Month: July 2021

To get certain types of loans, such as a mortgage, you need to have a good or excellent credit score and a strong credit report to qualify for the best terms possible. But it can be difficult to build a good credit history or establish your credit score without having any loans.

If you’re wondering how you can build your credit score, the good news is that there are several options available to help you establish credit and get on the path toward homeownership. Learn more about what mortgage lenders are looking for in a credit report and what you can do to make your credit score and history look attractive.

Table of Contents

- Credit 101

- How to Build Credit to Get a House

- How to Practice Good Credit Habits

- Benefits of Building Credit

- Boost Your Credit With Assurance Financial

Credit 101

Credit lets you borrow money to purchase items you can’t afford to pay for in full upfront. For example, it allows people to pay for cars, education and houses. When a lender extends credit to you, they expect you to pay back what you borrow, plus interest, usually on a set schedule. Lenders who issue credit can’t simply trust their gut when deciding whether or not to lend money to a person. They usually check that person’s credit report to see whether they have a history of paying on time or missed payments.

The longer a person’s credit history, the more information a lender has to go on. For example, if someone opened their first credit card 20 years ago, the lender can see whether they have made consistent and timely payments over the years. The more varied someone’s credit history is, the more the lender has to judge whether or not an individual would be able to handle repaying another loan. The amount a person has borrowed also plays a part in influencing a lender’s decision about whether or not to give that person another loan.

While it can be relatively easy to get approval for some types of loans, others have more stringent lending requirements and might require a person to have a stronger credit history. If buying a house is in your future plans, it can be worthwhile to focus on building credit — making you a more attractive borrower to lenders and helping you get the best terms and conditions possible on your home loan.

How to Build Credit to Get a House

If you’re starting from scratch and don’t have a credit history at all, you have several options for building up your credit and making yourself a more attractive borrower to lenders.

1. Consider a Secured Loan

Several types of loans are available for people who want to improve or establish their credit. Both types require you to make a deposit that acts as collateral, but how the loans go about doing that is slightly different.

For example, you first need to put down a deposit if you open a secured credit card. The deposit acts as the collateral on the card, reducing the risk to the lender if you can’t make payments on the card. Usually, the amount of your deposit serves as the card’s limit. If you open a card with a security deposit of $500, you can charge up to $500 on the card. Once you pay off the full balance, you can charge up to $500 once again.

One thing to understand about a secured credit card is that your deposit won’t count toward your payments on the card. If you use the card to purchase things, you need to pay it by the due date to avoid late fees and other penalties.

[download_section]

Secured credit cards tend to have higher interest rates than other types of credit cards, making it worth your while to pay your balance in full before the due date rather than pay only the minimums. In addition, many cards will convert to an unsecured version after a year or so, meaning you get the amount of your deposit back. Depending on the terms of the credit card, you might need to ask the card company to convert the card to an unsecured one, or the conversion might be automatic.

Another option for people with limited credit histories is a credit-builder loan. Credit-builder loans work differently from other loan types. When a person applies for a credit-builder loan, a lender deposits the amount of the loan, such as $1,000, into an account. The borrower then makes payments to the lender, such as $75 per month, plus interest. When the borrower makes payments, the lender transfers that amount of the loan into the borrower’s account. The lender also reports the borrower’s payments to the three credit reporting bureaus, helping people build their credit to purchase a home.

A study from the Consumer Financial Protection Bureau found that nearly one-quarter of people who didn’t previously have credit were able to establish a credit history after they got a credit-builder loan. The average credit score increased by 60 points after individuals opened a credit-builder loan.

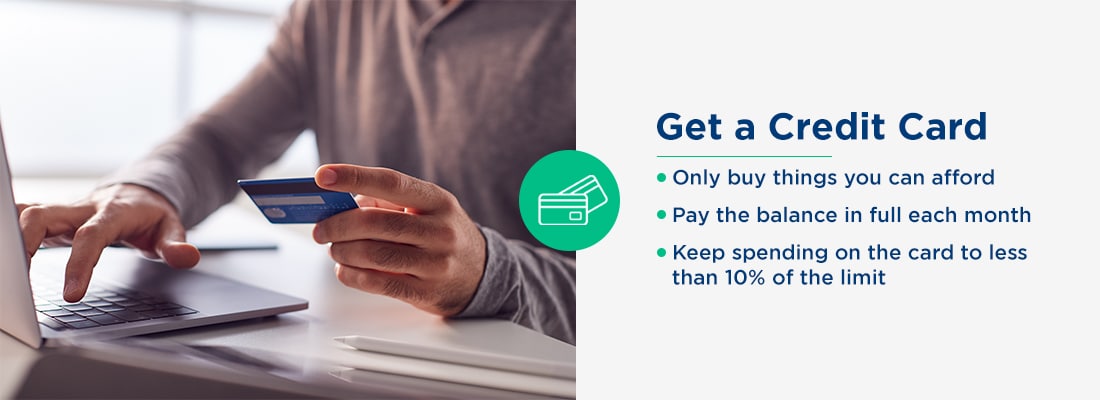

2. Get a Credit Card

You might not have to apply for a secured credit card to start building credit. Several “starter” cards are available that let you build your credit history without putting down a deposit. Often, starter cards are targeted at students, meaning you might have to be in college to qualify for the card. There are some cards that are designed for adults who aren’t in school, though.

When you get your first credit card, keep in mind that it might have a high interest rate and a low credit limit. A credit card company might be willing to issue you a card, but it is also likely to take steps to minimize its risks. A higher-than-average interest rate is one way to do so, as is limiting the amount you can borrow. There are a few things you can do to make the most of your new credit card:

- Only buy things you can afford: Use your card for purchases you would make anyway, such as groceries. That way, you won’t run the risk of charging more than you can afford to pay back on the card.

- Pay the balance in full each month: Pay the full amount of the balance by the due date to avoid having to pay interest on the things you’ve charged. Paying in full by the due date also helps you avoid late fees and keeps your payment history positive.

- Keep spending on the card to less than 10% of the limit:How much you’ve borrowed compared to your credit limit affects your credit score and history. To boost your score, keep your spending on the card below 10% of the limit. That means if you have a $1,000 limit, don’t charge more than $100 at a time.

3. Get Installment Loans

Your credit mix plays a part in determining your credit score. The more varied the history on your credit report, the more reliable you might appear as a borrower. Along with considering revolving credit in the form of credit cards, it’s a good idea to add an installment loan or two to your credit mix. While revolving loans let you pay off your balance and borrow more, installment loans are issued in a lump sum. You then pay them back with interest in monthly installments. How long it takes to repay the loan depends on its term.

A mortgage is an example of an installment loan, as are student loans and car loans. If you’re looking to build credit, getting a student loan or car loan is likely going to be easier than getting a mortgage. Some types of student loans, notably federal student loans, don’t require a credit check first, making them easy to get, even if you have no credit at all. Some car loans are also available to people with minimal credit histories.

As with any type of loan, it’s important you make sure you can repay your installment loan based on its terms. You can take out several student loans without a credit check and borrow thousands of dollars to pay for school, but for the sake of your future credit, it’s important you can afford the monthly payments on those loans after you graduate.

If you’re considering a car loan, also be sure you can afford the monthly payment. You might consider making a larger down payment or buying a cheaper car to be absolutely certain you’ll be able to repay the loan without paying late or missing payments.

