Category: Credit

When you’re shopping for a home, you want to do as much as possible to show sellers you’re serious and make yourself stand out in a crowded field. That’s particularly true when you’re looking to buy in a seller’s market. In a seller’s market, there are more people trying to buy homes than properties available.

One way to make yourself stand out is to get a pre-approval from a lender. With a mortgage pre-approval letter in hand, you demonstrate to sellers that you’re ready to buy and likely have the loan to back you up.

Before you get a pre-approval, you might wonder about its impact on your credit score and report. However, for the most part, getting pre-approved will only help you. Read on to have your questions about pre-approval answered.

What Is a Pre-Approval?

A mortgage pre-approval is essentially a stamp of approval from a lender. It’s very similar to the process of applying for a mortgage loan. A lender will review your documents and history during the pre-approval process to determine your interest rate and how much you can comfortably borrow.

Mortgage pre-approval is sometimes confused with pre-qualification, but there are distinct differences. A pre-qualification is generally less serious than a pre-approval. It’s like a rough sketch. When pre-qualifying you, a lender might look at your income and ask about your credit history, but they won’t dig very deep.

A pre-qualification can be valuable when you’re in the early stages of home buying. For example, pre-qualification can give you some general guidance if you’re about to dip your toes in and aren’t sure how much you can afford to buy or if you’d even be eligible for a mortgage. It’s an estimate regarding what you can afford and whether you’re likely to qualify for a loan.

A pre-approval comes after the pre-qualification once you know that you want to buy a home and are ready to jump in with a real estate agent. To get a pre-approval, you need to provide the lender with some documentation and evidence of your financial status.

During the pre-approval process, a lender will look at documents that verify your income, such as income tax returns or paystubs. They might also ask you to provide copies of bank statements to show how much money you have available and what you’ve saved for a down payment.

Crucially, a pre-approval involves a credit check. The lender will review your credit history during the credit check, looking for concerns such as missing or late payments. They might also look for bankruptcies and other signs that you’ve had trouble with loans in the past. They’ll get your credit score, too.

A pre-approval doesn’t always guarantee that you’ll get final approval for a mortgage. There can be circumstances that stand in the way of getting approved, such as an issue with the property’s title or a home appraised at less than the sale price. Changes in your financial situation between the time you get pre-approved and when you’re ready to apply for the actual mortgage can also affect the process.

Why Get a Pre-Approval?

Although a pre-approval isn’t a 100% guarantee that you’ll get a mortgage, it’s an excellent first step. It makes you look more attractive as a buyer to sellers. When someone is selling a property, they want to work with buyers who will provide the smoothest experience possible. Someone who’s got a mortgage lender behind them and who’s taken the time to go through the pre-approval process is more likely to commit to the home buying process.

Getting pre-approved also helps you narrow down your options. For example, a lender might pre-approve you for a $250,000 loan. With that information in hand, you know where you can set your budget.

Going through the pre-approval process also allows you to shop around and see what different lenders can offer you. You’ll be more likely to get a mortgage that works for your budget and financial situation if you have a chance to shop around.

How to Get Pre-Approved

One way to look at the pre-approval process is as a dress rehearsal for an actual mortgage application. You’ll need to give the lender certain documents, and they’ll review your financial information to determine the following:

- How much you can borrow

- What interest rate you’ll pay

- The mortgage term

To start the pre-approval process, your lender will most likely ask you to provide:

- Proof of income: Depending on how you earn income, your proof can be paystubs or tax returns. Self-employed individuals usually provide tax returns, while employed people can provide paystubs.

- Proof of assets: A lender might also request bank statements or other documents that verify how much you have saved or invested. Some lenders will only verify that you have enough for the down payment and closing costs. Others will want to see evidence of cash reserves and savings beyond what you need for closing costs and down payment.

- Employment verification: You will most likely need to verify that you’re still employed or still have a source of income. You can ask your employer for an employment letter, or the lender might call your employer to see if you’re still working there.

- Identification: A lender will need to verify your identity to run the credit check and confirm that you’re who you claim to be. Besides providing your social security number, you’ll also have to provide a photo ID, such as a passport or driver’s license.

- Information about other debts: Your other debt obligations can affect whether you get approved for a mortgage or not or how much you’re approved to borrow. A lender will likely ask you to provide information about any other debts, including the monthly payments and the total amount owed.

Once you’ve given all your details to the lender, they’ll run your credit score and review the information to determine a maximum loan amount and your interest rate. The higher your income and credit score, the more you can borrow and the lower your rate. Whether it’s 15 or 30-years, the length of your mortgage term will also affect your loan amount and interest rate.

If you get the pre-approval, the lender will give you a letter detailing how much you can borrow and the interest rate. When you make an offer on a home, you submit a copy of the pre-approval letter to the seller.

Usually, a pre-approval locks in the interest rate for a limited period, such as 90 days. That means you should find and buy a house within that period to get the rate. Otherwise, you might have to start the pre-approval process over again.

What’s in Your Credit Score?

