Month: July 2020

Key Takeaways

- 15-year fixed mortgages lock in constant interest rates, typically lower than 30-year loans, providing payment predictability throughout the loan term.

- Monthly payments include principal, interest, homeowner’s insurance, property taxes, and potentially private mortgage insurance if the down payment is under 20%.

- Understanding how 15-year loans affect total costs requires requesting loan estimates, comparing options, and preparing for closing.

You plan on buying a house in the near future, and you know you’ll need a mortgage to do so. The question is, which type of mortgage may be best for you? Mortgages vary in term length, type of interest rate and the amount of interest charged. One available option is a 15-year, fixed-rate mortgage.

Apply NowStill have questions or need more information? Below is an overview of what this article covers!

Topics Covered

Frequently Asked Questions

- What Is a 15-Year Fixed Mortgage?

- How Does a 15-Year Fixed-Rate Mortgage Work?

- What Makes up Your Mortgage Payment?

- How Much Can You Afford to Borrow?

- Is a 15-Year Fixed Mortgage Right for Me?

- Apply for a Home Loan Online

As you weigh your mortgage options, it’s important to understand how getting a 15-year home loan will affect your monthly payments and how much you end up paying for your home over the long run. It’s also important to understand how a fixed interest rate differs from an adjustable rate. Get all the details on a 15-year fixed mortgage so you can determine if it’s the right option for you.

What Is a 15-Year Fixed Mortgage?

A 15-year fixed mortgage is a loan with a repayment period of 15 years and an interest rate that remains the same throughout the life of the loan. Like other types of mortgages, you use a 15-year, fixed-rate mortgage to buy property. Many people obtain a mortgage to buy their primary residence, while others obtain a mortgage to buy a vacation home or property to rent out to others.

To understand what a 15-year fixed mortgage is, it helps to break down some commonly used terms in the mortgage business:

- Term: The mortgage term is the length of time you have to repay the loan. At the end of the term, the entire loan needs to be repaid to the lender. The length of the term influences the size of the monthly payments, as well as the interest charged on the loan. Mortgages with shorter terms, like a 15-year home loan, are considered less risky to the lender, so they often have slightly lower interest rates compared to longer-term mortgages, like a 30-year loan.

- Interest: Interest is the price you pay to borrow money, usually a percentage of the loan, such as 3% or 4%. A lender determines your interest rate based on factors such as your credit score, income, the loan term and the market. The type of interest rate — whether it’s fixed or adjustable — also plays a part in determining when you pay.

- Fixed-rate: Some mortgages have a fixed interest rate. With a fixed-rate mortgage, you pay the same interest rate throughout the life of your loan. For example, a 15-year mortgage with a 5% fixed rate will have a 5% rate until the borrower pays off the mortgage or refinances. One advantage of a fixed-rate mortgage is that it allows you to lock in a rate when they are low. You can rest assured that your mortgage principal and interest payment will stay the same month after month, no matter what happens in the market. On the flip side, if you get a fixed-rate home loan when rates are high, you could be stuck paying a high interest rate for years.

- Adjustable-rate: Unlike a fixed-rate home loan, the interest rate on an adjustable-rate mortgage (ARM) changes at various points throughout the repayment period. Often, an ARM may have an introductory rate. The introductory rate tends to be lower than the interest rate available on a fixed-rate loan. After the introductory period ends, the rate may change based on whatever is going on in the market. It can go up, meaning your monthly payments may go up. It can also drop, meaning you may pay less each month. Some borrowers take out an ARM initially and later refinance to a fixed-rate loan.

- Principal: The principal is the amount of money you’ve borrowed to buy your home. If you purchase a $250,000 house, pay a 10% down payment of $25,000 and borrow $225,000, the $225,000 would be the loan’s principal. If you can pay extra against the principal as you pay down your mortgage, you can shorten the length of time it takes to pay off the loan completely.

- Mortgage insurance: Depending on the size of your down payment, you may have to pay mortgage insurance on top of the principal and interest charged on the loan. Mortgage insurance offers an additional layer of protection to the lender, in case the borrower struggles to make payments. It is usually required when a person makes a down payment under 20% of the home’s value. You can cancel the mortgage insurance payment once you have paid off enough of the principal to have 20% equity in your home.

How Does a 15-Year Fixed-Rate Mortgage Work?

A 15-year fixed-rate mortgage works similarly to other types of mortgages. You apply for the loan by providing proof of income, employment, assets and your credit history. If approved, you put down a certain amount of money, then make payments on the loan each month until it is paid off. The amount you can afford to borrow when you apply for a 15-year fixed mortgage depends on a variety of factors.

When you apply for a 15-year fixed-rate mortgage, you will typically take the following steps:

- Request a loan estimate from a lender: A loan estimate lets you know how much you can borrow, the interest rate and the anticipated closing costs. You can request estimates from multiple lenders to get a sense of what’s available.

- Indicate your intent to proceed: If you decide to move forward with one lender, you need to let them know. Lenders must honor the estimate for 10 business days, so you should decide if you’re moving forward within that time.

- Begin the application process: After you tell the lender you want to go ahead with the mortgage, you’ll need to submit documents, such as proof of income and bank statements, to start the formal application process.

- Prepare for closing: If all goes well with the application, home inspection and process as a whole, you can get ready for the closing date. It’s important to keep things moving as scheduled, as a delay in closing can mean you lose the rate you locked in or that you have to start over.

What Makes up Your Mortgage Payment?

One miscalculation many aspiring homebuyers make is to assume their monthly mortgage payment only includes the principal and interest. In reality, your mortgage payment includes multiple components. When you take out a 15-year home loan, your monthly payments can be divvied up in the following ways:

- Principal payment: This portion of your monthly payment goes toward the amount you’ve borrowed. As you pay down your mortgage, you’ll likely see the amount of your payment that goes to the principal increases while the amount you pay in interest decreases. Many lenders also let you pay additional amounts toward the principal to help pay off your mortgage more quickly. Paying more than the minimum due toward the principal monthly can help you get out of debt sooner.

- Interest: Think of the interest rate on your mortgage as the money you pay the lender in order to use their service. The lower your interest rate, the more affordable the loan is. As you pay down the principal, the amount you pay in interest each month shrinks.

- Homeowner’s insurance premiums: Your lender may also collect your homeowner’s insurance premiums and put them in an escrow account to be paid to your insurer. The size of your premiums depends on the value of your house and the amount of insurance you buy.

- Property taxes: Your lender may also collect your property tax payments and put them in an account to be paid to your local government by the due date each year. Property tax amounts vary widely from location to location.

- Private mortgage insurance: If you put down less than 20%, your lender may require private mortgage insurance. The amount varies based on the size of your down payment. The more you put down, the lower the insurance premium. Once you’ve made enough payments to equal 20% of the value of your home, you can ask the lender to remove the insurance.

How Much Can You Afford to Borrow?

You want to have a sense of how much you can afford to borrow before you start looking for a home and applying for a mortgage. Usually, since you pay off a 15-year home loan in half the time it takes to pay off a 30-year loan, the amount you can afford to borrow is less. You might be able to purchase a $200,000 home by putting 20% down if you apply for a 30-year loan. Since the monthly payments on a 15-year loan are often about twice as much as those on a 30-year loan, you might be able to purchase a $150,000 home with a 15-year loan.

You can use a mortgage calculator to compare the monthly payments on a 15-year versus a 30-year mortgage.

To determine how much you can borrow with a 15-year mortgage, pay attention to how much you can afford to pay each month. Look at your total debt compared to your total income. When getting a mortgage, your ideal housing ratio, also known as a front-end debt-to-income ratio, is 28%. With insurance and property taxes included, your housing payments should be within 28% of your total income.

Lenders also use the back-end ratio, which is all your debts compared to your income. An ideal back-end ratio is 36%. If you have other significant debts, such as student loans or car loans, your ideal monthly mortgage payment can end up being much lower than 28% of your total income.