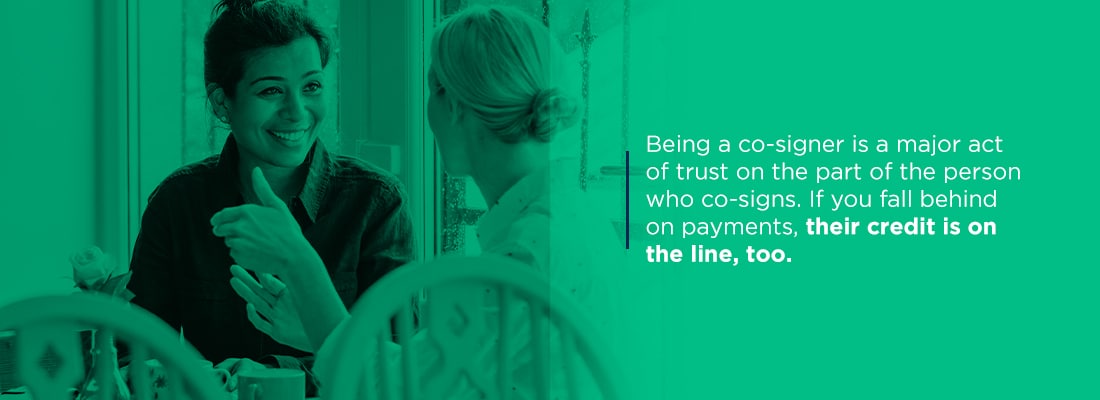

4. Ask Someone to Be a Co-Signer for You

If you’re having difficulty getting approved for a loan or credit card, one option is to find someone who can be a co-signer. A co-signer is usually someone with an established history of good credit, such as a parent, spouse or older sibling. When they co-sign a loan with you, they agree to take on responsibility for it. The loan will appear on their credit report, and they will be expected to pay it if you stop making payments or otherwise fall behind.

Being a co-signer is a major act of trust on the part of the person who co-signs. If you fall behind on payments, their credit is on the line, too. Before you ask someone to co-sign for you, be clear about your plans for the loan. Your co-signer might want to set up rules about the repayment process or otherwise verify you can make the payments. Good communication is key to protecting each person’s credit and preserving your relationship.

A slightly less risky option for a person with established credit is to add you as an authorized user on an existing account, such as a credit card. Some credit cards let account holders add others as authorized users, meaning a person gets a credit card in their name and is put on the account. The authorized user doesn’t own the account and isn’t fully responsible for making payments.

In many cases, the credit card appears on the authorized user’s credit report, helping them establish credit. You don’t have to use the card you’re an authorized user on. Simply having it appear on your report can be enough to improve or establish credit. The trick is to make sure the person who owns the card pays it as agreed and doesn’t pay late.

5. Make Sure Your Loans Get Reported

Three credit reporting bureaus exist that compile all the details about your loans and credit card accounts. Mortgage lenders use the information on the credit bureau’s reports to calculate your credit score. For an account to “count” toward your score, it needs to show up on your credit report.

For the most part, credit card companies and lenders will report your information to the appropriate credit bureaus. But it’s still a good idea to double-check and make sure your account details are going to show up on your credit history. If you’re completely new to building credit, another option is to have your rental payments and utility bills show on your reports. Some lenders will use that information when making a decision about you, and others won’t. If you have a good history of paying your rent and utility bills on time, it can be a useful thing to have show up on your credit report.

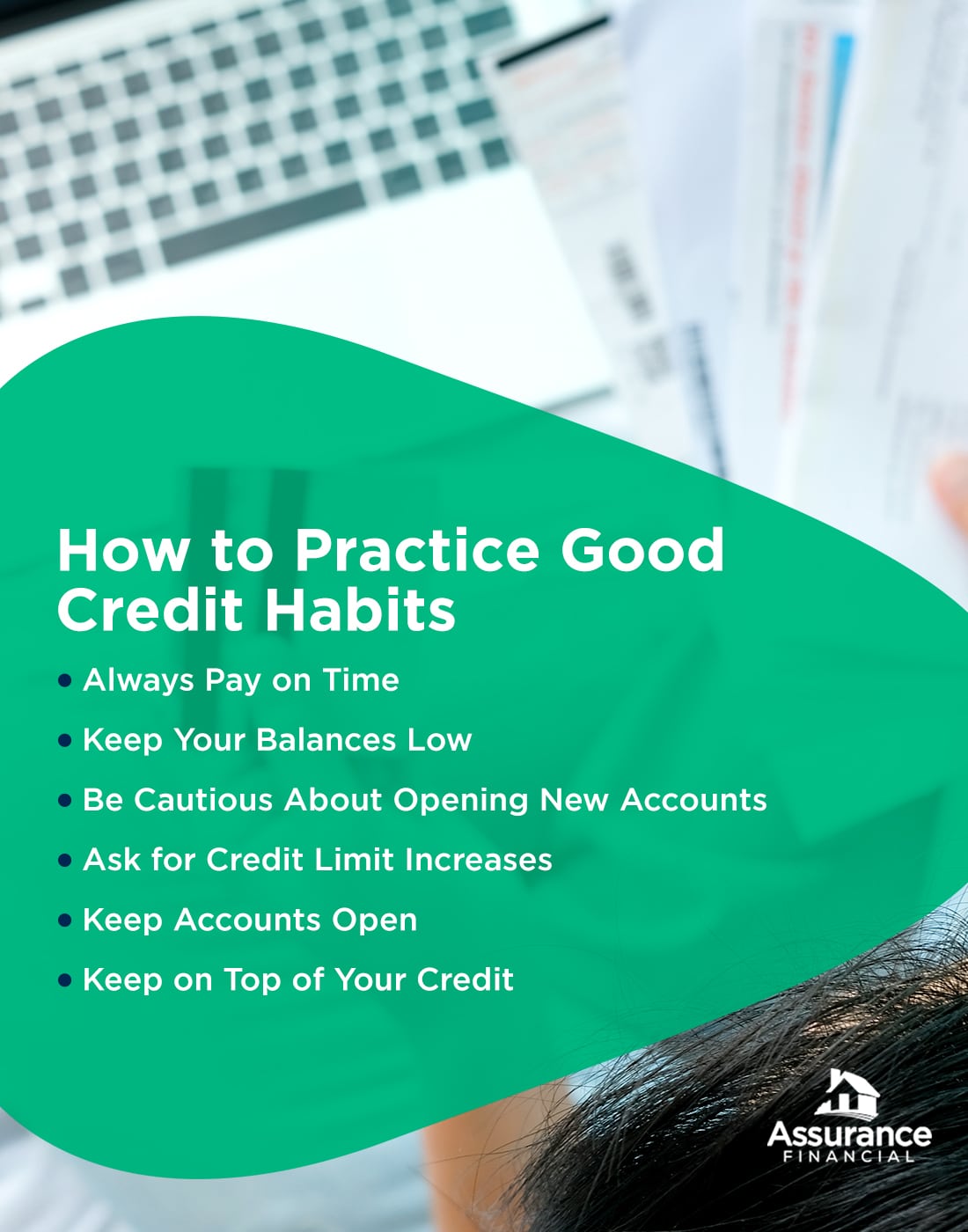

How to Practice Good Credit Habits

After you’ve established a credit history, there are some best practices to follow to help keep your score high and make you an attractive borrower to lenders. Here’s what you can do to build and boost your credit:

1. Always Pay on Time

Your payment history makes up 35% of your credit score, making it the most important factor when it comes to determining your credit. Make sure you always pay your bills on or before the due date and always pay at least the minimum owed. You can pay more than the minimum if you prefer. In fact, paying as much as you can is also good for your credit, as it helps to reduce the total amount you owe.

If you’re worried about missing payments or paying late, you have a few options. You can set up calendar reminders so you get a notification just before the due date. Another option is to automate your payments using a bill-paying service. Some credit cards let you set up automatic payments, so your cards get paid off each month without you having to check a calendar.

2. Keep Your Balances Low

The amount you owe also plays a big part in determining your credit score. The less you owe, particularly in comparison to the amount you can borrow, the better your score. Even if you have a high limit on your credit card, keep your balance well below it. It’s easier to repay your debts when you don’t borrow too much. You also look more reliable to lenders when your balances stay low.