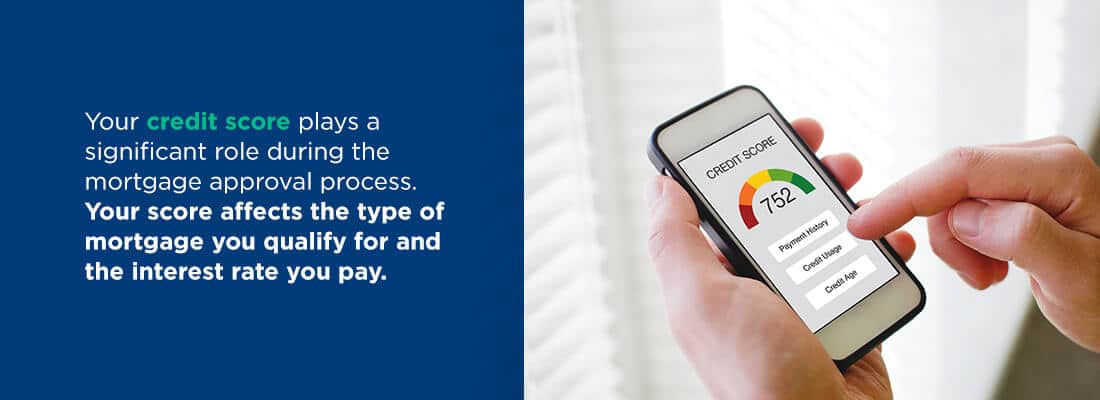

Your credit score plays a significant role during the mortgage approval process. Your score affects the type of mortgage you qualify for and the interest rate you pay. Your score can affect whether you get approved or not. Some mortgage programs, such as FHA loans, are designed to help borrowers who might not have the credit score needed to qualify for a conventional loan.

The companies that calculate credit scores use secret formulas to come up with the three-digit numbers. While the companies keep their exact formulas under wraps, they have detailed the factors that contribute to your overall score:

- Total amount of debt: The total amount is how much you’ve borrowed at the moment.

- Payment history: Your payment history details whether you pay on time or have a history of paying 30 or more days late.

- Age of credit accounts: The age of your credit accounts refers to how long you’ve had a credit history, dating from the time you opened your first currently active credit account.

- Number and type of accounts: The number of accounts refers to how many credit cards or loans you have open. The type refers to whether those accounts are secured loans, credit cards or other types of unsecured loans.

- How much credit you use: How much credit you use refers to the amount you’ve borrowed compared to how much you can borrow. For example, you have a credit utilization ratio of 10% if you have a $1,000 balance on a credit card with a $10,000 limit.

- Recent credit applications: Recent credit applications refers to how many accounts you’ve applied for in the past couple of years. Any recent mortgage pre-approvals or credit card applications will show up here.

Each factor has a different impact on your score. For example, payment history typically has the most considerable effect, while credit applications and types of accounts have less of an impact.

Does Getting Pre-Approved Hurt Your Credit?

In short, yes, getting pre-approved for a mortgage can affect your credit score. But the impact is likely to be less than you expect and shouldn’t stand in the way of you getting final approval for a mortgage.

What Happens to Your Credit Score After a Pre-Approval

When a lender checks your credit for a mortgage pre-approval, they run a hard inquiry. A hard inquiry can cause your score to dip slightly. The impact on your credit will be minimal. The small credit score change after pre-approval won’t cause the lender to change their mind when it comes time to apply for a mortgage.

The drop is temporary. If you continue to pay your bills on time and are punctual with your mortgage payments once you receive one, your credit score will soon recover.

What Are Different Types of Credit Inquiries?

There are two ways of checking credit. A lender might run a soft or hard inquiry, depending on the situation. Each type of credit inquiry has a different impact on your credit score.

Hard Credit Inquiries

When lenders perform the pre-approval process, they run a hard credit inquiry. A hard credit inquiry is like a large flag that tells other lenders you’re in the process of applying for a loan.

A hard credit inquiry affects your credit score, as it signals that you’ve recently applied for credit. If you have several new credit applications on your credit report within a short period, such as within a few months, a lender might see that as a red flag or a sign that you’re having financial difficulties. Usually, the more hard inquiries you have in a limited period, the more significant the impact on your score.

For that reason, it’s usually recommended that you do not apply for a car loan, credit card or other types of loan while you’re applying for a mortgage.

It’s important to understand that although a hard inquiry often causes a score to drop, hard inquiries in and of themselves aren’t necessarily bad things. You need a hard inquiry to get any type of loan.

Soft Credit Inquiries

A soft credit inquiry doesn’t have an impact on your credit score. A soft inquiry occurs whenever you check your credit report. A lender won’t be able to see that you’ve run a credit check on yourself.

If a lender wants to pre-approve you for a credit card, they’ll also run a soft inquiry on your credit. The lender uses the information they get to put together a credit card pre-approval offer to send you. Other examples of a soft inquiry include when a utility company checks your credit before opening a new account or when an employer runs a credit screening before hiring you.

Does Getting Multiple Pre-Approvals Hurt Your Credit Score?

Shopping around for a mortgage is often recommended to people looking to buy a home. But, if getting pre-approved for a mortgage requires a hard inquiry on your credit report, won’t getting several pre-approvals create several hard inquiries, increasing the damage to your credit score?

Fortunately, the impact several pre-approvals have on your credit score is minimal. When you get pre-approvals for multiple lenders, the credit bureaus typically lump them together as a single hard inquiry. Bureaus understand it’s common to shop for a mortgage. Borrowers who get pre-approvals from multiple lenders aren’t penalized for trying to get the best offer possible.

