Month: May 2022

Several government loan programs exist to help buyers take one step closer to the American dream of homeownership. If you’re considering buying a home and don’t think you’ll qualify for a conventional mortgage, a Federal Housing Administration (FHA) loan or a United States Department of Agriculture (USDA) loan might be right for you.

While the FHA loan program and the USDA loan program have some similarities, they ultimately have slightly different goals and different requirements. Generally speaking, USDA loans have more restrictions than FHA loans. Your income and where you want to live can influence whether an FHA or USDA loan is the right choice for you.

What Is an FHA Loan?

An FHA loan is a type of mortgage for new buyers in the United States. The FHA is part of the U.S. Department of Housing and Urban Development (HUD). It guarantees or insures the FHA loan program.

FHA loans don’t come directly from the government. Instead, they are from private lenders. The lenders have the FHA’s guarantee that it will step in and cover the cost of the loan if the borrower is unable to pay or stops making payments.

Since private lenders have insurance from the FHA, they are more likely to lend money to people who wouldn’t qualify for a conventional mortgage. FHA loans are therefore available to buyers with low credit scores and those who can’t make a down payment of 10% or more.

FHA Loan Term and Interest

FHA lenders generally offer a 15- or 30-year term. Borrowers can repay the loan early by making larger or more frequent installments than the minimum requirement.

An FHA may have a fixed interest rate, meaning it will stay the same throughout the term. Conversely, an FHA may also have a variable interest rate.

FHA Down Payments and Insurance

You must put at least 3.5% of the purchase price down when you finance your home purchase via an FHA loan if your credit score is 580 or higher. The minimum down payment is 10% for buyers with a 500-579 credit score.

In exchange for financial flexibility, the FHA requires borrowers to take out a two-part mortgage insurance policy. Part one is an upfront expense equal to 1.75% of the loan. Part two is an annual fee that varies based on the size of your down payment, the loan term and the amount of the loan. You can pay the second part once per year or divide the annual balance over 12 months. A smaller down payment results in a larger mortgage insurance premium.

The size of your down payment also affects how long you need to maintain the mortgage policy. The mortgage insurance policy remains in place throughout the loan’s term when you put less than 10% down. If you put down 10% or more, you can eliminate the premium after 11 years of consistent payment.

What Is a USDA Loan?

USDA loans, also known as Rural Development loans, make homeownership affordable and provide affordable housing in rural and some suburban areas. You can’t apply for a USDA loan if you want to purchase property in the middle of a big city or metropolitan area.

USDA Down Payments and Other Features

You don’t have to make a down payment if you qualify for a USDA loan. You will have to pay a funding fee, which acts as insurance. The amount of the fee can vary but can’t be more than 3.5% upfront and 0.5% of the average annual unpaid balance monthly.

USDA loan borrowers need to meet income requirements, which vary based on the part of the country where they want to purchase a home.

USDA loans have 30-year terms and fixed interest rates, which are set by the lender.

Types of USDA Loans

The USDA supports two types of loans.

Single Family Direct Loans are issued by the USDA. They are designed for borrowers with a low or very low income who want to purchase a home in a rural area. The loans have up to 33-year terms — and up to 38 years for very-low-income individuals — no down payment required and financial assistance for borrowers. As of 2022, Single Family Direct Loans have a fixed interest rate of 2.5%.

The other USDA loan program, the Single Family Housing Guaranteed Loan program, has some features in common with FHA loans. It’s guaranteed by the USDA and issued by approved, private lenders. Lenders who participate in the USDA loan program can have up to 90% of the loan amount insured by the USDA.

USDA vs. FHA — What Do FHA and USDA Loans Have in Common?

While USDA and FHA loans have their differences, there is some overlap between the two loan programs. Some of the features the loans have in common include:

1. Government Guarantee

Both FHA and USDA loans are guaranteed by the government. However, the agencies that guarantee the loans differ. The FHA provides insurance for lenders who participate in the FHA loan program, while the USDA backs USDA loans.

The government guarantee matters because it gives lenders peace of mind. When a lender issues a loan, it wants some reassurance that a borrower will repay it. To get that reassurance, lenders look at borrowers’ credit scores, income and assets. Generally, the higher a person’s credit score and income and the more assets they have, the less risky they look to a lender.

A borrower who doesn’t have a high credit score, substantial income or lots of assets might still be able to pay their mortgage as agreed, but a lender might hesitate to approve them. In the case of either a USDA loan or FHA loan, a government agency is stepping in to provide an extra layer of security to the lender, minimizing its risk.

The government guarantee doesn’t come free to borrowers. In the case of both an FHA and a USDA loan, the borrower has to pay mortgage insurance premiums to cover the cost of the agencies’ guarantees.

2. Availability to Buyers Who Might Have Difficulty Qualifying for Other Mortgages

Another feature FHA and USDA loans have in common is that both are available to homebuyers who might not qualify for other types of mortgages. The FHA loan program is meant for buyers who might have excellent, very good or fair credit scores and who aren’t able to make a large down payment. These buyers might have tried to apply for conventional mortgages but were turned down.

The USDA loan program is for buyers in rural or suburban areas who might not have enough income to qualify for another type of mortgage and who don’t have the down payment available for an FHA loan.

3. Fixed Interest Rates

Both USDA and FHA loan programs offer borrowers fixed interest rates. A fixed interest rate stays the same throughout the loan term. If you take out an FHA mortgage with a 3.85% rate, you’ll pay 3.85% on day one and on the last day.

There are several advantages to getting a mortgage with a fixed rate. You always know what your monthly payments will be when the rate is constant. Getting a mortgage with a fixed rate also lets you lock in a rate when they are low, without worrying that it will increase in the future.

In contrast, adjustable-rate mortgages (ARMs) have interest rates that change on a set schedule, such as every three years. The rate on an ARM can jump one day, increasing the size of your monthly mortgage payment.

USDA vs. FHA — What’s the Difference Between FHA and USDA Loans?

While there are some similarities when you compare USDA loans versus FHA ones, the mortgages come from two distinct programs. There are some other notable differences between FHA and Rural Development loans.

1. Down Payment Requirements

One of the biggest differences between a USDA loan and an FHA loan is the down payment requirement. In short, you can get a USDA loan without making a down payment. The loan program is designed to make homeownership an option for buyers who would otherwise be excluded from the process.

To get an FHA loan, you need to put down at least 3.5% of the purchase price. The general down payment requirement for FHA loans ranges from 3.5% to 10%. You can put down more, but the usual recommendation is to consider another type of mortgage, such as a conventional mortgage, if you can afford a bigger down payment. The cost of an FHA loan’s mortgage insurance can make it more expensive than other options for borrowers who can make larger down payments.

2. Location Requirements

Another notable difference between the FHA and USDA loan programs is the location restrictions the USDA loan program has. If you want to buy a home with an FHA loan, you can purchase property anywhere in the country. You can buy a four-unit place in the heart of New York City or a sprawling ranch in the middle of Montana.

That’s not the case with a USDA loan. The property you purchase with a USDA loan needs to be located in an eligible area. Eligible areas include rural parts of the country, as well as some suburban areas. You might be surprised at what counts as “rural” under the USDA’s definition, so unless you want to buy a home in a metropolitan area, it can be worthwhile to check the USDA’s eligibility map to see if your location qualifies.

3. Credit Score Eligibility

Your credit score plays a part in the approval process when you want to get a mortgage to buy a home. But, in the case of an FHA or USDA loan, it might play less of a part than it would if you were applying for a conventional mortgage.

Both loan programs have more lenient credit requirements than other mortgage programs. The USDA loan program has no set credit requirements. That said, the lender you work with might have its own set of requirements for borrowers who want to apply for a USDA loan. Often, a credit score over 640 is recommended for people who are interested in a USDA loan.

The credit requirements for an FHA loan determine the size of the down payment you can make. If your score is less than 580 but more than 500, you can qualify for an FHA loan but need to put down 10%. If your score is over 580, you can put down as little as 3.5%.

4. Mortgage Insurance Requirements

Mortgage insurance is part of the bargain whether you apply for an FHA or a USDA loan. But the amount of your mortgage insurance premiums will vary considerably depending on the program you choose.

FHA loans have higher mortgage insurance premiums than USDA loans, particularly if you make a smaller down payment. If you put down the minimum 3.5%, your monthly mortgage insurance premium will be 0.85% of the loan amount. You need to pay the premium for the entire term of the mortgage. The monthly premium is in addition to the 1.75% you paid upfront.