3. Be Cautious About Opening New Accounts

Although you need to have credit accounts to establish a credit history and start building your score, it’s possible to have too much of a good thing. New credit affects your score, and every time you open a new account, your score drops a bit. If you go out to the mall and open several new store credit cards in a day, that can have a notable impact on your credit. Opening several new credit cards at once can be a red flag for a lender. They might look at your new accounts and wonder if you’re experiencing financial difficulties, which would make it challenging for you to repay a new loan.

If you’re in the process of applying for a mortgage, it’s critical you avoid opening new accounts, at least until you have final approval on the mortgage and have closed on your home. Opening a new credit card or taking out a car loan while your mortgage is in the underwriting process can sound like a warning bell to the lender, causing them to press pause on the proceedings.

4. Ask for Credit Limit Increases

Your credit utilization ratio affects your credit score. The ratio compares how much credit you have available vs. how much you have used. For example, if you have a credit card with a $1,000 limit and a balance of $100, your credit utilization ratio is 10%. The lower the ratio, the better for your credit. Keeping your balances low is one way to keep your ratio low. Another way is to increase your credit limit. For instance, you can ask the credit card company to raise your $1,000 limit to $2,000.

Credit card companies might be willing to increase your limit in several cases. If you have a history of paying on time, the company might see you as a lower-risk borrower and agree to increase your limit. An improvement in your credit score or an increase in your household income can also convince a credit card company that you’re a good candidate for a limit increase.

5. Keep Accounts Open

The longer your credit history is, the better it looks to lenders. A person with a 20-year history has more to show than someone with a five-year history. When possible, keep your credit accounts open to maximize the length of your history. For example, if you have a credit card that you no longer use, it’s still a good idea to keep the account open.

Another reason to keep credit card accounts open is that doing so helps your credit utilization ratio. If you have three credit cards that each have a $5,000 limit, your available credit is $15,000. Close one of those cards, and your available credit drops to $10,000.

6. Keep on Top of Your Credit

Everyone makes mistakes, including the credit reporting agencies. Whether you plan on applying for a mortgage soon or in the distant future, it’s a good idea to keep a close eye on your credit reports, so you can detect and fix any issues that come up. Possible mistakes include incorrectly reported payments, accounts that don’t belong to you and outdated information. If you see a mistake on your report, you can let the credit bureau know, and it will take action to correct it.

The Benefits of Building Credit

Having a solid credit history can help you in many areas. With a strong credit score, you can get the best rates on a mortgage or construction loan. Your credit also plays a role in helping you qualify for other loans and can let you get a better rate on insurance. Some employers also check credit when making hiring decisions.

That can mean the sooner you start building credit, the better. Even if buying a house seems like it’s years in the future, laying the groundwork today could mean a lower interest rate and better terms later on.

Boost Your Credit With a Mortgage From Assurance Financial

When you buy a home, getting a mortgage could help your credit. Once you’re approved for the home loan and make regular payments on it, you’re likely to see your score improve. Assurance Financial has simplified the mortgage application process, making it easier for you to become a homeowner and start living your dreams. Start your application with us online today.

Linked Sources:

- https://files.consumerfinance.gov/f/documents/cfpb_targeting-credit-builder-loans_report_2020-07.pdf

- https://www.myfico.com/credit-education/whats-in-your-credit-score

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/how-to-get-a-mortgage-loan/

- https://assurancemortgage.com/important-credit-score-home-loan/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/credit-score-determined

Many homebuyers make a list of the things they’d like in their new home — including the number of bedrooms, the types of amenities and the size of the yard, to name a few. When shopping for a home, it’s just as important to make a list of things you’d like from your mortgage — including the length of the loan, the interest rate and the repayment terms.

You have lots of options when choosing a mortgage. Some home loans are designed for people who meet specific criteria, and others for people who might not qualify for another type of loan. Take a look at some of the different types of mortgages available and what they offer to find the best mortgage for you.

Table of Contents

- What is a Mortgage?

- What Mortgage Do I Need?

- Fixed-Rate Mortgages

- Adjustable-Rate Mortgages

- Other Mortgage Options

- Programs to Help You Get a Mortgage

- Apply with Assurance Financial Today

What Is a Mortgage?

A mortgage is a type of loan you acquire to purchase a home. When you apply and are approved for a mortgage, the lender agrees to let you borrow a sum of money that is usually less than the home’s value. You need to repay the mortgage according to the terms of the loan. Most mortgages require you to make monthly payments of principal, interest and other fees, such as private mortgage insurance (PMI).

When you have a mortgage, the home acts as collateral. If you stop making payments and don’t work something out with the lender, they can foreclose on the home. Since the home is collateral, many mortgages have lower interest rates than unsecured loans, such as personal loans or credit cards.

When choosing a mortgage, there are several things to pay attention to:

- The length of the loan term:30 years is a popular mortgage term, but 10, 15 and 20-year mortgages are also available.

- The size of the interest rate: The market influences your interest rate, as does your credit score, income and loan size.

- The type of interest rate: Your rate can be fixed, meaning it will stay the same throughout the life of the loan or adjustable.

- The type of fees, such as PMI, lender’s fees and other fees: You’ll most likely need to pay an assortment of closing costs and may need to pay fees such as PMI premiums each month.

- The loan size:The amount you borrow depends on the size of your down payment, the cost of the house and what you can afford.

What Mortgage Do I Need? The Best Type of Mortgage to Get

How do you know which mortgage is right for you? It helps to consider your financial stability, your employment situation and your credit history. Two broad categories of mortgages exist, private loans and government-backed loans. Private loans often have stricter requirements, while government-backed loans are guaranteed by various federal agencies or departments and have looser requirements.

Your lender will let you know which mortgages you qualify for and help guide you to the one that best meets your needs. Get to know some of the most common mortgage options:

1. Conventional Conforming

A private lender makes a conventional mortgage. It’s not guaranteed or backed by the government. A conforming loan aligns with the standards created by the Federal Housing Finance Agency. One of those standards is a loan limit for all loans that Freddie Mac and Fannie Mae purchase. As of 2021, the limit for a conforming loan is $548,250* for a single-family home. The limit in areas with a high cost of living and higher-than-average housing prices is $822,375*.

You need to meet stricter requirements to qualify for a conventional loan. One of the requirements is a higher credit score. While you might get approved for a conventional loan with a score around 620, to get the best possible terms, including the lowest possible interest rate, it’s better to have a score in the mid-700s or higher.

The down payment requirements for a conventional loan are typically different than for other mortgage types. The standard advice is to put down at least 20% to get a conventional mortgage. But your lender might be willing to approve you if you have a smaller down payment. If you put down 5% or 10%, you can expect to pay PMI premiums in addition to your monthly principal and interest payments. How long you need to pay for insurance depends on how long it takes you to pay off at least 20% of the home’s value.

Once the loan-to-value ratio is 80% or less, you can ask the lender to remove the PMI premiums. The lender should automatically cancel your PMI premiums when the loan-to-value ratio falls to 78%.

A conventional conforming mortgage offers you a fair amount of flexibility. You can choose the mortgage term and the type of interest rate, such as fixed or adjustable. Some conventional loan programs even allow you to put down just 3% of the home’s value, making homeownership potentially more attainable and affordable.

Are you eligible for a conventional loan? Review these requirements to determine whether you qualify for this mortgage loan type and whether it’s right for you:

- Your credit score is above average. A higher score can potentially result in a lower interest rate, especially for those with a score over 740.

- You have a reasonable or low debt-to-income ratio. The ratio of your financial obligations to your monthly income should not exceed 43%.

- You have saved up enough for a down payment between 3% and 20%. Keep in mind that with a smaller down payment, you will most likely need to buy private mortgage insurance.

2. Conventional Non-Conforming

Some homes cost way more than the conforming loan limits set by the Federal Housing Finance Agency due to the home’s size, amenities or location. You can still get a mortgage for an expensive home, but the type of mortgage you get will be slightly different from a conventional conforming loan.