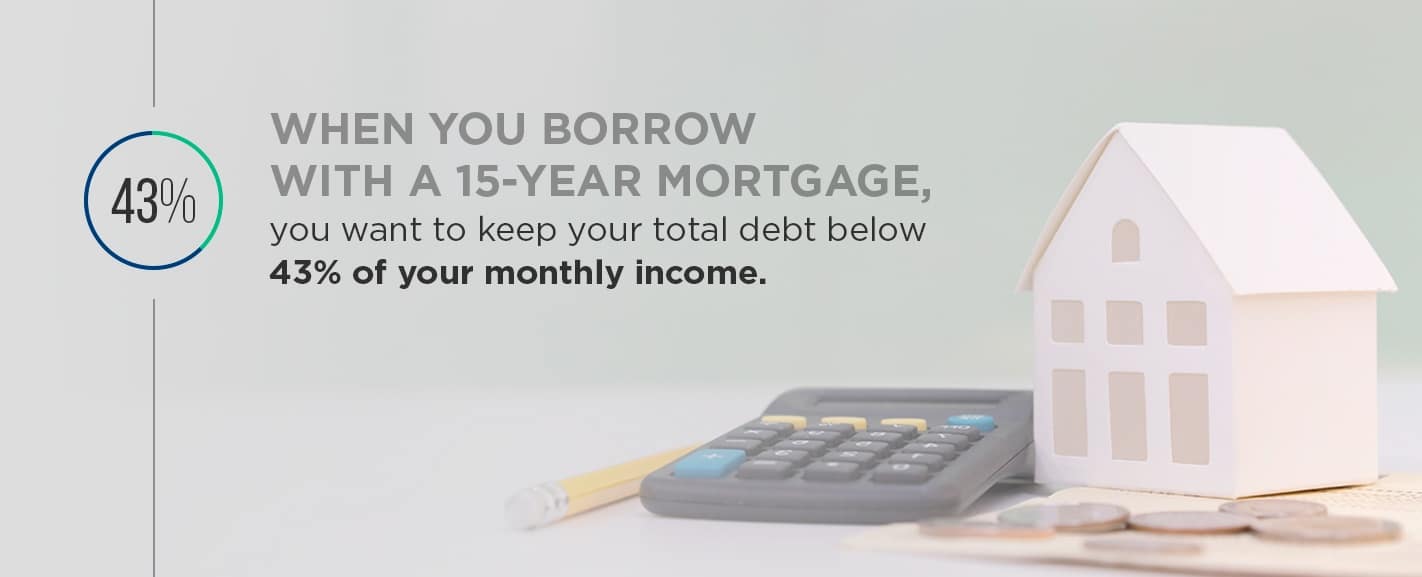

While the 28 and 36% ratios are ideal, lenders understand that life can be complicated. Depending on your income or credit score, you might be able to borrow as much as 43% of your monthly income.

To get your monthly payments under the desired percentage of your income, you may need to either pay off some debts before applying for your mortgage or find a way to increase your earnings.

Is a 15-Year Fixed Mortgage Right for Me?

Paying off your mortgage in half the time can seem pretty appealing. Before you decide to apply for a home loan with a 15-year term instead of a 30-year term, it’s important to consider your personal situation. You’ll pay the loan off sooner, but that usually means a higher monthly payment or buying a less expensive house. Some things to consider before applying for a 15-year fixed-rate home loan include:

- Your income stability: Since a 15-year mortgage typically means higher monthly payments compared to a 30-year home loan, it’s vital that you have the income needed to afford those payments. It’s also helpful if you have a steady record of earning either the same amount or increasing amounts of income each year. If there’s a lot of up-and-down in terms of what you bring in or if you aren’t sure how long your current employment and income situation may last, it may not be the right time to get a 15-year mortgage.

- Current interest rates: Take a look at the current interest rates. If they are low, getting a mortgage with a fixed rate is likely to be in your favor, as you’ll get to keep that rate for years to come. If rates are on the high side, you might consider an ARM instead. When it comes time for the rate on your loan to adjust, you can refinance to a fixed-rate loan or keep the ARM.

- Your age: Your age or season in life can help you determine if a 15- or 30-year loan makes more sense. If you are older and approaching retirement, a longer term may have you making payments on your loan after you’re no longer working. If you don’t want to have a mortgage throughout retirement, choosing one with a shorter term can make more sense.

- Your other financial goals: Consider your other financial goals in light of your mortgage. If you are trying to save for retirement or save for your child’s education, you may not want to pay a considerable amount of your monthly income toward your home. On the other hand, if you have already achieved other financial goals or have a high amount of disposable income each month, putting that toward your housing payment can be a good move.

- The price of homes in your area: The average price of houses in your area may influence whether you can afford a 15-year mortgage or not. The more expensive homes are, the higher your payment may be. But if homes are relatively affordable, getting a 15-year loan can help you own your home outright in less time and for less money.

[download_section]

Pros of a 15-Year Fixed-Rate Mortgage

If you’re still not sure if a 15-year fixed-rate mortgage is right for you, it helps to look at a few advantages of this type of home loan:

- You build up equity more quickly: Equity is the difference between the value of your home and the amount you still owe on the mortgage. Having equity in your home gives you leverage. When you sell the home, you get more money from the sale if you have more equity in it. You can also use equity to borrow against your home to cover the cost of renovations or other repairs.

- You own your home faster: With a 15-year mortgage, you can own your home completely in half the time it would take if you were to get a 30-year loan. Once your home is fully paid off, your cost of living can drop significantly.

- You pay less in interest: Since you have a 15-year mortgage for less time than a 30-year loan, you usually end up paying considerably less in interest. More of your monthly payment goes toward the principal sooner. Although you have bigger monthly payments, the total cost of a 15-year loan is often much less than the cost of a longer mortgage.

- You might get a better interest rate: The less time you need to pay off a loan, the less of a risk you are in the eyes of a lender. Depending on other factors, many lenders are likely to offer lower interest rates on 15-year mortgages compared to 30-year loans.

- You don’t have to worry about interest rates changing: With a fixed-rate loan, the rate you pay on day one is the same as the rate you pay on day 5,000. You don’t have to worry that your payment may suddenly balloon or that you’ll be left with an unexpectedly high mortgage bill.

- You have the same payment month after month: A 15-year, fixed-rate mortgage eliminates one uncertainty from your life: How much your housing payment will be. When you rent, your monthly obligation can increase from year to year if your landlord decides to raise the rent. With an ARM, your payment can go up, as well. Your fixed-rate mortgage payment stays the same year after year, even if you begin to earn more money or other costs increase.

- You might be able to make a larger down payment: Since the price of the home you can buy with a 15-year mortgage could be lower than what you can afford with a 30-year mortgage, you may be able to put down more upfront — potentially saving you the cost of private mortgage insurance. For example, if you can afford a $200,000 home with a 30-year mortgage and have $30,000 to put down, your down payment would be 15% and you’ll have to pay mortgage insurance. If you can afford a $150,000 home with a 15-year mortgage and put $30,000 down, your down payment is 20%. Putting down 20% upfront can also make you more likely to get a lower interest rate, helping you save even more.

Cons of a 15-Year Fixed-Rate Mortgage

While a 15-year fixed-rate mortgage can have several benefits for the right borrower, there are also some potential drawbacks to consider:

- You have a higher monthly payment: Usually, the monthly payment required on a 15-year mortgage is higher than that required by a 30-year mortgage since you are paying the loan in half the time. If your income is high enough and you have enough financial stability, the extra monthly payment in exchange for saving more overall might not be a concern. But if you struggle to make ends meet each month or have other financial obligations, a high mortgage payment can be a challenge.

- You could end up “house poor”: You build up equity more quickly with a 15-year loan. This can also mean you end up house poor, meaning most of your net worth is tied up in your home. Day-to-day, that might not be an issue. But if you need cash quickly and don’t have a lot of savings or liquidity, it can pose a problem.

- You might have to buy a less expensive house: Depending on where you live, you might not be able to afford to buy a house with a 15-year mortgage. If housing prices are high, a 30-year loan might be a necessity to keep your monthly payment within reach. Another option may be to buy a smaller, less expensive home, such as a two-bedroom instead of a three-bedroom or a house in a neighborhood that offers fewer amenities.

- You might get stuck with a high interest rate: Interest rates fluctuate from year to year, so depending on when you buy your home, you may end up getting a higher rate compared to someone with similar income or credit who buys a home a year before or after you. Since the interest rate on a fixed-rate mortgage is the same for the life of the loan, you could be stuck with a high rate unless you refinance.

Apply for a Home Loan Online

Assurance Financial aims to help people achieve the American dream of homeownership. If you’re ready to make the first step towards buying your home, we’re here to help. Abby, our online mortgage assistant, can walk you through the process of putting together your application.

You can get started today or set up an appointment to put together your application at a time that works for you. If you’d rather talk to a representative right away, you can connect with a loan advisor in your state who can help you review your mortgage options and choose the one that works for you.

Sources

- https://assurancemortgage.com/purchase-your-home/

- https://www.consumerfinance.gov/ask-cfpb/on-a-mortgage-whats-the-difference-between-my-principal-and-interest-payment-and-my-total-monthly-payment-en-1941/

- https://www.lendingtree.com/home/mortgage/common-mortgage-terms/

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-debt-to-income-ratio-why-is-the-43-debt-to-income-ratio-important-en-1791/

- https://www.phila.gov/services/property-lots-housing/property-taxes/real-estate-tax/

- https://www.mortgageloan.com/why-you-should-and-shouldnt-get-a-15-year-mortgage

- https://www.credit.com/blog/can-you-qualify-for-a-15-year-mortgage-113487/

- https://www.bankrate.com/calculators/mortgages/mortgage-calculator.aspx

- https://www.nerdwallet.com/mortgages/mortgage-calculator/calculate-mortgage-payment

- https://www.bankrate.com/mortgages/arm-vs-fixed-rate/

- https://www.rocketmortgage.com/learn/15-vs-30-year-mortgage

- https://www.fool.com/mortgages/4-reasons-to-get-a-15-year-mortgage.aspx

- https://www.bankrate.com/finance/mortgages/fixed-rate-mortgages-1.aspx

- https://www.quickenloans.com/learn/home-equity-and-how-to-use-it

- https://www.nerdwallet.com/article/mortgages/pros-cons-15-year-mortgage

- https://www.daveramsey.com/blog/what-is-a-15-year-fixed-rate-mortgage

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/find-a-loan-officer/

It’s the age-old question: What came first, the home or the baby? Many people are asking themselves, “Should we buy a house or have a baby?” Does it make more sense to buy a house after having a baby, or should you do it before, so that you’re all settled in by the time you’re ready to start a family?