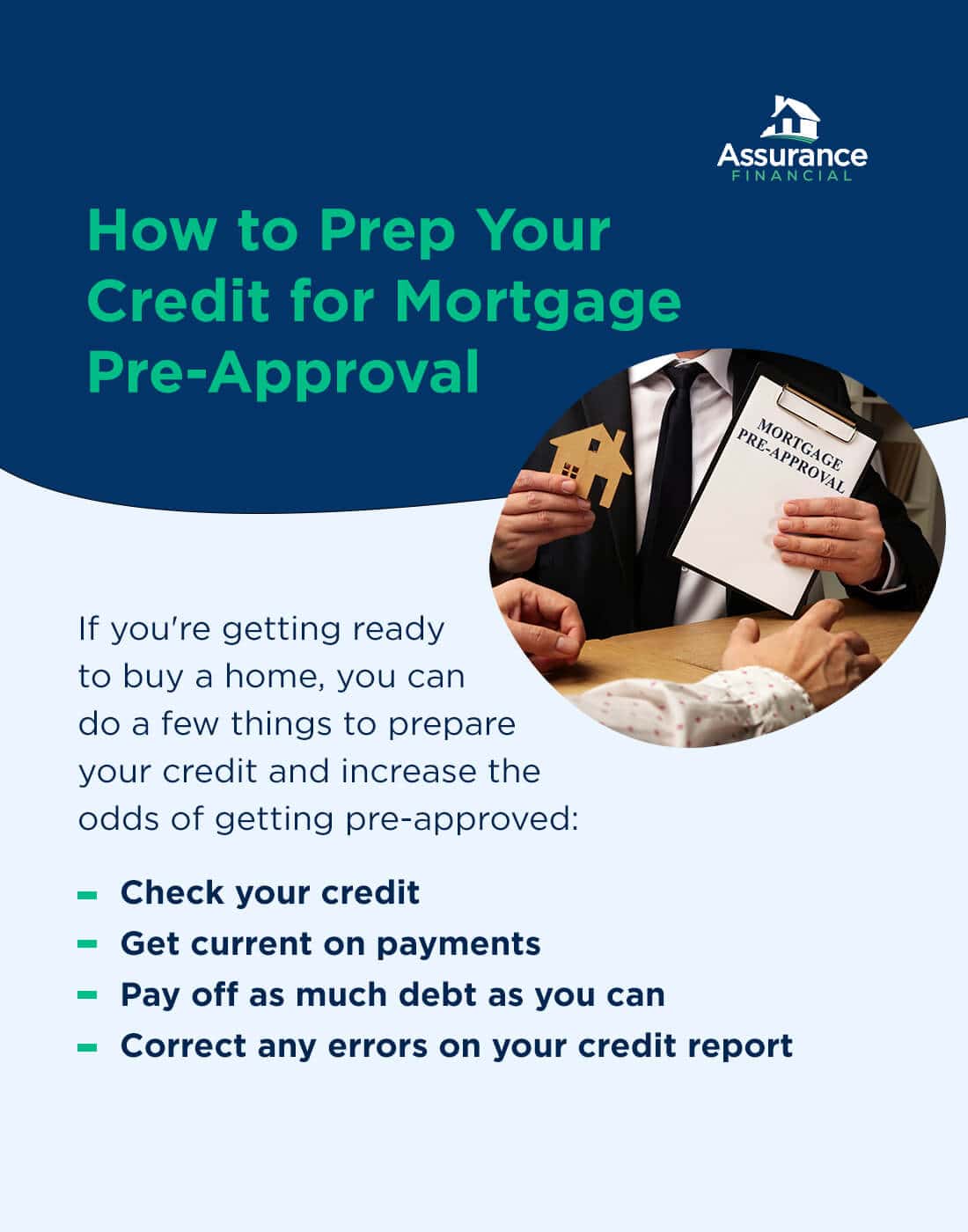

How to Prep Your Credit for Mortgage Pre-Approval

If you’re getting ready to buy a home, you can do a few things to prepare your credit and increase the odds of getting pre-approved:

- Check your credit: Checking your credit creates a soft inquiry, which doesn’t affect your score. It’s a good idea to check your credit for at least several months or even up to a full year before you start looking for homes. Checking in advance gives you plenty of time to take action to improve your history and score if needed.

- Get current on payments: If you have a history of paying late on any of your loans, make an effort to get current on your payments. Pay off any late fees and back-due amounts. Then, commit to paying your loans by the due date every month. You can set up a payment reminder or schedule automatic payments to ensure you don’t forget.

- Pay off as much debt as you can: How much debt you have or the amount of debt compared to your income can affect your credit score and eligibility for a mortgage. If you have a lot of debt, try to pay some off before applying for a home loan.

- Correct any errors on your credit report: The credit bureaus can make mistakes. Let the agency know if you notice anything strange or incorrect on your credit report. Common errors include accounts that belong to someone else — usually someone with a similar name — or accounts you’ve closed still showing as open. </span >In some cases, errors in your credit report can be a sign of identity theft or fraud.

[download_section]

Do’s and Don’ts After Getting a Mortgage Pre-Approval

Once you have the pre-approval, you’re ready to roll and can put in an offer on a home. Remember that getting pre-approved doesn’t mean you’ll necessarily get fully approved for a mortgage. Certain actions between the pre-approval and final approval can affect your credit and interfere with the mortgage process. Here’s what to do and not do when you’re in the home stretch of getting a mortgage.

Do: Continue to Pay Off Other Debts

If you have other debts, keep making payments on them while looking for a home and going through the mortgage process. Any change in your payment history can impact your credit score, causing a lender to reconsider approving you for a mortgage.

Don’t: Apply for New Credit

While credit bureaus group several mortgage pre-approvals together and count them as a single hard inquiry, the bureaus won’t group other loan applications with your mortgage pre-approval. Several other hard inquiries can affect your credit score, such as a credit card application or personal loan application.