Conventional non-conforming mortgages are also called jumbo loans due to their size. As a general rule, lenders consider jumbo loans to be riskier than conforming loans. The borrower is borrowing more from the lender, so there is a slightly higher risk of default. For that reason, jumbo loans traditionally have slightly higher interest rates than conforming loans. They also usually have stricter eligibility and down payment requirements.

For example, while you might get a conventional conforming loan with as little as 3% down, you can expect to put down at least 20% to get a jumbo loan. You also need a higher credit score to qualify for a jumbo loan. Usually, the minimum score a lender will consider is 700. The higher your score, the more likely you are to get approved and potentially get a lower interest rate.

A lender will also carefully consider your debt-to-income ratio before approving you for a jumbo loan. The more existing debt you have, the less likely you are to get approved for the loan. There is a limit to jumbo loans. Usually, the maximum amount you can borrow to buy a single-family home is around $1 million.

Are you eligible for a jumbo loan? Review these requirements to determine whether you qualify for this mortgage loan type and if it’s right for you:

- Your credit score is above average.

- You have a debt-to-income ratio below 36%.

- You have saved up a hefty down payment, at least 20% of the home’s price.

- You need to buy a home that costs more than the conforming loan limit.

[download_section]

3. FHA

Government-sponsored mortgage programs aim to help people who might have difficulty qualifying for conventional loans purchase a home. The first type of government-backed mortgage is an FHA loan. The FHA loan program dates back to 1934. The government created it to ease credit requirements, allow for smaller down payments and reduce closing costs, making it possible for people to buy their first homes.

Usually, FHA loans allow borrowers to put down between 3.5% and 10% of the home’s value. How much you need to put down depends on your credit score. FHA loans allow borrowers to have slightly lower credit scores than conventional mortgages. To get an FHA loan with a 3.5% down payment, your score must be at least 580. If your score is at least 500, you’ll need to put down 10%.

Although FHA loans are government-backed, the mortgages themselves don’t come from the government. Instead, private lenders issue them with the understanding that the government will step in and cover the cost if the borrower defaults or stops making payments on the loan. The government guarantee protects the lender from losing too much money on a potentially risky loan.

In exchange for the government’s backing, you need to pay mortgage insurance if you decide to take out an FHA loan. FHA mortgage insurance is slightly different from the PMI premiums you pay on a conventional mortgage. First, the mortgage insurance is for the entire term of the loan if your down payment is under 10%. Unless you refinance an FHA loan to a conventional loan at some point, you’ll be responsible for premiums from the first payment until the last. You’ll also have to pay a mortgage insurance premium upfront, along with a monthly premium.

FHA loans can have terms of 15 or 30 years. The interest rate is fixed, meaning it stays the same throughout the entire term. An FHA loan might be a good option if you’re having trouble qualifying for a conventional loan due to a lower credit score or lower income.

Are you eligible for an FHA loan? Review these requirements to determine whether you qualify for this mortgage loan type and whether it’s right for you:

- You have a FICO credit score in the range of 500 to 579 with a down payment of at least 10%.

- You have a FICO credit score of at least 580 with a down payment of at least 3.5%.

- You’ve been employed for the past two years.

- You can verify your income with pay stubs, bank statements and tax returns.

- Your FHA loan will be used for your primary residence.

- Your property is appraised and meets property guidelines.

- Your monthly mortgage payments won’t be more than 31% of your monthly income. Some lenders may allow up to 40%.

4. VA

VA loans are available to people who are veterans or who are currently serving in the armed forces. Similar to an FHA loan, a VA loan is government-backed. In this case, Veterans Affairs guarantees the mortgages, which private lenders issue.

VA loans have two distinct advantages over conventional and FHA loans. The first advantage is that they don’t require a down payment. They are one of the few types of mortgages available that allow for 100% financing. Unlike conventional or FHA loans, you don’t have to pay mortgage insurance premiums on a VA loan, even if you put down 0% upfront.

VA loans also offer reduced closing costs. If you take out a VA loan, you need to pay the VA funding fee, which ranges from 1.4% to 3.6%, depending on the size of the down payment and whether you’re buying your first home or not. Other closing costs can be negotiated with the seller, meaning you might be able to get the seller to agree to pay for a portion of the costs.

Since VA loans come from private lenders, the lender might have its own requirements when deciding who to approve for the mortgage. A lender can determine what credit score you need, for example. It might also have certain income requirements.

If you’re a current or former member of the U.S. armed forces, a VA loan might offer the best value for you when buying a home. Spouses and widows of former or current service members can also qualify for VA loans.

Are you eligible for a VA loan? Review these requirements to determine whether you qualify for this mortgage loan type and whether it’s right for you. You may qualify for a VA loan if:

- For 90 consecutive days, you served in active service during a time of war.

- For 181 days, you served in active service during a time of peace.

- For 6 years, you have been an active member of the Reserves or National Guard.

- You are the spouse of a service member who died during active service or from a disability related to their service.

5. USDA

The United States Department of Agriculture (USDA) loan program aims to help borrowers who want to buy homes in rural areas and don’t have high incomes. Like FHA and VA loans, USDA loans are guaranteed by the government — in this case, the USDA. Private lenders issue the mortgages.

To qualify for a USDA loan, you need to meet several requirements. Your income can’t be higher than 115% of the median household income in the area. The home you want to buy needs to be in a rural area or a qualifying part of a suburb. Homes in cities or metropolitan areas don’t qualify for USDA loans.

Since one of the USDA mortgage program goals is to provide housing to people with the greatest need, it’s usually a loan program worth considering if you don’t qualify for other types of mortgages and want to live in a rural area. Though the loan program targets people with low to moderate incomes, you still need to prove a steady income, such as at least two years of stable employment, to qualify. You can get a USDA loan with a lower credit score, but you are likely to get a better interest rate and terms with a score of at least 640.

Like a VA loan, you can get a USDA loan with as little as 0% down. To further assist you with the homebuying process, USDA loans allow sellers to contribute to your closing costs.

Are you eligible for a USDA loan? Review these requirements to determine whether you qualify for this mortgage loan type and whether it’s right for you:

- You have a relatively low income in your area. You can check the USDA’s page on income eligibility to determine whether you qualify.

- You’ll be making the home your primary residence, or for a repair loan, you occupy the home.

- You must be able to verify that you’re able and willing to meet the credit obligations.

- You must either be a U.S. citizen or meet the eligibility requirements for a noncitizen.

- You must be purchasing a property in an eligible area.

What Are Fixed-Rate Mortgages?

An additional thing to consider when choosing the right home loan is the type of interest rate the loan has. A variety of factors influence the rate a lender offers you, including your credit score, income and the loan size.

Another factor that comes into play is whether the rate is fixed or adjustable. A fixed-rate mortgage has an interest rate that stays the same throughout the term of the loan. One advantage of a fixed-rate mortgage is that it lets you lock in a low interest rate, provided rates are on the low end when you buy the home.

A potential drawback of a fixed-rate mortgage is that it can confine you to paying a high interest rate, even after rates have dropped. If you’d like to lower your interest at some point due to a drop in interest rates overall or an improvement in your credit score, you’d need to refinance, taking out an entirely new mortgage.

A mortgage with a fixed rate might be right for you if you plan on staying in your home for the long term and rates are low when you apply for the loan and buy the house. With a fixed-rate loan, you have some reassurance that your principal and interest payment will stay the same throughout the loan term, allowing you to create a steady budget and have a good idea of what to expect when it comes to your housing costs.

What Are Adjustable-Rate Mortgages?

The interest rates on an adjustable-rate mortgage (ARM) fluctuate throughout the life of the loan. Often, ARMs offer an introductory rate that stays the same for several years. For example, you might get a 5/1 ARM, which has a five-year introductory period. After the first five years, the rate changes based on what’s going on in the market.

