Month: September 2019

You’ve been with your significant other for a while, and now you’re planning on spending the rest of your lives together. Marriage should be a cause for celebration, not for stress, but thinking about buying a home as you begin your new life together can be intimidating. Should you buy a home before or after marriage? Does marriage status affect mortgage rates? What factors should you consider when making your choice?

Don’t get overwhelmed by the questions you have about buying a home before or after marriage. We’ll help you evaluate the pros and cons of either situation to get a better understanding of buying a house before vs. after marriage.

- Pros and Cons of Joint Tenancy

- Factors to Consider

- Does Marriage Status Affect Mortgage Rates?

- Property Rights

- Tax Considerations

- Why Wait to Buy a House Until After the Wedding?

- Take Your Time With Your Decision

Pros and Cons of Joint Tenancy

Joint tenancy allows two or more people to access an account or have an undivided share in the property. It is a practice couples and business partners alike take part in, and unmarried couples commonly seek joint tenancy. If you’re considering buying a home before marriage, you will want to evaluate the pros and cons of joint tenancy. You can also find joint tenancy with rights of survivorship (JTWROS), which allows living owners to pass on their share to someone else when the owner is still alive.

Here are some of the benefits of joint tenancy to consider.

- Share assets and debt: Share any rent or profit you see as a result of your property between you and your partner. While we hope you only experience the positive gains, it may be comforting to know that you must handle debt together. It could lead to quicker elimination of your debt if you both work together to solve it. Shared debt also protects individuals should the relationship end. One joint tenant cannot leave the other with all of the financial obligations.

- Skip probate: When an individual dies, a probate court reviews the will to determine its validity. In a joint tenancy, if one of the joint tenants dies, there is no need for this process. Assets, like a home, will go to the surviving joint tenant as long as the individuals are married. If they are not married, they may choose a JTWROS to ensure they do not need to go through probate if one of them passes away.

- Implement it easily: You can achieve joint tenancy with a clause in your property’s title. Be sure to work out the legal details even before implementing this choice.

- Financial security: No matter how you go about purchasing a home, it is a smarter financial decision than renting with your partner for an extended period. You can build your assets together and improve your credit. Since the two of you are coming together to purchase a home, you will have two salaries to help cover costs.

With joint tenancy, you must make decisions about your property with each other’s consent. Working together could be either a pro or a con depending on the stability of a relationship. Open communication about the property can help strengthen a relationship, but choices can be difficult if the relationship is on rocky ground.

Of course, with the positives of joint tenancy come the negatives. The cons of joint tenancy include:

- The court may freeze the assets due to excessive debt after one of the joint tenants passes away.

- Unless you are married, you may have to pay gift taxes as a joint tenant.

- The property cannot go to an inheritor since it goes to the other joint tenant when one passes away.

If you want to purchase a home as joint tenants, evaluate your credit scores. If one of you has a better credit score, it may be best for that individual to purchase the home with their stronger credit. Remember if you go that route, your mortgage application will only include one person’s income.

[download_section]

