Category: Loans

Taking out your first mortgage is a huge life step. A mortgage is a critical tool to have — it allows you to become a homeowner without putting down hundreds of thousands of dollars on the spot, and it lets you pay off your loan over time. About 96% of first-time homebuyers finance the purchase with a mortgage.

But mortgages are immensely complex, and many homeowners have questions when they first get started. How do mortgage payments work, exactly? And what is included in your monthly mortgage payment? We’re here to answer your questions so you can approach your new mortgage with confidence.

Topics Covered

- What Are Mortgage Payments?

- How Does a Mortgage Loan Work?

- What Is Included in a Mortgage Payment?

- Mortgage Payment Formula

- Mortgage Vs Loan

- Frequently Asked Questions About Mortgage Payments

What Are Mortgage Payments?

What is a mortgage payment? Mortgage payments are the payments you make on a long-term loan that enables you to buy your home.

Almost everyone who owns a home has a mortgage and makes mortgage payments. Homeowners typically make these payments monthly, over a fixed period of years. Some standard options include 15-year and 30-year mortgages.

What are the advantages of spreading out mortgage payments across more or fewer years? Each approach comes with pros and cons:

- Shorter mortgages: Shorter mortgages tend to have lower interest rates and allow the homeowner to pay less interest overall. The tradeoff is that because the schedule becomes more compressed, these mortgages require higher monthly payments.

- Longer mortgages:Longer mortgages tend to have higher interest rates. So homeowners who choose these mortgages will pay more interest overall. The appealing tradeoff is that by spreading the payments over a longer term, homeowners can lower their monthly payments to more affordable sums. So extended options are often attractive to homeowners looking to create more room in their budgets each month.

Benefits of Making Regular Mortgage Payments

Paying down your mortgage provides you with a couple of different benefits. One is that it reduces the amount of debt you have. As you slowly, steadily make payments, you decrease your debt burden. You increase your debt-to-income ratio, making yourself a more attractive borrower if you decide to take out new loans. You also get a little closer to having your home paid off and having a bit more cash to spend each month.

The second benefit is that you accrue home equity. Home equity is the amount of your home that you have paid off. It equals the value of your home minus the value of your remaining mortgage. So the more of your mortgage you pay down, the more home equity you’ll have. Maintaining as much home equity as you can is an excellent strategy for maintaining financial stability. You can also borrow strategically against your equity by taking out home equity loans — to perform renovations, say, and boost the eventual resale value of your home.

How Does a Mortgage Loan Work?

A mortgage loan is a type of loan that is used to purchase a property, such as a home or a piece of land. You borrow money from a lender to purchase the property and the property serves as collateral for the loan. Here’s how it works:

- Application: You apply for a mortgage loan with a lender, which involves providing personal and financial information.

- Pre-approval: The lender evaluates your creditworthiness and pre-approves you for a certain loan amount.

- Property search: You search for a property to purchase within the pre-approved loan amount.

- Property appraisal: The lender hires an appraiser to determine the value of the property to ensure it is worth the amount being borrowed.

- Loan approval: The lender approves the loan, and you sign a mortgage agreement that outlines the terms and conditions of the loan.

- Down payment: You make a down payment on the property, which is a percentage of the purchase price.

- Closing: You meet with the lender to finalize the transaction. This involves signing a promissory note and a deed of trust, which gives the lender a security interest in the property.

- Repayment: You make monthly payments on the loan, which typically include principal, interest, taxes and insurance. The loan is usually repaid over a period of years.

- Ownership: Once the loan is fully repaid, you own the property outright.

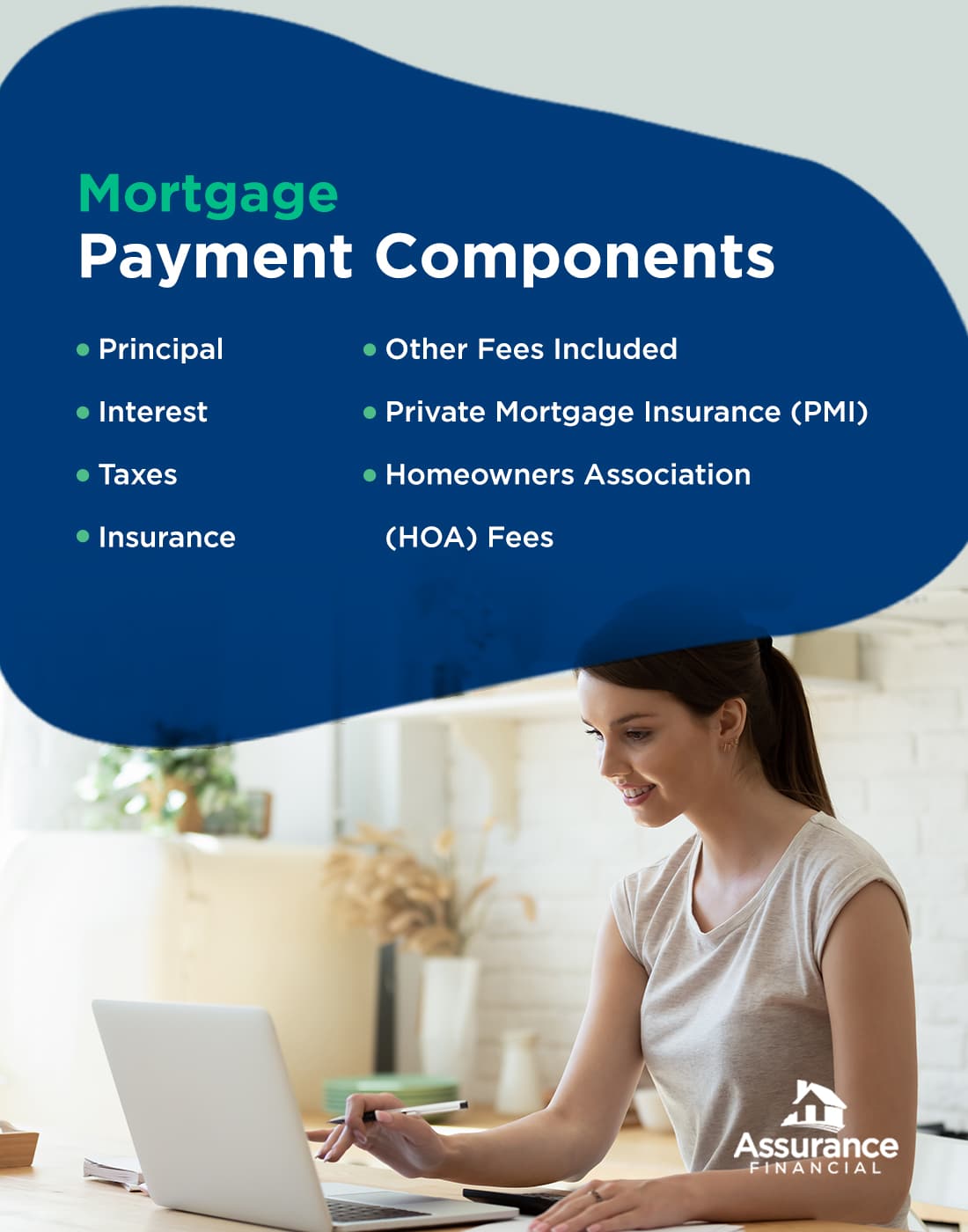

What Is Included in a Mortgage Payment?

Your mortgage payments consist of many different components that all combine into a single sum. Four main components — principal, interest, taxes and insurance (PITI) — go into the makeup of your mortgage payments, and additional fees may be included as well.

Below is a breakdown of those components:

1. Principal

The principal is the amount of money you borrowed from your mortgage lender and have to pay back. Generally, that sum is the price of your home minus your down payment. Say you bought a $300,000 house and put down a 20% down payment of $60,000. Your principal is then $300,000 – $60,000, or $240,000.

Most of your mortgage payment each month goes toward paying down the principal and interest. The part of your monthly payment that goes toward your mortgage principal is what pays down your loan and builds your home equity. Most mortgage structures favor paying down more of the interest at the beginning of the loan and more of the principal at the end.

2. Interest

Interest is the amount charged on the principal because the lender is loaning you the money. The purpose of interest is to reward the lender for taking the risk of lending to you. Charging interest is how lenders make money, keep their businesses running and pay their employees.

Interest rates vary from mortgage to mortgage, and conditions can change quickly. Interest rates decreased between 2018 and 2021, with average interest rates on a 30-year fixed-rate mortgage falling to as low as 2.65% in January 2021. Interest rates in 2023 are somewhat elevated, but many experts predict decreases as the year goes on.

The amount of interest included in your monthly mortgage payment varies inversely with the amount of principal included. At the beginning of your home loan, your payments will include a higher proportion of interest. Toward the end of your loan, that proportion will be much lower.

3. Taxes

Some mortgage payments also include real estate taxes, also known as property taxes.

Local governments assess property taxes to fund public services like schools, fire and police departments and the public works departments that maintain municipal infrastructure. The government requires these taxes annually, but homeowners typically pay them in monthly installments as part of their mortgage payments.

How does the local government receive those funds if it collects them only once per year? Your lender will hold the taxes for you in escrow and pay them once they come due.

If you’re looking at your property taxes and wondering why they don’t line up with the price of your home and your tax rate, remember that counties usually base property taxes on the assessed value of your home rather than on the purchase price. A property assessor looks over your house and then tells the local government its value.