After the introductory period, your rate can increase or decrease. If it increases, your monthly mortgage payment will also increase. If it drops, your monthly payment will also drop. When the introductory period is over, the interest rate will adjust based on a set schedule. In the case of a 5/1 ARM, the rate adjusts every year.

ARMs often have a rate cap, which keeps the interest rate from increasing too much and helps you avoid a monthly payment beyond your reach. The cap can be on each adjustment, as well as a lifetime cap on interest increases. For example, your ARM might have an adjustment cap of 2% and a lifetime cap of 5%.

One feature that makes ARMs appealing is a low interest rate when you take out the mortgage. The rate you’re offered on an ARM will often be lower than the rate on a fixed-rate mortgage. For that reason, it can make sense to choose an ARM over a fixed-rate loan if you’re not planning on staying in the home for the long run. If you anticipate selling before the end of the introductory period, you can enjoy several years of reduced interest.

Another potential benefit of an ARM is that your rate could fall even more in the future. If you feel that interest rates will keep falling, getting an ARM can help you take advantage of lower rates without the need to refinance your mortgage.

It’s important to note that adjustable rates aren’t offered on all types of mortgages. You can choose a conventional mortgage, FHA loan or VA loan with an adjustable rate.

Other Mortgage Options

In addition to conventional mortgages and government-backed loans, there are several other home loan options for borrowers who might be in unique situations. If you already own a home, it’s possible to get another mortgage on the property, for example. You can also get a loan to build your home.

1. Construction Loan

This type of mortgage loan involves buying land on which to build a house. These loans typically come with much shorter terms than other loans, at a maximum term of one year. Rather than the borrower receiving the loan all at once, the lender will pay out the money as the work on the home construction progresses. Rates are also higher for this mortgage loan type than for others.

There are two types of construction loans:

- Construction-to-permanent: A construction-to-permanent loan is essentially a two-in-one mortgage loan. This is also known as a combination loan, which is a loan for two separate mortgages given to a borrower from a single lender. The construction loan is for the building of the home, and once the construction is completed, the loan is then converted to a permanent mortgage with a 15-year or 30-year term. During the construction phase, the borrower will pay only the interest of the loan. This is known as an interest-only mortgage. During the permanent mortgage, the borrower will pay both principal and interest at a fixed or variable rate. This is when payments increase significantly.

- Construction-only: A construction-only loan is taken out only for the construction of the house, and the borrower takes out another mortgage loan when they move in. This may be a great option for those who already have a home, but are planning to sell it after moving into the home they’re building. However, borrowers will also pay more in fees with two separate loans and risk running the chance of not being able to move into their new home if their financial situation worsens and they can no longer qualify for that second mortgage.

2. Second Mortgage

Second mortgages are taken out after a borrower’s first mortgage and are generally used for financing home improvements, consolidating debt or for covering enough of the first mortgage to avoid the requirement of paying the mortgage insurance. Second mortgages generally have terms that last only up to 20 years and can be as short as one year.

Programs to Help You Get a Mortgage

If you’re buying your first home, several programs exist that help simplify the process or make homeownership more affordable. First-time homebuyers programs are usually available on a state or local level. Some offer grants to help you afford a down payment, while others might help with closing costs or other fees.

Another thing to consider if you’re about to buy your first home is working with a financial counselor. A counselor can help you make a plan for saving for a down payment or help you work on improving your credit so you’ll get the best mortgage terms possible, whether you qualify for a conventional loan or a government-sponsored one.

One thing worth noting is that specific mortgage types aren’t limited to first-time buyers. You might qualify for a USDA or VA loan if you’re buying your second or third home, provided you plan on using the home as your primary residence. The same is true of FHA loans. While the loan programs expect you to live in the home as a condition of qualifying for the mortgage, they don’t require you to be a first-timer.

Another option is the Good Neighbor Next Door Program. It is sponsored by the U.S. Department of Housing and Urban Development and assists law enforcement, firefighters, teachers and emergency medical technicians with housing. The program offers a 50% discount on a home’s listed price in locations deemed “revitalization areas.” To be eligible, you must commit to living in the home for at least 36 months.

Your mortgage lender is also happy to discuss the different types of home loans available. They can work with you to help you choose a mortgage that works best with your current financial situation and that will help you achieve your goals in the future.

Apply for a Mortgage With Assurance Financial Today

Buying a home starts with getting the right mortgage. Assurance Financial has home loan options for every type of buyer, from first-time homebuyers to more experienced buyers. If you’re a veteran, we can help you get a VA loan. If you’re likely to buy in a rural area, we can help you with a USDA loan. Start your application today, or reach out to find a loan officer near you.

Linked Sources:

- https://singlefamily.fanniemae.com/originating-underwriting/loan-limits

- https://www.consumerfinance.gov/ask-cfpb/when-can-i-remove-private-mortgage-insurance-pmi-from-my-loan-en-202/

- https://assurancemortgage.com/jumbo-loans/

- https://www.hud.gov/buying/loans

- https://assurancemortgage.com/fha-loans/

- https://assurancemortgage.com/va-loans/

- https://www.va.gov/housing-assistance/home-loans/funding-fee-and-closing-costs/

- https://www.rd.usda.gov/programs-services/single-family-housing-guaranteed-loan-program

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/find-a-loan-officer/

- https://www.hud.gov/program_offices/housing/sfh/reo/goodn/gnndabot

- https://assurancemortgage.com/usda-loans/

- https://eligibility.sc.egov.usda.gov/eligibility/incomeEligibilityAction.do?pageAction=state

*Not a commitment to lend or extend credit. Restrictions may apply. Loan limits, information and/or data subject change without notice. All loans subject to credit approval. Not all loans or products are available in all states. Assurance Financial is committed to compliance with Section 8 of RESPA and does not offer free marketing services in exchange for referrals or the expectation of referrals.

Ready to take the first steps toward buying a home? If you’re going to finance your home purchase, one of the first things to do is figure out how to get a mortgage. You might have heard that getting a mortgage is a long and complicated process, with plenty of twists and turns along the way.

While it’s true there are several steps involved in applying and getting approved for a home loan, with a bit of preparation and attention, getting a mortgage doesn’t have to be complicated. Here’s what you need to know as you prepare to pursue your dream of becoming a homeowner.

10 Steps to Get a Mortgage Loan

What does it take to qualify for a mortgage? You can divide the home loan process into three major parts — the preparation period, the application period and the approval period. Depending on your timeline and preference, you can spend months or years in the preparation period before moving onto the other two phases. If you’re ready to learn more about how to get a loan for a house, take a look at the steps involved:

1. Save up for a Down Payment

The home loan process always starts with saving. The exact amount you need to save up for a down payment depends on the type of loan you choose, the market conditions and your financial situation. You might have heard a 20% down payment is ideal when you’re buying a home. That might be true, as putting down 20% allows you to avoid paying private mortgage insurance (PMI) premiums and can mean you get a better interest rate on your loan. But it can take many years to save up 20% of a home’s price, especially if you’re buying in a market with high housing prices.

Fortunately, there are other options available. You might qualify for a conventional mortgage with a 5% or 10% down payment. You will have to pay PMI premiums when you make your monthly mortgage payment, but those premiums will go away once you’ve paid at least 20% of the house’s value. If you meet certain requirements, you might qualify for a conventional loan with just a 3% down payment.

Certain mortgage programs, particularly government-backed loan programs, let you get a home loan with much less than 20% down, too. USDA Rural Development and VA loans accept 0% down. There are other factors to consider when deciding which loan to apply for as well.