The required premiums, or funding fee, for a USDA loan aren’t more than 0.5% of the remaining balance and 3.75% upfront. You have to pay the monthly premium through the entire term of the USDA loan.

5. Closing Costs

With both a USDA and an FHA loan, the borrower is responsible for paying closing costs. But how the closing costs are handled can differ. With a USDA loan, you can borrow more than the value of the home and use some of the extra money to cover closing costs. That’s usually not an option with an FHA loan. Financing some or all of the closing costs can make buying a home more affordable.

An FHA loan does allow you to accept seller concessions or a seller assist. If you’re buying a home in a buyer’s market, meaning there are more houses for sale than people interested in buying, you might be able to get the seller to contribute to your closing costs. Usually, a seller assist is tougher to get in a seller’s market, when there are more buyers than homes available.

6. Income Requirements

Your income doesn’t matter if you’re interested in an FHA loan. There are no maximum or minimum income requirements, aside from being able to prove that you have an income and that it’s enough to pay back your loan. Usually, you’ll need to provide tax returns, pay stubs and proof of employment when you apply for an FHA loan.

The guaranteed USDA loan program does have income requirements. Your income can’t be more than 115% of the median income in your area. Since the cost of living and income varies considerably from state to state, some areas have higher income maximums than others. You can check to see if your income is eligible based on your location at the USDA’s website.

7. Loan Terms

The length of your mortgage can vary depending on whether you go for a USDA or FHA loan. FHA loans are available in 15- or 30-year terms. Depending on your income and goals, there are advantages and disadvantages to choosing a 15- or 30-year mortgage.

A mortgage with a 15-year term typically has a lower interest rate than a 30-year mortgage. But your monthly payments are usually higher with a 15-year loan. Another benefit of a 15-year mortgage is that you pay it off more quickly. Mortgages with 30-year terms usually have slightly higher interest rates but lower monthly payments, helping to make buying a home more affordable.

If you want a USDA loan, you can’t select a 15-year term.

8. Home Requirements

The requirements for the home you purchase with a USDA or FHA loan vary slightly. In addition to meeting location requirements, a home purchased with a USDA loan needs to meet certain habitability requirements. Most notably, it needs to be safe to live in. The house also has to act as your primary residence.

The home you purchase with an FHA loan needs to meet HUD health and safety standards. An appraisal is part of the loan application process. During the appraisal, the appraiser will determine more than the market value of the home. They’ll also assess its quality and whether it meets safety requirements.

While you do need to live in the home you purchase with an FHA loan, houses with multiple units, such as two or three-unit properties, are eligible for FHA mortgages.

A home inspection isn’t required for a USDA loan. But it’s a good idea to get an inspection before you purchase a home to ensure there aren’t major, hidden concerns with the property. You can negotiate with the seller if an inspection turns up any issues.

Is It Easier to Get an FHA Loan or a USDA Loan?

Whether it’s easier to get a USDA or an FHA loan varies based on the borrower. If your goal is to buy a home in a rural or suburban area, your income isn’t more than 115% of the median in the area and you meet other requirements, a USDA loan is going to be easier to apply and get approval for.

But if you earn more than 115% of the median income, you won’t be able to get a USDA loan, even if you want to purchase a home in a rural or suburban area.

[download_section]

Is an FHA or a USDA Loan Better?

Whether an FHA or USDA loan is better or not also depends on the borrower and their specific circumstances. USDA loans are ideal for borrowers with lower incomes who want to buy in rural areas. FHA loans are often ideal for borrowers who have a small down payment saved and credit scores that aren’t high enough to get a low interest rate on a conventional mortgage.

How to Decide Between FHA and USDA Loans

Some of the questions to ask when deciding between an FHA or USDA loan include:

- Where do you want to purchase a home? You can choose the FHA or USDA loan if you want to purchase a rural or suburban home. The USDA loan is exclusively compatible with homes in rural areas and select suburban regions.

- How much can you afford to put down? If you don’t have anything saved for a down payment, a USDA loan is likely the better option.

- Do you have enough for closing costs? The USDA loan covers up to 100% of the property’s appraised value. With a large enough down payment, you may have room to roll in closing costs.

- How long do you want to have a mortgage? While both USDA and FHA loans offer 30-year mortgages, only FHA loans give you the option of a 15-year term.

- What’s your income? If your income is higher than 115% of the local median, you would only qualify for the FHA loan.

Why Trust Us for FHAs and USDAs?

Assurance Financial is an experienced financial agency that has helped numerous buyers choose the ideal borrowing option for their circumstances. We use our experience and analytical skills to help customers determine if an FHA or USDA loan complements their financial situations and lifestyle preferences. Then, through a seamless online application system, we streamline the process of connecting borrowers with the money they need to purchase a home.

Our end-to-end services and relationship-driven approach have earned us an average rating of 4.98 stars across thousands of reviews.

Apply for a Mortgage With Assurance Financial Today

Apply today to experience the services that make us a trusted provider of FHA and USDA loans.

For more on our mortgage options, find an Assurance Financial adviser near you.

Linked sources:

- https://assurancemortgage.com/fha-loans/

- https://www.consumerfinance.gov/owning-a-home/loan-options/fha-loans/

- https://assurancemortgage.com/everything-need-know-fha-loans/

- https://www.hud.gov/sites/documents/15-01MLATCH.PDF

- https://assurancemortgage.com/usda-loans/

- https://www.rd.usda.gov/programs-services/single-family-housing-programs/single-family-housing-direct-home-loans

- https://www.rd.usda.gov/programs-services/single-family-housing-programs/single-family-housing-guaranteed-loan-program

- https://www.ecfr.gov/current/title-7/subtitle-B/chapter-XXXV/part-3555#p-3555.107(g)

- https://assurancemortgage.com/fixed-interest-rate-vs-adjustable-interest-rate/

- https://assurancemortgage.com/what-is-down-payment-home-loan/

- https://assurancemortgage.com/what-is-a-usda-loan-how-to-apply/

- https://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do

- https://assurancemortgage.com/important-credit-score-for-home-loan/

- https://assurancemortgage.com/buyers-vs-sellers-market/

- https://eligibility.sc.egov.usda.gov/eligibility/incomeEligibilityAction.do?pageAction=state

- https://assurancemortgage.com/15-vs-30-year-mortgages/

- https://www.rd.usda.gov/files/3550-1chapter05.pdf

- https://assurancemortgage.com/finding-right-mortgage-loan-for-you/

- https://assurancemortgage.com/apply/

When you’re shopping for a home, you want to do as much as possible to show sellers you’re serious and make yourself stand out in a crowded field. That’s particularly true when you’re looking to buy in a seller’s market. In a seller’s market, there are more people trying to buy homes than properties available.

One way to make yourself stand out is to get a pre-approval from a lender. With a mortgage pre-approval letter in hand, you demonstrate to sellers that you’re ready to buy and likely have the loan to back you up.

Before you get a pre-approval, you might wonder about its impact on your credit score and report. However, for the most part, getting pre-approved will only help you. Read on to have your questions about pre-approval answered.

What Is a Pre-Approval?

A mortgage pre-approval is essentially a stamp of approval from a lender. It’s very similar to the process of applying for a mortgage loan. A lender will review your documents and history during the pre-approval process to determine your interest rate and how much you can comfortably borrow.

Mortgage pre-approval is sometimes confused with pre-qualification, but there are distinct differences. A pre-qualification is generally less serious than a pre-approval. It’s like a rough sketch. When pre-qualifying you, a lender might look at your income and ask about your credit history, but they won’t dig very deep.

A pre-qualification can be valuable when you’re in the early stages of home buying. For example, pre-qualification can give you some general guidance if you’re about to dip your toes in and aren’t sure how much you can afford to buy or if you’d even be eligible for a mortgage. It’s an estimate regarding what you can afford and whether you’re likely to qualify for a loan.

A pre-approval comes after the pre-qualification once you know that you want to buy a home and are ready to jump in with a real estate agent. To get a pre-approval, you need to provide the lender with some documentation and evidence of your financial status.

During the pre-approval process, a lender will look at documents that verify your income, such as income tax returns or paystubs. They might also ask you to provide copies of bank statements to show how much money you have available and what you’ve saved for a down payment.

Crucially, a pre-approval involves a credit check. The lender will review your credit history during the credit check, looking for concerns such as missing or late payments. They might also look for bankruptcies and other signs that you’ve had trouble with loans in the past. They’ll get your credit score, too.