So if you got a massive house at a great price, you might still have hefty property taxes incorporated into your mortgage payments. Say you bought a $600,000 home for $500,000. If the county property tax rate is 1.5%, you’ll pay $9,000 in property taxes for the year — $600,000 x 0.015. Divided by 12 months, that’s $750 in taxes on your mortgage payment.

4. Insurance

Does a mortgage payment include insurance? Usually, though not always. Your mortgage payment generally includes your property insurance payment and your private mortgage insurance (PMI) payment if applicable.

Property insurance is the insurance that covers your home in the event of a disaster like a fire, hurricane, tornado or even a burglary. It can include homeowners insurance as well as additional riders like flood and earthquake insurance.

Property insurance takes most of the risk from the homeowner and transfers it to the insurance company. So you’ll pay a little more each month, but you’ll pay a lot less in repair and replacement costs if disaster strikes.

Insurance payments work similarly to property tax payments. You’ll include them as part of your monthly mortgage payment even though they’re due only once a year. Your lender will hold the insurance money in escrow for you and pay it when the insurance company requires it.

5. Other Fees Included

Your mortgage payments may also include miscellaneous other fees, such as loan processing fees. These fees are likely to account for a minimal percentage of your overall monthly payment.

6. Private Mortgage Insurance (PMI)

If you make a down payment of less than 20% when you buy your home, your lender will likely require you to take out private mortgage insurance (PMI). Lenders use your down payment amount as a proxy to assess the risks associated with lending to you. Your PMI costs add a little to your mortgage payment each month.

Unlike property insurance, which protects you in case of a disaster, PMI protects your lender. It covers your lender if you become unable to make your monthly mortgage payments. If you miss payments, your PMI will kick in to cover the costs so your lending company doesn’t lose its investment. PMI will not protect you, however. If you fall behind on payments, you can still lose your home to foreclosure even though you have PMI coverage.

PMI is also important to many lenders because it enables them to sell loans to other investors. Having insurance backing minimizes these investors’ risk and makes them more willing to take on the loans.

PMI is relatively easy to remove from your mortgage payments after a while. Generally, once you’ve accumulated 20% home equity, you’ve convinced your lender of your fiscal reliability and can request to drop your PMI. Alternatively, you can sometimes stop your PMI at the midpoint of your amortization schedule — after the 20th year of a 40-year mortgage, for instance.

Additionally, once you pay off more of your loan, your mortgage insurance should drop automatically — usually once the balance reaches 78% or less of the original mortgage amount.

7. Homeowners Association (HOA) Fees

If you belong to an HOA, your mortgage payment sometimes includes HOA fees. These fees keep you in good standing with your HOA and, as with the lumped-in insurance and tax payments, offer convenience by minimizing the number of separate payments you must make.

Check out our mortgage calculators to help you better prepare for your loan.

Mortgage Payment Formula

The formula to calculate the monthly mortgage payment is:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1 ]

Where:

M = Monthly mortgage payment

P = Principal amount borrowed (the loan amount)

i = Monthly interest rate

n = Number of monthly payments (loan term in years multiplied by 12)

For example, let’s say you take out a $200,000 mortgage loan with a 4% annual interest rate and a 30-year loan term. To calculate the monthly mortgage payment:

P = $200,000

i = 4% / 12 = 0.003333 (monthly interest rate)

n = 30 x 12 = 360 (number of monthly payments)

M = $200,000 [0.003333(1 + 0.003333)^360] / [(1 + 0.003333)^360 – 1]

M = $954.83 (rounded to the nearest cent)

Therefore, your monthly mortgage payment would be $954.83. Note that this formula does not include taxes, insurance or any other additional fees that may be included in the monthly mortgage payment.

Mortgage vs. Loan

A mortgage is a type of loan that is specifically used to purchase a property, such as a home or a piece of land. The property serves as collateral for the loan, which means that if you don’t make the mortgage payments, the lender can foreclose on the property and sell it to recoup their losses.

On the other hand, a loan is a more general term that can refer to any type of borrowing, such as a personal loan, a car loan or a business loan.

The main differences between a mortgage and a loan are:

- Purpose: A mortgage is used to purchase a property, while a loan can be used for a variety of purposes.

- Collateral: A mortgage is secured by the property being purchased, while a loan may or may not require collateral.

- Repayment period: Mortgages typically have longer repayment periods than other types of loans, often spanning decades.

- Interest rates: Mortgage interest rates are typically lower than interest rates for other types of loans due to the fact that they are secured by the property being purchased.

Frequently Asked Questions About Mortgage Payments

Below are a few commonly asked questions about mortgage payments and how they work:

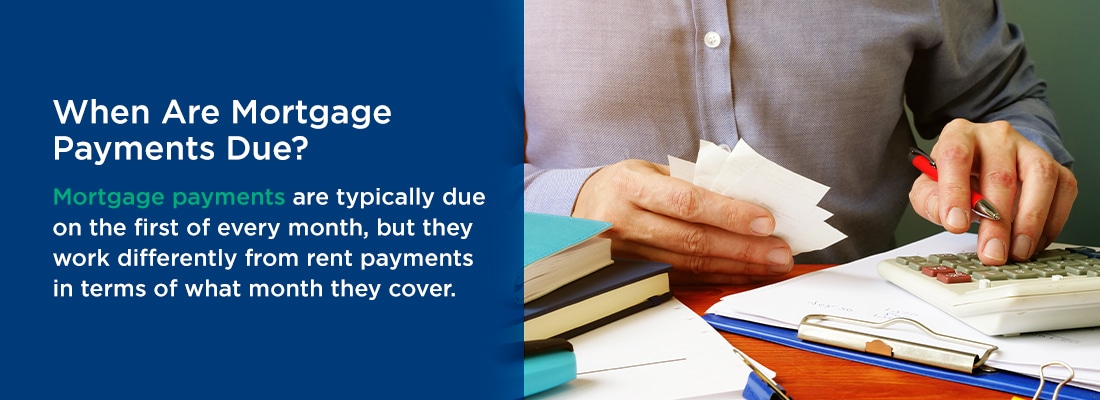

1. When Are Mortgage Payments Due?

Mortgage payments are typically due on the first of every month, but they work differently from rent payments in terms of what month they cover. With rent payments, you typically pay upfront, putting down money on the first of the month for the upcoming month. With mortgage payments, on the other hand, you generally pay in arrears — paying for the previous month instead of the upcoming one.

2. When Do Mortgage Payments Start?

When new homeowners close on a house, paying the closing fees as they do, they often wonder how soon their mortgage payments will kick in, hoping for a little breathing room.

And they typically get it. Because you pay in arrears, your first mortgage payment is usually due on the first day of the month after the month you closed. Say for example that you closed on your house on January 19. Your first mortgage payment would be due on March 1 and would cover February.

What about the interest due for January? That interest generally rolls into your closing costs. You’ll be able to see the exact amount in your closing disclosure forms, along with your interest rate, loan amount and monthly payments.

3. Do Mortgage Payments Go Down Over Time?

If you have a fixed-rate mortgage, your mortgage payments will not drop over time.

However, the amounts that comprise your loan do change over time due to your amortization schedule — the schedule of your payments. This schedule impacts how interest payments and principal payments are distributed. Generally, your initial mortgage payments favor your interest. You’ll be paying off more of your interest at first and less of the principal. Over time, as you pay down your home loan, your payments start to include more principal and less interest.

The result is that you pay down your interest faster than you pay down your principal. Why?

At the beginning of your loan, you naturally have a higher loan balance. So you owe more interest every month once you apply your interest rate to that loan balance. As time goes by and your loan balance decreases, you’ll owe less interest every month. So most of your payment will then go toward the principal, even though your total payment stays the same.

All that said, your mortgage payments may change slightly because of alterations in your insurance or tax rates. If your home’s value rises, for instance, your property taxes will likely rise as well, increasing your overall mortgage payment.

4. What Happens if I Make a Large Principal Payment on My Mortgage?

If you make a large payment on your mortgage, the extra payment goes toward paying down your principal. So in many cases, making a large payment is advantageous if you can afford it. It enables you to pay down your mortgage sooner and build equity faster.

And paying down the principal also helps you reduce your interest. The reason is that your lender calculates your interest from the amount of your principal. So if you lower your principal, you’ll lower your remaining interest as well.

With some mortgages, though, your lender will assess a prepayment penalty if you pay your mortgage down early. The prepayment penalty exists to compensate the lender for the interest it loses if you pay off your mortgage more quickly than expected. So you’ll probably want to sit down and do the calculations to figure out the best option for your finances. Determine whether your finances will benefit more if you pay your mortgage early and lower its overall cost or if you pay it slowly and steadily to avoid the prepayment penalties.

5. What Happens if I Miss a Mortgage Payment?

If you miss a mortgage payment, the penalties you’ll face depend on how late you were and how often you’ve missed payments in the past.

First Payment

Generally, the first time you miss a payment, you’ll receive a short grace period in which to get your payment up to date. That grace period is often about 15 days. Mortgage lenders need to receive their money — still, they understand that life happens, and they don’t want to penalize otherwise good, reliable clients. If you make your payment within that grace period, you probably won’t incur any penalties.

Second Payment

If you miss a second payment, or if the grace period goes by and you still haven’t made your first missed payment, you’ll start to feel the consequences. The first thing your lender will do if you miss mortgage payments or don’t pay within the allotted grace period is to impose a late fee. You’ll still be responsible for the missed payment, and you’ll have to pay a little extra as well. The late fee acts as a deterrent to discourage you from missing future payments. Depending on its policies, your lender may also report your delinquency to the credit bureaus. If your lender reports the late payment, you’ll take a hit to your credit score.