The answer is that there is no one right answer. Buying a house and having a baby at the same time makes sense for some people. Purchasing a home before welcoming a child is the right choice for others, and buying a house after having a baby makes sense for some. Here’s what you need to know about getting a mortgage, expenses connected to your new home and new baby and a few benefits of each option.

Qualifying for a Mortgage Before Having a Baby

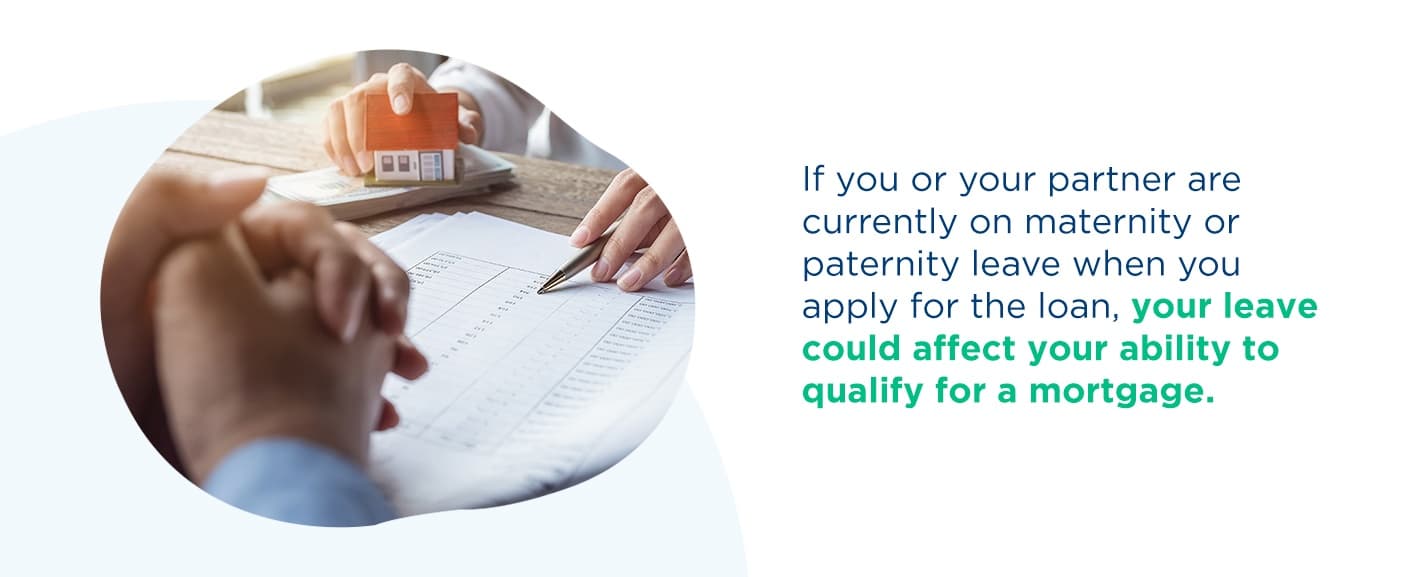

The process of qualifying for a mortgage before you have a baby is very similar to qualifying for a mortgage after you’ve had your child, with one notable exception. If you or your partner are currently on maternity or paternity leave when you apply for the loan, your leave could affect your ability to qualify for a mortgage. Being on unpaid leave can complicate the mortgage application process, as your mortgage lender might not be able to verify your income, even if you plan on returning to work after a few weeks. For that reason, it can make more sense to apply for your mortgage and buy your house pre-baby or wait until both you and your partner have gone back to work after the baby arrives before you start the mortgage process.

When you apply for a home loan, the lender will look at the following areas to determine whether you’re eligible for a mortgage, how much you can borrow and the interest rate you’ll pay.

- Your income: How much you and your partner earn plays a major role when it comes to determining how much you can borrow. As a general rule, the more you earn and the more stable your income is, the more you can borrow to buy a house. If either you or your partner plans on staying home with the baby and not earning income, it might be a good idea to see if you qualify for a mortgage using the other person’s salary. That way, you’ll avoid buying more house than you can comfortably afford after the baby arrives and your income situation changes.

- Your credit: Your credit history and score also have a considerable effect on the mortgage process. The higher your score, the better the terms on the loan you’ll receive. As with income, if one person doesn’t have the best credit or has a troubled credit history, it might be worthwhile to try and qualify for the mortgage using just one partner’s credit.

- Your employment history: How long you’ve been with a particular employer or have been self-employed also plays a role when you’re qualifying for a home loan. Lenders like to see a stable employment history, as it implies that you will continue to work for a company or continue to have a reliable source of income.

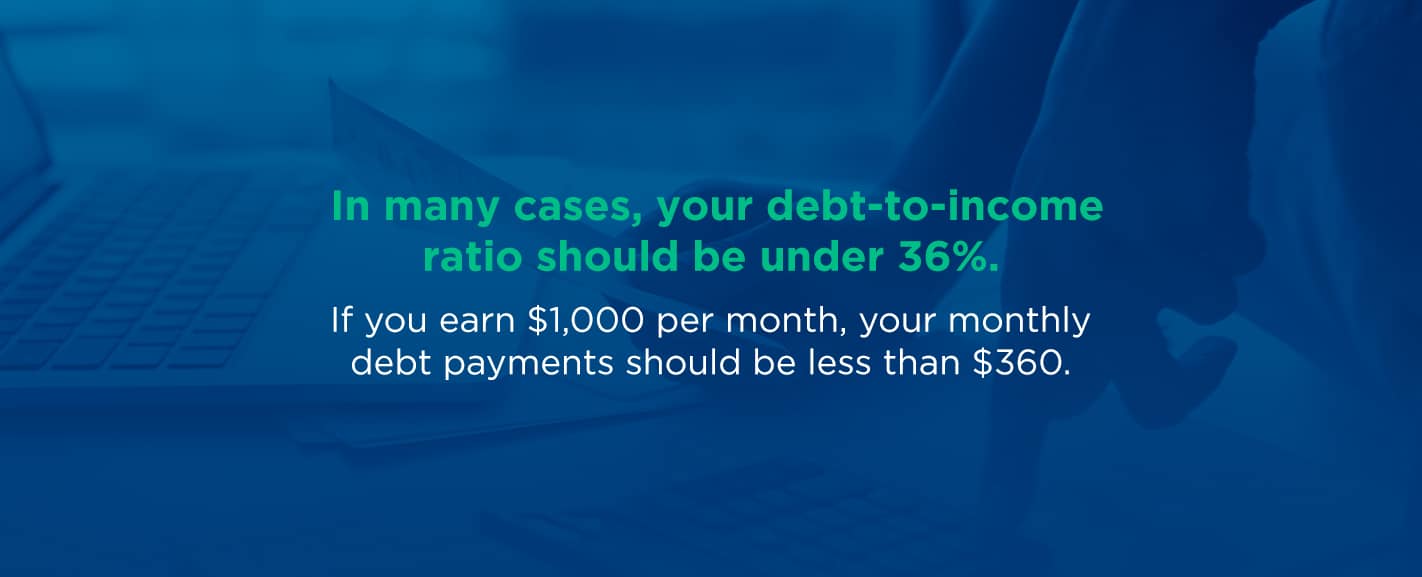

- Your other debts: Another factor lenders consider when reviewing a mortgage application is the number of other debts an individual or couple has and the amount of those debts. In many cases, your debt-to-income ratio should be under 36%. If you earn $1,000 per month, your monthly debt payments should be less than $360. In some cases, your debt-to-income ratio can be up to 45% or 50%, but 36% is usually preferable for you and your lender.

- Your assets: A lender wants to know how much you have in savings or investments when you apply for a mortgage. There are two reasons why information about your assets is important. First, it lets a lender know that you have enough money for the down payment. It also can provide some peace of mind to the lender that if you lose income, you’ll still have a way to make your mortgage payments.

Do You Need to Tell the Lender About Your Family Plans?

Lenders can’t discriminate against people who are pregnant, who have children or who are considering having children in the near future. They also can’t discriminate against people who are out on parental leave. If you are currently pregnant or have plans to become pregnant soon, you have no obligation to tell a lender. They also can’t ask you about your family plans.

If you are currently on maternity or paternity leave, it is a slightly different story. Income is an essential element when approving or denying a person for a loan, so consider providing your lender with plenty of documentation about your leave, such as when it will end and how much your income will be once your leave is over. Your employer might be willing to write a note that provides income information and a start and end date for your leave.

While lenders can’t discriminate against people on leave, being on unpaid leave can make it challenging for parents to get a mortgage. It’s a good idea to work with a lender who is understanding from the beginning and willing to work around your leave rather than deny your application.