Once you’re ready to start saving, there are a few ways to go about doing it. First, set a goal amount. If homes in your area cost an average of $250,000, and you want to save up 5%, for a down payment, you’ll need to save $12,500. Next, set a target date. Let’s say you want to have your down payment within 24 months. Once you know how much to save and how long you have to save, you can figure out how much to put aside each month. In this example, you’ll need to save around $520 monthly.

You might have to consider how you’ll come up with that $520 each month. One way to do that is to create a budget and to plan your expenses with care, so you have enough to save for your goal. To make the process of saving easy, set up an automatic transfer from your checking account to a designated savings account. That way, you’ll save without having to think about it.

2. Track Your Credit Score

Having a good credit score makes the homebuying process a breeze! Before you start the buying process, get a copy of your credit report. You can request a free report from annualcreditreport.com. Your bank might also let you review your report for free. Some also give you access to your credit scores, which can give you a good idea of where you fall on the credit score range. Once you’ve examined your credit profile, you can begin taking steps to improve your credit score if need be.

What should you look for when reviewing your credit history and score? First, it helps to understand what a credit score is and what makes one “excellent” versus “good” or “poor.” Scores range from 300 to 850. If your score is above 800, way to go! You have what most lenders consider an excellent score. Scores between 740 and 799 are usually “very good”, while scores between 670 and 739 are “good.” It can be difficult, but not impossible, to get a mortgage with a score below 670.

One factor that plays a significant role in determining your credit score is your payment history. If you have a lot of missed payments or late payments on your credit report, your score is going to take a hit. How much you owe also plays a big part in determining your score, so if you have several credit cards with high balances or owe a lot on a car loan or in student loans, your score might be lower than you want.

Fortunately, you can take action to improve your score. The first thing to do is get current on paying your accounts if you’ve fallen behind. If you aren’t behind, commit to staying caught up with your payments. The next thing to do is to focus on reducing how much you owe. Reducing your overall debt burden can also help you later on in the mortgage application process, as a lender will look at how much you currently owe when determining how much you can borrow for your home.

3. Explore Your Loan Options

Despite their sound advice, the loan program that worked best for your parents may not always be ideal for you. Take some time to research which loan program will fit your current financial situation. Everyone has a set of unique financial needs. With a little digging and help from our reliable loan advisors, you’ll be able to find the loan that best suits your needs.

Some mortgage options include:

- Conventional mortgages: A conventional mortgage is your standard home loan. It’s not guaranteed by the U.S. government, so a lender assumes the full risk of extending the loan to you. You might need to meet stricter requirements to get a conventional mortgage compared to other home loan options, such as having a higher income, above average credit, and a sizable down payment. Often, a combination of some factors, such as a steady employment history with a high income and an excellent credit score, can make up for missing other factors, such as only having a 5% down payment.

- Federal Housing Administration (FHA) loans: FHA loans are guaranteed by the U.S. Department of Housing and Urban Development (HUD), a government If a borrower stops paying their FHA loan, HUD will make payments to the lender. The guarantee from HUD means lenders are willing to approve borrowers with smaller down payments — as little as 3.5% — and lower credit scores for mortgages. In exchange, the borrower needs to pay PMI and an upfront mortgage insurance premium.

- VA loans: VA loans are for active-duty or veteran service members. They’re backed by the Department of Veterans Affairs and allow people to get a mortgage without a down payment.

- USDA loans: The USDA loan program is guaranteed by the U.S. Department of Agriculture. Its purpose is to encourage people to buy homes in rural or certain suburban areas. The loan program allows buyers to put zero down.

- Jumbo loans: A jumbo loan is also called a non-conforming loan. It’s a conventional mortgage that’s above the lending limits set by FreddieMac and FannieMae. If you’re looking to buy a large, expensive home, you might need a jumbo loan to do it. Often, you’ll need to have excellent credit and a hefty down payment to qualify for a jumbo loan.

[download_section]

4. Get Organized and Prepared

Congratulations, by this point, you’re nearing the end of the preparation period of the mortgage process. You’re now getting ready to actually apply for the loan itself. When you submit your mortgage application, you’ll need to hand over a few important financial documents to your lender. The exact documents you’ll need might vary slightly based on the lender you work with and your particular situation. The more prepared and organized you are, the better. Some of the documents you’ll want to have ready include:

- Tax returns: Have at least the past two years of tax returns handy before you meet with a lender to apply for a mortgage. Your lender might also ask you to complete and sign Form 4506-T, so it can pull your returns from the IRS.

- Pay stubs or other proof of income:Your lender will also want to verify your current income. If you are employed, you can present your most recent paystub or Form W-2. If you’re a freelancer or work for yourself, be prepared to show proof of income in other ways, such as Forms 1099, your tax returns or profit and loss statements.

- Bank statements:Your lender will want proof that you have enough saved up to make the down payment and cover closing costs. They might also want to see evidence of additional assets. Have all of your most recent bank statements, plus statements from any investment accounts you have, ready. Also gather up documents concerning other debts you have, such as credit card or student loan statements.

- Credit report: Your lender is going to pull your credit and won’t need you to show them the report. It’s a good idea to have it on hand so you can read it over and discuss any areas of concern to the lender. If there are mistakes on the report, contact the credit reporting bureaus before you meet with the mortgage lender to have the incorrect information removed from your report.

- Rental history: If you’re a renter, your lender might ask to see proof that you’ve paid your rent for the past year.

- Identification:You’ll need photo identification, such as your passport or driver’s license, when you apply for a mortgage.

5. Fill out a Mortgage Application

You’re prepped and ready, it’s time to start the process of applying for a mortgage. Gather up your financial documents and apply online.

The lender will review your documents to see how your income compares to your debts and to see how your credit stacks up. With this information, they’ll provide a maximum loan amount and let you know the interest rate you can expect to pay. At this point, if all goes well, you’re pre-qualified for a mortgage and can start the process of looking at homes.

6. Think About What Affordable Means to You

As you move into the application portion of the mortgage process, it can be useful to think about what you really want to spend on a home. Lenders consider your debt-to-income (DTI) ratio before pre-qualification. DTI compares your monthly income to the amount you owe each month. Your front-end DTI is how your projected total housing payment compares to your monthly income. The back-end DTI includes all your monthly debts. The ideal front-end DTI to back-end DTI ratio is about 25%/41%. Some conventional loans will allow a back-end of 50%, and FHA will even allow 56.99%.

While the “ideal” back-end DTI is about 41% and your lender might allow you to have a DTI of 50% or more, think carefully about whether that’s something you’re comfortable with. You might prefer to buy a less expensive house to keep your total debts low. If you have many other debts, you might want to buy less house so you can focus on paying off the more expensive debts. On the flip side, if you are going into the mortgage process without any other debts or financial obligations, you might feel comfortable purchasing a home at the upper end of your price range.

7. Start Looking at Houses

Once you’ve set a budget and know your price range, it’s time to get out there and start looking at homes. It takes time to find the right home. At the beginning of the house shopping process, make a list of the things you need to have in your future home. Some features to consider include:

- Number of bedrooms: Think about your family size now and in the future. If you’re single or have a partner, do you want to have kids someday? If so, do you want to continue to live in your current home? Another thing to think about when deciding how many bedrooms to have is whether you have guests frequently and whether you need a place to work from home.

- Number of bathrooms: A one-bathroom home might be fine for a couple or a single person, but it can be challenging for larger households. You might also want a half bath on the first floor for people to use when they visit your home.

- Kitchen size and layout: You might not need a big kitchen, but you probably want one that’s well laid out so it’s not difficult to get what you need when cooking. Another thing to consider is an open or closed layout. Some people like to see the rest of the living space from the kitchen, while others prefer a kitchen that’s separate from the rest of the house.

- Outdoor space: Do you want a yard? If yes, how big should the yard be? You might be happy with a concrete patio, or you might want a large backyard with a lush, green lawn.

- Location: Carefully consider where you want to live. How long do you want your commute to be, how important are quality schools to you, and how safe is the neighborhood overall?