Applying for new credit while shopping for a home can also raise alarm bells for your mortgage lender. They might wonder why you’re applying for multiple loans while you’re trying to buy a home. To keep your lender calm and increase your odds of approval for a home loan, wait until after closing to apply for other types of credit.

Do: Shop for a Home

Pre-approvals don’t last forever, so it’s a good idea to get out there and start looking for your dream home once you have the pre-approval letter in hand. Usually, your pre-approval will be valid for several months, so don’t panic if you don’t find your home immediately.

Contact your lender if you don’t find the right home before the pre-approval expires. Some are willing to extend the offer beyond the initial period without making you go through the entire credit check and application process again.

Don’t: Make Other Big Purchases

If possible, try not to make big purchases between getting pre-approved, putting an offer in on a home and closing. Buying a new car or new furniture can affect your cash reserves, which might make a lender reconsider approving you for a mortgage. Using a credit card to buy furniture will increase the amount of debt used, affecting your credit score.

It’s better to wait until you’ve closed on your home to purchase furnishing for it or before making any other large purchases.

Do: Keep Your Lender Up-to-Date on Any Life Changes

Depending on how long it takes to find a home and put in an offer, you might experience some life changes between getting pre-approved and closing on your home. Let your lender know whether it’s a change in income, a new family member or getting an inheritance. Changes in your financial status can affect your mortgage eligibility.

Don’t: Quit or Change Jobs

A history of steady employment is very attractive to mortgage lenders, as it suggests that you’ll continue to have the means to pay your mortgage for years to come. While your job status might be out of your control in some cases, if possible, wait until you’ve closed on the home before quitting your current gig or finding a new job.

Becoming unemployed before you have final mortgage approval affects the process. The same is true if you change jobs and accept a lower-paying position.

Get Pre-Approved With Assurance Financial Today

The first step to getting a mortgage is getting pre-approved. Apply today or contact a loan officer.

Linked Sources:

- https://assurancemortgage.com/buyers-vs-sellers-market/

- https://assurancemortgage.com/15-vs-30-year-mortgages/

- https://assurancemortgage.com/important-credit-score-for-home-loan/

- https://assurancemortgage.com/fha-loans/

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/how-to-get-a-mortgage-loan/

- https://assurancemortgage.com/apply/

To get certain types of loans, such as a mortgage, you need to have a good or excellent credit score and a strong credit report to qualify for the best terms possible. But it can be difficult to build a good credit history or establish your credit score without having any loans.

If you’re wondering how you can build your credit score, the good news is that there are several options available to help you establish credit and get on the path toward homeownership. Learn more about what mortgage lenders are looking for in a credit report and what you can do to make your credit score and history look attractive.

Table of Contents

- Credit 101

- How to Build Credit to Get a House

- How to Practice Good Credit Habits

- Benefits of Building Credit

- Boost Your Credit With Assurance Financial

Credit 101

Credit lets you borrow money to purchase items you can’t afford to pay for in full upfront. For example, it allows people to pay for cars, education and houses. When a lender extends credit to you, they expect you to pay back what you borrow, plus interest, usually on a set schedule. Lenders who issue credit can’t simply trust their gut when deciding whether or not to lend money to a person. They usually check that person’s credit report to see whether they have a history of paying on time or missed payments.

The longer a person’s credit history, the more information a lender has to go on. For example, if someone opened their first credit card 20 years ago, the lender can see whether they have made consistent and timely payments over the years. The more varied someone’s credit history is, the more the lender has to judge whether or not an individual would be able to handle repaying another loan. The amount a person has borrowed also plays a part in influencing a lender’s decision about whether or not to give that person another loan.

While it can be relatively easy to get approval for some types of loans, others have more stringent lending requirements and might require a person to have a stronger credit history. If buying a house is in your future plans, it can be worthwhile to focus on building credit — making you a more attractive borrower to lenders and helping you get the best terms and conditions possible on your home loan.

How to Build Credit to Get a House

If you’re starting from scratch and don’t have a credit history at all, you have several options for building up your credit and making yourself a more attractive borrower to lenders.

1. Consider a Secured Loan

Several types of loans are available for people who want to improve or establish their credit. Both types require you to make a deposit that acts as collateral, but how the loans go about doing that is slightly different.

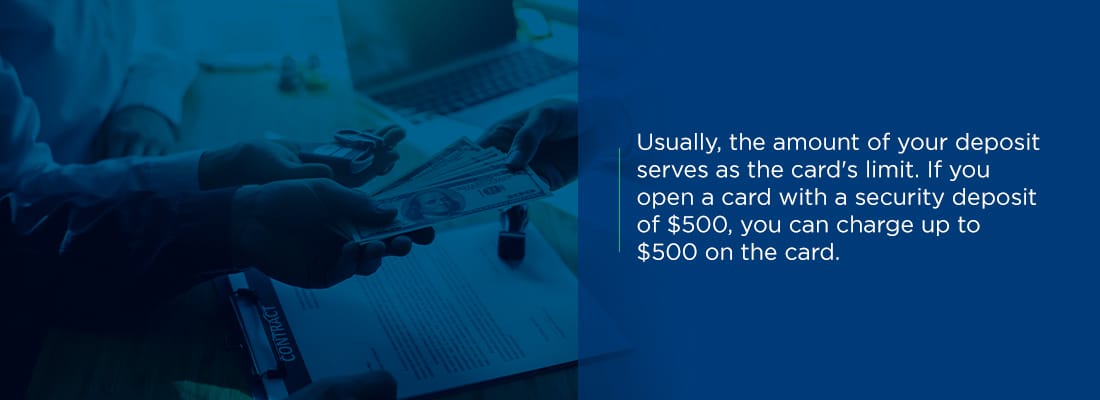

For example, you first need to put down a deposit if you open a secured credit card. The deposit acts as the collateral on the card, reducing the risk to the lender if you can’t make payments on the card. Usually, the amount of your deposit serves as the card’s limit. If you open a card with a security deposit of $500, you can charge up to $500 on the card. Once you pay off the full balance, you can charge up to $500 once again.