A pre-approval doesn’t always guarantee that you’ll get final approval for a mortgage. There can be circumstances that stand in the way of getting approved, such as an issue with the property’s title or a home appraised at less than the sale price. Changes in your financial situation between the time you get pre-approved and when you’re ready to apply for the actual mortgage can also affect the process.

Why Get a Pre-Approval?

Although a pre-approval isn’t a 100% guarantee that you’ll get a mortgage, it’s an excellent first step. It makes you look more attractive as a buyer to sellers. When someone is selling a property, they want to work with buyers who will provide the smoothest experience possible. Someone who’s got a mortgage lender behind them and who’s taken the time to go through the pre-approval process is more likely to commit to the home buying process.

Getting pre-approved also helps you narrow down your options. For example, a lender might pre-approve you for a $250,000 loan. With that information in hand, you know where you can set your budget.

Going through the pre-approval process also allows you to shop around and see what different lenders can offer you. You’ll be more likely to get a mortgage that works for your budget and financial situation if you have a chance to shop around.

How to Get Pre-Approved

One way to look at the pre-approval process is as a dress rehearsal for an actual mortgage application. You’ll need to give the lender certain documents, and they’ll review your financial information to determine the following:

- How much you can borrow

- What interest rate you’ll pay

- The mortgage term

To start the pre-approval process, your lender will most likely ask you to provide:

- Proof of income: Depending on how you earn income, your proof can be paystubs or tax returns. Self-employed individuals usually provide tax returns, while employed people can provide paystubs.

- Proof of assets: A lender might also request bank statements or other documents that verify how much you have saved or invested. Some lenders will only verify that you have enough for the down payment and closing costs. Others will want to see evidence of cash reserves and savings beyond what you need for closing costs and down payment.

- Employment verification: You will most likely need to verify that you’re still employed or still have a source of income. You can ask your employer for an employment letter, or the lender might call your employer to see if you’re still working there.

- Identification: A lender will need to verify your identity to run the credit check and confirm that you’re who you claim to be. Besides providing your social security number, you’ll also have to provide a photo ID, such as a passport or driver’s license.

- Information about other debts: Your other debt obligations can affect whether you get approved for a mortgage or not or how much you’re approved to borrow. A lender will likely ask you to provide information about any other debts, including the monthly payments and the total amount owed.

Once you’ve given all your details to the lender, they’ll run your credit score and review the information to determine a maximum loan amount and your interest rate. The higher your income and credit score, the more you can borrow and the lower your rate. Whether it’s 15 or 30-years, the length of your mortgage term will also affect your loan amount and interest rate.

If you get the pre-approval, the lender will give you a letter detailing how much you can borrow and the interest rate. When you make an offer on a home, you submit a copy of the pre-approval letter to the seller.

Usually, a pre-approval locks in the interest rate for a limited period, such as 90 days. That means you should find and buy a house within that period to get the rate. Otherwise, you might have to start the pre-approval process over again.

What’s in Your Credit Score?

Your credit score plays a significant role during the mortgage approval process. Your score affects the type of mortgage you qualify for and the interest rate you pay. Your score can affect whether you get approved or not. Some mortgage programs, such as FHA loans, are designed to help borrowers who might not have the credit score needed to qualify for a conventional loan.

The companies that calculate credit scores use secret formulas to come up with the three-digit numbers. While the companies keep their exact formulas under wraps, they have detailed the factors that contribute to your overall score:

- Total amount of debt: The total amount is how much you’ve borrowed at the moment.

- Payment history: Your payment history details whether you pay on time or have a history of paying 30 or more days late.

- Age of credit accounts: The age of your credit accounts refers to how long you’ve had a credit history, dating from the time you opened your first currently active credit account.

- Number and type of accounts: The number of accounts refers to how many credit cards or loans you have open. The type refers to whether those accounts are secured loans, credit cards or other types of unsecured loans.

- How much credit you use: How much credit you use refers to the amount you’ve borrowed compared to how much you can borrow. For example, you have a credit utilization ratio of 10% if you have a $1,000 balance on a credit card with a $10,000 limit.

- Recent credit applications: Recent credit applications refers to how many accounts you’ve applied for in the past couple of years. Any recent mortgage pre-approvals or credit card applications will show up here.

Each factor has a different impact on your score. For example, payment history typically has the most considerable effect, while credit applications and types of accounts have less of an impact.

Does Getting Pre-Approved Hurt Your Credit?

In short, yes, getting pre-approved for a mortgage can affect your credit score. But the impact is likely to be less than you expect and shouldn’t stand in the way of you getting final approval for a mortgage.

What Happens to Your Credit Score After a Pre-Approval

When a lender checks your credit for a mortgage pre-approval, they run a hard inquiry. A hard inquiry can cause your score to dip slightly. The impact on your credit will be minimal. The small credit score change after pre-approval won’t cause the lender to change their mind when it comes time to apply for a mortgage.

The drop is temporary. If you continue to pay your bills on time and are punctual with your mortgage payments once you receive one, your credit score will soon recover.

What Are Different Types of Credit Inquiries?

There are two ways of checking credit. A lender might run a soft or hard inquiry, depending on the situation. Each type of credit inquiry has a different impact on your credit score.

Hard Credit Inquiries

When lenders perform the pre-approval process, they run a hard credit inquiry. A hard credit inquiry is like a large flag that tells other lenders you’re in the process of applying for a loan.

A hard credit inquiry affects your credit score, as it signals that you’ve recently applied for credit. If you have several new credit applications on your credit report within a short period, such as within a few months, a lender might see that as a red flag or a sign that you’re having financial difficulties. Usually, the more hard inquiries you have in a limited period, the more significant the impact on your score.

For that reason, it’s usually recommended that you do not apply for a car loan, credit card or other types of loan while you’re applying for a mortgage.

It’s important to understand that although a hard inquiry often causes a score to drop, hard inquiries in and of themselves aren’t necessarily bad things. You need a hard inquiry to get any type of loan.

Soft Credit Inquiries

A soft credit inquiry doesn’t have an impact on your credit score. A soft inquiry occurs whenever you check your credit report. A lender won’t be able to see that you’ve run a credit check on yourself.

If a lender wants to pre-approve you for a credit card, they’ll also run a soft inquiry on your credit. The lender uses the information they get to put together a credit card pre-approval offer to send you. Other examples of a soft inquiry include when a utility company checks your credit before opening a new account or when an employer runs a credit screening before hiring you.

Does Getting Multiple Pre-Approvals Hurt Your Credit Score?

Shopping around for a mortgage is often recommended to people looking to buy a home. But, if getting pre-approved for a mortgage requires a hard inquiry on your credit report, won’t getting several pre-approvals create several hard inquiries, increasing the damage to your credit score?

Fortunately, the impact several pre-approvals have on your credit score is minimal. When you get pre-approvals for multiple lenders, the credit bureaus typically lump them together as a single hard inquiry. Bureaus understand it’s common to shop for a mortgage. Borrowers who get pre-approvals from multiple lenders aren’t penalized for trying to get the best offer possible.