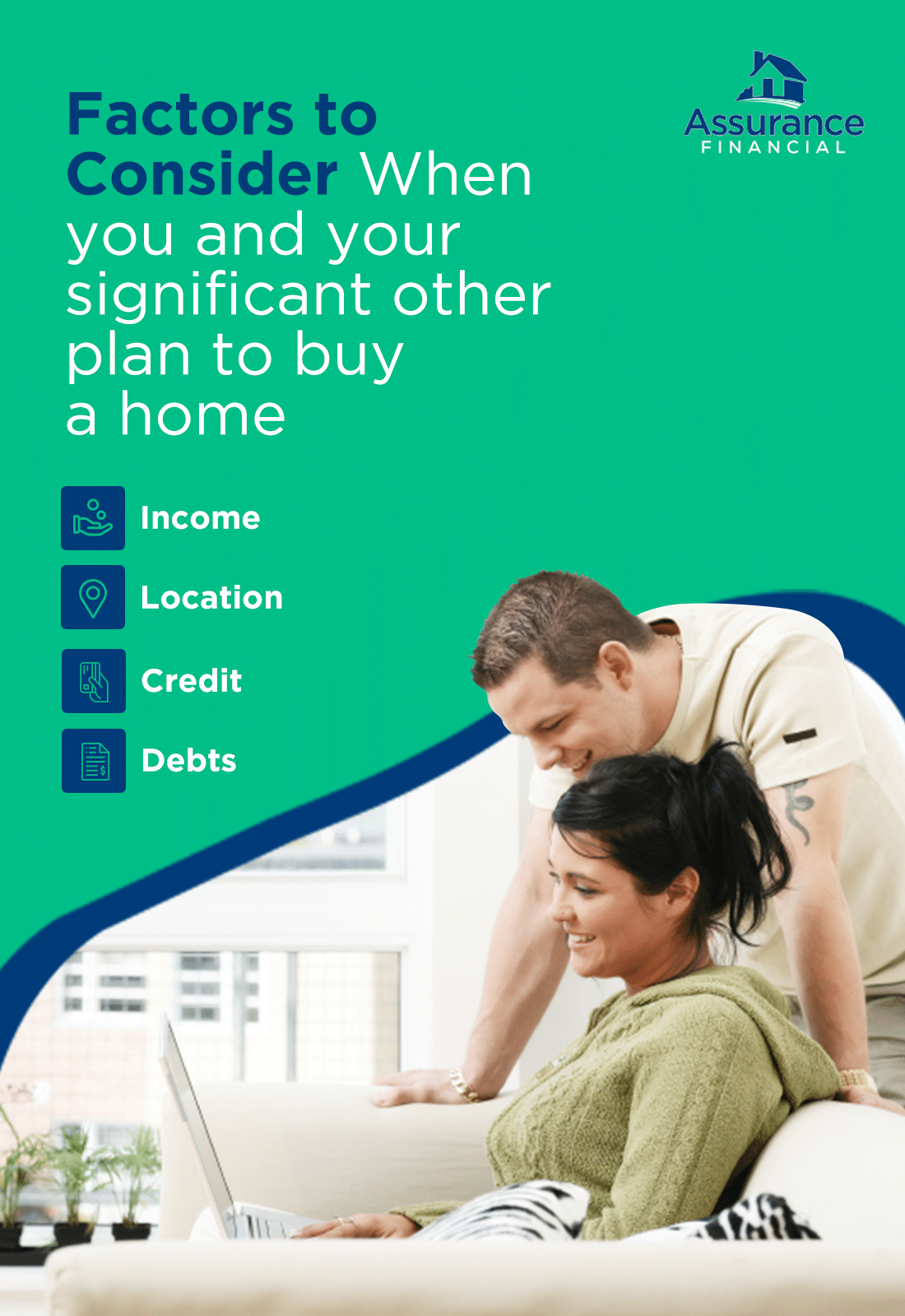

Factors to Consider

When you and your significant other plan to buy a home, evaluate certain aspects of your situation. Determining these factors will help you choose between buying a house before versus after marriage.

- Income: Take both of your salaries into account when deciding when to buy a home. You should have a stable job and some money saved up if you can before venturing into the housing market.

- Location: Whether you buy a home before or after marriage, look into the area you’ll be living in, since laws vary from state to state. Some states allow community property titles, which we will explain later on, but other property and tax laws differ between states.

- Credit: Compare yours and your partner’s credit scores to determine your course of action. If your scores are similar, you can apply together for a mortgage. If one of you has a stronger score, you may decide for that individual to apply.

- Debts: Since lenders evaluate your credit score and any liabilities you have, you and your partner should consider your debts from student loans or other sources. If one of you has less debt and good credit, you could opt for sole ownership of property. You may also choose to wait until you’ve paid off your student loan debt or other liabilities before purchasing a home.

While a tricky part of the home-buying journey is taking some “what ifs” into account, it’s best to have these conversations early. If you are purchasing a home before marriage, work out a legal agreement that outlines what you’ll do if your relationship ends or one of you passes away. Depending on how you will go about purchasing your home, you will also want to think about:

- Who will apply for the mortgage

- How you will split ownership, if applicable

- How you will protect both parties with the property title

- Whether or not you will evenly split additional costs

- What happens if the relationship ends

It may seem overwhelming to have these discussions, but getting organized and figuring out a plan can help you as you move forward with your relationship and the home-buying process.

Does Marriage Status Affect Mortgage Rates?

If you want to buy a house after marriage, you’ll want to know if marriage status affects your mortgage rates. No matter your relationship status, details like your credit score, income, debt and other financial factors influence mortgage rates. While you won’t see a direct impact from your marital status on the rates lenders offer you, related factors of your relationship status can have an effect.

- Single: Before you began your relationship, being a single-income household would have affected your mortgage rates. While lenders don’t penalize you for being single, making less than a married or dating couple may mean you get approved for less.

- In a committed relationship: If you and your partner are serious about your relationship and moving in together, consider what happens when applying for a mortgage before marriage. If you apply together, a lender will take the lower credit score into account. Applying together while not yet married can involve a bit more complex paperwork than if you applied as a married couple or an individual. You or your partner may decide to apply as an individual if your credit scores are drastically different.

- Married: As you would in a committed relationship, you and your spouse likely have a two-income household. Calculate your debt-to-income ratio, as you should no matter your relationship status, to determine how your incomes will combine.

As long as you and your partner have strong credit scores, good incomes and minimal debt, you will likely receive the best mortgage rates as a married couple. For the best outcome, marry before buying a house if your finances are in order. Take into account the factors we mentioned earlier as well as what is best for you as a couple to determine what type of ownership suits your needs.

Property Rights

As you and your partner plan to purchase a home, consider what title works best for you. Potential ownership options work with the different factors above, such as how you will divide the property. Consider these possibilities whether you’re buying a home before or after marriage.

- Sole ownership: One individual owns 100% of the property in sole ownership. When that owner dies, the property goes to someone else through transfer documents, such as a will. The decision may also go through probate. For a married couple or a couple seriously considering marriage, sole ownership may not be the best choice. Unless one of you has a significantly better credit score, you may think about one of the other title options.

- Joint tenancy: Depending on where you live, joint tenancy usually allows the surviving joint owner in the event of another’s passing ownership of the property. Married couples can find tax benefits with qualified joint tenancy, but anyone can enter into this title.

- Tenancy in common: Unlike joint tenancy, which involves an undivided share of the property, tenancy in common allows for different percentages for each owner. The ownership percentage helps determine how much in mortgage interest and property taxes an individual pays. Upon death, an individual’s will can pass the property onto someone other than their spouse, also unlike joint tenancy. With tenancy in common, you can sell your share of assets without the other tenancy in common’s consent. If you seek joint ownership of the property before marriage, it may default to tenancy in common unless you opt for a different ownership method.

- Community property: Available in certain states, community property involves an equal share between spouses. Unlike joint tenancy, individuals can leave their portions of their property to heirs after they pass away. Community property begins at marriage and ends should the couple decide to separate. Any property an individual owned before marriage is called separate property. The individual can maintain control over the separate property or share it with a spouse once married.

With these options, you and your partner can find the title option that suits your needs. Before choosing one, you should also take into account how buying a house before or after marriage can affect your taxes.

Tax Considerations

Evaluate how your marriage affects your taxes to help you decide if you should marry before buying a house. Typically, married individuals have more tax benefits than couples.

As an unmarried couple, you cannot file joint taxes. You will have to organize how you will file separately. Only one homeowner, for example, can claim the deduction on mortgage interest, so two individuals filing separately cannot both claim that deduction. If the relationship ends before marriage, the individuals will have to sort out who covers taxesand other costs.