Common Expenses Related to Homes and Children

Buying a home and having a child are two major life events that bring with them several expenses. Understanding the cost of getting pregnant and buying a house can help you determine if one or the other — or both — is the right choice for you at the moment. Take a look at some of the hidden and not-so-hidden costs of homeownership and parenthood.

House-Related Expenses

Some of the expenses related to owning a home are ongoing, while others are less frequent.

- Utilities: You’ll need to pay to keep the lights on, the furnace operating and the water running at your home. If you want internet and television services, you’ll need to pay for those, as well. The cost of utilities can vary based on the size of the house and how much energy your family uses. Local rates also vary, and some areas are more expensive than others.

- Repairs and maintenance: The equipment and systems that keep your house ticking will need ongoing care and maintenance and might need more extensive repairs from time to time. Maintenance involves things such as tune-ups of the HVAC system or furnace, cleaning the dryer vents and mowing the lawn. Repairs can include fixing broken appliances, leaks in the plumbing or issues with the electrical system. Experts usually recommend that homeowners have at least 1% of the price of the home set aside to cover maintenance costs and repair bills.

- Furniture, appliances and decorations: You’ll want to fill your new home with furniture and decor to put your own personal spin on it. Depending on what type of appliances came with the house and their age, you might also want to purchase new ones or upgrade existing ones. While furniture and appliances can be expensive, especially if you’re buying a lot all at once, the good news is that they are usually a one-time cost or a once-in-a-decade cost.

- Homeowner’s insurance premiums: If you have a mortgage, you need to have homeowner’s insurance. Usually, your monthly mortgage payment includes the cost of your insurance premiums. Still, it’s something to plan for, as you don’t want to be surprised when your first mortgage bill is several hundred dollars more than you expected.

- Property tax: Property tax is another expense that can vary widely based on location. Some areas have a high tax rate, while others have a relatively low one. Some cities or municipalities offer tax abatements to certain types of homeowners or to people who buy specific kinds of property. Like your homeowner’s insurance, your property tax is usually collected with your mortgage payment.

- Homeowners’ association (HOA) fees: Depending on the type of neighborhood you move into, you might have to pay HOA fees. Usually, HOA fees are required when you live in a condo or townhouse development. The fees cover the cost of maintaining common areas, such as the lobby of a condo building or the parking area in a residential development. The fees can vary from area to area and can suddenly increase if an unexpected event, such as an excessive amount of snowfall or extensive storm damage, occurs.

Child-Related Expenses

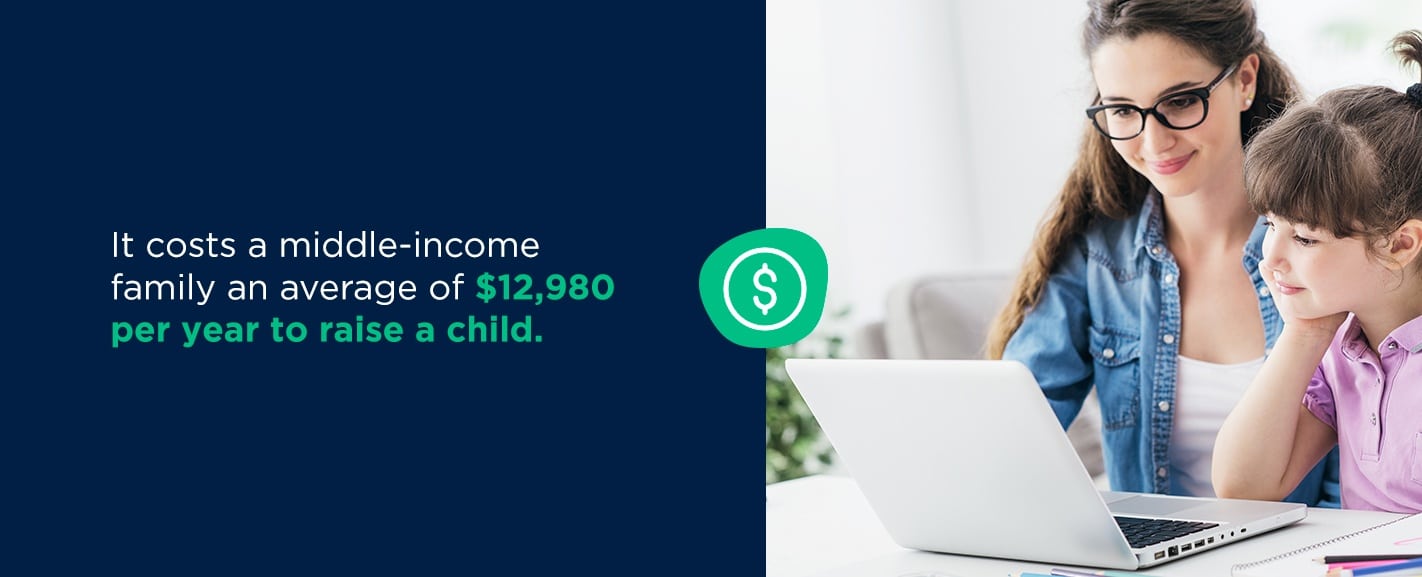

It costs a middle-income family an average of $12,980 per year to raise a child. The three largest expenses are housing, food and child care and education. For now, let’s take a look at the costs associated with bringing a new baby home.

- Delivery: Although insurance is meant to cover many of the costs of having a baby, the average insured woman paid $4,569 to deliver a baby in 2015. How the baby is born and where they are born can affect the price of delivery. For example, it usually costs more to have a C-section than to deliver vaginally.

- Clothing: Baby clothes are cute, but they also cost money. You might get a lot of clothes at your baby shower, but you can also expect your little one to outgrow those onesies and tiny T-shirts at a rapid pace.

- Baby gear: Babies typically need a lot of stuff, from car seats to bassinets and from cribs to strollers. There’s also the cost of “fun” things for babies, such as toys and walkers. One way to reduce the cost of gearing up for baby is to buy previously-owned items or to accept hand-me-downs from relatives and friends.

- Food: Babies who breastfeed get a nearly free source of food for the first few months or year of their lives. But not every baby can be breastfed, meaning some parents will need to plan on purchasing formula. As your baby begins to eat solid foods, usually around six months, you’ll want to add the cost of their food to your budget.

- Daycare: Although parents can decide to stay home with their child indefinitely, many need to go back to work at some point. The cost of daycare for an infant varies greatly from region to region but is generally high. In Mississippi, annual infant care costs $5,436, or about 11% of the median household income. In Washington, D.C., the average annual infant care cost is $24,243, or 28.3% of the median household income.

Should you buy a house before you start or increase your family? There are some advantages to finalizing the housing search and purchase before the baby arrives.

- You have time to settle in: If you buy your home with a growing family in mind, but before any children arrive, you will have plenty of time to settle into the house and get unpacked before you start planning the next phase of your life. You can even enjoy the house as just the two of you for a while, depending on whether you are pregnant when you buy your home.

- You can finish home projects before baby arrives: Waiting to start your family until after you’ve bought a home gives you time to tick all those home projects off of your list. The nesting instinct often kicks in when women are pregnant, which means you might get a shot of energy and feel the gumption to fix that leaking kitchen faucet, redo the backsplash or wallpaper the bedroom before your newest family member arrives.

- You’ll have less to pack: Babies and children might be small, but they tend to have a lot of stuff. If you buy your house before getting pregnant, any gifts you get during the shower or any items you purchase for your newborn can be sent directly to your home. You’ll end up with fewer things to pack and haul, which can also help you save money on the cost of movers or renting a truck.

- Baby can get settled into their new home: Babies and toddlers are creatures of habit and routine — once you establish those habits and routines with them. Moving can throw a wrench into their routine, meaning you might go from having a baby who sleeps through the night to having a baby who wakes up every two hours screaming. If you’re already in your home and settled when the baby is born, you don’t have to worry about disrupting their sleep schedule or another routine later.

- It can be easier to search for a house when child-free: Before you buy a house, you have to find a house. That can be easier to do when it’s just you or you and your partner looking. If you have a baby already, you’ll need to find a babysitter for them or bring them with you to look at homes. While a very young baby will likely sleep through the experience of househunting with their parents, you might not want to run the risk of them waking up screaming when you’re in the middle of checking out an open house.