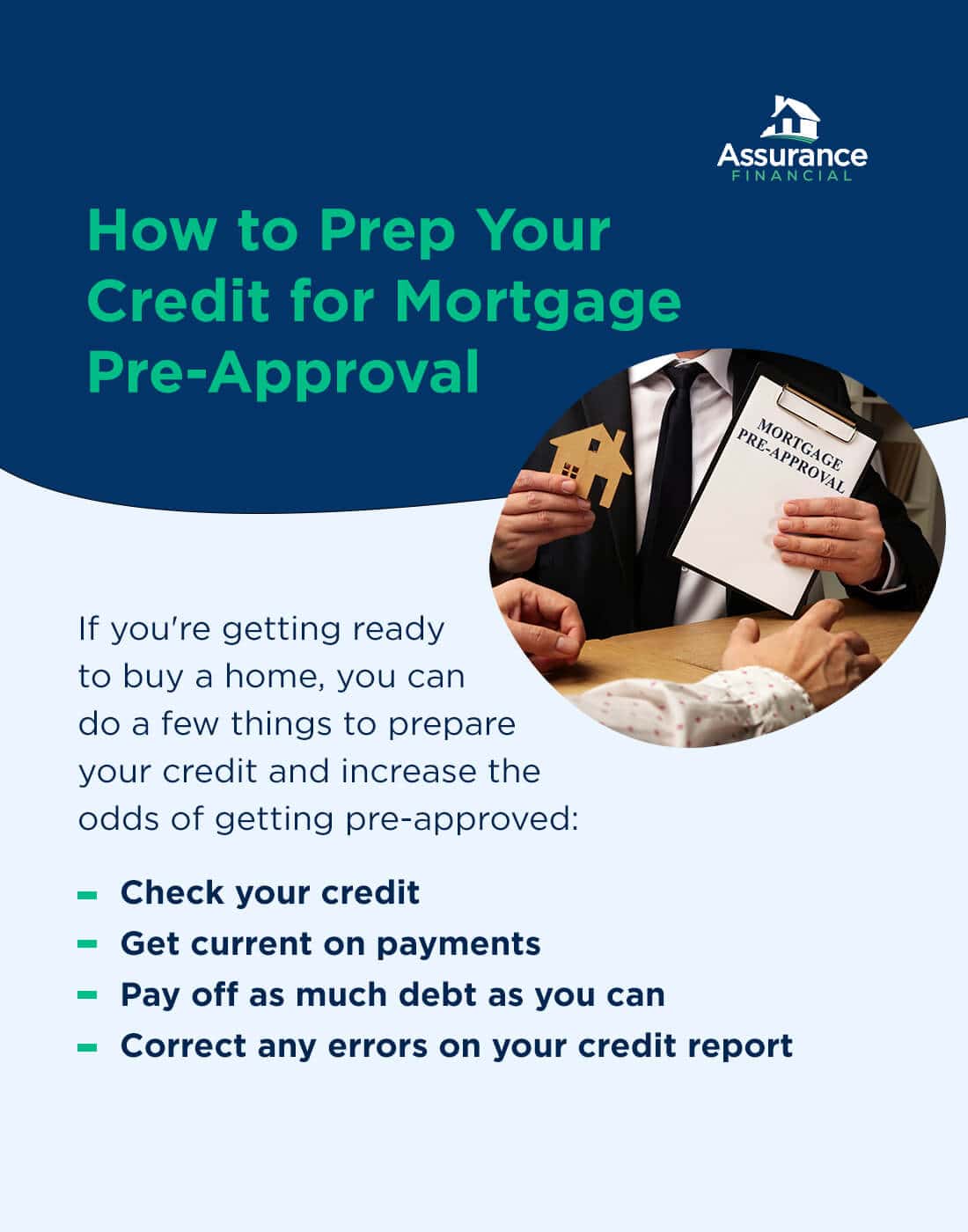

How to Prep Your Credit for Mortgage Pre-Approval

If you’re getting ready to buy a home, you can do a few things to prepare your credit and increase the odds of getting pre-approved:

- Check your credit: Checking your credit creates a soft inquiry, which doesn’t affect your score. It’s a good idea to check your credit for at least several months or even up to a full year before you start looking for homes. Checking in advance gives you plenty of time to take action to improve your history and score if needed.

- Get current on payments: If you have a history of paying late on any of your loans, make an effort to get current on your payments. Pay off any late fees and back-due amounts. Then, commit to paying your loans by the due date every month. You can set up a payment reminder or schedule automatic payments to ensure you don’t forget.

- Pay off as much debt as you can: How much debt you have or the amount of debt compared to your income can affect your credit score and eligibility for a mortgage. If you have a lot of debt, try to pay some off before applying for a home loan.

- Correct any errors on your credit report: The credit bureaus can make mistakes. Let the agency know if you notice anything strange or incorrect on your credit report. Common errors include accounts that belong to someone else — usually someone with a similar name — or accounts you’ve closed still showing as open. </span >In some cases, errors in your credit report can be a sign of identity theft or fraud.

[download_section]

Do’s and Don’ts After Getting a Mortgage Pre-Approval

Once you have the pre-approval, you’re ready to roll and can put in an offer on a home. Remember that getting pre-approved doesn’t mean you’ll necessarily get fully approved for a mortgage. Certain actions between the pre-approval and final approval can affect your credit and interfere with the mortgage process. Here’s what to do and not do when you’re in the home stretch of getting a mortgage.

Do: Continue to Pay Off Other Debts

If you have other debts, keep making payments on them while looking for a home and going through the mortgage process. Any change in your payment history can impact your credit score, causing a lender to reconsider approving you for a mortgage.

Don’t: Apply for New Credit

While credit bureaus group several mortgage pre-approvals together and count them as a single hard inquiry, the bureaus won’t group other loan applications with your mortgage pre-approval. Several other hard inquiries can affect your credit score, such as a credit card application or personal loan application.

Applying for new credit while shopping for a home can also raise alarm bells for your mortgage lender. They might wonder why you’re applying for multiple loans while you’re trying to buy a home. To keep your lender calm and increase your odds of approval for a home loan, wait until after closing to apply for other types of credit.

Do: Shop for a Home

Pre-approvals don’t last forever, so it’s a good idea to get out there and start looking for your dream home once you have the pre-approval letter in hand. Usually, your pre-approval will be valid for several months, so don’t panic if you don’t find your home immediately.

Contact your lender if you don’t find the right home before the pre-approval expires. Some are willing to extend the offer beyond the initial period without making you go through the entire credit check and application process again.

Don’t: Make Other Big Purchases

If possible, try not to make big purchases between getting pre-approved, putting an offer in on a home and closing. Buying a new car or new furniture can affect your cash reserves, which might make a lender reconsider approving you for a mortgage. Using a credit card to buy furniture will increase the amount of debt used, affecting your credit score.

It’s better to wait until you’ve closed on your home to purchase furnishing for it or before making any other large purchases.

Do: Keep Your Lender Up-to-Date on Any Life Changes

Depending on how long it takes to find a home and put in an offer, you might experience some life changes between getting pre-approved and closing on your home. Let your lender know whether it’s a change in income, a new family member or getting an inheritance. Changes in your financial status can affect your mortgage eligibility.

Don’t: Quit or Change Jobs

A history of steady employment is very attractive to mortgage lenders, as it suggests that you’ll continue to have the means to pay your mortgage for years to come. While your job status might be out of your control in some cases, if possible, wait until you’ve closed on the home before quitting your current gig or finding a new job.

Becoming unemployed before you have final mortgage approval affects the process. The same is true if you change jobs and accept a lower-paying position.

Get Pre-Approved With Assurance Financial Today

The first step to getting a mortgage is getting pre-approved. Apply today or contact a loan officer.

Linked Sources:

- https://assurancemortgage.com/buyers-vs-sellers-market/

- https://assurancemortgage.com/15-vs-30-year-mortgages/

- https://assurancemortgage.com/important-credit-score-for-home-loan/

- https://assurancemortgage.com/fha-loans/

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/how-to-get-a-mortgage-loan/

- https://assurancemortgage.com/apply/

Key Takeaways

- In a seller’s market, buyers face significant disadvantages and have limited leverage to negotiate for concessions, contingencies, or repairs, requiring focus on what matters most.

- Getting pre-qualified for a home loan is essential to demonstrate you’re a serious buyer capable of securing financing for a specific amount.

- Strategic planning and financial readiness are critical to compete effectively with other buyers in competitive markets.

During home shopping, most homebuyers want to know whether the current housing market is a seller’s market or a buyer’s market, along with how to get a good deal in a seller’s market. Though certain seasons tend to be busier, fluctuations in the housing market are more likely influenced by supply and demand than the season. As such, it’s essential for buyers to be aware of the state of the housing market and whether the area is currently experiencing a seller’s market or a buyer’s market.

To help you navigate the homebuying process, we cover how to identify whether you’re shopping in a buyer’s or seller’s market, what the current housing market is in 2024 and how to negotiate buying a house in a seller’s market.

Buyer’s vs. Seller’s Market

The housing market is either a buyer’s market or a seller’s market. These terms mean that the market either favors buyers or sellers.

What Is a Buyer’s Market?

When the supply of properties exceeds demand, this is known as a buyer’s market. When many homes are available for purchase yet there is a low number of interested buyers, buyers have an advantage. A buyer has leverage over the seller because there is less competition over a home.

In a buyer’s market, homes are on the market for longer periods and real estate prices drop. Essentially, sellers are competing with one another to attract buyers. A seller may be forced to drop their asking price to make the sale, and they may be more open to negotiating offers.

When you’re home shopping, a buyer’s market is the ideal time to buy. You can take your time, visit as many homes as you want before making an offer and negotiate with the seller to bring the price down. In a buyer’s market, sellers need to make repairs, market their property and price it competitively.

What Is a Seller’s Market?

On the other hand, when demand for homes exceeds supply, this is known as a seller’s market. Though many individuals are interested in purchasing a home, the inventory of available properties is low. Sellers have an advantage in this housing market since the lack of available homes creates more competition among buyers. Homes sell more quickly in a seller’s market, and because buyers are competing over the same properties, sellers can increase asking prices.