While tax and property law vary between states, there are more factors to consider as an unmarried couple than a married one. You may find it’s easier to get married before purchasing a home. That way, you can focus on learning about these laws specifically for married couples.

Whichever title you choose for your home, be sure to watch for any liability to pay the taxes due on your property. Even if the responsibility belongs to the other owner, you may be legally responsible if taxes go unpaid. Learn the law where you live and choose your best course of action, which may be purchasing a home after marriage.

Why Wait to Buy a House Until After the Wedding?

While you may have planned on buying a house before marriage, you may want to consider getting married and then buying a home. Marry before buying a house for benefits such as:

- Filing joint taxes

- Ease of applying for a mortgage

- Saving on the stress of house hunting and planning your marriage

- Flexibility with mortgage applications and title options

Though buying a home after marriage makes more financial sense, it is still something you should have a conversation about with your spouse-to-be. You want to be on the same page in terms of buying a home and your goals before you get married to avoid any surprises later.

Take Your Time With Your Decision

Like marriage, buying a house is a big decision. With so many factors to consider, you won’t want to rush into a choice. Evaluate aspects of you and your partner’s life, such as the following.

- Your income and finances: Do you and your spouse have stable jobs? Have you been saving for some time? Take the time to go over your finances and sort out your budget before you begin house hunting. From there, you can make informed decisions about how you will split the property or who will apply for the mortgage if one of you has a better credit score.

- Your long-term goals: Think about your jobs and where you see yourself in the future. Do you plan on moving? Are you going to have children?

- Your relationship: It’s difficult to talk about with your partner, but ensuring your relationship will last a long time creates a secure foundation for buying a home. Work out what your options are should the relationship end. Know that the conversation doesn’t mean it’s going to happen. It means you and your partner have prepared for the future.

- The distant future: Preparing for the future also, unfortunately, means you must think about what happens when one individual in the relationship passes away. Consider the title you obtained when purchasing your home as that influences who the share of the property goes to or if you need to go through probate.

Figuring out the course of your relationship and future will help you and your partner forge a plan. Move forward confidently with your marriage and buying a home after you’ve evaluated your finances and goals.

Purchase a Home With Help From Assurance Financial

Buying a home can be as exciting of a journey as marriage if you know how to approach it correctly. Communicate with your significant other about what both of you want now and what could be best for your shared future. Don’t delay the tough conversations, either. It may be hard to think about what you would do if one of you passes away or if your marriage ends, but preparing for those unfortunate possibilities makes your relationship stronger.

No matter when you decide to purchase a home, contact us at Assurance Financial. Apply online or meet with one of our licensed experts to plan a bright future with your spouse.

Popular Loan Types

- First Time Home Buyer Loans

- FHA Loans

- Conventional Loans

- Construction Loans

- VA Loans

- Jumbo Loans

- Refinancing

Additional Resources You May Also Like

After the hassle of buying a home, does refinancing make sense? In some situations, you may benefit from refinancing your home, but you need to know more about these particular instances as well as when refinancing may not benefit you. Do not lightly make your decision to refinance your home. Careful consideration of your finances and your current situation will help you choose when to refinance your home.

- Why Would You Want to Refinance a Mortgage Right After Purchase?

- How Often Can You Refinance a Mortgage?

- What to Know Before Refinancing

- How to Know When Refinancing a Mortgage Is Right for You

Why Would You Want to Refinance a Mortgage Right After Purchase?

When someone asks us, “Can I refinance right after buying a home?” the answer is yes, but with reservations. Many lenders will require at least a year of payments before refinancing your home. Some refuse to refinance in any situation within 120 to 180 days of issuing the loan. The more money you put into your home, the easier it will be to refinance, regardless of when you do it. Ideally, you should pay at least 20% of the home’s value before you seek to refinance to make qualifying a more straightforward process.

Only a couple of situations justify refinancing soon after you buy your home. These typically deal with major changes in your life or finances. Even if you experience a change that might warrant a rapid refinance of your mortgage, always talk to your lender, first to get personalized advice. Here are some reasons you might need to refinance soon after buying:

1. Interest Rates Changed Dramatically

The economy can change in the blink of an eye, and if mortgage interest rates in your area have plummeted since you bought your home, you may consider refinancing. Unless interest rates drop more than 0.5%, refinancing for lower payments does not make sense.

A study done in December 2010 showed that households eligible for refinancing could save $160 monthly on their mortgage payments thanks to lower interest rates. Unfortunately, at the time, 20% of families that could have refinanced to take advantages of the savings did not, leaving behind an average of $11,500 on their homes they could have saved.

If the interest rates decline significantly, you will save more money the sooner you refinance. However, don’t forget about closing costs. The amount you save should cover the closing costs for refinancing, which could be 3% to 6% of your home’s value. If you cannot justify the closing costs in monthly savings from the lower interest rate, you may not need to refinance.

2. Life Changed Your Ability to Pay Higher Rates

Occasionally, unexpected life events will sometimes get in the way of your ability to pay your mortgage. If you initially took out a 15-year loan, you can stretch out the payments by refinancing to a 30-year loan. You will still need to pay the closing costs, but the option of changing to a longer-term loan could help save money if an unexpected circumstance leaves you unable to afford your higher mortgage payments. The downside to this option is the increased amount of interest you will pay over time, but you may need the lower rates more than the lower total cost.

3. Your Credit Rating Rose

The interest rates you get for your mortgage depend mainly on your credit score. While your credit score may not usually change quickly, it could surge after clearing disputed charges or paying off large debts. Also, the more time that passes after a bankruptcy, the less of an effect the event has on your credit. Talk to your lender if your credit score has risen significantly since you took out your home loan to see if you can qualify for lower rates through refinancing with your new, better credit score.

4. You Divorced

When you signed your home loan, if you did so with your spouse, refinancing is the only way to get that person off your mortgage if you divorce. When refinancing, your individual income may change rates unless you have a cosigner on the loan whose assets can ensure you get the same or lower interest than before.