Once you have a basic idea of what you want, book an appointment with a real estate agent and start touring homes in your desired area. Once you found one that works for you, put in an offer.

8. Get Ready for Loan Processing

After the seller has accepted your offer and the home has passed inspection, it’s time for the meat of the mortgage application process to start. At this stage, the lender is going to run all your documents, verify all your information and let you know whether you’re approved or not.

Your loan application gets sent over to the loan processors. Once it’s in their hands, they begin double-checking everything on your application. The processor will prepare and organize the file before it’s sent over to the bank or mortgage lender for approval. They will contact your employer to verify your job and the salary on your application. If there are any questions regarding the information on your application, they will have your loan officer contact you for details. Any mistakes you’ve made will arise during this stage, giving you a chance to make corrections before the file is handed off to the underwriter.

Keep your phone handy during this stage, as the processor is likely going to call you to verify information or correct details. They might call or e-mail you to ask you to send them even more paperwork, particularly if you’re self-employed.

9. Wait for the Underwriter’s Decision

Once your loan application passes the processing stage, it heads to the underwriter. The underwriter is the person who decides whether or not to issue the final approval on your mortgage application. To approve your application, they’ll pull your credit again and will review your job history and income.

Before the loan moves to the underwriting phase, the mortgage lender will likely require a home appraisal. During the appraisal, a third party will evaluate the home to determine its worth. They’ll use the prices of similar, recent sales in the area, the condition of your home and its size when determining its value. Ideally, the appraiser will decide that your home is worth as much as you’re paying for it, if not more. If the appraiser under-values your home, meaning they think it is worth less than the mortgage, your lender could deny your loan.

When your loan is in the underwriting phase, it’s important that you leave your credit and employment situation alone. Now’s not the time to change jobs or quit your job. It’s also not the time to start buying furniture for you new place or apply for credit cards or other loans.

10. Head to Closing

If all goes well with underwriting, the lender will approve your application and clear you for closing. You’re so close to being a homeowner at this stage!

On the day of closing, you’ll need to bring your down payment and any other fees and closing costs. Usually, you’ll need the money in the form of a cashier’s check, or you’ll need to arrange for a wire transfer of the funds. Your lender will let you know how much you need to bring with you, usually a few days in advance, so you have time to get the cashier’s check or set up the wire transfer.

At closing, you’ll sign a lot of paperwork, will likely pose for a few photos with your real estate agent and lender, and most importantly, will get the keys to your new home.

Start the Mortgage Application Process With Assurance Financial Today

Are you ready to start the process of getting a home loan? Assurance Financial can help. You can find a loan officer near you and set up an in-person visit to get the process started today.

Linked Sources:

- https://assurancemortgage.com/loan_process/

- https://assurancemortgage.com/ways-to-save-for-a-down-payment/

- https://www.annualcreditreport.com/index.action

- https://assurancemortgage.com/conventional-loans/

- https://assurancemortgage.com/fha-loans/

- https://assurancemortgage.com/va-loans/

- https://assurancemortgage.com/usda-loans/

- https://assurancemortgage.com/why-get-pre-qualified-before-looking-for-home/

- https://assurancemortgage.com/loan-options-self-employed-buyers/

- https://assurancemortgage.com/what-to-expect-during-a-home-inspection/

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/find-a-loan-officer/

Buying a home is a major commitment, both on the part of the buyer and the lender. As a buyer, you agree to take care of your new home and repay your mortgage based on the terms of the loan. The lender is taking a chance by providing you a significant sum of money upfront, with the expectation that you’ll pay it back with interest.

Lenders use several factors when deciding whether or not to lend money to an individual or group of people. One of those factors is the borrower’s credit history and credit score. Learn more about the importance of your credit history when getting a mortgage and what you can do to make the most of yours.

Table of Contents

- What is a Credit History?

- How Important is a Credit Score?

- How Does Your Credit Affect Interest Rates?

- What Happens to Your Credit After Approval?

- Other Factors to Consider When Buying a Home

- How to Improve Your Credit Score

- Apply for Home Loan Insurance Today

What Is a Credit History?

Your credit history is a snapshot of how you’ve used money and loans throughout your life. Generally, your credit history includes the following:

- The number of loans or credit accounts you have:Your credit history includes accounts that are currently open as well as closed accounts. Examples of closed accounts include a loan you’ve paid off or a credit card you canceled.

- The amount you owe on each account:Your credit history also reflects how much you owe on each account. For example, you might have a student loan with a principal balance of $15,000, and you might owe $2,500 on a credit card. If the account has a limit, such as a credit card with a limit of $7,000, that will also be part of your credit history.

- The types of accounts you have: Loans typically come in two forms — revolving and installment. Installment loans include personal, auto and student loans. Credit cards are common examples of revolving loans.

- Your payment history: Whether you pay on time, have made late payments or have missed payments will all be part of your credit history. If you have any loans that went into collection or that were charged off, those will appear on your credit history, too.

The information that makes up your credit history is contained in a credit report. There are three bureaus that put together credit reports. What gets reported by one bureau might not get reported by another, which can affect the accuracy of your credit history. In addition to details about your credit and loan accounts, your credit report will contain identifying information, such as your current address and a list of your previous addresses, your birthdate and your Social Security number.

How Do Lenders Use Your Credit History?

Lenders look at your credit history to get a sense of your relationship to loans and money in the past. If you have a very short credit history or don’t have one at all, a lender doesn’t have much to work with. They have no way of knowing whether you’re likely to pay your loan as agreed or if there’s a high risk that you’ll default on it.

If you have a history of on-time payments and a variety of loan accounts, a lender might feel more confident in letting you borrow money. Lenders also look at how much you owe when making a decision about you. If you have a lot of outstanding debt, they might be hesitant to offer you more credit. Along with approving you for a mortgage, a lender might also offer you a lower interest rate or let you borrow more money if you have a strong payment history and don’t currently owe a lot of money.

How Important Is a Credit Score?

Your credit history plays a significant role in determining your credit score, a three-digit number ranging from 300 to 850. If you’re interested in getting a mortgage, your credit score is important, as it lets a lender see at a glance how you’ve handled money and loans in the past. The higher your score, usually the better the terms you’ll get on a mortgage.

Certain parts of your credit history influence your score more than others. Usually, the following five factors determine your total score:

- Payment history: Your payment history has the biggest impact on your score, accounting for 35% of the total score. That makes sense, as a lender may hesitate to let someone who regularly misses payments or pays late borrow money.

- Amount you owe: How much you owe on existing loans also has a considerable impact on your score, accounting for 30% of the total. A lender is likely to be nervous about lending money to someone who already has a significant amount of debt.

- Length of history: The longer your credit history, the better, although the length of your history only accounts for 15% of your total score. If you’re interested in getting a mortgage one day, it may be a good idea to open up your first credit card or get another type of loan when you’re relatively young.

- Types of accounts: The type of accounts you have play a smaller part in determining your score. Credit mix accounts for 10% of your total score. While you don’t have to have one of every possible type of loan, it’s useful to have a variety of accounts in your history, such as a credit card and a personal loan, or a credit card and auto loan.

- New credit: New credit accounts for 10% of your score. Multiple new accounts on a credit report can be a red flag to lenders. They might wonder why someone opened several credit cards or took out multiple loans at once.

Your credit score has a part in determining how much interest you pay on a loan and can also play a role in the type of loans you’re eligible for.

What Is a Good Credit Score for a Home Loan?

If you’re going to pay for your new home in cash, you technically don’t need to worry about your credit history or score, as you aren’t borrowing money. But if you plan to get a mortgage to pay for part of your new home, your credit score is going to play a bigger role. The credit score you need to qualify for a home loan depends in large part on the loan you’re applying for and the amount you hope to borrow.