With this price increase, buyers may need to be willing to spend a greater amount of money on a property. When there are many parties interested in a home, buyers rarely have negotiating power and may need to accept a property as-is. A housing shortage can lead to a bidding war, and the competing offers can drive the price above the seller’s asking price. Sellers can take time to carefully consider their offers and only consider pre-qualified buyers.

Even though sellers have an advantage in a seller’s market, you can still succeed as a homebuyer and find the home of your dreams in this market.

Signs of a Seller’s Market

Before you start home shopping, you may want to determine whether your local area is currently experiencing a seller’s market or a buyer’s market. The following are some signs of a seller’s market:

- Lack of price cuts: Sellers are more likely to drop their asking prices in a buyer’s market, so several price cuts to listed homes could indicate a buyer’s market. On the other hand, a lack of price cuts can indicate a seller’s market. Keep in mind, however, that sellers can have unrealistic expectations about the value of their properties, so look for a trend in pricing rather than a single occurrence.

- Sales over asking price: Check the recent sales of the property you’re interested in and homes comparable to it. If homes have usually been selling above the asking price, this may indicate a seller’s market. Homes selling below the asking price, on the other hand, may indicate a buyer’s market.

- Bidding wars: A bidding war occurs when multiple buyers present competing offers for the same property. Buyers attempt to outbid each other by gradually increasing their offer. If you keep getting into bidding wars or you know friends or family who are home shopping and getting caught in bidding wars, this could indicate that the housing market is currently a seller’s market.

- Market trends: One of the strongest indicators of the current housing market is determining whether home prices in your area have been decreasing or increasing. Look at market trend reports to review the homes in your local area to get information on the median sale price, the number of properties on the market and how the numbers have changed during the last year. Increasing prices and decreasing inventory often indicate a seller’s market.

- Shorter time on the market: How long a home sits on the market is another factor that could indicate whether the housing market is currently a seller’s or buyer’s market. In a seller’s market, homes sell faster than in a buyer’s market. So if you notice a lot of quick sales, this could indicate a seller’s market.

- Fewer houses on the market: Consider the homes currently for sale. If the inventory is large, your local area may be in a buyer’s market. However, if the inventory is limited, then your local area may be in a seller’s market. Divide the number of properties for sale by the number of properties that were purchased in the past month. If you come up with a low number, this could indicate a seller’s market.

Is It a Buyer’s or Seller’s Market in 2024?

The current housing market is a seller’s market. The pandemic has had a dramatic impact on the housing market and ushered in new rules and processes, such as virtual open houses and tours.

The typical seasonality of home buying has changed in the past couple of years. While spring and summer used to be the height of the home buying season and turn to a seller’s market, the pandemic has led to a highly competitive seller’s market that has endured and made buying a home challenging, even during the slower winter season.

Current Trends in the Housing Market

Keep the following trends in mind if you are buying in the current seller’s market:

Virtual Home Tours

Many real estate agents are conducting virtual tours and walkthroughs as the buyer’s first view of the home. As a buyer, you may encounter everything from a simple video walkthrough to a more immersive experience with 3D technology.

A virtual tour can save you time that you would’ve otherwise spent traveling to and from the property, especially if you looking to buy in a different city or state. Before the virtual home tour, make sure you download the appropriate app, charge your device and have a good internet connection. You should also ensure you’re in a quiet place where you can hear the real estate agent.

Take advantage of this opportunity to view the home virtually by asking the agent to zoom in on certain areas, open closet doors and describe specific features.

Increased Buying Activity

Buyers are showing continued interest in purchasing properties, even as mortgage rates and home prices steadily rise. While the number of homes for sale on the market hit a record low, sales and median home listing prices shot up.

A slight majority of buyers have owned a home previously, and those that have been renting before buying cite the desire to own a home as their decision for buying. Others want a larger property or want to move to be closer to family or friends.

Bids Above the Asking Price

With so many competitive buyers bidding on homes, many offers are coming in above the asking price. As we approach the spring and summer seasons, this flurry of homebuying activity is likely to only get more hectic. Buyers have been lining up to purchase homes for months, even in the winter, which has led to an unusually low real estate inventory and greater competition over homes.

This increase in demand drives up prices, and other buyers are likely to put in offers on the same property, so if you want to get your dream home, you may have to place a bid above the asking price.

How To Buy a House in a Seller’s Market

If you want to buy now, in a seller’s market, you should know how to navigate this housing market and get a good deal even when there is a limited supply of homes. Though you probably shouldn’t expect to negotiate for repairs or convince a seller to accept less than their asking price, you can utilize some methods and strategies to successfully compete in this ultra-competitive housing market. Follow these tips for buying in a seller’s market:

1. Be Aware of the Current Market

While home shopping and making an offer, keep in mind what kind of housing market you’re shopping in and know that you are at a disadvantage. In a seller’s market, you may not have the leverage to push for concessions, contingencies, repairs or a strict closing date. Be sure to focus on what matters most to you, and consider whether the stipulations you want to be included in the contract are worth losing the home over.

2. Get Pre-Qualified for a Home Loan

Getting pre-qualified for a mortgage means a lender is willing to lend you a certain amount for the purchase of a home. Though this isn’t a guarantee of a mortgage, it gives you a maximum loan amount to work with. Many sellers only want to consider offers from pre-qualified buyers, especially in a seller’s market. Apply to get pre-qualified with Assurance Financial when you’re ready.

[download_section]

3. Get Pre-Approved for a Mortgage

After getting pre-qualified, your next step is getting pre-approved for a mortgage. A pre-approval is based on an analysis of your finances. The pre-approval offers a more concrete number for a loan amount. The lender will review your completed mortgage application and conduct a credit check. Though pre-approval is also not a guarantee of a mortgage, it’s a more accurate estimate than pre-qualification.

4. Work With a Real Estate Agent

Whether you’re buying in a seller’s market or a buyer’s market, working with a real estate agent can ensure you navigate the current housing market successfully. Real estate agents can give you an advantage over other competitive buyers, as they have the skills and knowledge you need on your side. Real estate agents may also have connections allowing them to identify and view homes before they’re even on the market or before the final bids are considered.

To choose the right real estate agent, read their reviews, find out what their experience is and speak with buyers they’ve worked with. After you narrow down your list to a few options, there are a few important questions you can ask to choose the right agent for you:

- What are your fees?

- How familiar are you with this area?

- What’s the most difficult deal you facilitated?

- Do you have access to properties that aren’t listed yet?

- How can you strengthen my offer in a competitive seller’s market?

Your real estate agent can help you strengthen your offer by looking beyond price. Consider what else the seller values to give you an advantage, such as conveniences or contingencies. For example, if you can close earlier or you don’t need to move immediately and can give the seller more time to find their next home, this could give you an advantage when the seller is considering their offers.

5. Have Your Down Payment Ready

Be sure to save up enough for a down payment. If someone is giving you the money for your down payment in the form of a gift, discuss this process with your lender. The person giving you this money may need to write a gift letter that explains you don’t need to repay the money. Many lenders will also want to see the bank statements from the account with your down payment funds, and they may want to see that the funds have been in the account for a couple of months.

6. Look at Homes Under Budget

In a seller’s market, many sellers receive multiple offers on their homes. As a buyer in a seller’s market, you should look for homes that fall below your spending limit. Other buyers are likely to bid higher than the asking price, so you want to look at homes on which you can afford to bid higher than the asking price. With this strategy, you can afford to bid up without exceeding your comfortable spending limit or needing to dip into your savings.

7. Act Quickly

When you find your dream home in a seller’s market, it’s important to act quickly. Hesitating to make an offer on a home you know you love and want to purchase may mean losing your dream home. By the time you make your offer, the home may no longer be available. Ensure you get preapproved for a home loan before you start shopping so you can make an offer immediately.

8. Stay Patient

In a competitive seller’s market, it’s normal to lose out on homes you’re interested in. Try not to get discouraged, and stay patient. Inexperienced buyers could get frustrated, find themselves caught up in a bidding war and offer more on a home than they’re comfortable spending or more than the property is actually worth.

Keep in mind, though, that you don’t have to give up as soon as you sense someone could outbid you or has an all-cash offer. Deals fall through all the time, as your real estate agent can attest, so being the second-choice offer can still work out in your favor.