When refinancing, you may be able to request a loan to include your spouse’s half of the equity to pay her for half the house. For example, if you have a $200,000 home loan, and have paid $60,000 of it, you will owe your spouse $30,000 for his portion of the home. You should then refinance for $170,000 to cover the remaining $140,000 in the house plus your spouse’s $30,000.

Since this matter also has legal implications, talk to your lawyer about property and divorce laws in your area if you have any questions about your specific situation.

5. You Want to Get Rid of PMI

Personal mortgage insurance, PMI, ensures your lender that you will make mortgage payments. Usually, you will need this if you get a loan with a down payment of less than 20% of the home’s value. However, did you know that when you make enough payments to have 20% of your home’s value in equity, you can drop PMI? In some cases, you can call the lender, but just a phone call may not be enough. If rates have also changed, you may want to refinance to get rid of the PMI monthly payments and take advantage of better rates. Doing so can save you money each month.

How Often Can You Refinance a Mortgage?

Technically, American law doesn’t officially limit the number of times you can refinance your home. Since you have no legal restrictions, you could seek new loan terms as many times as you want. Certain factors will play into when and how often you should refinance, including when you can break even and how many properties you have.

Some people refinance more than once. One couple did it twice on the same property in the same year, but this may not make financial sense for you. If you need to know how soon you can refinance after refinancing, look at the numbers. The savings must make up for the payments and any penalties. When the figures show you can recoup your losses quickly, you can refinance as often as you like.

Decide your break-even time. This time will be when you recover the costs you paid from your refinance in savings you’ve made. Compare your current loan payments and subtract the amount after refinancing. Divide the closing costs and fees by this number to find out how many years it will take for your investment to pay for itself.

For instance, if you have a $200,000 mortgage and closing costs to refinance cost 4% of the total, you will pay $8000 in closing fees. If you reduce your payment by 1%, you will save $2000 each year. To recover the closing amount, you will need to make payments on your newly refinanced loan for four years.

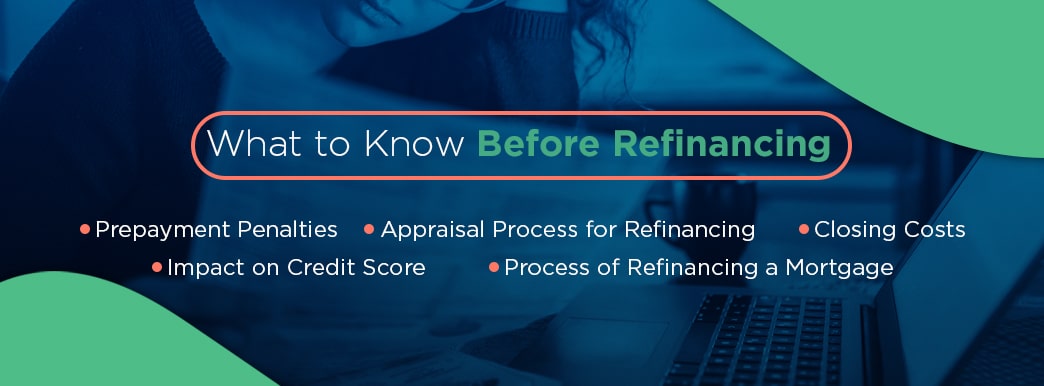

What to Know Before Refinancing

Before you refinance, you need to understand about the possible drawbacks of the process as well as the steps of the ordeal itself. Pay attention to these factors:

1. Prepayment Penalties

Paying off your mortgage early by refinancing or selling your home may come with prepayment penalties. Some mortgages come with prepayment penalties. Talk to your lender about the policy on early payment for your current home loan before refinancing. Your lender should inform you about prepayment penalties when you close on your mortgage.

Mortgages may have one of two types of prepayment penalties, also known as prepays. Both types penalize you if you refinance before paying off the loan. Hard prepays penalize buyers for both selling and refinancing, whereas soft prepayment penalties only cost borrowers a fee after selling the home.

While these penalties only happen during the first one to three years of the loan, they can add up. For instance, some lenders may charge 80% over six months of interest-only payments. You will most likely want to read the information about prepays in your closing information carefully and discuss any questions you have with your lender.

2. Appraisal Process for Refinancing

Your home will need reappraising as a part of the refinancing process. The appraisal process protects the lender by ensuring the value of the house is close to the mortgage value. Since so much of your mortgage payment comes from the home’s value, having an accurate appraisal will help you, too. You won’t overpay for your home.

You must schedule the appraisal and pay for it yourself. These inspections can cost between $300 and $400. If you have a large property or multiple units, the cost and time to conduct the appraisal will rise. Standard times for the assessment can take between three and ten business days.

3. Closing Costs

Just as you had to pay closing costs with your original home loan, you will need to cover these for your refinancing. Essentially, refinancing is transferring your old mortgage to a new rate. It still requires the same steps required for you to take out a loan, including paying 2% to 5% of the home’s value in fees.

4. Impact on Credit Score

Each time you refinance, the lender will conduct a hard inquiry of your credit. Too many of these types of examinations can negatively impact your credit score, even if you make regular on-time payments. Refinancing once or twice is fine, but the shorter the time between these loans or your original borrowing and refinancing, the more significant the impact you will see on your credit score.

5. Process of Refinancing a Mortgage

The process of refinancing has multiple steps. You will need to prepare yourself for the process, so you don’t feel surprised or unprepared by anything. Researching the process and your options will make you better prepared for choosing the right lender and finding the best interest rates.

First, get an idea of your home’s worth and determine how much equity you have. Generally, lenders won’t refinance if you have less than 5% equity in your home. Ideally, you want 20% equity or more in your home for the best chances at qualifying for a refinance.