Once you miss two payments, your lender considers you to be in default on your mortgage. At this point, the lender is likely to become stricter and more forceful in its communications with you about making payments. However, most lenders don’t want to foreclose on a home unless they have no other options, so you can very likely still work out a payment deal at this point.

Third Payment

After three missed payments, you will receive a letter from your lender advising you that you have 30 days to make the missed payments, and then your lender will begin foreclosure proceedings. If you don’t make payments during that 30 days, foreclosure will start.

The upshot is that you’ll need to ensure you make your mortgage payments on time each month so you can stay in the home you love. Remember that your mortgage is a secured loan — your house and property make up the collateral to secure it. If you fail to make mortgage payments, you could lose your home to foreclosure.

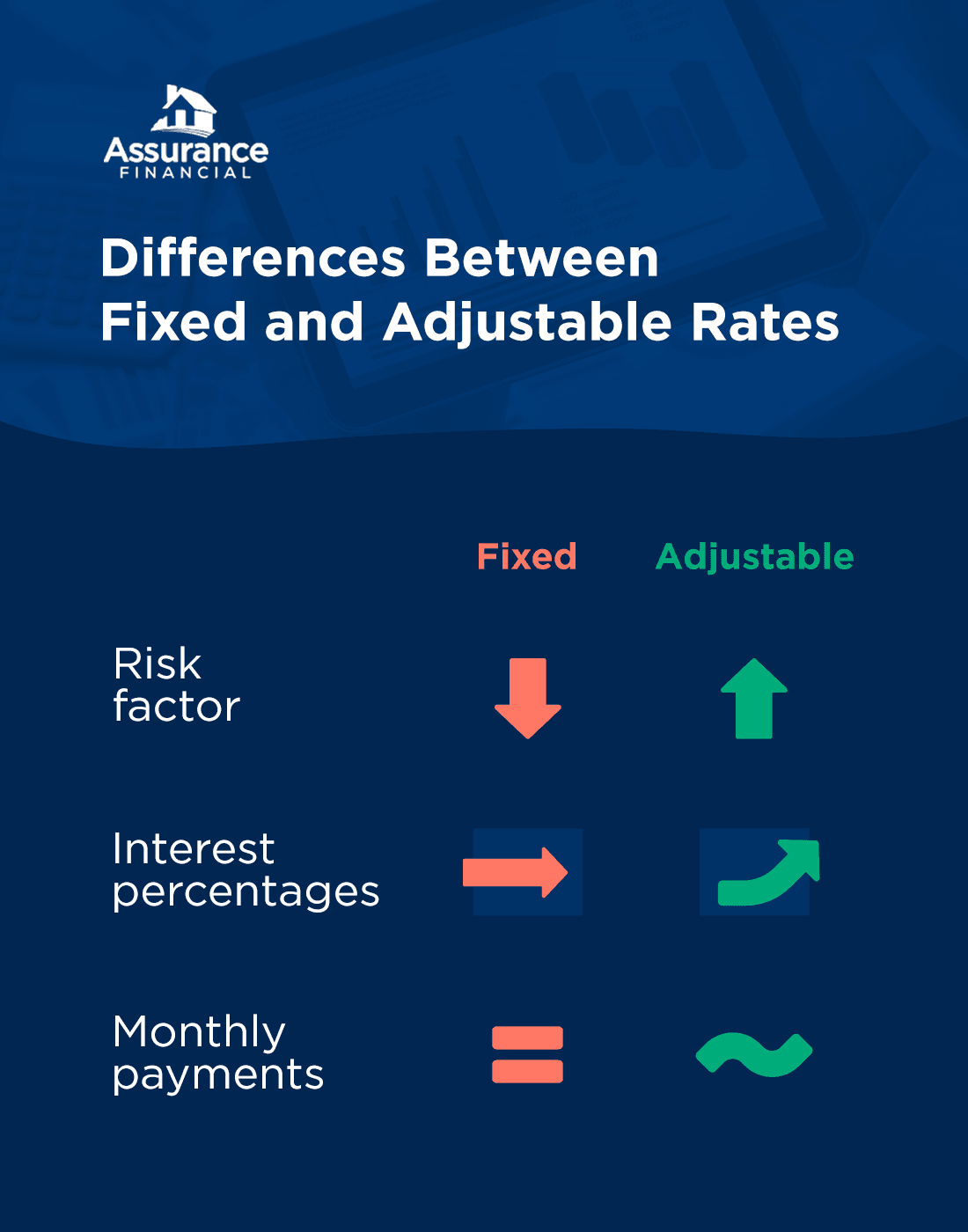

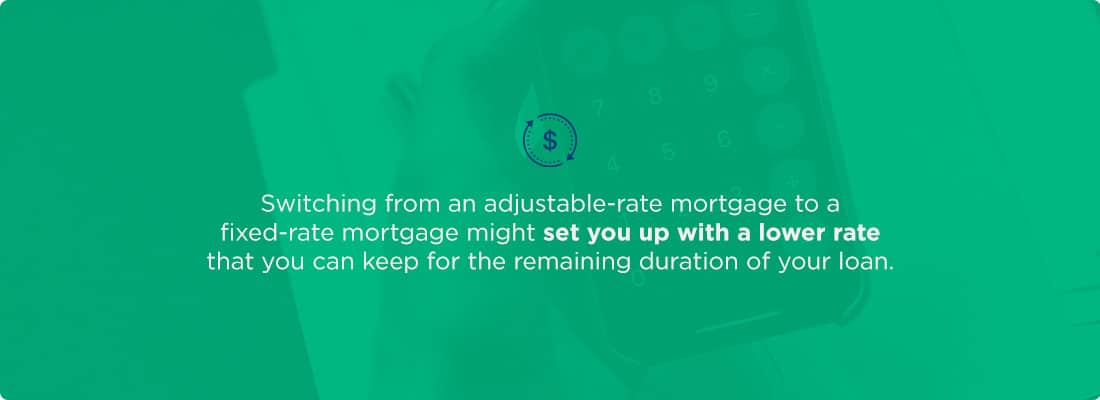

6. Can I Change My Mortgage Payment Amounts?

If you have a fixed-rate mortgage, you’d usually need to refinance your home to change your mortgage payment amounts.

Many homeowners refinance their homes at some point to lower their interest rates, increase or reduce the mortgage length, or reduce their monthly bills. Refinancing is a considerable undertaking since you’re applying for a mortgage all over again. Still, it is well worth the trouble in many scenarios.

To obtain changeable mortgage payments, you can also take out an adjustable-rate mortgage. If you have an adjustable-rate mortgage, your monthly payments will change often as your interest rates fluctuate.

With an adjustable-rate mortgage, the interest rate remains fixed for a determined time and then adjusts at predictable intervals — every five years, every year, even every month. At the end of the predetermined period, the interest rate adjusts to reflect the current market rate.

Adjustable-rate mortgages can be a risky gamble — you can’t be certain how your rates will change. If you feel confident that interest rates will drop over time, though, you might consider taking out an adjustable-rate mortgage to reap the benefits of market changes.

Apply for a Mortgage With Assurance Financial

When you’re ready to take the exciting step of purchasing a new home, work with Assurance Financial to take advantage of historically low rates.

We make it easy to apply for a mortgage and estimate costs during the process, and you can get pre-qualified in 15 minutes. Our licensed, approachable, trustworthy loan officers have the industry knowledge and expertise to get you custom competitive rates. And we have just about every type of home loan available, from conventional loans to FHA and VA loans to loans designed specifically for jumbo or modular homes.

Whether you’re a first-time homeowner, downsizing, dreamsizing or looking for an investment property or a vacation home, we can make getting started with your loan quick and convenient. And because we’re an independent lender rather than a mortgage broker, we give you the security and peace of mind of knowing we’ll never pass your loan or personal data on to anyone else.

Apply online, or contact us today for a no-obligation quote.

Sources:

- https://files.consumerfinance.gov/f/documents/cfpb_market-snapshot-first-time-homebuyers_report.pdf(4)

- https://assurancemortgage.com/everything-you-need-to-know-about-30-year-fixed-rate-mortgages/

- https://assurancemortgage.com/how-to-get-a-mortgage-loan/

- https://assurancemortgage.com/does-pre-approval-affect-credit-score/

- https://assurancemortgage.com/loan-application-process/

- https://assurancemortgage.com/what-is-down-payment-home-loan/

- https://assurancemortgage.com/what-are-closing-costs/

- https://assurancemortgage.com/what-is-a-mortgage-payment/

- https://fred.stlouisfed.org/graph/?g=NUh

- https://www.forbes.com/advisor/mortgages/mortgage-rates/

- https://www.forbes.com/advisor/mortgages/mortgage-interest-rates-forecast/

- https://www.consumerfinance.gov/ask-cfpb/when-can-i-remove-private-mortgage-insurance-pmi-from-my-loan-en-202/

- https://assurancemortgage.com/calculators/

- https://assurancemortgage.com/how-do-you-calculate-your-estimated-mortgage-payment/

- https://www.investopedia.com/ask/answers/081516/how-many-mortgage-payments-can-i-miss-foreclosure.asp

- https://assurancemortgage.com/refinance-your-home/

- https://assurancemortgage.com/purchase-your-home/

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/contact-us/

What Is a Home Equity Line of Credit?