9. Widen Your Search

The most popular neighborhoods understandably come at the highest prices. If you want to own a home in a specific ZIP code but homes in the area are not within your budget, you may want to consider widening your search. Identify what you like about this neighborhood, such as the school, parks, public transportation or local businesses and restaurants. Once you determine what features you want in your neighborhood, you can try to find them in locations you haven’t explored or considered before.

10. Avoid Settling

When a homebuyer grows tired of losing out on homes, they may make an offer on a home they wouldn’t be interested in otherwise. Try to avoid this situation, and keep in mind that purchasing a property is a huge, long-term investment. You may be living in and paying for this home for decades, so don’t settle for a home you don’t love unless you need to move immediately.

Similarly, try to avoid fixating on the first home you fall in love with. This can lead to a huge disappointment, or even worse, a bad financial decision made during a moment of desperation.

Contact Us at Assurance Financial to Learn More

As a mortgage lender, Assurance Financial is a home loan expert. We want to help you realize your dreams of owning a home, and our team can assist you through every step of the process, regardless of whether you want to buy a starter home or a vacation home. You have several different loan options for your mortgage, including conventional loans, FHA loans, VA loans and jumbo loans.

With our financial mortgage services, we can offer you a customized option for paying for your home. Contact us at Assurance Financial to learn more about how to find a house in a seller’s market and get the mortgage loan option that’s right for you.

Every year, your family enjoys a getaway in the mountains, at the beach or in a cabin in the woods. And, every year, you wonder if it’s finally time to buy a vacation property.

If you already have a primary residence, purchasing a second home can be an excellent investment. You have a guaranteed vacation spot each year and can rent the house out to bring in some extra income.

The process of buying a vacation home has some things in common with buying your first house. You want to put as much time and effort into finding your dream vacation spot as you did in finding the place you call home. There are a few differences between a vacation property and your primary home when it comes to financing a second property.

Why Buy a Vacation Home?

Buying a vacation home can make good financial sense for a few reasons. One reason is that it sets you up with a vacation spot for as long as you own the home. When you already own your vacation spot, you don’t have to pay for travel expenses such as hotels or rentals anymore, which can save you money over time.

Another reason is that buying a vacation home can give you a source of passive income. You can rent the home out to others when you’re not using it. Renting the property out can help you cover the cost of the mortgage or give you a little extra spending money.

Some people like to buy a property to use as a vacation home now and then move into the property full-time after they retire. If you dream of retiring to the beach or mountains, owning a property already gets you one step closer to achieving that dream.

Finally, you can look at a vacation home as an investment. Over time, the value of the home will likely increase. When your family is no longer interested in vacationing there, you can sell the property or continue to rent it out, generating an ongoing source of income.

Important Questions to Ask Before You Purchase a Vacation Home

Before you start the process of purchasing a vacation home, carefully weigh the pros and cons and ask yourself a few questions to make sure it’s the right option for you.

What’s Your Vacation Style?

Everyone has different vacation styles. Some people prefer to visit the same area yearly, such as the beach, woods or mountains. They like to build up traditions and enjoy the familiarity of staying in the same place.

Others prefer to see the entire world. They might spend a few weeks at the beach one summer, then head off to Europe for a backpacking vacation the next. These people prefer a varied, diverse vacation scene. They choose to visit all the popular vacation spots rather than stay in the same place.

If your vacation style is similar to the first one and you like to go to the same area every year, then buying a second home in that area can make sense. You won’t have to hunt around for a hotel or home rental every time you want to travel. If your style is closer to the second one, purchasing a vacation home might not be the best option for you at the moment.

Buying a vacation home can also make sense if you prefer to take longer vacations or if you want to go away several times during the year. When you own the property, you can easily spend a month or longer there. You can also visit whenever you want, provided you haven’t rented the space out.

Can You Afford a Second Home?

Two residences means two mortgage payments and two sets of property taxes. Buying a second property can stretch your budget depending on your current income and obligations.

Here’s what to look at when deciding whether a second home will work with your budget:

- Your current savings: Ideally, buying a second home won’t keep you from saving for retirement and other goals, such as your kids’ education. If you’re behind on saving for those milestones, waiting to purchase a second home can make sense.

- Your current mortgage: If you’ve nearly already paid off your mortgage, you may have the wiggle room in your budget to buy a second home. Similarly, if you have a lot of equity in your primary residence, you can borrow against it to buy a vacation home.

- Your income: You might have high expenses, such as a big mortgage payment, but at the same time, your income might be high enough to allow you to buy a second home without derailing your other financial goals.

Keep in mind that the cost of a vacation home can vary considerably based on location and size. If you’re comfortable buying a small property in a less popular vacation area, you might get a better price than if you purchased a home in a busier spot or wanted to buy a larger property.

Can You Rent Out the Home?

Unless you decide to make it your primary residence, a vacation home can provide a steady supplemental income stream. You can rent out the property during the weeks you don’t use it or during the low season to bring in some extra cash or help pay down the mortgage.

You’ll want to consider a few factors before you decide to rent out a vacation home, though. While renting the property out can help you pay down the mortgage, you might not want to rely on rental income to cover the second mortgage since you might not rent the property out enough to cover the costs.

Also, consider the effort involved in renting the property. If the vacation home is a considerable distance from your primary home, it can make sense to hire a property management company that’s closer to it. You want someone to be available to respond to the renters’ issues and take care of repairs as needed.

Who Will Take Care of the Home?

Similarly, it’s essential to think about who will care for the vacation home. Houses need regular upkeep. Otherwise, you might spend the first part of your vacation mowing the lawn or fixing leaking pipes.

A property management company can look after the house if you plan on renting it out. The management company charges you for its services and any repairs.

Another option is to hire a housekeeper or groundskeeper to look in on the property and take care of things as needed when you’re not there. The housekeeper can visit weekly during the off-season or when the home is unoccupied to ensure everything’s fine and clean surfaces or the exterior as needed. If you rent the home, the housekeeper can clean it between rentals.

What Are Property Taxes?

Along with paying for the property itself, buying a second home means paying another set of property taxes. Tax rates vary considerably based on location. It’s a good idea to look at taxes before you decide on an area.

The taxes in your dream spot might make owning a home there impractical. However, the taxes in the next town over or in a neighboring vacation locale might be much more reasonable.

How Will You Pay for the Home?

You have a few options for paying for your vacation home. If you have savings, you might pay for it in full, in cash. Another option is to refinance the mortgage on your primary home and use the proceeds from that to pay for a second home.

You can also take out a second mortgage, if you have the credit, a down payment and can afford the additional monthly mortgage payment. You might want to use the rental income from the property to cover the mortgage cost. A more reliable option is to ensure you can afford the mortgage without renting the property out. That way, you’ll always be able to pay the mortgage, even if no one is renting your vacation home.

Does Owning a Second Home Affect Your Taxes?

Buying a second home affects your taxes in a few ways. First, if you rent the property out, you’ll need to declare the rental income when you file your taxes. You might also be able to deduct expenses related to the rental, provided you meet the 14-day rule, meaning you don’t use it as a residence for more than two weeks or 10% of the number of days you rent it out.

Owning a second home can mean you can deduct the interest you pay on the mortgage, provided the total value of both mortgages is less than $750,000. You can deduct property taxes, too.

Benefits of Owning a Vacation Home

If it works for your budget, there are definite benefits to owning a vacation home:

- Better vacations: When you own a vacation property, your holidays can be longer and more affordable. Instead of spending $100 or $200 per night on a hotel or rental home, you’re building equity in your vacation property when you own the house. If you work remotely, you can easily spend the entire summer at your vacation home.

- You can swap: Owning a vacation property doesn’t limit your vacations to one geographic area. You might also sign up for a home exchange program that lets you swap homes with other vacation homeowners, giving you some variety.

- Additional income stream: Your vacation property can create an additional revenue stream for you, helping you build up a solid financial cushion. Just be sure to balance the cost of managing a rental property and the other tax responsibilities with the income it brings in.

- Improved quality of life: Owning your vacation spot can mean you see an improvement in your quality of life. If you’ve had a rough week at work, you can dash off to your cabin in the woods or your home by the shore for some much-needed relaxation.

- Greater financial security: A vacation home can be an investment that leads to greater financial security. You can sell the property later and enjoy a decent return on it. You can also use it as your primary home in retirement or pass it on to your children.

- Tax breaks: Owning two homes can mean more tax deductions, which can lower your tax bill and help you save more money.

How to Pay For a Vacation Home

If you’re not going to pay cash for your second home, you have a few options for financing a vacation property.