A lot of the refinancing process requires research. Not all lenders offer the same interest rates, and your credit score and other personal factors will affect how much you pay. You need to compare rates from several lenders and find out what fees they charge. Check with the mortgage companies to see what paperwork they need hard copies of. Many can connect electronically to various financial institutes, so you don’t require printouts of financial documents.

Once you’ve done your research, apply for a loan to get an estimate for refinancing. You should get an estimate within three days. If you approve of the terms, the loan process continues with the lender carefully reviewing your application documents.

At this stage, you need to get an appraisal. In some cases, your lender may set up this inspection or ask you to do it. After appraising the home, the reviewer will send a report about the home’s value to both you and the lender.

The lender will have an underwriter comb over the paperwork and your home’s appraisal. You may need to answer questions about your refinancing application. Address these quickly to keep the process moving forward.

Lock in the rate at any time, but you should do it before closing. At closing, you will sign the needed documents and make any fee payments. Once closed, your new loan takes over for covering your home’s mortgage.

How to Know When Refinancing a Mortgage Is Right for You

Several situations make refinancing a good option. Don’t just go through the process if mortgage rates drop a little. Wait for a significant drop or any of these other signs that you will save a considerable amount of money. Refinancing is a good idea if you:

- Move from an adjustable rate mortgage to a fix-rate loan

- Change from a 30 or 40-year term to a shorter 15-year term

- See interest rates drop at least 0.5%

- Have an interest-only loan that will decrease

These situations could make refinancing a valuable way to save money. While you don’t want to enter the process needlessly, you also don’t want to leave money on the table by failing to refinance at the proper time.

Does Refinancing Make Sense for You?

Having a close relationship with your lender is critical to working through the refinancing process. At Assurance Financial, we have people and technology to work for you and with you. If you think it’s the right choice for you at this stage in your life, contact us at Assurance Financial about refinancing your home. Through a refinance, you may be able to lower your payments or get cash from your home’s equity.

To see if you qualify, meet with one of our loan advisors in person. You can find out more about our rates and whether you qualify for refinancing. No matter how you work with us, we’ll help you find your ideal home loan options. We’re the people you can trust.

Key Takeaways

- Critical first steps include checking and raising credit scores, establishing realistic price ranges, identifying priorities (must-haves vs. nice-to-haves), and comparing mortgage lenders before saving for a down payment.

- The systematic process continues with getting pre-approved, finding real estate agents, attending open houses, making offers, negotiating, inspecting, appraising, and finally closing.

- Credit score management and budgeting are critical first steps as they determine loan eligibility and interest rates.

When you’re shopping for a phone or a new pair of jeans, the process is relatively straightforward. You probably check out your options online, maybe try a few out in the store, pick the best fit and get on your way.

It’s not that simple with homebuying, though. Buying a home is an enormous investment. The process takes time, and especially for first-time buyers, it can be overwhelming.

Having a checklist to move through gives first-time homebuyers a sense of control and purpose. Being able to map out the process makes everything a little less daunting.

- It Helps Buyers Make Sense of an Unfamiliar Process

- It Helps Buyers Understand the Homebuying Timeline

- It Provides Valuable Information

- Check Your Credit Score

- Raise Your Credit Score

- Establish a Realistic Price Range

- Establish Your Priorities

- Check out Different Mortgage Lenders

- Scrape Together a Down Payment

- Get Pre-Approved for a Mortgage

- Shop Around for the Right Real Estate Agent

- Attend Open Houses

- Put in an Offer

- Negotiate

- Go Through Inspection

- Go Through Appraisal

- Renegotiate

- Close on the Home

Why It Helps to Have a Checklist Before Buying a Home

Buying a home can be a long, demanding process. According to the National Association of Realtors, the median buyer looks for 10 weeks before finding a place, and sees an average of 10 homes during that time.

First-time homebuyers are a large cohort, making up over a third of all buyers. But sometimes first-time buyers don’t have all the information they need to take the proper steps or make the right decisions at every turn.

A first-time buyer checklist, then, is useful for a few reasons.

1. It Helps Buyers Make Sense of an Unfamiliar Process

If you’re a first-time homebuyer, many of the terms and procedures involved in home buying will be new to you. You’ll have to learn what closing costs and fixed-rate mortgages are. You’ll face moments of uncertainty about all the different people and negotiations involved in the process. You’ll need to know what steps to take when, and you’ll need to be aware of what difficulties could arise so you can prepare to head off problems before they throw a wrench into your search.

Having a checklist provides you with a practical sense of how the homebuying process works. That way, you’ll understand exactly what needs to happen before you have the keys to your new home securely in your pocket.

2. It Helps Buyers Understand the Homebuying Timeline

“When should we apply for a mortgage loan?” “When should we get an appraisal?” “Should we have talked to a real estate agent already?” Questions like these can muddy the waters of the homebuying timeline, leading to doubt and frustration.

The virtue of a first-home checklist is that it provides visual orientation. That way, buyers can address these questions at a glance, and quickly figure out what needs to happen when. This clarity helps buyers focus their energy where it needs to be, instead of worrying about escrow when they haven’t even figured out a budget yet.

3. It Provides Valuable Information

Being armed with knowledge and information gives first-time homebuyers a leg up on the competition — and the housing market can be competitive for sure. You’ll need to keep many essential items in order, or a sudden setback could derail the process just when you think you’re all set.

How to qualify for a home loan as a first-time buyer is one of the first, most critical questions. Having a first homebuyer’s checklist as part of the mortgage process provides valuable tips and tricks to make sure everything goes smoothly and you end up with favorable loan rates.

First-Time Homebuyer Checklist

The checklist below will help with what first-time homebuyers need to know before buying a home.

