You’ve been with your significant other for a while, and now you’re planning on spending the rest of your lives together. Marriage should be a cause for celebration, not for stress, but thinking about buying a home as you begin your new life together can be intimidating. Should you buy a home before or after marriage? Does marriage status affect mortgage rates? What factors should you consider when making your choice?

Don’t get overwhelmed by the questions you have about buying a home before or after marriage. We’ll help you evaluate the pros and cons of either situation to get a better understanding of buying a house before vs. after marriage.

- Pros and Cons of Joint Tenancy

- Factors to Consider

- Does Marriage Status Affect Mortgage Rates?

- Property Rights

- Tax Considerations

- Why Wait to Buy a House Until After the Wedding?

- Take Your Time With Your Decision

Pros and Cons of Joint Tenancy

Joint tenancy allows two or more people to access an account or have an undivided share in the property. It is a practice couples and business partners alike take part in, and unmarried couples commonly seek joint tenancy. If you’re considering buying a home before marriage, you will want to evaluate the pros and cons of joint tenancy. You can also find joint tenancy with rights of survivorship (JTWROS), which allows living owners to pass on their share to someone else when the owner is still alive.

Here are some of the benefits of joint tenancy to consider.

- Share assets and debt: Share any rent or profit you see as a result of your property between you and your partner. While we hope you only experience the positive gains, it may be comforting to know that you must handle debt together. It could lead to quicker elimination of your debt if you both work together to solve it. Shared debt also protects individuals should the relationship end. One joint tenant cannot leave the other with all of the financial obligations.

- Skip probate: When an individual dies, a probate court reviews the will to determine its validity. In a joint tenancy, if one of the joint tenants dies, there is no need for this process. Assets, like a home, will go to the surviving joint tenant as long as the individuals are married. If they are not married, they may choose a JTWROS to ensure they do not need to go through probate if one of them passes away.

- Implement it easily: You can achieve joint tenancy with a clause in your property’s title. Be sure to work out the legal details even before implementing this choice.

- Financial security: No matter how you go about purchasing a home, it is a smarter financial decision than renting with your partner for an extended period. You can build your assets together and improve your credit. Since the two of you are coming together to purchase a home, you will have two salaries to help cover costs.

With joint tenancy, you must make decisions about your property with each other’s consent. Working together could be either a pro or a con depending on the stability of a relationship. Open communication about the property can help strengthen a relationship, but choices can be difficult if the relationship is on rocky ground.

Of course, with the positives of joint tenancy come the negatives. The cons of joint tenancy include:

- The court may freeze the assets due to excessive debt after one of the joint tenants passes away.

- Unless you are married, you may have to pay gift taxes as a joint tenant.

- The property cannot go to an inheritor since it goes to the other joint tenant when one passes away.

If you want to purchase a home as joint tenants, evaluate your credit scores. If one of you has a better credit score, it may be best for that individual to purchase the home with their stronger credit. Remember if you go that route, your mortgage application will only include one person’s income.

[download_section]