[download_section]

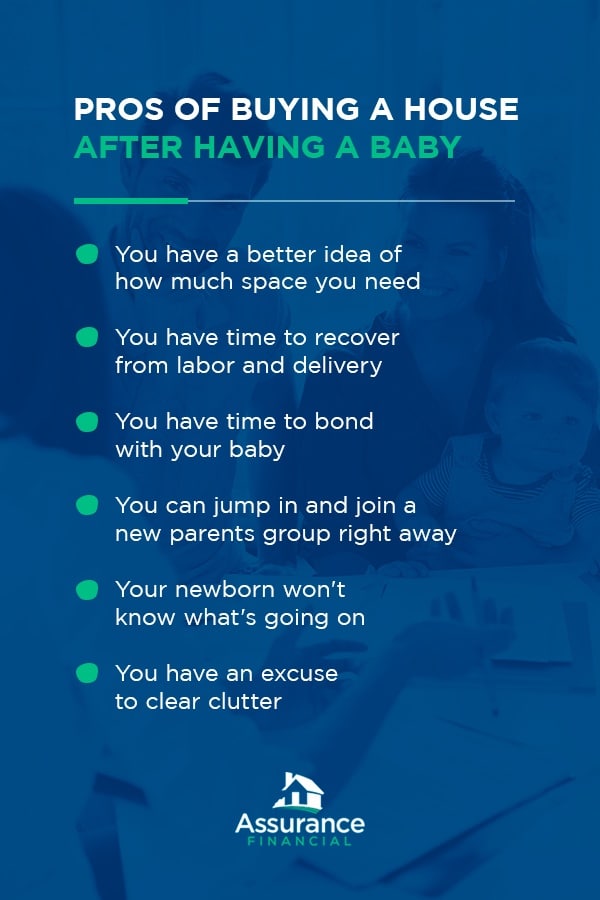

Pros of Buying a House After Having a Baby

Waiting to buy your home and move until after you have had your child or expanded your family can also make sense, depending on your needs and circumstances. Some of the benefits of postponing the home buying process until after you have a baby include:

- You have a better idea of how much space you need: If you wait to start looking for a home until after you’ve had your child, you’ll have a better idea of what works and what doesn’t in your current home and what you would like from your future residence. For example, you might find that a two-bedroom is too small for you, your partner and your baby and that you’d like at least a three-bedroom home. Or you might realize that you want some outdoor space for your child to play safely as they get older. You might decide going up and down steps with a baby in tow is challenging and that you’d prefer to move into a single-story ranch home.

- You have time to recover from labor and delivery: Although it varies from woman to woman, many find that they do need time to take it easy and recover after childbirth. That can be particularly true of women who give birth via a C-section. If you wait to start looking for homes until after your baby is born, you can also give yourself plenty of time to heal from the labor itself.

- You have time to bond with your baby: You can take all the time you need to bond with your baby if you decide to wait until after they are born to move. You might choose to postpone the housing search until after your parental leave is up so that you can spend that time connecting with your child.

- You can jump in and join a new parents group right away: Depending on how far away you end up moving, you might need to find a new social circle when you arrive. You might want to expand your social group after having a baby anyway, especially if the rest of your friends are still child-free. Waiting to move until after your baby is born means that as soon as you get settled into your new neighborhood, you can join a local parents group or another social club designed for parents of young ones, such as a Mommy and Me yoga club or a Stroller Strides exercise club.

- Your newborn won’t know what’s going on: Babies, particularly newborns, are easier than most people give them credit for. They sleep a lot of the day and aren’t going to have a clue what is going on. You can tuck your sleeping baby into their car seat and drive them across town or across the state, and they will have no idea that they are somewhere different when they arrive. If you need to find a babysitter for your little one while you move, you might find that you have an easy time convincing a grandparent or close friend to watch them.

- You have an excuse to clear clutter: You might have gotten a lot of gifts and gear for your baby that you ended up not needing. Depending on when you move, your little one might have already outgrown some of their clothes. Waiting until after baby arrives to move can mean that you have a chance to sell or give away some of the baby gear you know you won’t need. You don’t have to worry about lugging it from one home to the next.

Pregnant and Buying a House? Apply for a Mortgage Online With Abby

Whether you’re currently pregnant, about to become pregnant or have recently added to your family, the first step in the home buying process is to get approved for a mortgage. Abby is Assurance Financial’s digital loan assistant. She’s here to walk you through the process and to help you gather all the information you need during your application. If you’re ready to get started, you can apply for a mortgage in less than 15 minutes.

Sources:

- https://assurancemortgage.com/applying-for-home-loan-pregnant/

- https://selling-guide.fanniemae.com/Selling-Guide/Origination-thru-Closing/Subpart-B3-Underwriting-Borrowers/Chapter-B3-6-Liability-Assessment/1736872241/B3-6-02-Debt-to-Income-Ratios-02-05-2020.htm

- https://selling-guide.fanniemae.com/Selling-Guide/Origination-thru-Closing/Subpart-B3-Underwriting-Borrowers/Chapter-B3-3-Income-Assessment/Section-B3-3-5-DU-Requirements-for-Income-Assessment/1736867221/B3-3-5-01-Income-and-Employment-Documentation-for-DU-08-07-2019.htm

- https://www.zillow.com/mortgage-learning/qualifying-for-a-mortgage/#qualify

- https://www.capitalone.com/bank/money-management/saving-house/qualify-for-mortgage/

- https://theweek.com/articles/717349/3-tips-buying-home-expecting-child

- https://www.bankrate.com/mortgages/proving-income-to-land-a-mortgage/

- https://dreamhomefinancing.com/buy-house-before-having-baby/

- https://themortgagereports.com/60552/how-to-get-a-mortgage-on-maternity-leave

- https://www.nytimes.com/2010/07/20/your-money/mortgages/20mortgage.html

- https://www.credit.com/blog/can-you-be-denied-a-mortgage-if-youre-pregnant-157075/

- https://www.bankrate.com/mortgages/maternity-leave-mortgage-approval/

- https://www.usda.gov/media/blog/2017/01/13/cost-raising-child

- https://www.realtor.com/advice/home-improvement/how-much-should-you-budget-for-home-maintenance-and-repairs/

- https://www.nerdwallet.com/blog/finance/budgeting-for-new-homeowners/

- https://www.hgtv.com/lifestyle/real-estate/immediate-expenses-for-new-homeowners-to-expect

- reuters.com/article/us-health-maternity-costs/even-for-insured-women-having-a-baby-in-the-u-s-is-costly-idUSKBN1Z7300

- https://www.epi.org/child-care-costs-in-the-united-states/#/DC

- https://www.newyorklife.com/articles/breakdown-of-biggest-expenses-for-your-child

- https://www.moving.com/tips/why-you-should-move-before-the-baby-comes-or-wait-why-you-shouldnt/

- mortgages.com/buying-house-and-owning-home/buying-house-when-babys-way-look-and-budget-you-leap

- https://assurancemortgage.com/meet-abby/

- https://assurancemortgage.com/apply/

Key Takeaways

- VA loans are exclusively for veterans and active-duty members with no published credit score minimum, often requiring zero down payment (~90% of VA loans), while FHA loans are available to anyone with a Social Security number, requiring 3.5-10% down and a 500+ credit score.

- VA loans require no mortgage insurance, whereas FHA loans mandate both upfront (1.75%) and monthly mortgage insurance premiums (0.45-1.05%) for the loan’s entire term.

- Both loans require primary residence use and can be used for 1-4 unit properties, but VA loans offer the same conforming mortgage limits while FHA limits vary by location.

Not every potential homeowner qualifies for a conventional mortgage — and that’s okay. Several mortgage programs exist that help people buy a home, even if their credit isn’t the best or even if they don’t have a large down payment saved up. If you are hoping to buy a home soon, but aren’t sure that you’ll qualify for a conventional mortgage, it can be worthwhile to look at government-backed home loan options, such as a VA loan or FHA loan.

While both have less-strict requirements for borrowers compared to conventional loans, there are some differences between FHA and VA loans. Some people might qualify for an FHA loan, but not a VA loan, for example. Another notable difference between a VA loan and an FHA loan is the size of the down payment. In this guide, we’ll discuss what’s required of each, so you can determine which one might be right for you.

Table of Contents

- FHA Loan Requirements

- VA Loan Requirements

- Similarities and Differences

- Which is Right for You?

- Find Out if You Qualify Today

FHA Loan Requirements

The Federal Housing Administration (FHA) loan program has been around since 1934. Its goal is to help as many people as possible buy a home. Under the program, mortgages are made by the same lenders and banks who issue conventional mortgages. Unlike conventional mortgages, the amount of an FHA loan is backed or insured by the government.

If the borrower stops making payments, the FHA will step in. Since the government insures the loan, lenders can feel comfortable offering mortgages to people who don’t have excellent or very good credit. Lenders can also offer a relatively favorable interest rate to an FHA borrower, even if the borrower isn’t making a large down payment or doesn’t have the best credit.

FHA loans aren’t available to everyone, though. A borrower does need to meet a few requirements before they can get approved from an FHA mortgage. For example, they need to have a credit score of at least 500. The down payment on an FHA loan can be as little as 3.5 percent of the price of the home, but to put down less than 10 percent, a person’s credit needs to be at least 580.

Another notable requirement of an FHA loan is mortgage insurance. While the government’s guarantee does make mortgages possible for more people, the guarantee isn’t free. Borrowers need to pay mortgage insurance on the loan, in addition to the principal and interest. FHA mortgage insurance comes in two forms.

The first is an upfront payment of 1.75 percent of the loan’s value. The second is an ongoing monthly payment ranging from 0.45 to 1.05 percent of the value of the loan. The amount of the monthly payment depends on the size of the down payment and the length of the loan.