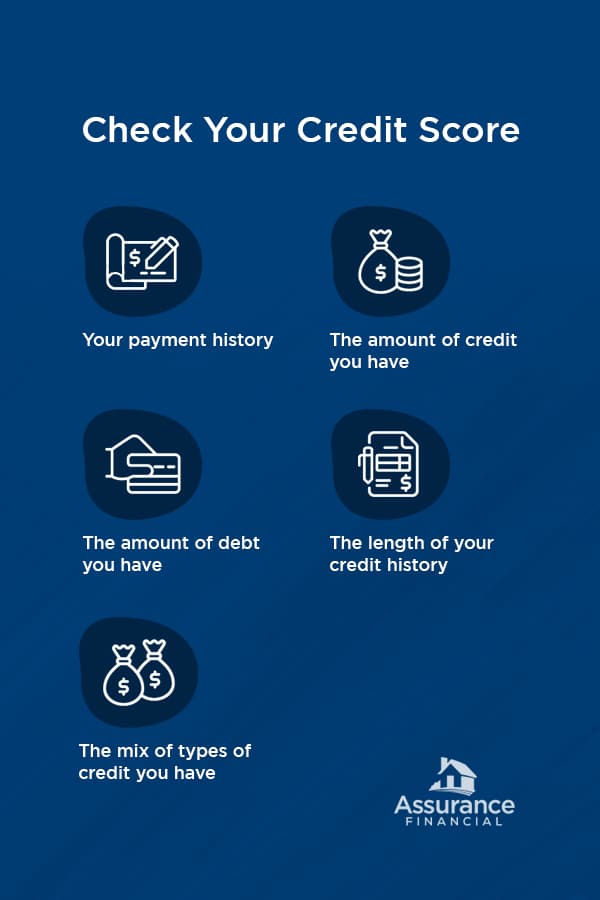

1. Check Your Credit Score

Your credit score is crucial, because mortgage lenders look at it to determine your creditworthiness and loan eligibility. Your credit score determines the rates you’ll receive. A better credit score leads to lower interest rates, whereas a lower score leads to higher rates.

Credit bureaus typically base your credit score on a combination of factors such as:

- Your payment history

- The amount of credit you have

- The amount of debt you have

- The length of your credit history

- The mix of types of credit you have

For example, a person with a blend of student loans and credit cards likely has a better credit score than a person who owes the same amount on credit card debt alone.

It takes time to raise your credit score, so it’s wise to assess it early. You can check your credit score for free online. Some credit card companies offer a free credit score once a year, or you can check for free at sites like CreditKarma.com or AnnualCreditReport.com.

2. Raise Your Credit Score

One critical part of your credit score is the amount of credit available on the amount of credit you have. If you can do so, pay off some debts. If you have any outstanding bills, prioritize paying them before they get too far past due. Creditors don’t typically report missed payments until 30 days past the due date, but after that, unpaid bills will lower your score. If you see any errors in your credit report — it does happen — contact the credit bureau with proof of the mistake, so they can issue a correction. Even if you have excellent credit, a small boost may help you qualify for better loan rates.

Raising your credit score can help you secure the lowest interest rates on your mortgage loan. Many traditional lenders require a score 660 or higher to qualify for a mortgage loan, and you’ll likely need a score of 740 or higher to get the best interest rates. If you have poor credit of 580 or above, though, you may be able to get a mortgage loan through government programs like the Federal Housing Administration (FHA), which will consider lower scores if you’re willing to put down a larger down payment. Active-duty and retired military personnel are eligible for Department of Veterans Affairs (VA) loans, which also tend to be lenient with poor credit.

3. Establish a Realistic Price Range

While you’re waiting for your credit score to go up a few points, think realistically about what your budget has room for. What down payment can you afford, and what mortgage payment can you afford? You can use online calculators to figure out monthly mortgage payments and play around with variables like the amount of the down payment and fluctuating interest rates.

Don’t forget the mortgage won’t be your only payment — homeowner insurance and property taxes can add up to to a hefty chunk.

4. Establish Your Priorities

Maybe having three bedrooms and two bathrooms is a hard-and-fast requirement. Perhaps you’re firm on having a manageable commute to work and not buying a house in the floodplain. Maybe you’d love a yard with a river view and a big patio to grill on, or an interior with exposed brick and crown moldings, but you can live without those things. Or, perhaps your 5-year-old insists on an in-ground swimming pool and unicorn paddock, but would be OK as long as there is treehouse potential.

No matter what your priorities are, make sure you’ve thought seriously about them before you start looking. If you and your spouse or partner are looking together, be sure to put together a wishlist that reflects the priorities you both have. You’ll both be substantially invested in your new home, financially and otherwise, so you both need to be happy.

Be prepared for some of your priorities to shift during the house-hunting process, though. If you find a house that checks all the boxes, but you can’t see your kids growing up there, it’s OK to listen to your gut. If you always thought the north side of town was too far away from work, but discover the perfect house right on the bike trail, don’t write it off because it doesn’t fit with the list you originally made.

5. Check out Different Mortgage Lenders

Call and ask about your options with different banks, credit unions and mortgage brokers, or speak with the VA if that option applies to you. See if you qualify for a mortgage and what rates your credit score makes you eligible for. Treat your potential mortgage the same way you’ll treat your potential home: Don’t choose the first one you see. Look at several to figure out their advantages and drawbacks.

It’s vital to compare rates across different lenders. For example, you may find two lenders that both offer 30-year fixed-rate mortgages. If one offers a 4% interest rate and another offers a 4.4% interest rate, that extra 0.4% adds up to a lot more extra money than you might think over the 30 years of the mortgage. Especially if you have a so-so credit history, different lenders may offer you markedly different rates, so shopping around can lead to significant savings.

With a $300,000 mortgage at a 4% interest rate, for example, you might have a monthly payment of $1,289 a month and $164,040 in interest paid over 30 years. For that same mortgage at a 4.4% interest rate, you might pay $1,352 a month and $186,720 interest over 30 years. That’s a difference of over $22,000 over the span of the loan, from a variance of only 0.4% in interest rates.