1. Cash-Out Refinancing

You can refinance your primary mortgage to either pay for your second home or come up with a down payment for your vacation home. When you apply for a cash-out refinance, you replace your existing mortgage with a larger one. The amount you can borrow is based on the market value of your home.

Here’s an example. You purchased your first home 15 years ago for $150,000. You still have about $30,000 left on the principal. Since then, the home’s value has increased to $350,000. The vacation home you’re interested in purchasing costs $175,000. You decide to refinance your home, borrowing 80% of its current value ($280,000).

Since the amount you’re borrowing is more than you owe on the mortgage, you receive $250,000 in cash. You can then use that cash to purchase your vacation home.

A cash-out refinance might not always provide you with enough to cover the entire cost of a second home. For example, if the value of your home hasn’t increased by much since you bought it, you might not have enough equity in your home to get that much cash when you refinance. Instead, you might be able to get enough money to cover the down payment then apply for a mortgage on the vacation home.

There are some things to consider before you refinance. One is the cost of the refinance. You’ll have to pay closing costs when you refinance, which can be several thousand dollars.

Another is the interest rate on the refinanced loan. Interest rates are still pretty low but might not be lower than what you’re currently paying, based on when you took out your first mortgage. You might end up with a higher rate than you started with, which means you’ll spend more on your mortgage over time.

2. Home Equity Loan

Another way to tap into your primary home’s equity and use it to buy a second home is through a home equity loan. While a refinance replaces an existing mortgage with a new one, a home equity loan is a second loan in addition to your mortgage.

The loan size depends on the amount of equity in your primary home. For example, if your home is currently valued at $300,000 and you owe $150,000 on your mortgage, your equity is $150,000. You can choose to borrow against the equity, taking out a home equity loan for $100,000. You’ll get the $100,000 in a lump sum, which you can then use to make a big down payment on a vacation home.

If your home is worth enough and you have enough equity, you might be able to borrow enough to cover the full cost of a second home.

Usually, you can borrow up to 80% of the equity in your home. Similar to refinancing, you’ll have to pay closing costs on a home equity loan, which can add up. Closing costs vary based on your location.

One drawback of a home equity loan is losing your home if you fall behind on payments. You’re borrowing against your home, and a lender might foreclose on it if you can’t make the payments on either your home equity loan or your primary mortgage.

3. Second Mortgage

Suppose you don’t have much equity in your current home or don’t want to put your primary residence up as collateral for your vacation home. In that case, another option is to take out a conventional mortgage for your vacation home.

Getting a second mortgage is different from getting your first mortgage in many ways. A lender will want to check your credit, verify your income and ensure you have a down payment. Usually, the lending requirements are stricter for a second home than for your first, particularly if you’ll have two mortgages simultaneously.

If you have a down payment saved up, have an excellent credit score and don’t owe too much on your first mortgage compared to your income, getting a second mortgage can be the way to go.

Vacation Home Mortgage Requirements

Lenders consider vacation homes to be somewhat riskier than primary residences. A borrower is more likely to default on a second property than on their primary home if they lose their job or otherwise can’t afford payments. For that reason, vacation home mortgage requirements are usually a little stricter than for a first home.

Here’s what you’re likely to need to take out a second home mortgage.

1. Down Payment

How much you need to put down on your vacation home depends on how you plan on using it. If you live there at least some part of the year, the lender may consider the home as a second residence and may require a slightly lower down payment. If you plan on renting the property out for much of the year, a lender is more likely to consider it an investment property and might require a down payment of 20% or more.

2. Debt to Income Ratio

Your debt to income ratio (DTI) compares how much you owe to how much you earn. The lower your DTI, the less risky you look to lenders. Paying off your primary mortgage before borrowing for a second home can help you lower your DTI and increase your odds of being approved for a loan.

Lenders look at all your debts when determining your DTI. Paying off your credit cards and avoiding taking on more debt as you prepare to buy a vacation home will also increase your odds of approval.

3. Credit Score

Your credit score matters when you want to take out a mortgage for a second home. It might matter more now than it did when you got your first mortgage, as some mortgage programs, such as the FHA, VA or USDA loan programs, accept buyers with less than excellent credit scores.

4. Cash Reserves

You might not have needed to have much cash in the bank to buy your first home. With a second home, it’s a bit different. Lenders usually like to see cash reserves — money in a savings account — worth at least two months of mortgage payments. Having some cash reserves gives the lender a little peace of mind that you’ll keep paying even if you hit a financial rough patch.

In many cases, a lender will look at the big picture when deciding whether to approve you for a second home mortgage or when determining the interest rate to offer you. For example, having a credit score in the excellent range might make up for having a high DTI. A big down payment might make up for limited cash reserves or a good, but not excellent, credit score.

Apply for a Second Home Mortgage Today

Assurance Financial can help you find the financing that works for you if you’re thinking about buying a vacation property. We offer refinancing as well as conventional mortgages.

To learn more and see what you qualify for, start the online application process with us today.

Most people dream of owning a home, whether it’s a small one in the city or a rural one with a huge property. However, affording a home is difficult and saving up enough money can be challenging. Obtaining a mortgage is a big step, and you likely have many questions. One important thing you will need to know is how much of a mortgage you can afford based on your income. You can use a few different guidelines to discover what percent of your net income should go toward mortgage payments each month.

What Is Included in a Mortgage Payment?

The first thing you need to know is what exactly is included in the monthly mortgage payment. Your monthly mortgage payment is usually made up of four components:

- Principal amount

- Loan interest

- Property taxes

- Insurance

This means that your monthly payment may be more than you are expecting since it includes more than just your loan.

1. Principal

The principal is the portion of the mortgage payment that goes to the actual repayment of the amount loaned. Loans are structured so that the repayment of the principal is low at first but then increases in later years.

This means most of your money goes towards interest at the beginning of paying a mortgage. At the end of your mortgage term, the amount of principal paid will add up to the amount loaned. For example, if you purchase a $200,000 home and put $40,000 down, your total principal would be $160,000.

2. Interest

Interest is the price you must pay for borrowing money. At the beginning of your mortgage term, you will pay more towards interest than the principal.

When you’re in the process of getting your mortgage, you will be able to see how much interest you will end up paying over the course of your loan. This can end up being a lot of money, but that’s the cost of obtaining a loan. Interest rates vary but are typically between 3% and 5%, sometimes more or less, depending on different factors.

3. Taxes

You pay your property taxes to local governments to fund things like schools, firehouses, police departments and other public works. They are based on your property’s value and local tax rates.

While property taxes are calculated each year, you can usually include them in your monthly payments. The lender holds the funds in escrow until the taxes are due. This allows you to pay your taxes over time rather than paying a large sum all at once.

4. Insurance

You may have to pay two different types of insurance. If you pay less than 20% on the down payment, you may be required to purchase private mortgage insurance. Since loans with low down payments are riskier, lenders want to be protected. Private mortgage insurance protects the lender if you stop making payments. If you want to avoid an additional monthly cost on your conventional loan, you must put down 20% or more.

You will also need homeowners insurance. Most mortgage companies will not let you purchase a home without it. It protects your home and finances in the event of a natural disaster, fire or accident at the property. You should consider home insurance even if you are not required to.

Other Important Mortgage Terms

The mortgage process is often confusing, and it’s even worse if you don’t understand some of the terms. These are a few of the important mortgage terms to know:

- Amortization: The process of paying off a loan is called amortization.

- Annual Percentage Rate (APR): The APR is the cost of taking out a loan.

- Assessed value: The assessed value of a home is the value the local tax agency places on it, regardless of the selling price. Property taxes are based on the assessed value.

- Cash to close: This term refers to the amount of money you will need to bring with you to closing.

- Default: If you stop making payments on the loan or are paying less than required, you are defaulting on your mortgage. This can lower your credit score and cause the bank to foreclose on your home.

- Equity: As you pay off your principal, you are gaining equity in the home. Equity is the difference between the home’s value and the amount you owe.

- Foreclosure: If you default on your loan, the lender will take control of the property and try to get the money owed by selling the house.

- Title: The title is the record of who owns and has owned the property.