Homeownership comes with a wide range of benefits. One significant advantage is that you can build equity as you pay off your mortgage over time. You can leverage home equity to access cash for major purchases, alternative debt repayment, retirement plans or home renovations. You can also use it to obtain funds via a second mortgage like a home equity line of credit, or HELOC.

When you obtain a HELOC, you are securing it against your home equity value. As such, lenders may offer lower rates compared to other personal loans. At Assurance Financial, we offer HELOCs to homeowners who qualify.

What Does HELOC Mortgage Mean?

A home equity line of credit is a revolving fund source you can obtain when you have equity in your home. Your home equity is the difference between your home’s value and your current mortgage balance. For example, if your home is worth $200,000 and your current mortgage balance is $150,000, your home equity would be $50,000.

There are a few ways to build equity in your home, including refinancing, renovating, paying down your mortgage and making a sizeable down payment. Your home’s value may also increase with an upward trend in the housing market.

If you own your home and have already paid off your mortgage, you may also be able to obtain a HELOC. In this case, the HELOC will be your primary mortgage rather than a second mortgage. Like a credit card, you can access this source of funds as needed. You may have several different ways to do so, such as by writing a check, making an online transfer or using a credit card associated with your account.

A HELOC mortgage may have few or no closing costs and usually comes with a variable interest rate, though you may be able to get a fixed rate for a few years. A HELOC is not the same as a home equity loan, which is cash that comes to you in a lump sum. Homeowners are more likely to opt for a home equity loan for a one-time purchase or expense like a major renovation.

What Can You Use a HELOC For?

HELOCs are versatile because you can use yours however you want without restrictions. The following are some of the expenses you can use a HELOC for.

- Educational costs: If you want to return to college to get a degree, you can use a HELOC to cover your college expenses.

- Emergency funds: You can also use a HELOC to cover emergency expenses, such as damage to your home not covered by insurance, a medical emergency or the loss of a vehicle.

- Debt consolidation: Credit card debt can quickly become overwhelming, costing thousands every year in interest alone. You can use a HELOC to consolidate and pay off your debt.

- Home improvements: You can leverage your home equity to make improvements, such as renovating your kitchen or installing new windows. Remodeling projects are among the most popular uses of a HELOC.

How Does a Home Equity Line of Credit Work on Your House?

With a HELOC, your home equity is collateral. As such, a lender may be able to offer competitive interest rates comparable to rates for first mortgages. A HELOC will likely have an adjustable interest rate that rises and falls with market conditions. Your lender begins with an index rate to set your interest rate, and depending on your credit, will then add a markup. The better your credit, the lower your markup is likely to be. Before you sign for a HELOC, be sure to ask about this amount.

If you are still paying off your first mortgage, your HELOC will be a second mortgage, which is any type of loan borrowed against your home’s equity. You can borrow funds against your credit line whenever you want, and if you do not use funds, you will not owe interest.

You can repay all or a portion of what you draw from your line of credit each month. When you pay off the balance, you will have access to your full credit line again. For example, if you have a $40,000 line of credit and you spend $5,000, you will need to repay that $5,000 before you can access the full amount of $40,000.

If your lender does not require minimum withdrawals, a HELOC can be a source of emergency funds. For example, if you lose your job, you can take out a HELOC for extra cash as long as you have equity in your property. Your lender will specify how many years you can withdraw from your credit line while only paying back interest and how many years you have to repay the principal and interest.

There are two phases of a home equity credit line, which we’ll explain below.

Draw Period

The first stage of a HELOC is the draw period. During this phase, you can access the credit available to you as needed. You typically only need to make interest payments in the draw period. However, if you choose, you can pay extra and apply it toward the principal. In some cases, you can ask for an extension after the draw period is over. If you do not want an extension, your HELOC will move into the next stage.

Repayment

The second phase of a HELOC is the repayment period. During this stage, you cannot access additional funds. You will also be making payments of principal and interest rather than interest-only. You will continue paying until you have repaid your balance. Repayment options during this phase vary from lender to lender. Remember, payments in this stage could be much higher than they were during the draw period, so be sure to create a repayment plan and include this expense in your budget.

Do You Have to Pay Back a HELOC?

Yes, as with other forms of debt, you have to pay back a HELOC. When you repay a portion of your principal, these funds will return to your home equity line of credit. You must pay off the rest of your principal and interest during the repayment period.

Can You Repay Your Debt Early?

If you’re already making regular payments, you may want to repay your debt more quickly to pay less total interest. During the draw period, you can opt to make principal payments, even if the agreement’s terms only require you to make interest payments.

Review your budget to determine how much you can put toward repaying your HELOC each month. If you are concerned about how much interest you’ll be paying, you may want to look for opportunities to make additional payments toward the principal and lower your overall monthly payments.

Is There a Prepayment Penalty?

Some lenders charge penalties for paying off a HELOC early. Whether you want to get ahead or you’re planning to sell or refinance your home, prepayment penalties can throw your plans for a loop if you’re not expecting the charge. Before you pay back your HELOC early, be sure to ask your lender about these penalties. Typically, small amounts beyond your required monthly payment will not incur a prepayment penalty, but you should carefully review your agreement and terms before moving forward.

What Are the Advantages of a HELOC?

If you qualify for a HELOC, there are a few reasons you may want to apply for this line of credit. The following are some of the advantages of a HELOC.

- Skip the fees: While credit cards tend to charge cash advance fees, you likely won’t have these when you draw funds from your HELOC. If a lender charges a fee every time you draw money, you may want to look for another lender.

- Improve your credit: Two factors that affect your credit score are your credit mix and payment history. You can increase your credit score by securing different types of credit — such as loans and credit cards — and making consistent, on-time payments. Obtaining a HELOC may boost your score if you steadily pay off the loan.

- Get a low interest rate: Even when mortgage interest rates are higher, a HELOC typically has a lower rate. HELOCs often come with adjustable interest rates, and though these can fluctuate, there are limits on how much the rate can rise while you have your loan.

- Pay lower initial costs: Similarly, HELOCs tend to come with lower initial costs than credit cards. That makes a HELOC ideal for ongoing projects or debt consolidation.

- Get a higher credit limit: You can likely get a much more generous credit line from a HELOC than from a credit card. Remember, the amount you can receive depends on the equity in your home and your credit score.

- Convert to a fixed rate: You may be able to convert your adjustable interest rate to a fixed rate, which can make your payment and interest rate more consistent and predictable. Though this may happen automatically when your HELOC enters the repayment phase, you may be able to convert it to a fixed rate earlier.

- Pay low or no closing costs: While you likely have to pay closing costs for your first mortgage, when you get a HELOC, you may not have to pay any at all if you have good credit. Any required closing or appraisal costs are likely to be low.

- Borrow the funds you need: With a HELOC, you’ll use the funds you need when you need them. You can borrow cash as you go, and if you eventually need less than you anticipated, you will pay a lower monthly payment. This flexibility is one significant advantage for borrowers who apply for a HELOC.

- Use the funds as you see fit: A HELOC imposes few restrictions on how borrowers can use the loan. Though many homeowners renovate or update their properties, you don’t have to. You can put the money toward various expenses, such as travel, higher education or debt consolidation.

- Deduct interest on your taxes: According to the IRS, you can deduct interest payments if you use your HELOC to substantially improve, build or buy the home that secures your loan. There is a limit on how much you can deduct, combined with the interest on your first mortgage.

- Enjoy flexible options for repayment: Many HELOCs come with flexible repayment options, including the timeline and interest-only payments versus payments that include principal and interest. Your timeline for repayment can vary depending on your lender and the amount you borrow. You can likely make additional payments to lower your remaining balance.

What Are the Disadvantages of Home Equity Lines of Credit?

While there are many advantages to securing a HELOC, you may want to consider some drawbacks before you apply.

- Fees: While lenders make money from the interest you pay, you may also owe some fees, such as an annual fee, transaction fee, appraisal fee or a fee if you refinance or cancel your HELOC before the end of the draw period. Some lenders may also charge fees if you do not borrow a specific amount or maintain a given loan balance. Be sure to review these fees before moving forward with a HELOC.

- Upfront costs: Some lenders charge upfront costs to get a HELOC, such as an application fee, home appraisal, title search and real estate attorney fees. Consider these to determine whether a HELOC is the right option for you.

- Loss of equity: With a HELOC, you borrow against your home equity. If your home’s value drops with a dip in the housing market, you could owe more than your property is worth. When you have an outstanding HELOC, you may also be ineligible for other opportunities to borrow against your home’s equity.

- Payment increase: While the low payment during the draw period can be tempting, your minimum monthly payment will increase in your repayment period to include principal and interest. To avoid an unwelcome surprise, plan for your monthly payment to go from a small sum to hundreds of dollars.

- Limited draw period: Every HELOC has a draw period, which is the only time you can draw funds. After this phase, you will need to repay your HELOC.

- Variable interest rate: A HELOC often comes with a variable rate, so it can rise or fall depending on the market. Even if the HELOC has a low interest rate when you obtain it, that could go up when your HELOC enters the repayment period.

- Risk of overspending: Though overspending is not an inherent disadvantage of HELOCs themselves, you should be aware of the risk. Since you only need to make interest-only payments in the draw period, you can easily access more cash than needed, which could lead to financial ramifications.

- Minimum withdrawals: Some HELOCs may come with minimum withdrawal requirements, which means you’ll need to borrow a specific amount and keep your credit line open for a given period.

- Use of your home as collateral: Since you are using your home as collateral, you risk losing the house if you can’t repay your HELOC. That’s why it’s wise to only use a HELOC to increase your emergency funds or cover expenses that can help you accumulate wealth, such as home renovations and improvements.