It’s also essential to figure out the pros and cons of different lenders. If they sincerely want your business, some lenders may offer an expedited process or be amenable to paying your closing costs. But lenders also charge different fees: loan application fees, rate lock fees and many more.

6. Scrape Together a Down Payment

In recent studies, 13% of all buyers reported saving for the down payment proved their most significant hurdle to homeownership. To get the best rates, you’ll likely have to put down 20% of the list price, though it is possible to buy a home with a smaller downpayment. For a $300,000 home, that 20% comes to $60,000 — not a trifling amount. With federally-backed VA and FHA loans, people typically put down much less. The average down payment percentage also varies by region, soaring higher in areas where housing costs more.

Make sure you’ve saved up, and think about how you can save more if you’re serious about reaching your goal. To this end, you’ll want to keep your financial life stable. If you’re planning to buy a home, it’s probably not the right time to quit your job, go back to school, buy a brand-new car or open new lines of credit — unless doing so will help your credit score. Find ways to save instead of spending. If you can’t comfortably cut back, that may be a sign your homebuying budget is unrealistic.

7. Get Pre-Approved for a Mortgage

Pre-approval means a lender looks over your income information, assets and credit score. The lender tells you what loans you qualify for and what interest rates you can expect to receive, and provisionally agrees to lend you a specific sum.

Especially in competitive markets, pre-approval is almost a necessity. A mortgage pre-approval statement provides sellers with specific details of the loan you will get, so the seller can feel confident your offer won’t fall through.

8. Shop Around for the Right Real Estate Agent

Studies show that in all demographics except for buyers aged 71 and up, the majority of people search online listings first before contacting a real estate agent. Online searches are a beneficial first step. At some point, though, you will probably want to reach out to a professional.

Your agent will be your negotiator, the person who helps you navigate offers and counteroffers and deal with the closing process. You need someone savvy, so do your homework by reading online reviews or speaking to past customers if you can. When you’re choosing a real estate agent, a friendly, laid-back person you get along with is a plus. However, don’t discount someone just because that person seems blunt or aggressive. A bulldog of an agent can help you at negotiation time.

Studies show 88% of buyers purchase a home through an agent, and a whopping 92% of buyers 36 and younger do so. Not seeking out a real estate agent can put first-time buyers, especially younger buyers, at a significant disadvantage.

9. Attend Open Houses

Sometimes a house looks great in photos, but once you get there, you realize strategic uplighting worked magic on rooms that are gloomy in real life, or that despite the grassy expanse of lawn you saw, the neighbors are only six feet away. Sometimes the opposite is true, and a home that doesn’t photograph well shows up stately and charming in real life. Going to open houses lets you see real homes in all their quirks and glory. It’s a good idea to take photos yourself, so you can keep details straight.

Keep in mind you’re not just seeing the homes — you’re scoping out the locations, too. If you love the gingerbread trim, but the neighborhood seems unsafe, or you wanted to be near the university, but the noise from the stadium is overwhelming, chances are those homes may not be the right fit.

10. Put in an Offer

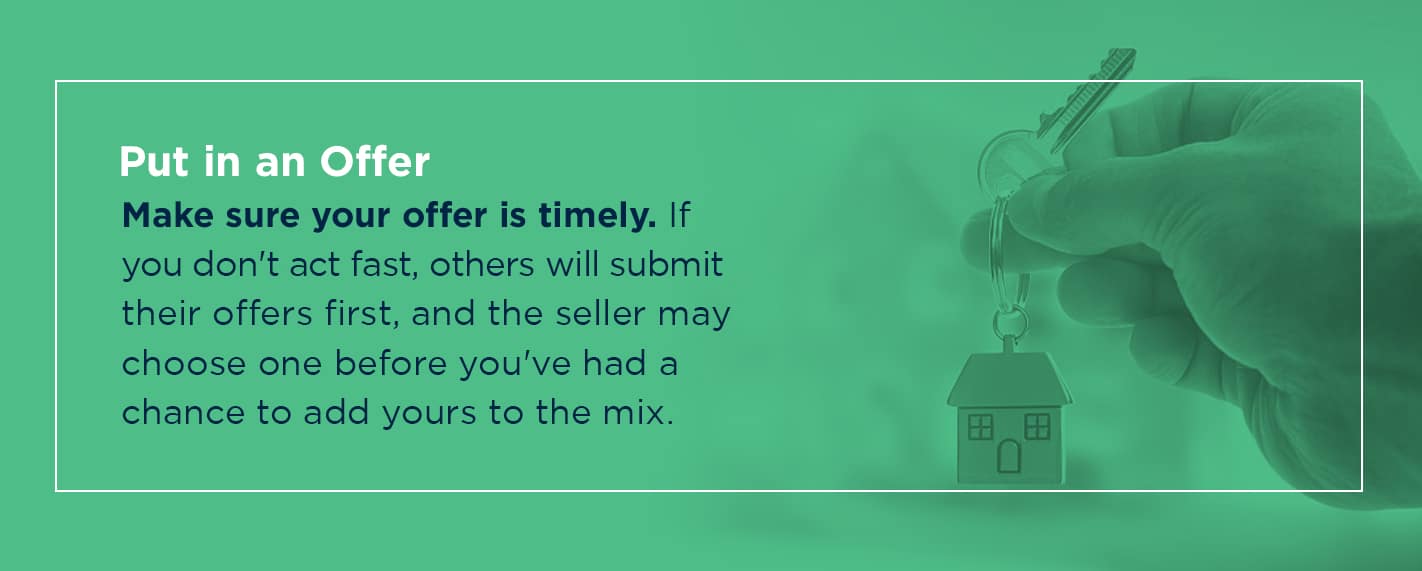

Browsing listings and seeing open houses is fun and exciting, but at some point, you’ll have to pull the trigger. If you’ve found a home you love and are serious about, your real estate agent can help you get your offer together. Preparing an offer typically includes setting your offer price, receiving disclosures, figuring out contingency clauses and setting a time frame for closing.