The monthly mortgage insurance premium would be for the entire length of the FHA loan unless the down payment was 10 percent or higher. If a borrower puts down more than 10 percent of the value of the home, they will need to pay a mortgage insurance premium for 11 years.

VA Loan Requirements

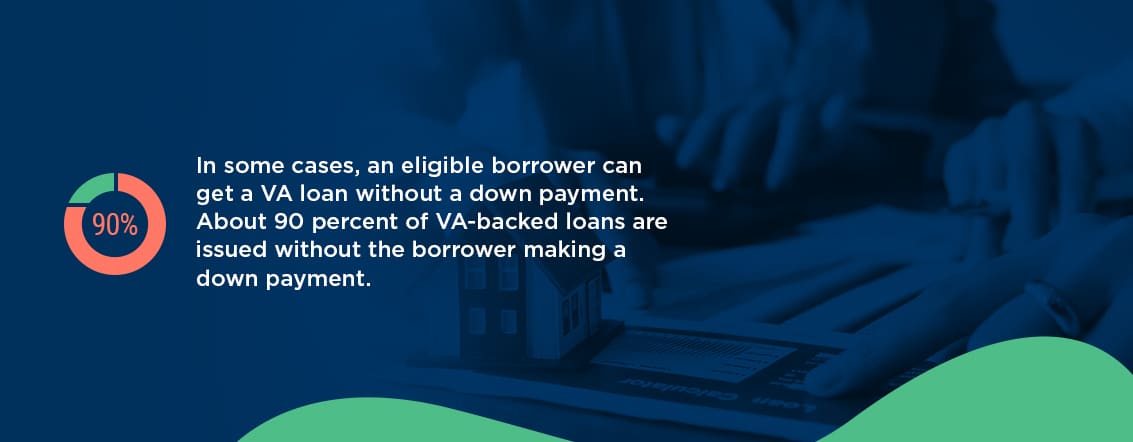

Like the FHA loan program, the VA loan program is a government-insured mortgage program. Also, like FHA loans, VA loans are made by private lenders and banks. However, in the case of VA loans, The Department of Veterans Affairs backs or insures the loans. VA loans have lower down payment requirements compared to conventional mortgages and FHA loans. In some cases, an eligible borrower can get a VA loan without a down payment. About 90 percent of VA-backed loans are issued without the borrower making a down payment.

There isn’t a published minimum credit score that a person needs to have to be eligible for a VA loan. Instead, a lender typically reviews applications for VA loans on a case-by-case basis.

The most notable requirement of VA loans is that the person is either a veteran or active-duty service member or a member of the National Guard or Reserve. How long a person needs to have served varies based on when they served or if they are currently on active duty. In some cases, the length of service requirement doesn’t need to be met if a person was discharged for a qualified reason. Surviving spouses or spouses of prisoners-of-war or veterans who are missing in action might also be able to qualify for a VA loan.

To prove eligibility, a veteran or active duty service member needs to apply for a certificate of eligibility.

VA Loan Versus FHA Loan: Similarities and Differences

If you’re shopping for a mortgage, it can be helpful to take a close look at how FHA loans compare to VA loans. If you’re eligible for both, understanding the differences between the two can help you narrow down your home loan options.

1. Eligibility

The most important difference between a VA loan and an FHA loan is eligibility. You can only get a VA loan if you are currently or have been a member of the armed forces or if you’re a surviving spouse of a veteran or POW. You also need to meet the length-of-service requirements.

FHA loans aren’t restricted to a certain type of person or a certain group of people. You do need to have a Social Security number to be eligible for an FHA loan.

2. Type of Home

For both an FHA loan and a VA-backed loan, the home you purchase needs to be the home you’ll live in as your primary residence. You can’t use either loan to buy a vacation property or investment property.

You can use an FHA loan or VA loan to purchase a home with one to four units.

One common misconception about both FHA and VA loans is that they are only for first-time homebuyers. While both types of mortgages can be a great choice for a first-time buyer, there are no rules that restrict the loans to first-timers only.

3. Minimum Credit Score

One difference between FHA and VA loans is the credit score required. For an FHA loan, you need to have a credit score of at least 500. If your score is between 500 and 579, you’ll have to put down 10 percent to qualify for the mortgage. If your score is at least 580, your down payment can be as low as 3.5 percent.

The VA loan program doesn’t have a minimum score requirement. It encourages lenders to look at the full picture, including a borrower’s credit history, employment history and assets, when making a decision.

4. Maximum Loan Amount

The VA and FHA loan programs have different maximum amounts. The VA loan limit is the same as the limit for conforming conventional mortgages. The exact amount of the limit varies based on the number of units in the home and the location of the property. Homes in areas with a higher cost of living have higher mortgage limits compared to homes in areas with a lower cost of living.

Borrowers who qualify for a VA-backed loan are eligible for an entitlement, which is the amount the VA will pay to a lender if a borrower ends up defaulting on the loan. The VA has two types of entitlement:

- Basic entitlement: The basic entitlement is the lesser of $36,000 or 25 percent of the loan’s principal. Usually, a lender will lend up to four times the amount of the basic entitlement without requiring a down payment.

- Bonus entitlement: The bonus entitlement is based on the conforming loan limits for conventional loans. The VA will guarantee 25 percent of the conforming limit for your area with the bonus entitlement.

Although VA entitlement limits how much the VA insures, it doesn’t necessarily restrict how much you can borrow. If you have the means to make a down payment, you might be able to borrow more or buy a more expensive home.

The maximum amount of an FHA loan is based on the location and size of the home. A one-unit home in an area with an average cost of living can cost up to $331,760. A one-unit home in an area with a high cost of living can cost up to $765,600.

5. Minimum Down Payment

One of the features of the VA-back loan program that makes it so appealing to eligible borrowers is that often, a down payment isn’t required. The minimum down payment for an FHA loan is 3.5 percent.

6. Maximum Debt-To-Income Ratio

The debt-to-income ratio compares the amount of your monthly debt to the amount of your monthly income. You can calculate it by dividing your total monthly debt payments to your total monthly income. For example, if you pay $1,000 toward a credit card and student loan payment each month and you earn $4,000 a month, your debt-to-income ratio is 25 percent:

1,000/4,000 = 0.25 (25%)

When deciding to approve or deny a mortgage application, a lender will look at your total debt-to-income ratio to see if the amount you want to borrow will be too much of a burden or too challenging for you to pay.

For most mortgages, including an FHA loan, the maximum debt-to-income ratio is 43 percent. There are some exceptions, though, and some lenders might accept a borrower with a debt-to-income ratio as high as 50 percent.

VA loans don’t have a maximum debt-to-income ratio, but a ratio of 41 percent or lower is often preferred.

The lower your debt-to-income ratio, the more comfortable you’re likely to be making your mortgage payments and affording other expenses. Although you can go up to 50 percent for an FHA loan, you might not want to do so.

7. Mortgage Insurance Premiums

Another major difference between an FHA loan and a VA loan is the mortgage insurance premium requirement. FHA loans require you to pay both an upfront mortgage insurance premium and a monthly premium. Unless your down payment is 10 percent or higher, you’ll need to pay the monthly premium for the entire term of the loan.

In contrast, VA loans don’t have mortgage insurance. They do have a one-time funding fee, which you pay upfront. The funding fee ranges from 1.4 to 2.3 percent and is based on the size of your down payment.

8. Interest Rates and Closing Costs

VA loans tend to have lower interest rates than conventional mortgages or FHA loans. Additionally, the closing costs on VA loans tend to be lower than for other types of mortgages. While VA loans have fixed interest rates, FHA loans can have fixed or adjustable interest rates.

9. Loan Length

One thing VA and FHA loans have in common is that both are available in a range of terms. Depending on your budget and needs, you can apply for a 30-year FHA loan or a 30-year VA loan. The mortgages are also available in 15-year or 10-year terms.

10. Application Process

Both VA and FHA loans require you to apply and to submit documentation and paperwork to verify your identity and income. You can expect to submit paystubs, income tax returns, bank statements and proof of other debts when you apply. Requirements can vary from lender to lender.

[download_section]

FHA vs. VA Home Loan: Which Is the Right Loan for You?

Since VA loans are only available to qualified veterans or active-duty service members, if you don’t have a history of service in the armed forces, you most likely don’t qualify for a VA loan. But even if you are a veteran or active-duty service member, you might still be wondering whether an FHA or VA loan is better for you.

One thing to consider before you apply for either is how much you can afford to put down. If you don’t have much saved for a down payment, or any money saved up, a VA loan might be the better choice. A VA loan can also be less expensive in the long run, as it doesn’t require mortgage insurance, and the closing costs and interest rates are often lower, compared to FHA or other loan options.

Your credit is another thing to consider when deciding between an FHA or a VA loan. While VA loans don’t have specific credit requirements, a lender might expect a person applying for a VA loan to have a good credit score. If your score is lower than 580, the FHA loan program might be a better choice, provided you have at least 10 percent saved for a down payment.

Find out If You Qualify for a VA or FHA Loan Today

Ready to jump in and get started with the process of finding the right mortgage for you?