If your income is not stable and you can’t make your monthly payments, a HELOC may not be the right option for you. Additionally, if you aren’t looking to borrow a large amount of money, you may want to opt for a low-interest credit card instead.

How Do I Get an Equity Line of Credit?

Once you’ve decided you want to obtain a HELOC, begin the application process. Follow the steps below to get an equity line of credit.

- Ensure you have sufficient home equity: Use a HELOC calculator or discuss your situation with our team at Assurance Financial to determine whether you have enough equity in your home to qualify for a HELOC.

- Review your credit score: You may be more likely to get approved for a HELOC and qualify for a better interest rate if you have a higher credit score. If you want to improve your credit score before you apply, you can plan to pay off some of your debts and make on-time payments. You can also review your credit report to ensure there are no errors you need to dispute.

- Speak to several lenders: Shop around at several lenders to make sure you can get the best terms and rate. Research lenders and ask about pre-qualification offers that may be available to you. At Assurance Financial, we offer historically low rates.

- Collect your application materials: Once you find your lender, you will need to provide your application materials — such as your identification, employment and salary information — plus your estimated home value and your outstanding mortgage balance.

- Provide verification documents: After you accept a HELOC offer, you will need documentation to verify the information you have provided. This paperwork may include tax returns, W-2s or pay stubs. The lender may also require an appraisal for your home and will complete a hard credit check, which will temporarily affect your credit score.

- Wait through the underwriting process: As with your first mortgage, you will have to wait for the underwriting process. For a HELOC, the underwriting is less extensive.

- Receive your funds: Finally, you will sign your paperwork and receive your money, which you can then start drawing from. The amount of time between approval and funds disbursement will depend on your lender.

Apply for a HELOC Loan With Assurance Financial Today

When you apply for a HELOC loan with Assurance Financial, we only need your asset information, proof of income, two most recent tax returns, proof of identification and credit score. We can review your application faster when you use our secure bank connector, and you can take a simple snapshot of a pay stub as proof of income. On the other hand, if your employer uses ADP, all you’ll need is your payroll login.

Contact us at Assurance Financial if you want to learn more about getting a HELOC or apply for a HELOC loan with Abby, our virtual assistant that can help guide you through the loan process.

Potential homebuyers, especially first-time homebuyers, often wonder how much money they should save to purchase a home. There are a number of costs associated with the process, including a down payment and closing costs. Fortunately, 100% financing options are available for home loans that may allow you to purchase a home with no money down. If you are looking for a home loan with 100% financing, meaning a home loan that doesn’t require a down payment, we cover what you need to know.

What Is a 100% Financing Home Loan?

A 100% financing home loan is a type of mortgage loan that allows you to finance the entire purchase price of a home without making a down payment. With this type of loan, you don’t need to put any money down, which can make it easier for you to purchase a home if you do not have a large amount of savings or want to keep your savings for other purposes.

There are a few different types of 100% financing home loans available, including United States Department of Agriculture (USDA) loans and Veterans Affairs (VA) loans. These loans are backed by the government and are designed to help make homeownership more affordable and accessible to a wider range of people.

While a 100% financing home loan may appeal to some borrowers, this option may also come with higher interest rates and fees. Carefully consider your options and work with a reputable lender to ensure you are getting the fairest loan terms possible.

What Options Are Available for No Money Down Home Loans?

There are two government-backed home loan options that do not require a down payment — a USDA loan and a VA loan.

USDA Home Loan

This type of mortgage loan is guaranteed by the United States Department of Agriculture (USDA). A USDA home loan is designed to help low- to moderate-income borrowers in rural areas purchase a home or make home repairs. USDA loans typically offer favorable terms, including low-interest rates and zero down payment requirements. They are also available to borrowers with lower credit scores than other types of loans.

To qualify for a USDA loan, the property you plan to purchase or renovate may need to be located in a designated rural or suburban area as defined by the USDA. Additionally, you may need to meet certain income limits based on the area you are buying in and your household size. USDA loans are administered by approved lenders, and since the USDA guarantees these loans, lenders are protected from losses if you default on your loan.

VA Home Loan

This type of mortgage loan is guaranteed by the U.S. Department of Veterans Affairs (VA). A VA loan is designed to help current and former members of the U.S. military and their qualifying surviving spouses buy or refinance a home. VA loans typically offer favorable terms, such as no down payment requirement and no private mortgage insurance requirements, making them an attractive option for eligible borrowers.

To qualify for a VA loan, you may need to obtain a Certificate of Eligibility (COE) from the VA. The COE verifies that you meet the VA’s service requirements and are eligible for the loan. Like USDA loans, VA loans are administered by approved lenders, and the guarantee from the VA protects lenders from losses if you default on the loan.

Benefits of 100% Financing for Home Loans

Receiving 100% financing for home loans, also known as zero-down payment loans, can offer you several benefits. The following are some of the potential benefits:

- Increased flexibility: If you have saved up a down payment, you can use these funds for other expenses, such as home renovations, moving costs or emergency expenses.

- No down payment required: With 100% financing, you are not required to come up with a large down payment to purchase a home, which can be a significant financial burden.

- Faster path to homeownership: With 100% financing, you can achieve your dream of homeownership sooner.

- Affordable monthly payments: With no down payment, the loan amount is higher, but the monthly payments may still be manageable, especially with competitive interest rates.

100% financing may not be available for all types of home loans, and we recommend that you carefully consider the terms and conditions of any loan before making a decision. Additionally, you may be required to have strong credit scores and income to qualify for this type of loan.

How to Buy a House With No Money Down

Buying a house with no money down is possible, but it may require careful planning and a good understanding of your options. The following are some potential ways you can buy a house with no money down:

- Gift funds: If you have friends or family who are willing to help you purchase a home, they can give you a monetary gift that you can use as a down payment.

- Negotiate with the seller: In some cases, you may be able to negotiate with the seller to cover some or all of the down payment as part of the sale agreement.

- Apply for a VA loan or USDA loan: If you are a current or former member of the U.S. military or a qualifying surviving spouse, you may be eligible for a VA loan, which requires no down payment. If you are looking to buy a home in a rural area, you may be eligible for a USDA loan, which also requires no down payment.

- Down payment assistance programs: Some state and local governments offer down payment assistance programs to help you buy a home with little or no down payment if you are a low- to moderate-income earner.

Keep in mind that even if you are able to buy a house with no money down, you may still be responsible for other costs associated with the home purchase, such as closing costs and appraisal fees. Carefully consider all of your options and speak with a qualified mortgage professional to help you navigate the homebuying process.

What if I Don’t Qualify for 100% Financing for a Home Loan?

If you don’t qualify for 100% financing for a home loan, you may have some other options, such as applying for a conventional loan, applying for an FHA loan, applying for down payment assistance, applying for closing cost assistance or saving for a down payment.

Apply for a Conventional Loan

This type of mortgage loan is not guaranteed or insured by a government agency like the U.S. Department of Veterans Affairs (VA) or the Federal Housing Administration (FHA). Conventional loans are backed instead by private lenders and investors. Typically, conventional loans come with stricter credit and income requirements than government-backed loans. They are often a good option for borrowers who have good credit scores and sufficient income to qualify for a loan.

Conventional loans can be conforming or nonconforming. Conforming loans are those that meet the guidelines set by Fannie Mae and Freddie Mac, the two government-sponsored enterprises that buy and sell mortgage loans. Nonconforming loans, also known as jumbo loans, exceed the conforming loan limits set by Fannie Mae and Freddie Mac.

Conventional loans typically require a down payment of at least 3% of the purchase price, although some lenders may want a larger down payment depending on your credit score and other factors. You may also be required to pay private mortgage insurance (PMI) if you make a down payment of less than 20%. Conventional loans are a popular option for homebuyers who meet the credit and income requirements and want to avoid the mortgage insurance requirements of government-backed loans.

Apply for an FHA Loan

This type of mortgage loan is backed by the Federal Housing Administration (FHA), a government agency that belongs to the Department of Housing and Urban Development (HUD). An FHA loan is designed to help lower-income and first-time homebuyers who may have difficulty qualifying for a conventional mortgage loan. The FHA insures the loan, which means that if you default on the loan, the lender is protected against losses.

FHA loans typically have more lenient credit and income requirements than conventional loans, and they may require a lower down payment. The down payment for an FHA loan can be as low as 3.5% of the purchase price, although you may be required to make a down payment of at least 10% if your credit score is lower than 580.

One of the key benefits of an FHA loan is that it allows you to qualify for a loan with a lower credit score than would typically be required for a conventional loan. Additionally, FHA loans may offer lower interest rates and more flexible repayment terms than conventional loans. However, FHA loans may also require you to pay an upfront mortgage insurance premium (MIP), as well as an annual MIP that is added to the monthly mortgage payment. The MIP is used to fund the FHA loan program and protect lenders against losses.

Apply for Down Payment Assistance

Down payment assistance (DPA) is a type of financial assistance that is designed to help homebuyers cover the upfront costs associated with purchasing a home, specifically the down payment and closing costs. Down payment assistance programs are often administered by state and local housing agencies and nonprofit organizations.

Down payment assistance can take many forms, such as grants, loans or forgivable loans. The funds can be used to cover all or a portion of the down payment and closing costs, depending on the program’s guidelines and your qualifications. DPA programs are typically targeted at low-income homebuyers and first-time homebuyers who may struggle to save for a down payment. They can also be available to certain groups, such as first-time homebuyers, veterans or teachers.

