home is $665,000, while the median rent is $2,190.

- Portland: Oregon: In Portland, the median listing price for a home is $450,000, and the median monthly rent cost is $1,950.

- Las Vegas, Nevada: In Las Vegas, the median home price is $288,000, while the median rent is $1,490.

- Sacramento, California: In California’s capital, the median listing price is $329,000 for a home, while the median rent cost is $1,570 per month.

- Los Angeles, California: In LA, the median listing price for homes is $880,000, and the median rent is $3,790.

- Washington, D.C.: The median listing price for a home here is $599,000, while the median monthly rent is $2,680.

For both buyers and renters in these cities, the cost of living can be enormous and the shortage of available homes can make finding a place to live, let alone an affordable one, extremely challenging for some would-be and current residents.

Securing a Home Mortgage With Assurance Financial

You deserve to find your dream home and be able to afford it. At Assurance Financial, we want to help you make that happen by providing you with the mortgage terms that are right for you.

We’re an independent lender, and we can help turn your dreams of homeownership into reality. With end-to-end processing under one roof, you can rest assured that your path to homeownership will be fast and smooth.

Ready to finance your home? Contact one of our loan officers today so we can help you secure the right mortgage for your dream home.

Popular Loan Types

- First Time Home Buyer Loans

- FHA Loans

- Conventional Loans

- Construction Loans

- VA Loans

- Jumbo Loans

- Refinancing