Learn more about what you need to get started today.

Sources:

- https://www.hud.gov/buying/loans

- https://www.consumerfinance.gov/owning-a-home/loan-options/fha-loans/

- https://www.investopedia.com/terms/f/fhaloan.asp

- https://www.hud.gov/sites/documents/17-07ML.PDF

- https://www.bankrate.com/mortgages/what-is-an-fha-loan/

- https://www.nerdwallet.com/article/mortgages/fha-loan

- https://www.benefits.va.gov/BENEFITS/factsheets/homeloans/VA_Guaranteed_Home_Loans.pdf

- https://www.va.gov/housing-assistance/home-loans/eligibility/

- https://www.hud.gov/sites/documents/4155-1_4_SECA.PDF

- https://assurancemortgage.com/first-time-home-buyer-loans/

- https://www.benefits.va.gov/WARMS/docs/admin26/pamphlet/pam26_7/ch04.pdf

- https://www.hud.gov/program_offices/housing/sfh/lender/origination/mortgage_limits

- https://www.va.gov/housing-assistance/home-loans/loan-limits/

- https://entp.hud.gov/idapp/html/hicost1.cfm

- https://www.va.gov/housing-assistance/home-loans/loan-types/purchase-loan/

- https://www.benefits.va.gov/WARMS/docs/admin26/pamphlet/pam26_7/ch04.pdf

- https://www.military.com/money/home-ownership/how-fha-and-va-loans-stack-up.html

- https://www.hud.gov/answers

- https://www.nerdwallet.com/blog/mortgages/fha-vs-va-loan/

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-debt-to-income-ratio-why-is-the-43-debt-to-income-ratio-important-en-1791/

- https://www.hud.gov/sites/dfiles/SFH/documents/SFH_FHA_INFO_19-07.pdf

- https://www.hud.gov/sites/documents/17-07ML.PDF

- https://www.va.gov/housing-assistance/home-loans/funding-fee-and-closing-costs/

- https://www.hud.gov/program_offices/housing/sfh/ins/203armt

- https://assurancemortgage.com/apply/

- https://www.military.com/money/home-ownership/how-fha-and-va-loans-stack-up.html

The average person living in the U.S. will move around 11 times during their life. Whether you’ve moved once, twice or 11 times, you know it’s not always the most enjoyable activity. Often, though, the benefits of moving outweigh the hassle and challenges. You may move before starting a new job and expanding your family, or you may move just to get a change of scene. Whether you need a fresh start, a bigger house or bigger yard or want to finally get a laundry room of your own, take a look at some of the more common reasons for moving.

Topics Covered

- 13 Reasons People Move

- What to Do If You’re Considering Moving

- Make Your Next Move With Assurance Financial

13 Reasons People Move

A home or apartment that was a perfect fit for your needs years ago may no longer be right for you. If you’re considering buying a new house and moving but are in need of some motivation, it helps to look at common reasons people move to see if they match your own reasons for wanting or needing to relocate.

1. They’d Like a Home Office

In 2019, 7% of U.S. workers, or 9.8 million people, worked from home some or all of the time. Whether your current job allows you to work from home or not, a home office can be a nice thing to have. If you don’t currently do paid work from home, you can use the home office as a quiet space to take care of household management tasks, such as paying the bills or speaking with contractors. If you do have the privilege of working from home for your job, a home office gives you a secluded place to accomplish your tasks for the day and have conference calls and video meetings in privacy.

Demand for home offices has increased among homebuyers in recent years. In 2003, 55% of buyers said they wanted a home office. In 2018, 65% of buyers said they wanted an office in their home. In 2020, the COVID-19 pandemic forced millions to work at home creating a vital need for a home office. If your current home office has no space for the desk and organizational items you need, you can upgrade your office with a move as well.

2. They Need More Storage Space

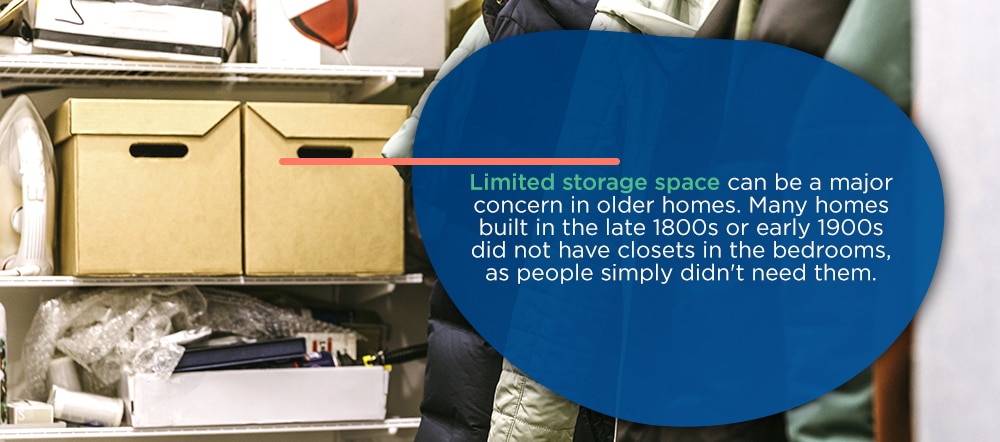

People in the U.S. tend to own more items than people living in other countries. While decluttering and donating, selling or discarding unused or unwanted items has become more popular lately, it’s also popular for people to move to get more storage space. Who hasn’t complained that their bedroom closet is too small? And who hasn’t wished that they had extra room in their kitchen, bathroom or living area for personal belongings?

Limited storage space can be a major concern in older homes. Many homes built in the late 1800s or early 1900s did not have closets in the bedrooms, as people simply didn’t need them. The few garments they owned were stored in trunks or dressers, not in closets.

If you’ve converted your garage to storage or rented an off-site storage unit, it can be easy to see why you’d want to upgrade to a home with more closet space or with built-in storage options, such as built-in bookshelves and storage cupboards. When all your belongings have a place to live, your home can be more organized and tidy, and you can feel more at peace.

3. They’d Like a Bigger Yard

While city living has its perks, one drawback for many people is the lack of yard space. In a city apartment or house, you may only have a small patio or a balcony to call your own. When summer barbecues begin and in-ground swimming pools beckon, people often find themselves drawn to homes that have significantly more yard space.

There are many things you can do in a larger yard, such as grow your own vegetables and flowers, invite friends over for lawn games and picnics, or install a pool. Homes with large, fenced-in backyards can be particularly desirable to people who have dogs, as the yard provides a safe space for the dog to run around and play outdoors. Families with children often find themselves moving to get a bigger yard. Young kids can play safely in a fenced-in yard, giving them the opportunity for fresh air and exercise.

4. They Are Downsizing

What people need from their home changes over the years. When you were single, a compact or studio space might have been the perfect fit. When you and a partner were raising kids and pets, a three- or four-bedroom home with a large backyard most likely worked well. Once the kids are grown up and in homes of their own, you might find that multiple bedrooms go unused. The large backyard might be too much work to take care of, or you might not use it as much as you once did.

Downsizing has its benefits. When you trade a larger home for a smaller one, you often end up with a smaller mortgage and lower monthly payments. Smaller homes can also be easier to take care of, as they require less cleaning and maintenance. Depending on your budget, if you need to downsize, you might be able to afford to live in a more desirable area or in a neighborhood with more amenities compared to if you wanted to buy a larger house.

Although downsizing is often associated with empty nesters or people in retirement, anyone can do it at any age. For example, when you bought your current home, a lot of bedrooms or a large yard might have seemed ideal. But after living in the house for a while, you may have realized all that space doesn’t work with your habits or lifestyle.

5. They Want a Better View

You open your bedroom curtains and see the brick wall of the house next door to you. Or, you look out the window in your living room and see a row of stores across the street. While the search for a better view might not be the sole reason for moving, it can play a significant role in the decision to relocate.

There are definite benefits of having something nice to look at when you glance out your windows. One study of 278 patients undergoing cardiac or pulmonary rehabilitation found that the patients who had a panoramic view of natural surroundings from their bedroom window were more likely to report improvements in their mental and physical health compared to patients who had a blocked view from their bedroom windows.

Another study found that people who took “microbreaks” and looked at images of nature were better able to concentrate and pay attention compared to those who didn’t.

6. They Want to Be Closer to Family

Over the years, families tend to become far-flung. One child might have traveled across the country for college, discovered they liked it there and stayed. Another might have relocated to Europe or Canada for work. Often, major life changes can inspire people who moved away from home to come back. In some cases, parents might pack up and move to be closer to their children and grandchildren.

Deciding to move closer to family has many benefits. For parents who move to be closer to their adult children, it provides the opportunity to maintain or build strong relationships with those children as they move through adulthood. It also gives older parents the opportunity to get to know their grandchildren. Instead of only seeing the grandkids on holidays or birthdays, a grandparent who lives in the same city or town has the chance to be involved in the daily lives of their grandchildren.