Make sure your offer is timely. If you don’t act fast, others will submit their offers first, and the seller may choose one before you’ve had a chance to add yours to the mix. It’s also essential to make sure your offer is realistic and well-calculated. If your offer is too low, you won’t stand a chance against the competition. If it’s too high, even if you love the house, you may feel you made a bad deal.

11. Negotiate

If the sellers choose your offer, that’s great news. You’re not quite done, however. The sellers may make a counteroffer, perhaps asking for a thousand dollars more or dropping the price by a grand or two if you agree to pay their closing costs on top of yours.

At this point, your real estate agent can be an excellent source of insight about how to proceed. If you love the house, you may accept what the sellers ask for, or if you can’t live with the new terms, you may want to counter for yourself.

12. Go Through Inspection

This step of the first home checklist process often leads to a few days of worrying. What if the inspector finds something severely wrong with the house, and you have to give it up? There’s nothing to do at this point but wait and see.

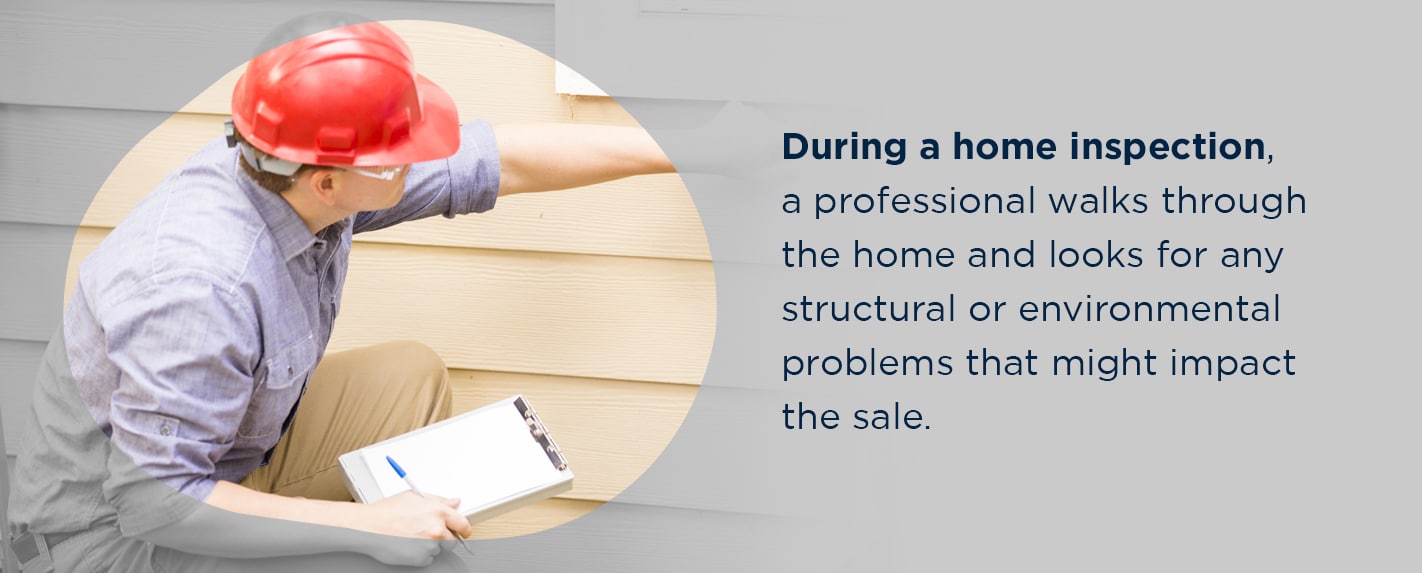

During a home inspection, a professional walks through the home and looks for any structural or environmental problems that might impact the sale. These can range from minor issues, like clogged gutters or a damp basement, to more serious problems, like a cracked foundation, faulty wiring or the presence of black mold, that would make the house too hazardous to be a wise investment.

13. Go Through Appraisal

Most mortgage lenders require an appraisal before they will officially approve a mortgage. During this process, a professional appraiser assesses the actual value of the home. They will consider factors such as the home’s condition, its features and amenities and its square footage, as well as its comps, or the sale prices of homes of comparable value.

If the sellers have listed a home at a price too far above its actual worth, the mortgage lender will issue a mortgage only for the appraised amount, leaving you to cover the rest or move on to a home whose listed price and appraised value align.

14. Renegotiate

After the inspection and appraisal, if you’re still on board with the sale, you can ask the sellers to perform any necessary repairs, or you can use the discovered problems as a bargaining chip to negotiate a lower price if you’re prepared to tackle some home-improvement projects after closing.

Your agent can advise you about what to ask for to bring the house up to a reasonable standard and what concessions to make in the interest of a quick closing process.

15. Close on the Home

When you’ve settled all the major issues and you and the sellers have agreed on final costs, the last step is to close. Once you’re there, you’ve made it! At closing, you will sign final paperwork to seal the deal. You’ll receive the deed to the property — and, after a long and sometimes grueling process, you’ll finally own your first home.

Get Started Buying Your First Home With Assurance Financial

Now that you have your first-time homeowner checklist, you’re ready to get started.

At Assurance Financial, we understand first-time homebuying can be a daunting and complicated process. Our trusted advisers will be with you every step of the way. We’ll answer your questions and make sure you get the right loan for your situation, so you can own the home of your dreams without financial worry.

As full-service residential mortgage bankers, we have the knowledge, insight and resources to help you obtain the loan that works for you. We treat all our customers with compassion and respect because we want to help them get into the homes of their dreams. Search for a loan officer using our online tool, or contact us today.

Popular Loan Types

- First Time Home Buyer Loans

- FHA Loans

- Conventional Loans

- Construction Loans

- VA Loans

- Jumbo Loans

- Refinancing