Conventional mortgages typically require higher credit scores than government-backed mortgages. A lender assumes more risk when issuing a conventional home loan, so it’s important for them to only lend money to people with strong credit scores. The minimum credit score for a conventional mortgage is around 620. But a borrower is going to get better rates and the best terms possible if their score falls in the “Excellent” range, meaning it’s above 740.

A borrower can qualify for certain government-backed mortgages, such as the FHA loan program or VA loans, with a much lower score. The FHA loan program may also accept borrowers with scores as low as 500, but those borrowers need to make a down payment of at least 10%.

How Does Your Credit Affect Your Interest Rates?

The higher your credit score, the lower your interest rate may be on a mortgage or any other type of loan. A lender will feel more confident issuing a mortgage to someone with a score of 800, for example, than they would approving a mortgage for someone with a score of 690. To reflect that confidence, the lender will charge less for the loan.

At first glance, the difference between the interest rate someone with a score of 800 is offered and the rate someone with a score of 690 is offered might not seem like much. For example, someone with a score of 800 might get a rate of 4%, while a person with a 690 score might be offered a rate of 4.5%. But over the 15-year or 30-year term of a mortgage, that half of a percentage point difference adds up to thousands of dollars.

Depending on the type of mortgage you apply for, you can qualify for a better rate with a lower score. For example, if you apply for an FHA loan with a score of 580, you’ll get a higher rate than someone who applies with a score of 700. But if the person with a score of 700 applies for a conventional mortgage, they are likely to get a higher rate on the conventional loan than on an FHA loan.

What Happens to Your Credit After You’re Approved for a Loan?

Your mortgage will appear on your credit reports and will affect your credit score. Overall, adding a mortgage to your credit history is a good thing. But there are a few things to note. One is that initially, your score might drop after you get approved for a mortgage and close on your home. When you get a mortgage, you add a significant amount to your total debts owed, which accounts for nearly one-third of your credit score. You also add new credit to your report, which accounts for 10% of your score.

Don’t panic if you see your score drop after taking out a mortgage. If you had a relatively high score to begin with, the drop is likely only to be a few points. You’re also going to improve your score relatively quickly. As you start paying off your mortgage, the lender that owns it will report your payments to the credit agencies. After a few months of on-time, consistent payments, you’ll have bolstered your payment history on your report.

Another reason not to panic about an initial drop in your credit score is that your mortgage will boost your score over time, provided you continue to pay regularly. Mortgages are examples of installment loans. You borrow X amount and as you pay it down, the amount you owe decreases. That reduces the total amount owed that shows on your credit reports, ultimately improving your score.

A mortgage also gives you a more diverse credit portfolio. If you previously had mostly credit cards, adding a mortgage increases the variety of your credit mix, which can boost your score.

Other Factors to Consider When Buying a Home

While your credit score is important, it’s not the only factor that determines the interest rate you’re offered or whether a lender approves your application or not. A few other things that influence your mortgage include:

- Your down payment: How much you can afford to put down influences the interest rate you’re offered as well as the type of mortgage you qualify for. If you plan on taking out a conventional loan, your down payment can range from 3% to 20%, but only borrowers who meet certain requirements can qualify for a 3% down payment. Usually, the more you put down, the lower your interest rate.

- Market conditions: The overall market also influences the rate you get offered on a home loan. When rates are high, your interest rate will be higher, even if you have the best credit possible. When rates are low, you can qualify for a lower rate than you would otherwise. How competitive the market is also influences your mortgage options. It can be more challenging to qualify for a mortgage with a low down payment or lower credit score when there’s a lot of demand from buyers and few homes available for sale.

- Mortgage options: Depending on the type of mortgage you apply for, you might not need to have a credit score in the “excellent” or “very good” category. Certain government-backed loan programs are available to borrowers with less-than-stellar credit. If you have a lower score and don’t have much for a down payment, an FHA loan, for example, might be your best option. On the flip side, if you plan on buying a very expensive home and need to take out a jumbo mortgage to do so, you’ll need to have a higher-than-average credit score and a sizable down payment.

- The price of the home: How much the home costs compared to how much you want to borrow also influences whether or not you get approved for a mortgage. The pricier the home, usually the bigger the risk to the lender. If you’re buying an inexpensive property, you’re likely to get a better interest rate, especially if you’re able to put down a large payment upfront.

- Your income: A lender is going to ask you how much you earn and ask you to verify your income before they agree to lend money to you. They want to ensure you can pay back what you’ve borrowed. The higher your income and how it compares to your total debt influences how much a lender will let you borrow and the interest rate they charge.

- Type of interest: The type of interest rate your mortgage has is another thing to consider. Mortgages with adjustable rates have lower rates at first, but those rates can increase when they adjust. A fixed-rate mortgage might charge a slightly higher rate than an adjustable-rate loan, but you have reassurance the rate will remain the same for the life of the home loan.

- Length of the mortgage:How long you have to repay the mortgage also influences your rate. Mortgages with longer terms, such as 30 years, usually charge higher rates than loans with shorter terms, such as 15 years.

Your lender is likely to look at the big picture, taking your credit score, income, down payment and other factors into consideration before making a lending decision.

[download_section]

How to Help Improve Your Credit Score

If you don’t have a credit history, have limited credit or have a poor credit history, you’ll want to focus on improving your credit before you apply for a mortgage, even if you plan on applying for a government-backed loan. Fortunately, there are a few ways you can boost your credit.

If you don’t have a credit history at all, the first thing to do is open your first account. You have a few options for doing that:

- Get a secured credit card:Secured credit cards help people with limited credit histories or with poor credit boost their scores. When you apply for a secured credit card, you put down a deposit, such as $500. The deposit acts as collateral on the card, reducing the risk to the lender.

- Apply for a credit builder loan: Another option is to apply for a credit-builder loan from a credit union or bank. Credit builder loans are slightly different from other types of loans. In effect, it works backward. You don’t get the borrowed money upfront. Instead, you pay the lender each month, and it holds your payments in an account. Once you’ve paid off the full balance of the loan, you can receive the funds and use them as needed.

- Apply for a store credit card: If a credit-builder loan or secured credit card doesn’t appeal to you, another way to establish credit is to apply for a store credit card. Be cautious with this approach, though. You don’t want to charge so much on the card that you have trouble paying off the balance and end up with missed or late payments.

- Ask someone to co-sign with you:Finding a co-signer is another way to qualify for a loan with a limited credit history. Your co-signer is a co-borrower, meaning they are responsible for paying the loan if you fall behind. Make sure the person who agrees to co-sign with you understands the risks they are taking on before going forward.

If you do have a credit history but your score isn’t what you want it to be, there are things you can do to improve your score. It might take a while to get your credit where you want it to be, so it can be useful to check out your credit report months or years before you plan on buying a home:

- Pay on time:Remember that payment history is the big one when it comes to your overall score. If you’ve fallen behind on certain accounts, do whatever you can to make them current. Commit to paying every other account on or before the due date.

- Avoid new credit accounts: Try to avoid opening lots of new credit accounts, as doing so will cause your score to drop. It’s especially important to avoid new accounts while you wait for final approval on your mortgage, as opening a new credit card or taking out a different loan during that time can disrupt the approval process.

- Keep your debt balances low: How much you owe overall plays a major part in the calculation of your credit score. If you currently have a lot of credit card debt or student loans, try focusing on paying them off or significantly reducing the balance before you apply for a mortgage.

Apply for a Home Loan With Assurance Financial Today

Is your credit score where you want it to be? Even if it’s not, our helpful loan officers can help you decide the what’s best for your home buying goals. You can start the application process online with Assurance Financial. A loan officer will then get in touch to finalize your application.

Linked Sources:

- https://www.myfico.com/credit-education/whats-in-your-credit-score

- https://assurancemortgage.com/conventional-loans/

- https://assurancemortgage.com/va-loans/

- https://assurancemortgage.com/fha-loans/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/apply/