The goal of down payment assistance is to make homeownership more accessible and affordable to a wider range of people. By reducing the upfront costs of buying a home, DPA programs can help you get into a home faster and with less financial strain. Down payment assistance programs may have specific requirements and qualifications that you may need to meet to be eligible. Carefully review the guidelines of any DPA program you are considering to ensure that you meet the qualifications and understand the terms of the assistance.

Apply for Closing Cost Assistance

Closing cost assistance is a type of financial assistance that can help you cover the closing costs associated with purchasing a home. Closing costs are expenses that are incurred during the homebuying process, such as lender fees, appraisal fees and title fees. Closing cost assistance programs are often administered by state and local housing agencies and nonprofit organizations. The assistance can be used to cover some or all of the closing costs.

Closing cost assistance is typically targeted at low- to moderate-income homebuyers who may struggle to cover the upfront costs of buying a home to make homeownership more accessible and affordable. Check if there are any closing cost assistance programs available in your area.

Save for a Down Payment

Trying to save for a down payment on a home can be a significant challenge, especially if you’re starting from scratch. However, there are several strategies that can help you save money more effectively and reach your down payment goal faster, such as:

- Reduce debt: Pay off high-interest debt, such as credit cards, as quickly as possible. This will free up more money for savings.

- Create a budget: Make a budget that takes into account your income and expenses and look for areas where you can cut back on spending. Consider reducing discretionary expenses like eating out, entertainment and subscriptions.

- Set a savings goal: Determine how much you need to save for a down payment and set a specific savings goal. This will help you track your progress and stay motivated.

- Consider a side hustle: Look for ways to earn extra income, such as freelancing, tutoring or selling items you no longer need. Put this extra income directly into your down payment savings account.

- Automate your savings: Set up automatic transfers from your checking account to a savings account each month. This will help you save money consistently and avoid the temptation to spend it elsewhere.

Saving for a down payment can take time and discipline, but if you don’t qualify for 100% financing, this can be an important step toward achieving homeownership.

Where to Start

Every homebuyer has different needs, which is why we offer so many different home loan options at Assurance Financial. We can help regardless of your life stage or homebuying goal, whether you are:

- First-time homebuyers.

- Vacation homebuyers.

- Experienced homebuyers.

- Self-employed homebuyers.

We can also assist if you’re downsizing your home, remodeling or building a home, or investing in real estate. Use a 100% financing mortgage calculator to determine how this mortgage may impact your finances.

Apply for a Loan Today With Assurance Financial

At Assurance Financial, we have been servicing the loan industry since 2001. We combine superior customer service with technology-focused solutions to bring you the most seamless homebuying experience possible. We handle the entire home loan process in-house, so you can rest assured that the process will go smoothly. If you are seeking 100% financing for a conventional loan or another type of home loan, apply for a loan with us at Assurance Financial today.

Key Takeaways

- Fannie Mae (established 1938, now shareholder-owned) primarily focuses on conventional conforming loans plus FHA and VA loans, while Freddie Mac (created 1970, government-owned) also emphasizes multifamily loans for properties with 5+ units.

- Fannie Mae faces more restrictive regulatory capital requirements and higher affordable housing goal targets, while Freddie Mac has less restrictive capital requirements.

- Both entities purchase mortgages from lenders and securitize them, though their market share has declined since the 2008 financial crisis.

Fannie Mae and Freddie Mac are two government-sponsored entities (GSEs) that play a significant role in the United States housing market by providing liquidity to the mortgage market. Over the years, there has been a lot of debate about the roles and responsibilities of these two entities.

Below, we will explore the differences between Freddie vs. Fannie and how to determine which may be right for you.

What Is Fannie Mae and Freddie Mac?

Below, we cover more about Fannie Mae and Freddie Mac.

What Is Fannie Mae?

Fannie Mae is a GSE that was established by Congress in 1938. Its purpose is to provide liquidity and stability to the housing market by buying mortgages from home loan lenders and securitizing them into mortgage-backed securities (MBS) that are sold to investors.

By purchasing mortgages from lenders, Fannie Mae helps to ensure that there is a steady supply of mortgage funds available to homebuyers. The securitization of these mortgages into MBS also helps to spread risk across a broad range of investors, which helps to make the housing finance system more resilient.

Fannie Mae is not a direct lender, but it does set underwriting guidelines and works with lenders to ensure that the loans they originate meet those guidelines. Fannie Mae is regulated by the Federal Housing Finance Agency (FHFA) and is one of two GSEs, the other being Freddie Mac.

What Is Freddie Mac?

Freddie Mac is a GSE that was created by Congress in 1970. Like Fannie Mae, its primary mission is to help make the housing market more stable. Like Fannie Mae, Freddie Mac is regulated by the FHFA.

Freddie Mac works with a network of lenders across the country to purchase conventional mortgages and package them into securities that are sold to investors. By doing so, Freddie Mac helps to ensure that there is a steady flow of funds available for mortgage lending, which in turn helps to keep interest rates stable and affordable for homebuyers.

Freddie Mac also plays a role in setting underwriting standards for the loans it purchases, working with lenders to help ensure that the loans they originate meet those standards. In addition, Freddie Mac has a mandate to support affordable housing and community development initiatives, which it does through various programs and partnerships.

What Does Fannie Mae and Freddie Mac Stand For?

Fannie Mae stands for the Federal National Mortgage Association. Freddie Mac, on the other hand, stands for the Federal Home Loan Mortgage Corporation.

Both Fannie Mae and Freddie Mac are publicly traded companies, but they are also under the conservatorship of the federal government, which means that the government has taken control of their operations to stabilize and strengthen them.

Are Fannie Mae and Freddie Mac the Same?

Fannie Mae and Freddie Mac are two separate entities, but they have a similar business model and operate in the same industry. Both entities were created to provide liquidity to the U.S. mortgage market by purchasing mortgages from lenders, pooling them together and then selling them as mortgage-backed securities to investors.

While their missions and structures are similar, there are some differences between Fannie Mae and Freddie Mac. Despite these differences, both Fannie Mae and Freddie Mac have played a significant role in the U.S. housing market, and their actions have had a significant impact on the availability and cost of home loans for American borrowers.

How Do I Know if My Mortgage Is Fannie Mae or Freddie Mac?

If you want to find out if your mortgage is owned or backed by Fannie Mae or Freddie Mac, you can follow these steps:

- Find your mortgage statement or payment book.

- Look for the name of the company that services your mortgage. This is the company that collects your mortgage payments and handles your account.

- Visit the Fannie Mae Loan Lookup tool or the Freddie Mac Loan Look-Up tool on their respective websites.

- Enter your personal information, such as your name, address and the last four digits of your Social Security number to verify your identity.

- Follow the instructions to see if your mortgage is owned or backed by Fannie Mae or Freddie Mac.

If your mortgage is owned or backed by Fannie Mae or Freddie Mac, you may be eligible for certain benefits or programs, such as loan modifications or refinancing options, so it’s important to know which entity holds your mortgage.

What Is the Difference Between Fannie Mae and Freddie Mac?

While Fannie Mae and Freddie Mac have similar business models and operate in the same industry, there are some key differences between the two entities:

1. History and Mission

Fannie Mae and Freddie Mac have similar histories and missions, as both were established by Congress as GSEs to provide liquidity and stability to the U.S. housing market. However, there are some differences in their histories and missions.

Fannie Mae was established in 1938 as part of President Franklin D. Roosevelt’s New Deal to help create more affordable housing options for Americans. The organization was originally a part of the government but was later privatized in 1968.

Freddie Mac, on the other hand, was established in 1970 to provide competition to Fannie Mae and increase liquidity in the mortgage market. Freddie Mac’s mission is similar to Fannie Mae’s in that it buys mortgages from different lenders and securitizes them into MBS, but it also focuses on supporting smaller banks and thrifts that may not have access to the same resources as larger lenders.

Another difference between Fannie Mae and Freddie Mac is their ownership structure. Fannie Mae was privatized in 1968 and is owned by shareholders, while Freddie Mac is still owned by the federal government.

2. Market Share

Fannie Mae and Freddie Mac have historically had similar market shares in the U.S. housing finance system. However, there have been some differences in their market shares over time.

In the years leading up to the financial crisis of 2008, Fannie Mae and Freddie Mac held a dominant position in the U.S. mortgage market. However, after the financial crisis, the government took over both companies and implemented changes to their operations to reduce their risk to taxpayers. As a result, their market share has since declined.

Fannie Mae and Freddie Mac still play a significant role in the U.S. housing market, but their market share has decreased. This is due in part to the growth of non-bank lenders and other private sector entities that have entered the mortgage market in recent years.

While Fannie Mae and Freddie Mac have similar market shares, there are some differences in the types of loans they purchase and securitize.

3. Mortgage Types

Fannie Mae and Freddie Mac both purchase and securitize various types of mortgage loans, but there are some differences in the types of loans they focus on.

Fannie Mae’s main focus is on conventional, conforming loans. These are loans that meet Fannie Mae’s underwriting and eligibility standards and conform to loan limits set by the FHFA. Fannie Mae’s loan limits vary by geographic location and are adjusted annually to reflect changes in housing prices. Fannie Mae also purchases loans that are insured by the FHA or guaranteed by the Department of Veterans Affairs (VA).