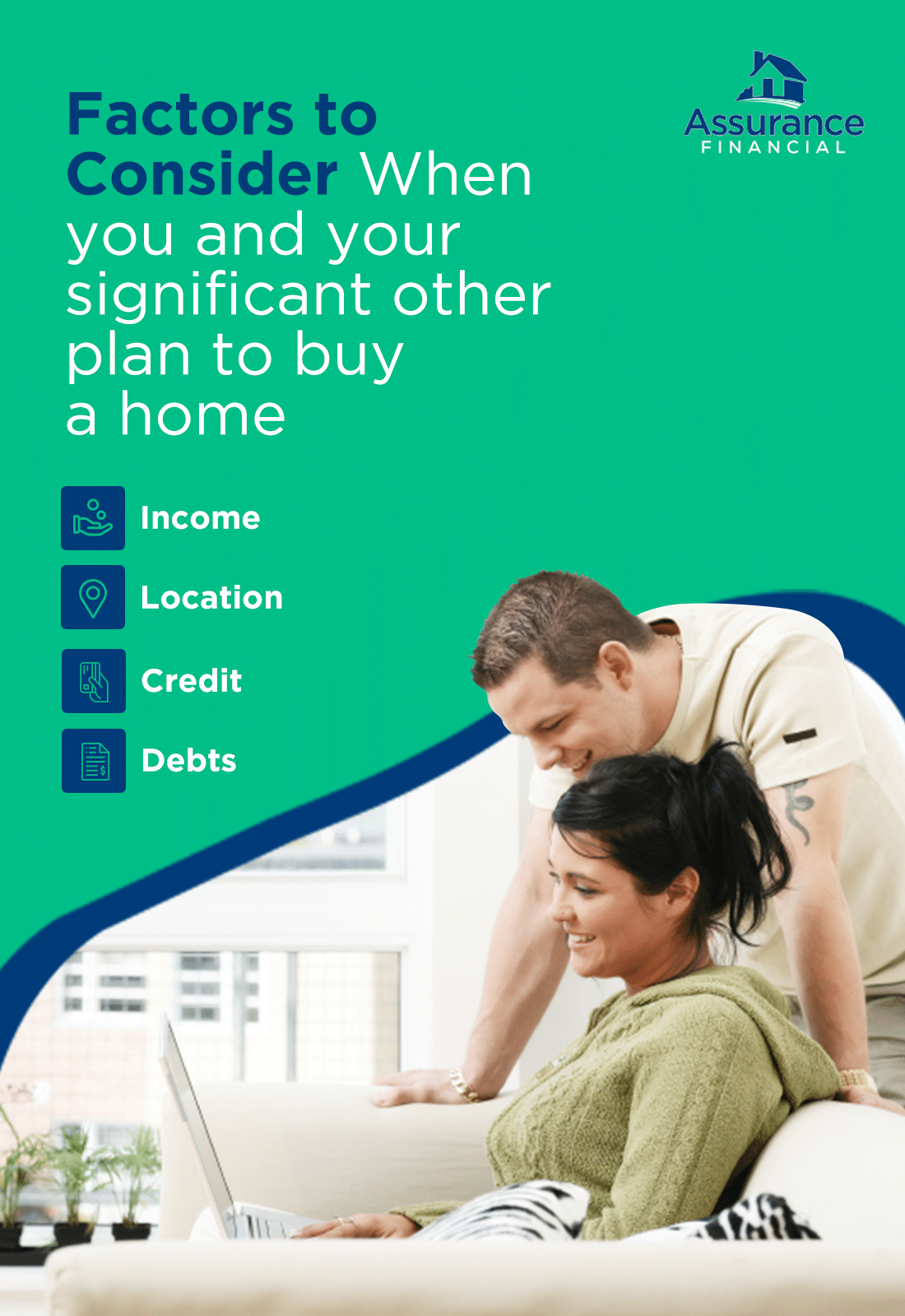

Factors to Consider

When you and your significant other plan to buy a home, evaluate certain aspects of your situation. Determining these factors will help you choose between buying a house before versus after marriage.

- Income: Take both of your salaries into account when deciding when to buy a home. You should have a stable job and some money saved up if you can before venturing into the housing market.

- Location: Whether you buy a home before or after marriage, look into the area you’ll be living in, since laws vary from state to state. Some states allow community property titles, which we will explain later on, but other property and tax laws differ between states.

- Credit: Compare yours and your partner’s credit scores to determine your course of action. If your scores are similar, you can apply together for a mortgage. If one of you has a stronger score, you may decide for that individual to apply.

- Debts: Since lenders evaluate your credit score and any liabilities you have, you and your partner should consider your debts from student loans or other sources. If one of you has less debt and good credit, you could opt for sole ownership of property. You may also choose to wait until you’ve paid off your student loan debt or other liabilities before purchasing a home.

While a tricky part of the home-buying journey is taking some “what ifs” into account, it’s best to have these conversations early. If you are purchasing a home before marriage, work out a legal agreement that outlines what you’ll do if your relationship ends or one of you passes away. Depending on how you will go about purchasing your home, you will also want to think about:

- Who will apply for the mortgage

- How you will split ownership, if applicable

- How you will protect both parties with the property title

- Whether or not you will evenly split additional costs

- What happens if the relationship ends

It may seem overwhelming to have these discussions, but getting organized and figuring out a plan can help you as you move forward with your relationship and the home-buying process.

Does Marriage Status Affect Mortgage Rates?

If you want to buy a house after marriage, you’ll want to know if marriage status affects your mortgage rates. No matter your relationship status, details like your credit score, income, debt and other financial factors influence mortgage rates. While you won’t see a direct impact from your marital status on the rates lenders offer you, related factors of your relationship status can have an effect.

- Single: Before you began your relationship, being a single-income household would have affected your mortgage rates. While lenders don’t penalize you for being single, making less than a married or dating couple may mean you get approved for less.

- In a committed relationship: If you and your partner are serious about your relationship and moving in together, consider what happens when applying for a mortgage before marriage. If you apply together, a lender will take the lower credit score into account. Applying together while not yet married can involve a bit more complex paperwork than if you applied as a married couple or an individual. You or your partner may decide to apply as an individual if your credit scores are drastically different.

- Married: As you would in a committed relationship, you and your spouse likely have a two-income household. Calculate your debt-to-income ratio, as you should no matter your relationship status, to determine how your incomes will combine.

As long as you and your partner have strong credit scores, good incomes and minimal debt, you will likely receive the best mortgage rates as a married couple. For the best outcome, marry before buying a house if your finances are in order. Take into account the factors we mentioned earlier as well as what is best for you as a couple to determine what type of ownership suits your needs.