One thing to understand about a secured credit card is that your deposit won’t count toward your payments on the card. If you use the card to purchase things, you need to pay it by the due date to avoid late fees and other penalties.

[download_section]

Secured credit cards tend to have higher interest rates than other types of credit cards, making it worth your while to pay your balance in full before the due date rather than pay only the minimums. In addition, many cards will convert to an unsecured version after a year or so, meaning you get the amount of your deposit back. Depending on the terms of the credit card, you might need to ask the card company to convert the card to an unsecured one, or the conversion might be automatic.

Another option for people with limited credit histories is a credit-builder loan. Credit-builder loans work differently from other loan types. When a person applies for a credit-builder loan, a lender deposits the amount of the loan, such as $1,000, into an account. The borrower then makes payments to the lender, such as $75 per month, plus interest. When the borrower makes payments, the lender transfers that amount of the loan into the borrower’s account. The lender also reports the borrower’s payments to the three credit reporting bureaus, helping people build their credit to purchase a home.

A study from the Consumer Financial Protection Bureau found that nearly one-quarter of people who didn’t previously have credit were able to establish a credit history after they got a credit-builder loan. The average credit score increased by 60 points after individuals opened a credit-builder loan.

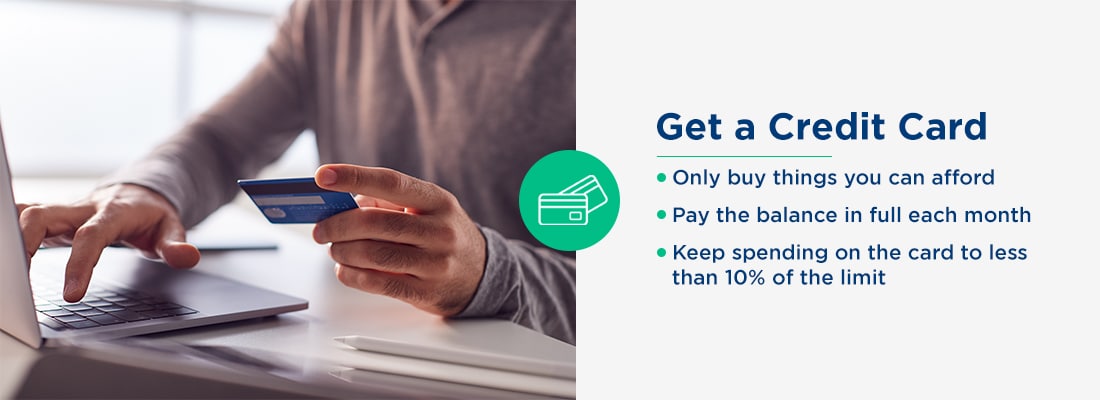

2. Get a Credit Card

You might not have to apply for a secured credit card to start building credit. Several “starter” cards are available that let you build your credit history without putting down a deposit. Often, starter cards are targeted at students, meaning you might have to be in college to qualify for the card. There are some cards that are designed for adults who aren’t in school, though.

When you get your first credit card, keep in mind that it might have a high interest rate and a low credit limit. A credit card company might be willing to issue you a card, but it is also likely to take steps to minimize its risks. A higher-than-average interest rate is one way to do so, as is limiting the amount you can borrow. There are a few things you can do to make the most of your new credit card:

- Only buy things you can afford: Use your card for purchases you would make anyway, such as groceries. That way, you won’t run the risk of charging more than you can afford to pay back on the card.

- Pay the balance in full each month: Pay the full amount of the balance by the due date to avoid having to pay interest on the things you’ve charged. Paying in full by the due date also helps you avoid late fees and keeps your payment history positive.

- Keep spending on the card to less than 10% of the limit:How much you’ve borrowed compared to your credit limit affects your credit score and history. To boost your score, keep your spending on the card below 10% of the limit. That means if you have a $1,000 limit, don’t charge more than $100 at a time.

3. Get Installment Loans

Your credit mix plays a part in determining your credit score. The more varied the history on your credit report, the more reliable you might appear as a borrower. Along with considering revolving credit in the form of credit cards, it’s a good idea to add an installment loan or two to your credit mix. While revolving loans let you pay off your balance and borrow more, installment loans are issued in a lump sum. You then pay them back with interest in monthly installments. How long it takes to repay the loan depends on its term.

A mortgage is an example of an installment loan, as are student loans and car loans. If you’re looking to build credit, getting a student loan or car loan is likely going to be easier than getting a mortgage. Some types of student loans, notably federal student loans, don’t require a credit check first, making them easy to get, even if you have no credit at all. Some car loans are also available to people with minimal credit histories.

As with any type of loan, it’s important you make sure you can repay your installment loan based on its terms. You can take out several student loans without a credit check and borrow thousands of dollars to pay for school, but for the sake of your future credit, it’s important you can afford the monthly payments on those loans after you graduate.