Freddie Mac also purchases conventional, conforming loans, but it has a stronger focus on multifamily loans. Multifamily loans are loans that are used to finance properties with five or more units, such as apartment buildings. Freddie Mac is the leading source of financing for multifamily properties in the U.S. and has specific loan products tailored to the needs of multifamily borrowers. Freddie Mac also purchases loans that are insured by the FHA or guaranteed by the VA.

4. Regulatory Oversight

Fannie Mae and Freddie Mac are both regulated by the FHFA, but there are some differences in their regulatory oversight.

The FHFA was established in 2008 as part of the Housing and Economic Recovery Act (HERA) in response to the financial crisis, with the primary responsibility of overseeing Fannie Mae, Freddie Mac and the Federal Home Loan Banks (FHLBs).

One key difference in regulatory oversight is that Fannie Mae is subject to more restrictive regulatory capital requirements than Freddie Mac. This means that Fannie Mae must hold more capital on its balance sheet to protect against losses than Freddie Mac does. Fannie Mae has historically had a larger portfolio of mortgage assets than Freddie Mac.

Another difference is that Fannie Mae is subject to a higher affordable housing goals target than Freddie Mac. As part of their mission to support affordable housing, both Fannie Mae and Freddie Mac are required to meet certain goals for the percentage of their business that is dedicated to serving low- and moderate-income families. However, Fannie Mae’s affordable housing goals are generally higher than Freddie Mac’s.

Both Fannie Mae and Freddie Mac are subject to significant regulatory oversight by the FHFA to ensure their safety and soundness and their ability to fulfill their mission of providing liquidity and stability to the U.S. housing market.

5. Ownership

Fannie Mae and Freddie Mac are both publicly traded companies, but there are some differences in their ownership structures.

Fannie Mae was originally established as a GSE and owned by private shareholders until it was placed into conservatorship by the U.S. government. Since then, Fannie Mae has been under the control of the FHFA, which serves as its conservator. The U.S. Treasury also holds senior preferred stock in Fannie Mae, which provides a source of funding for the company.

Freddie Mac was also originally established as a GSE and was owned by private shareholders until it was placed into conservatorship by the U.S. government. Since then, Freddie Mac has also been under the control of the FHFA as its conservator, and the U.S. Treasury holds senior preferred stock in the company.

While Fannie Mae and Freddie Mac are both publicly traded companies, their ownership structures are different from those of typical publicly traded companies. As GSEs, Fannie Mae and Freddie Mac were created by Congress to fulfill a specific public purpose and their operations are subject to significant regulatory oversight by the FHFA and other federal agencies.

Similarities Between Fannie Mae and Freddie Mac

Fannie Mae and Freddie Mac share many similarities, as they both operate in the same industry and have similar missions and business models.

- Business model: Both entities were created to provide liquidity to the U.S. mortgage market through the same process.

- Government-sponsored: Fannie Mae and Freddie Mac are both GSEs that operate in the private sector but have a public mission.

- Loan limits: Both entities have loan limits that determine the maximum amount of money that can be borrowed for a mortgage. These loan limits are set by the FHFA and are adjusted annually based on changes in home prices.

- Role in the housing market: Fannie Mae and Freddie Mac both play a significant role in the housing market by providing liquidity and stability to the mortgage market, which in turn helps to increase homeownership rates and provide affordable housing options.

- Impact on borrowers: The actions of Fannie Mae and Freddie Mac have a significant impact on borrowers, as they influence the availability and cost of home loans. Borrowers who obtain mortgages backed by Fannie Mae or Freddie Mac may be eligible for certain benefits or programs.

Which Is Best For You?

Whether Fannie Mae or Freddie Mac is best for you depends on various factors, such as your financial situation, the type of mortgage you need and your eligibility for certain programs or benefits.

Keep in mind that Fannie Mae and Freddie Mac are not lenders themselves — they are companies that purchase mortgages from home loan lenders and then sell them as mortgage-backed securities to investors. So, ultimately, the decision of which lender to use will depend on your individual needs and preferences.

Here are some things to consider when deciding between Fannie Mae and Freddie Mac:

- Mortgage type: If you need a conventional mortgage, either Fannie Mae or Freddie Mac could be a good choice. However, if you need a government-backed mortgage, such as an FHA or VA loan, you will need to look elsewhere.

- Loan limits: Fannie Mae and Freddie Mac have different loan limits, so you may want to check which entity offers loan limits that are most suitable for your needs.

- Eligibility for programs: If you are having trouble making your mortgage payments, you may be eligible for certain programs or benefits through Fannie Mae or Freddie Mac. However, the eligibility requirements and programs offered may differ between the two entities, so it’s important to check with both.

- Interest rates: Interest rates can vary between lenders and can change frequently, so it’s important to shop around and compare rates from different lenders, including those who sell mortgages to Fannie Mae or Freddie Mac.

Ultimately, it’s best to do your research and compare your options to find the best lender and mortgage product for your individual needs and financial situation.

What to Consider When Applying for a Mortgage

When applying for a mortgage, here are some factors to consider:

- Interest rates: The interest rate is one of the most important factors when choosing a mortgage lender. You’ll want to compare rates from different lenders to ensure you’re getting the best deal.

- Fees: Lenders may charge fees for origination, processing and other services. Ask about these fees upfront and compare them with other lenders.

- Customer service: Good customer service is important, especially when dealing with a complex financial transaction like a mortgage. You’ll want to choose a lender that is responsive and communicative throughout the loan process.

- Mortgage products: Different lenders may offer different types of mortgages, such as fixed-rate or adjustable-rate mortgages. You’ll want to choose a lender that offers the type of mortgage that best fits your needs.

- Reputation: Look for a lender with a good reputation in the industry. You can check online reviews and ratings from other borrowers, as well as the lender’s track record and history.

Keep in mind that every borrower’s situation is unique and what’s most important to you may differ from someone else. Do your research and compare your options to find the best mortgage lender for your individual needs.

Apply for a Mortgage From Assurance Financial

Below are some advantages of getting a mortgage from a reputable lender like Assurance Financial:

- Competitive rates: We offer competitive interest rates that can save you money over the life of your mortgage.

- Loan options: We offer a variety of loan options, such as conventional, FHA, VA and jumbo loans, that can be tailored to your specific needs.

- Expertise: We have experienced loan officers who can guide you through the mortgage process and help you find the best loan for your needs.

- Flexibility: We will be flexible in working with you to find a solution that fits your unique financial situation.

- Customer service: We prioritize excellent customer service, providing clear communication and support throughout the mortgage process.

- Streamlined process: We have a streamlined process for mortgage applications and approvals, saving you time and hassle.

Contact us at Assurance Financial to learn more about Freddie Mac vs. Fannie Mae or apply for a mortgage with us today.

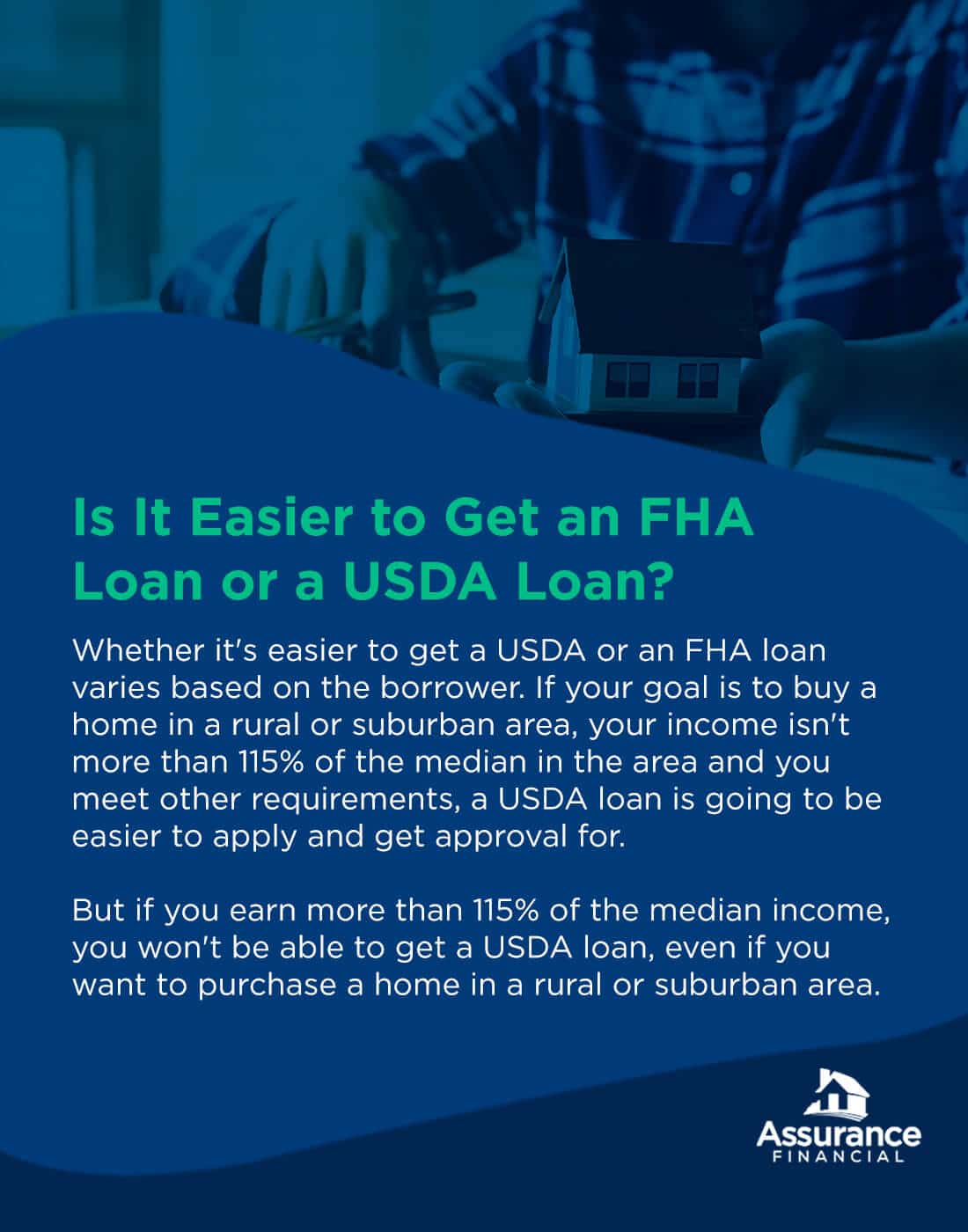

Several government loan programs exist to help buyers take one step closer to the American dream of homeownership. If you’re considering buying a home and don’t think you’ll qualify for a conventional mortgage, a Federal Housing Administration (FHA) loan or a United States Department of Agriculture (USDA) loan might be right for you.