Property Rights

As you and your partner plan to purchase a home, consider what title works best for you. Potential ownership options work with the different factors above, such as how you will divide the property. Consider these possibilities whether you’re buying a home before or after marriage.

- Sole ownership: One individual owns 100% of the property in sole ownership. When that owner dies, the property goes to someone else through transfer documents, such as a will. The decision may also go through probate. For a married couple or a couple seriously considering marriage, sole ownership may not be the best choice. Unless one of you has a significantly better credit score, you may think about one of the other title options.

- Joint tenancy: Depending on where you live, joint tenancy usually allows the surviving joint owner in the event of another’s passing ownership of the property. Married couples can find tax benefits with qualified joint tenancy, but anyone can enter into this title.

- Tenancy in common: Unlike joint tenancy, which involves an undivided share of the property, tenancy in common allows for different percentages for each owner. The ownership percentage helps determine how much in mortgage interest and property taxes an individual pays. Upon death, an individual’s will can pass the property onto someone other than their spouse, also unlike joint tenancy. With tenancy in common, you can sell your share of assets without the other tenancy in common’s consent. If you seek joint ownership of the property before marriage, it may default to tenancy in common unless you opt for a different ownership method.

- Community property: Available in certain states, community property involves an equal share between spouses. Unlike joint tenancy, individuals can leave their portions of their property to heirs after they pass away. Community property begins at marriage and ends should the couple decide to separate. Any property an individual owned before marriage is called separate property. The individual can maintain control over the separate property or share it with a spouse once married.

With these options, you and your partner can find the title option that suits your needs. Before choosing one, you should also take into account how buying a house before or after marriage can affect your taxes.

Tax Considerations

Evaluate how your marriage affects your taxes to help you decide if you should marry before buying a house. Typically, married individuals have more tax benefits than couples.

As an unmarried couple, you cannot file joint taxes. You will have to organize how you will file separately. Only one homeowner, for example, can claim the deduction on mortgage interest, so two individuals filing separately cannot both claim that deduction. If the relationship ends before marriage, the individuals will have to sort out who covers taxesand other costs.

While tax and property law vary between states, there are more factors to consider as an unmarried couple than a married one. You may find it’s easier to get married before purchasing a home. That way, you can focus on learning about these laws specifically for married couples.

Whichever title you choose for your home, be sure to watch for any liability to pay the taxes due on your property. Even if the responsibility belongs to the other owner, you may be legally responsible if taxes go unpaid. Learn the law where you live and choose your best course of action, which may be purchasing a home after marriage.

Why Wait to Buy a House Until After the Wedding?

While you may have planned on buying a house before marriage, you may want to consider getting married and then buying a home. Marry before buying a house for benefits such as:

- Filing joint taxes

- Ease of applying for a mortgage

- Saving on the stress of house hunting and planning your marriage

- Flexibility with mortgage applications and title options

Though buying a home after marriage makes more financial sense, it is still something you should have a conversation about with your spouse-to-be. You want to be on the same page in terms of buying a home and your goals before you get married to avoid any surprises later.

Take Your Time With Your Decision

Like marriage, buying a house is a big decision. With so many factors to consider, you won’t want to rush into a choice. Evaluate aspects of you and your partner’s life, such as the following.

- Your income and finances: Do you and your spouse have stable jobs? Have you been saving for some time? Take the time to go over your finances and sort out your budget before you begin house hunting. From there, you can make informed decisions about how you will split the property or who will apply for the mortgage if one of you has a better credit score.

- Your long-term goals: Think about your jobs and where you see yourself in the future. Do you plan on moving? Are you going to have children?

- Your relationship: It’s difficult to talk about with your partner, but ensuring your relationship will last a long time creates a secure foundation for buying a home. Work out what your options are should the relationship end. Know that the conversation doesn’t mean it’s going to happen. It means you and your partner have prepared for the future.

- The distant future: Preparing for the future also, unfortunately, means you must think about what happens when one individual in the relationship passes away. Consider the title you obtained when purchasing your home as that influences who the share of the property goes to or if you need to go through probate.

Figuring out the course of your relationship and future will help you and your partner forge a plan. Move forward confidently with your marriage and buying a home after you’ve evaluated your finances and goals.

Purchase a Home With Help From Assurance Financial

Buying a home can be as exciting of a journey as marriage if you know how to approach it correctly. Communicate with your significant other about what both of you want now and what could be best for your shared future. Don’t delay the tough conversations, either. It may be hard to think about what you would do if one of you passes away or if your marriage ends, but preparing for those unfortunate possibilities makes your relationship stronger.

No matter when you decide to purchase a home, contact us at Assurance Financial. Apply online or meet with one of our licensed experts to plan a bright future with your spouse.

Popular Loan Types

- First Time Home Buyer Loans

- FHA Loans

- Conventional Loans

- Construction Loans

- VA Loans

- Jumbo Loans

- Refinancing