If you’re considering a car loan, also be sure you can afford the monthly payment. You might consider making a larger down payment or buying a cheaper car to be absolutely certain you’ll be able to repay the loan without paying late or missing payments.

4. Ask Someone to Be a Co-Signer for You

If you’re having difficulty getting approved for a loan or credit card, one option is to find someone who can be a co-signer. A co-signer is usually someone with an established history of good credit, such as a parent, spouse or older sibling. When they co-sign a loan with you, they agree to take on responsibility for it. The loan will appear on their credit report, and they will be expected to pay it if you stop making payments or otherwise fall behind.

Being a co-signer is a major act of trust on the part of the person who co-signs. If you fall behind on payments, their credit is on the line, too. Before you ask someone to co-sign for you, be clear about your plans for the loan. Your co-signer might want to set up rules about the repayment process or otherwise verify you can make the payments. Good communication is key to protecting each person’s credit and preserving your relationship.

A slightly less risky option for a person with established credit is to add you as an authorized user on an existing account, such as a credit card. Some credit cards let account holders add others as authorized users, meaning a person gets a credit card in their name and is put on the account. The authorized user doesn’t own the account and isn’t fully responsible for making payments.

In many cases, the credit card appears on the authorized user’s credit report, helping them establish credit. You don’t have to use the card you’re an authorized user on. Simply having it appear on your report can be enough to improve or establish credit. The trick is to make sure the person who owns the card pays it as agreed and doesn’t pay late.

5. Make Sure Your Loans Get Reported

Three credit reporting bureaus exist that compile all the details about your loans and credit card accounts. Mortgage lenders use the information on the credit bureau’s reports to calculate your credit score. For an account to “count” toward your score, it needs to show up on your credit report.

For the most part, credit card companies and lenders will report your information to the appropriate credit bureaus. But it’s still a good idea to double-check and make sure your account details are going to show up on your credit history. If you’re completely new to building credit, another option is to have your rental payments and utility bills show on your reports. Some lenders will use that information when making a decision about you, and others won’t. If you have a good history of paying your rent and utility bills on time, it can be a useful thing to have show up on your credit report.

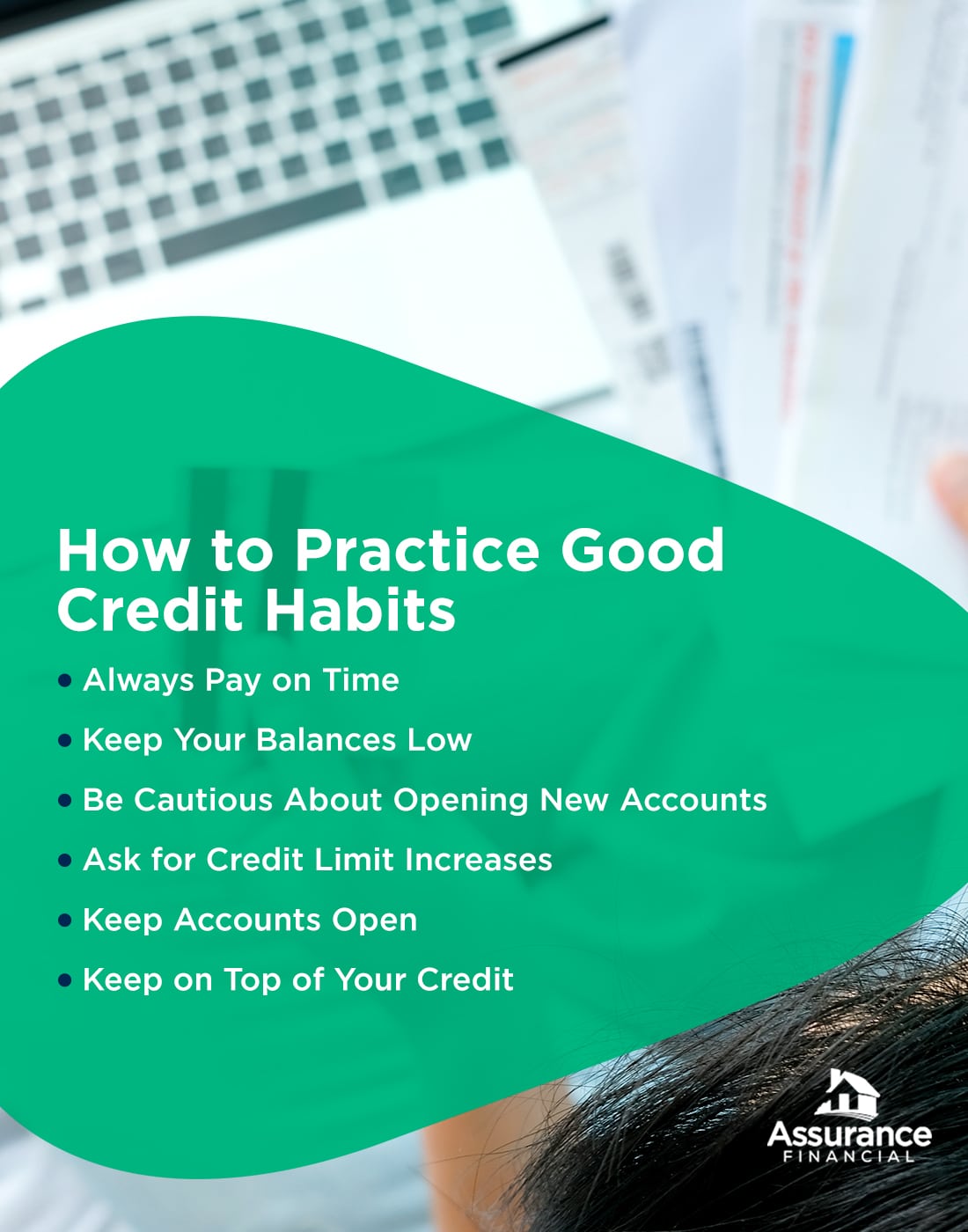

How to Practice Good Credit Habits

After you’ve established a credit history, there are some best practices to follow to help keep your score high and make you an attractive borrower to lenders. Here’s what you can do to build and boost your credit:

1. Always Pay on Time

Your payment history makes up 35% of your credit score, making it the most important factor when it comes to determining your credit. Make sure you always pay your bills on or before the due date and always pay at least the minimum owed. You can pay more than the minimum if you prefer. In fact, paying as much as you can is also good for your credit, as it helps to reduce the total amount you owe.

If you’re worried about missing payments or paying late, you have a few options. You can set up calendar reminders so you get a notification just before the due date. Another option is to automate your payments using a bill-paying service. Some credit cards let you set up automatic payments, so your cards get paid off each month without you having to check a calendar.

2. Keep Your Balances Low

The amount you owe also plays a big part in determining your credit score. The less you owe, particularly in comparison to the amount you can borrow, the better your score. Even if you have a high limit on your credit card, keep your balance well below it. It’s easier to repay your debts when you don’t borrow too much. You also look more reliable to lenders when your balances stay low.

3. Be Cautious About Opening New Accounts

Although you need to have credit accounts to establish a credit history and start building your score, it’s possible to have too much of a good thing. New credit affects your score, and every time you open a new account, your score drops a bit. If you go out to the mall and open several new store credit cards in a day, that can have a notable impact on your credit. Opening several new credit cards at once can be a red flag for a lender. They might look at your new accounts and wonder if you’re experiencing financial difficulties, which would make it challenging for you to repay a new loan.

If you’re in the process of applying for a mortgage, it’s critical you avoid opening new accounts, at least until you have final approval on the mortgage and have closed on your home. Opening a new credit card or taking out a car loan while your mortgage is in the underwriting process can sound like a warning bell to the lender, causing them to press pause on the proceedings.

4. Ask for Credit Limit Increases

Your credit utilization ratio affects your credit score. The ratio compares how much credit you have available vs. how much you have used. For example, if you have a credit card with a $1,000 limit and a balance of $100, your credit utilization ratio is 10%. The lower the ratio, the better for your credit. Keeping your balances low is one way to keep your ratio low. Another way is to increase your credit limit. For instance, you can ask the credit card company to raise your $1,000 limit to $2,000.

Credit card companies might be willing to increase your limit in several cases. If you have a history of paying on time, the company might see you as a lower-risk borrower and agree to increase your limit. An improvement in your credit score or an increase in your household income can also convince a credit card company that you’re a good candidate for a limit increase.

5. Keep Accounts Open

The longer your credit history is, the better it looks to lenders. A person with a 20-year history has more to show than someone with a five-year history. When possible, keep your credit accounts open to maximize the length of your history. For example, if you have a credit card that you no longer use, it’s still a good idea to keep the account open.

Another reason to keep credit card accounts open is that doing so helps your credit utilization ratio. If you have three credit cards that each have a $5,000 limit, your available credit is $15,000. Close one of those cards, and your available credit drops to $10,000.

6. Keep on Top of Your Credit

Everyone makes mistakes, including the credit reporting agencies. Whether you plan on applying for a mortgage soon or in the distant future, it’s a good idea to keep a close eye on your credit reports, so you can detect and fix any issues that come up. Possible mistakes include incorrectly reported payments, accounts that don’t belong to you and outdated information. If you see a mistake on your report, you can let the credit bureau know, and it will take action to correct it.

The Benefits of Building Credit

Having a solid credit history can help you in many areas. With a strong credit score, you can get the best rates on a mortgage or construction loan. Your credit also plays a role in helping you qualify for other loans and can let you get a better rate on insurance. Some employers also check credit when making hiring decisions.

That can mean the sooner you start building credit, the better. Even if buying a house seems like it’s years in the future, laying the groundwork today could mean a lower interest rate and better terms later on.

Boost Your Credit With a Mortgage From Assurance Financial

When you buy a home, getting a mortgage could help your credit. Once you’re approved for the home loan and make regular payments on it, you’re likely to see your score improve. Assurance Financial has simplified the mortgage application process, making it easier for you to become a homeowner and start living your dreams. Start your application with us online today.

Linked Sources:

- https://files.consumerfinance.gov/f/documents/cfpb_targeting-credit-builder-loans_report_2020-07.pdf

- https://www.myfico.com/credit-education/whats-in-your-credit-score

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/how-to-get-a-mortgage-loan/

- https://assurancemortgage.com/important-credit-score-home-loan/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/credit-score-determined

Building credit takes careful planning and due diligence to avoid unnecessary mistakes, like missed payments. Though it requires careful attention, it is not impossible. If your credit isn’t where you want it to be, you should evaluate your current status and develop a game plan if you plan on purchasing a home in the future (and even if you’re not, it’s good to know how to build your credit so that it works for you!)