7. They Want to Be Closer to Work

Commute times vary in cities across the U.S, with employees in Cleveland having the shortest commutes of 23 minutes, and employees in Chicago having the longest of nearly 35 minutes. For many people, moving to shorten a commute makes sense. The less time you are spending behind the wheel or sitting on a bus or train each day, the more time you will have for things that matter to you. If you shave 10 or 15 minutes off your one-way commute time, you’ll have enough time each day to watch a sitcom with your family, spend more time at the breakfast table with them or even sleep in a bit longer before getting up to get ready.

8. They Want to Be in a Better School District

You want to provide your child the best education possible so they learn to think critically and can get a job that pays well when they reach adulthood. Unless you plan on sending your children to private school, in many cases, where your kids go to school is determined by where you live.

When you moved into your current home, you might not have had children yet or might not have given much thought to the quality of the schools in your area. Now that your kids are at or near school age, it is likely a different story. You may decide to pack up and move so your family is in the catchment area of a highly rated school district. You may also want to move so your children can go to a school district that has a lot of magnet school options for specialized training, such as a performing arts school or a school that’s dedicated to the sciences.

9. They’re Looking to Reduce Living Costs

There are considerable differences in the cost of living across the U.S. Places such as San Francisco, California and Brooklyn, New York have the highest housing costs in the country, as well as above-average costs for utilities, groceries and other day-to-day necessities. In some areas, it can be difficult to make rent and afford to save up for a down payment on a home while earning an average salary.

One way to cut the cost of living is to move to a place that is cheaper than average. Reducing your housing costs and other expenses allows you to reach financial goals, such as paying down your debts or saving to buy a house. In some cases, a person who is currently renting might look to areas with lower costs when they are interested in buying a home. Moving somewhere with lower housing costs can mean that you get a bigger house, with a big yard and all the amenities you need, at a price you can afford.

10. They Want to Try Something New

For some people, moving is the start of a new adventure. Moving to get a fresh start is fairly common. A person might decide to move to a new state or city to start over after going through a divorce or the breakup of a long-term relationship. Recent college graduates might pack up and move to a new city in search of more job opportunities or for an adventure.

Although some people decide to move for a climate change or out of curiosity, others might spend a considerable amount of time choosing where they go. They might look at the job opportunities available to them in a particular area and compare those opportunities and the salary potential to the cost of living. In some cases, people decide to move to a new area based on its proximity to other major cities. For example, a person might decide to move to Philadelphia to take advantage of its proximity to both New York City and Washington, DC and its comparatively lower cost-of-living.

11. They Want an Updated Kitchen

The cost of a kitchen remodel can be anywhere from $23,452 for a minor upgrade to $135,547 for a top-of-the-line major renovation. Usually, homeowners recoup around 53.9% to 77.6% of the cost of the kitchen upgrade when they sell their home.

If you’re not thrilled with your current kitchen, it might make financial sense to find a new home that has a kitchen that meets your needs or that has been updated more recently. Moving to a house with a better kitchen can be ideal if you have to move for other reasons, too. It can make more sense to leave your current kitchen as-is and let the next homeowner put their own personal stamp on it, rather than invest in a remodel or renovation right before selling.

12. They Need More Bedrooms

There are several reasons why a person or family might need to upgrade to a house with more bedrooms. If you currently live with a partner in a two-bedroom home, it might seem that you have more than enough bedrooms for your needs. But if you both start working from home, you might appreciate having a separate room to go to where you can close the door when you are on calls or video conferences.

If you, your partner and your child live in a two-bedroom home and you’re expecting a new child, you may want an extra room for the baby. Or, you or your partner might have recently lost a parent and want to have an extra bedroom or an in-law suite for your remaining parent to sleep in when they come to visit.

It’s often easier to move to a home that already has the number of bedrooms you want than to try to make a home that is too small for your family work for you.

13. They Want a Home With Dedicated Laundry Space

Plenty of homes either do not have a washer and dryer or do not have the space needed for a laundry room. In some houses, the washer and dryer are combined into a stacked unit that’s tucked away in the corner of a kitchen or hallway. There’s no room for hanging clothes up to dry or for sorting garments on laundry day.

People who don’t have a washer or dryer at home can have an even more challenging experience doing laundry, especially if they live with other people. When there’s no laundry equipment at home, you may need to haul all your clothes, sheets and towels to the nearest laundromat and pay to use the machines there. You may also need to dedicate a few hours to sitting at the laundromat waiting for the wash and dry cycles to finish.

For some people, moving to a house that has its own laundry units or that has a dedicated laundry room is definitely worth it.

What to Do If You’re Considering Moving

In some cases, moving makes sense for you and your family. You can get back free time in your life after a move, enjoy a more affordable life or simply have more room to spread out at home. Whatever your reason for making a move, there are some things to do beforehand, including:

-

- Find out if your employer will pay for the move:If you’re moving for your current job or for a new position, there is a chance your employer may offer to cover the costs of your move. Find out if you qualify for a relocation stipend, and if you do, how much the stipend will be.

- Decide how you’ll move: If you have a relocation stipend, it might be worthwhile to spend some of it on hiring professional movers. A moving company can pack up your belongings, haul them into the truck and transport them to your new place. You might also consider doing the move on your own by renting a truck or van. Another option is to hire a packing cube, pack it yourself and pay a hauler to bring it to your new home.

- Start researching houses in your new area: Before you move, it may be helpful to get an idea of what you can afford in your new area and if the price of housing in that area lines up with your budget. If you’re planning on buying, now is a good time to start the mortgage application and pre-approval process, so you know how much how you can afford to buy and how your budget compares to what’s available in your new hometown.

- Learn as much as possible about the neighborhood and area:There’s more to moving than buying a house. It’s also important to learn about the area as much as possible, particularly your immediate neighborhood. Walk or drive around the neighborhood to see what’s available. Look up the schools, where the nearest hospital is and take a look at what amenities are nearby.

- Compare the cost of living to your salary: Confirm you can afford to live in or near an area before moving by looking at the overall cost of living and comparing it to your current or new salary. Keep in mind that if you currently live in an area with a high cost of living and plan on moving somewhere more affordable while keeping your job, your employer might cut your pay. Some companies offer employees who live in expensive areas out of necessity a cost-of-living increase or supplement. Once you move elsewhere, you might not get the supplement anymore.

[download_section]

Make Your Next Move With Assurance Financial

Ready for a change of scenery or an upgrade to a bigger house? It’s time to get moving! Assurance Financial can help you purchase your home. We’ve streamlined the mortgage application process and have made it quick and easy to do from the comfort of your home with the help of Abby, our digital assistant. If you’re ready to make a move, it takes just 15 minutes to complete our mortgage application and get the ball rolling today.

Sources:

- https://www.census.gov/topics/population/migration/guidance/calculating-migration-expectancy.html

- https://eyeonhousing.org/2020/05/most-home-buyers-want-a-home-office/

- https://www.pewresearch.org/fact-tank/2020/03/20/before-the-coronavirus-telework-was-an-optional-benefit-mostly-for-the-affluent-few/ft_20-03-18_telework_2/

- https://www.weforum.org/agenda/2020/03/working-from-home-coronavirus-workers-future-of-work/

- https://homebuying.realtor/content/why-old-houses-lack-closet-space-and-how-make-modern-adjustments

- https://time.com/3741849/americas-clutter-problem/

- https://www.nytimes.com/guides/realestate/create-an-outdoor-space-garden

- https://realestate.usnews.com/real-estate/articles/is-outdoor-living-space-always-a-good-investment

- https://www.pewtrusts.org/en/research-and-analysis/fact-sheets/2019/04/the-state-of-commuters-in-philadelphia-2019

- https://fee.org/articles/6-stats-that-show-americans-are-drowning-in-stuff-they-dont-need/

- https://www.marketwatch.com/story/more-americans-want-to-downsize-their-homes-than-supersize-them-2017-03-01

- https://www.washingtonpost.com/realestate/why-many-older-home-buyers-are-smart-sizing-rather-than-downsizing/2019/09/18/70a86b56-cb3c-11e9-be05-f76ac4ec618c_story.html

- https://www.sciencedirect.com/science/article/abs/pii/S0272494415000328

- https://pubmed.ncbi.nlm.nih.gov/21856720/

- https://www.parents.com/kids/education/elementary-school/how-ethical-is-it-to-move-to-a-neighborhood-for-its-school-rating/

- https://casafinarealty.com/3-reasons-worth-moving-better-school-district/

- https://insight.kellogg.northwestern.edu/article/why-sending-your-kid-to-the-best-possible-school-may-backfire

- https://www.themuse.com/advice/5-things-you-didnt-know-you-could-negotiate-when-relocating-for-a-job

- https://www.lifestorage.com/blog/moving/reasons-for-relocating-why-do-people-move/

- http://www.harradines.co.uk/news/what-are-the-top-10-reasons-people-move-house/

- https://www.mymovingreviews.com/move/why-do-people-move/

- https://www.siliconrepublic.com/advice/relocating-for-work-things-to-consider

- https://www.remodeling.hw.net/cost-vs-value/2020/

- https://assurancemortgage.com/purchase-your-home/

- https://assurancemortgage.com/meet-abby/

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/downsizing/