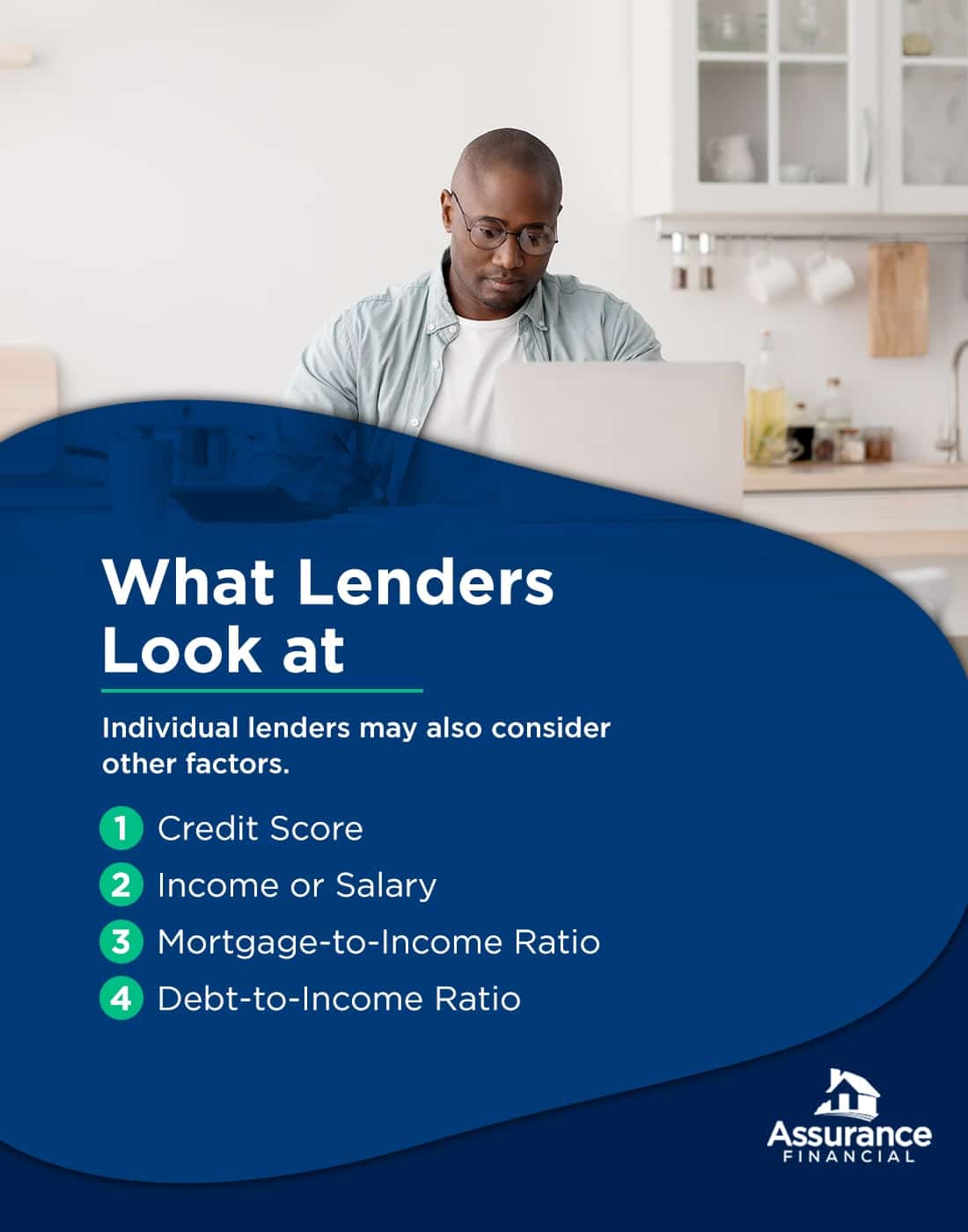

What Lenders Look at

Lenders look at more than just your income to determine what mortgage you qualify for. Your down payment, credit score and income will all be considered in relation to the amount of the loan you are seeking. Individual lenders may also consider other factors.

Credit Score

Many factors go into your credit score, such as how long you’ve had credit, the amount of credit you have access to, your repayment history and more. Lenders always check your credit score to determine if you are a responsible borrower who will pay off the loan.

A higher credit score will allow you to get better rates on your mortgage. Usually, a score of 740 or higher will help you get the best mortgage rates available. If your credit score is lower than 630, you may end up paying a much higher rate if you qualify for the loan. If your credit score is too low, you may not qualify for a conventional loan at all. Learn how to build your credit to get a mortgage loan.

Income or Salary

Lenders will need to know what your income is. They have to ensure you make enough money to pay the mortgage and all your other expenses. Of course, a higher income will likely help you qualify for a bigger mortgage.

Mortgage-to-Income Ratio

Your mortgage-to-income ratio, sometimes called the front-end ratio, will be calculated. This ratio is the percentage of your gross income that you have to put toward your mortgage payment. Most of the time, this should be below 28%. However, some lenders may allow it to be higher.

Debt-to-Income Ratio

Your debt-to-income ratio, sometimes called the back-end ratio, is also important. This ratio considers all your debt, like credit card debt, auto loans, child support, student loans and other debts in relation to your income.

How Much of Your Income Should Go Towards a Mortgage Payment?

When considering how much you can spend on a mortgage, you will need to calculate your income. Find your monthly gross income and monthly net income, as you will need both these numbers to help with these calculations.

It’s important to note that the amount of mortgage you can afford depends on more than just your income, so these are just guidelines to help. You’ll notice that the numbers will end up being different depending on which calculation you use.

28% of Gross Income

One calculation to calculate how much of your income can go towards your mortgage payment is the 28% rule. This rule says that you should not spend more than 28% of your gross income on your mortgage payment. Gross income is your income before any deductions or taxes are taken out. Find your monthly gross income by reviewing your recent paystubs. Then, multiply that number by 0.28 to find the maximum you should be spending on your mortgage payment.

For example, if you make $4,000 a month before taxes, you multiply that by 0.28 to get $1,120. The amount of $1,120 would be the max amount someone making $4,000 a month could spend on the mortgage payment. If you make $10,000 a month before taxes, you would be able to spend up to $2,800 on the mortgage payment each month. Income greatly affects the amount you can afford.

25% of Net Income

Another calculation you can use to find how much of your income you can spend on your mortgage payment is the 25% method. This method allows you to use your net income rather than your gross income. When you use your post-tax income, you use 25% instead of 28%. Find your monthly net income and multiply that number by 0.25. That number is the max you should be spending monthly on your mortgage.

For example, if you make $3,200 a month after taxes, you would multiply $3,200 by 0.25. Using these numbers, you would be able to afford a mortgage payment of $800 a month. This method can vary greatly because taxes are different depending on where you live.

35%/45% Debt Model

Another helpful calculation is the 35%/45% model. For this one, calculate your total monthly debts including, the mortgage payment. You will also need your pre-tax income and after-tax income amounts. If your other debts are fairly low, this method allows you to allocate more money to your mortgage payment. This method also provides a range your debts should fall in.

Multiply your pre-tax income by 0.35 and your after-tax income by 0.45. For example, let’s say someone makes $4,000 a month before taxes, which ends up being $3,200 after taxes. They would multiply $4,000 by 0.35, resulting in $1,400. Then, they would multiply $3,200 by 0.45, which is $1,440. This means this person’s monthly debts, including their mortgage payment, should be between $1,400 and $1,440.

Learn About Other Types of Loans

Most of these guidelines are in relation to conventional loans, but you may qualify for another type of loan. There are a few mortgage programs that allow people with low credit scores or savings to still purchase a home. VA loans and FHA loans have less strict requirements than conventional loans, so it’s worthwhile to look into them if you don’t think you will qualify for a conventional loan.

VA Loan

If you are a veteran, active-duty service member, member of the National Guard or Reserve, surviving spouse of a veteran or prisoner of war, you may qualify for a VA loan. VA loans have lower down payment requirements than conventional loans and FHA loans. You may not need to put down a down payment at all. There is also no credit score requirement, and lenders consider many factors before making a decision.

FHA Loan

To qualify for an FHA loan, you need to meet several requirements. You need a credit score of at least 500, and you will also need to put down a down payment. If you have a high credit score, you may be able to put down as little as 3.5%. If you’re approved, you will need to pay for mortgage insurance. Learn more about VA loans and FHA loans.

USDA Loan

If you are unable to get other types of loans, you may be able to get a USDA loan. There are many requirements, but they are designed for low-income borrowers. There are both direct loans and USDA guaranteed loans. Learn more about USDA loans.

[download_section]

How to Lower Your Monthly Mortgage Payment

If your income is too low or your monthly debts are too high, you may have trouble obtaining a mortgage. However, there are a few ways to lower your monthly mortgage payments:

- Find a home for a lower price: If you find the mortgage payments will be too high, you may need to spend less on your home. Use an affordability calculator to find out the approximate value of the home you can afford.