Credit Cards

One of the easiest ways to build credit is to use your credit card regularly and responsibly. Making your monthly payments on time and in full is positively reflected in your credit score. Every payment you make is reported to credit bureaus, regardless of whether you’ve made it on time or not. Paying each bill helps you build a positive credit profile, demonstrates that you’re capable of meeting a creditor’s conditions, and usually comes with some great perks! Though credit cards offer regular users rewards, like cash back, travel credits, and reward cards based on the user’s spending habits. They also give you the option to make large purchases upfront, which commonly leads many users to rack up debt fast. Credit card holders should be mindful of deadlines and late payment fees to avoid high spending.

Car Loans & Buying Pre-Owned

Introducing a car loan to your credit line helps diversify your credit profile and gives you the opportunity to boost your credit score.

Making each payment on time helps you build credit, however being late on just one payment can potentially negatively impact your credit score. Steady, reliable payments paint you as more trustworthy to lenders. Before you drive off the lot in a brand-new car, consider purchasing a pre-owned vehicle instead. Research shows cars depreciate by about 60% in just five years. In most cases, dealers offer extended warranties and special financing with the purchase of a pre-owned car.

Student Loans

Student loans are installment loans, which are a bit different than revolving credit, like credit cards.

Lenders offer these types of loans to users upfront, all at once, then require them to pay the amount back over a set period through regular installments. Car, mortgage, and home equity loans all fall into this category, but student loans are typically the first installment loans most people encounter.

Starting off your credit history with on-time student loan payments reflects positively on your credit score. Student loan borrowers can use their loans as a base to build up a good credit profile. If you do have student loans, be sure to always pay on time, and stick to a payment fee you can afford.

Mortgage Loans

Buying a home is likely the biggest and most important purchase most people make in their lives.

A mortgage loan helps people build credit, as long as they make their payments routinely and on-time. Despite being the biggest debt, most people owe; mortgage loans are considered good debt. Your home is a physical asset backing the loan. If you miss a payment, the lender can repossess the home, meaning a mortgage is a relatively safe investment for them. Paying your mortgage will boost your score and show creditors you’re a trustworthy borrower. Applying for a mortgage will initially lower your credit score. The application will trigger a hard credit inquiry, which only temporarily lowers your credit score for about 45-days.

Slowly and steadily, you can build up your credit. It takes time, but it is not completely impossible. If you’re looking to purchase a home in the future, create a game plan and stick to it. Showing consistency and responsibility is a factor when Loan Officers consider when determining a home mortgage loan. If you need more information, contact one of Assurance Financials’ home loan experts today!

[download_section]

You may be wondering what creditors take into account when determining your credit score. There are five factors involved in calculating your credit score, each varying in importance and value to credit scoring models. Here are the five more common criteria of what determines your credit score:

1. Payment History (35%)

The most important factor in determining your credit score is whether you pay your bills on time. Credit scoring models examine all the credit you’ve already been extended, including credit cards, auto loans, installment loans and any other line of credit. Any late or missed payments are noted and may negatively impact your credit score.

2. Debt/Amounts Owed (30%)

The second most important determining factor is the balance-to-limit ratio on your credit cards. Models will examine how much of the total credit line you’re using on all of your credit cards. In general, you should try to keep your utilization rate below 30% to avoid lowering your credit score. Keeping your balance below 108 will help you achieve a higher score.

3. Age of Credit History (15%)

The credit score calculation also reviews the age of every account you hold. Scoring models favor users who show they’ve been able to handle several credit accounts over time without penalties, late fees or closures.

4. New Credit/Inquiries (10%)

Your credit score will also reflect how much credit you’ve received or applied for recently. Any credit you’ve applied for within the past three to six months or new inquiries from creditors are recorded and used during calculations. The scoring model doesn’t consider requests a creditor has made to review your credit file or score to build a preapproved credit offer. Nor does it account for any personal requests you’ve made for a copy of your credit history.

5. A mix of Accounts/Types of Credit (10%)

Creditors like to see you’ve been able to balance multiple tradelines of different types. The scoring algorithm examines the types of credit accounts you have, including revolving debt and installment loans.

The above are the most common factors determining your Credit Score. Be aware that your Credit Score is one of a number factors we consider when determining your home mortgage loan. The best way to know if you qualify, and for how much, would be to discuss your situation with one of our home loan experts. Contact an Assurance Financial Loan Officer now!

[download_section]

Few things are more important than your credit history when it comes time to purchase your new home. Your credit score isn’t just a number; it paints a full financial picture. We’ve mapped out a guide to understanding your credit during the mortgage process and how to start planning for successful homeownership today.

Credit scores fall within a range from 300 to 900. Your credit score directly influences which programs you qualify for and subsequent loan rates. Individuals with higher scores face fewer limits during the mortgage process and sometimes the cost of private mortgage insurance.

Scores of 780 or higher are desirable to most creditors and receive the best possible rates. Borrowers with scores between 720 and 780 also receive lower interest rates and are considered excellent candidates in the eyes of lenders. Scores within the 660 and 719 range are respectable as well and qualify for most loans; however, these individuals face higher rates.

Any score below 660 will limit you to a select few programs and while offering higher consumer rates. People with a credit score of 580 or below risk the chance of not being approved for a loan. If they are approved, they’ll most likely encounter extreme rates.

Though your credit score is not the only determining factor, a Loan Office at Assurance Financial is ready to help work with you to determine which loans are available. Whether you are a First Time Home Buyer, a Veteran or looking for a USDA Rural Loan, we’re here to help. Find a loan officer near you and see how our home loan experts can help you today!

[download_section]