While the FHA loan program and the USDA loan program have some similarities, they ultimately have slightly different goals and different requirements. Generally speaking, USDA loans have more restrictions than FHA loans. Your income and where you want to live can influence whether an FHA or USDA loan is the right choice for you.

What Is an FHA Loan?

An FHA loan is a type of mortgage for new buyers in the United States. The FHA is part of the U.S. Department of Housing and Urban Development (HUD). It guarantees or insures the FHA loan program.

FHA loans don’t come directly from the government. Instead, they are from private lenders. The lenders have the FHA’s guarantee that it will step in and cover the cost of the loan if the borrower is unable to pay or stops making payments.

Since private lenders have insurance from the FHA, they are more likely to lend money to people who wouldn’t qualify for a conventional mortgage. FHA loans are therefore available to buyers with low credit scores and those who can’t make a down payment of 10% or more.

FHA Loan Term and Interest

FHA lenders generally offer a 15- or 30-year term. Borrowers can repay the loan early by making larger or more frequent installments than the minimum requirement.

An FHA may have a fixed interest rate, meaning it will stay the same throughout the term. Conversely, an FHA may also have a variable interest rate.

FHA Down Payments and Insurance

You must put at least 3.5% of the purchase price down when you finance your home purchase via an FHA loan if your credit score is 580 or higher. The minimum down payment is 10% for buyers with a 500-579 credit score.

In exchange for financial flexibility, the FHA requires borrowers to take out a two-part mortgage insurance policy. Part one is an upfront expense equal to 1.75% of the loan. Part two is an annual fee that varies based on the size of your down payment, the loan term and the amount of the loan. You can pay the second part once per year or divide the annual balance over 12 months. A smaller down payment results in a larger mortgage insurance premium.

The size of your down payment also affects how long you need to maintain the mortgage policy. The mortgage insurance policy remains in place throughout the loan’s term when you put less than 10% down. If you put down 10% or more, you can eliminate the premium after 11 years of consistent payment.

What Is a USDA Loan?

USDA loans, also known as Rural Development loans, make homeownership affordable and provide affordable housing in rural and some suburban areas. You can’t apply for a USDA loan if you want to purchase property in the middle of a big city or metropolitan area.

USDA Down Payments and Other Features

You don’t have to make a down payment if you qualify for a USDA loan. You will have to pay a funding fee, which acts as insurance. The amount of the fee can vary but can’t be more than 3.5% upfront and 0.5% of the average annual unpaid balance monthly.

USDA loan borrowers need to meet income requirements, which vary based on the part of the country where they want to purchase a home.

USDA loans have 30-year terms and fixed interest rates, which are set by the lender.

Types of USDA Loans

The USDA supports two types of loans.

Single Family Direct Loans are issued by the USDA. They are designed for borrowers with a low or very low income who want to purchase a home in a rural area. The loans have up to 33-year terms — and up to 38 years for very-low-income individuals — no down payment required and financial assistance for borrowers. As of 2022, Single Family Direct Loans have a fixed interest rate of 2.5%.

The other USDA loan program, the Single Family Housing Guaranteed Loan program, has some features in common with FHA loans. It’s guaranteed by the USDA and issued by approved, private lenders. Lenders who participate in the USDA loan program can have up to 90% of the loan amount insured by the USDA.

USDA vs. FHA — What Do FHA and USDA Loans Have in Common?

While USDA and FHA loans have their differences, there is some overlap between the two loan programs. Some of the features the loans have in common include:

1. Government Guarantee

Both FHA and USDA loans are guaranteed by the government. However, the agencies that guarantee the loans differ. The FHA provides insurance for lenders who participate in the FHA loan program, while the USDA backs USDA loans.

The government guarantee matters because it gives lenders peace of mind. When a lender issues a loan, it wants some reassurance that a borrower will repay it. To get that reassurance, lenders look at borrowers’ credit scores, income and assets. Generally, the higher a person’s credit score and income and the more assets they have, the less risky they look to a lender.

A borrower who doesn’t have a high credit score, substantial income or lots of assets might still be able to pay their mortgage as agreed, but a lender might hesitate to approve them. In the case of either a USDA loan or FHA loan, a government agency is stepping in to provide an extra layer of security to the lender, minimizing its risk.

The government guarantee doesn’t come free to borrowers. In the case of both an FHA and a USDA loan, the borrower has to pay mortgage insurance premiums to cover the cost of the agencies’ guarantees.

2. Availability to Buyers Who Might Have Difficulty Qualifying for Other Mortgages

Another feature FHA and USDA loans have in common is that both are available to homebuyers who might not qualify for other types of mortgages. The FHA loan program is meant for buyers who might have excellent, very good or fair credit scores and who aren’t able to make a large down payment. These buyers might have tried to apply for conventional mortgages but were turned down.

The USDA loan program is for buyers in rural or suburban areas who might not have enough income to qualify for another type of mortgage and who don’t have the down payment available for an FHA loan.

3. Fixed Interest Rates

Both USDA and FHA loan programs offer borrowers fixed interest rates. A fixed interest rate stays the same throughout the loan term. If you take out an FHA mortgage with a 3.85% rate, you’ll pay 3.85% on day one and on the last day.

There are several advantages to getting a mortgage with a fixed rate. You always know what your monthly payments will be when the rate is constant. Getting a mortgage with a fixed rate also lets you lock in a rate when they are low, without worrying that it will increase in the future.

In contrast, adjustable-rate mortgages (ARMs) have interest rates that change on a set schedule, such as every three years. The rate on an ARM can jump one day, increasing the size of your monthly mortgage payment.

USDA vs. FHA — What’s the Difference Between FHA and USDA Loans?

While there are some similarities when you compare USDA loans versus FHA ones, the mortgages come from two distinct programs. There are some other notable differences between FHA and Rural Development loans.

1. Down Payment Requirements

One of the biggest differences between a USDA loan and an FHA loan is the down payment requirement. In short, you can get a USDA loan without making a down payment. The loan program is designed to make homeownership an option for buyers who would otherwise be excluded from the process.

To get an FHA loan, you need to put down at least 3.5% of the purchase price. The general down payment requirement for FHA loans ranges from 3.5% to 10%. You can put down more, but the usual recommendation is to consider another type of mortgage, such as a conventional mortgage, if you can afford a bigger down payment. The cost of an FHA loan’s mortgage insurance can make it more expensive than other options for borrowers who can make larger down payments.

2. Location Requirements

Another notable difference between the FHA and USDA loan programs is the location restrictions the USDA loan program has. If you want to buy a home with an FHA loan, you can purchase property anywhere in the country. You can buy a four-unit place in the heart of New York City or a sprawling ranch in the middle of Montana.

That’s not the case with a USDA loan. The property you purchase with a USDA loan needs to be located in an eligible area. Eligible areas include rural parts of the country, as well as some suburban areas. You might be surprised at what counts as “rural” under the USDA’s definition, so unless you want to buy a home in a metropolitan area, it can be worthwhile to check the USDA’s eligibility map to see if your location qualifies.

3. Credit Score Eligibility

Your credit score plays a part in the approval process when you want to get a mortgage to buy a home. But, in the case of an FHA or USDA loan, it might play less of a part than it would if you were applying for a conventional mortgage.

Both loan programs have more lenient credit requirements than other mortgage programs. The USDA loan program has no set credit requirements. That said, the lender you work with might have its own set of requirements for borrowers who want to apply for a USDA loan. Often, a credit score over 640 is recommended for people who are interested in a USDA loan.

The credit requirements for an FHA loan determine the size of the down payment you can make. If your score is less than 580 but more than 500, you can qualify for an FHA loan but need to put down 10%. If your score is over 580, you can put down as little as 3.5%.

4. Mortgage Insurance Requirements

Mortgage insurance is part of the bargain whether you apply for an FHA or a USDA loan. But the amount of your mortgage insurance premiums will vary considerably depending on the program you choose.

FHA loans have higher mortgage insurance premiums than USDA loans, particularly if you make a smaller down payment. If you put down the minimum 3.5%, your monthly mortgage insurance premium will be 0.85% of the loan amount. You need to pay the premium for the entire term of the mortgage. The monthly premium is in addition to the 1.75% you paid upfront.

The required premiums, or funding fee, for a USDA loan aren’t more than 0.5% of the remaining balance and 3.75% upfront. You have to pay the monthly premium through the entire term of the USDA loan.

5. Closing Costs