Category: Construction

One of the first things you learn when you’re in the market for a new home is that no house is perfect. There will be things you like and dislike about every home you see. That doesn’t mean you need to live with the things you don’t like once you buy a house, though. After your purchase, you can renovate the property to make it suit your tastes and fit your needs.

Depending on the extent and cost of your home improvement goals, you might need to take out a loan for renovations. A home renovation loan is most likely not going to be the same as your mortgage. Learn more about loan options for remodeling your home to see which one will work for you.

Table of Contents

- Why Remodel Your Home?

- Should You Take Out a Loan for Remodeling?

- Can You Add Renovation Costs to Your Mortgage?

- What Loan is Best for Home Improvement?

- Can You Use a Credit Card for Home Renovation?

- Apply for a Home Renovation Loan Today

Why Remodel Your Home?

Whether you buy a home with an eye for renovating it or want to fix up a home you’re already in, there are several reasons why remodeling can make sense. Some reasons to renovate your home include:

- Update the design: Although some designs have more staying power than others, a home can start to look dated if its finishes and fixtures aren’t refreshed from time to time. Remodeling your home can give it a new lease on life and make it look more modern. Plus, a renovation allows you to update your home’s technology so you can bring in features, such as USB outlets and smart appliances.

- Make your home bigger: Your household size might have changed since you first bought the house. Maybe you got married or added to your family. You might feel like your home is bursting at the seams. You can add to the house with a renovation, giving you more bathrooms or bedrooms, as needed.

- Make your home suit your lifestyle: Similarly, your lifestyle and habits might have changed since you bought your home. You might want to turn a bedroom into a home office or finish your basement so the kids can use it as a play area. Maybe your in-laws are moving in, and you want to create a separate suite for them.

- Improve your home’s energy efficiency: Older homes can be much less energy efficient than newer ones, increasing utility bills. Renovating an older home allows you to seal it and stop drafts and other leaks.

- Get on top of maintenance: When you renovate your home, you can replace and update fixtures before needing significant repairs. For example, it’s usually better to replace your roof before it springs a leak and causes damage to the structure of your home.

- Get a good deal on a fixer-upper: If the homes you want to buy are all out of your price range, purchasing a house that needs a little care and attention can help you save money while getting the potential home of your dreams. Depending on the market, it might cost you less to buy and renovate a fixer-upper than to purchase a move-in-ready home.

Should You Take Out a Loan to Remodel Your House?

While you might prefer to pay upfront and in full for a home renovation project, doing so isn’t always possible. If the project’s estimated cost is high, you might need years to save up enough to cover it. In the meantime, you’ll be left living in a home that isn’t quite right. If you haven’t purchased your house yet, home prices might rise in the time it takes you to save for a renovation.

For that reason, taking out a loan to remodel your home can make the most sense for you. If you’re trying to decide if a fixer-upper loan will work for you, here are some things to consider:

- If you can afford the repayments: Whether you’re buying a fixer-upper or are renovating a home you’re living in already, you need to afford the monthly loan payments. Look at your income and current housing costs and calculate whether there’s any wiggle room in there to add on an additional monthly expense. You might also make cuts elsewhere in your budget to afford the renovation loan payments.

- If the renovations increase your property value: While you can’t expect to recoup the entire cost of a renovation if you end up selling your home later on, it can be worthwhile to see if your remodel will make your home more valuable, and if so, how much value it will add to your home.

- If renovating is better than moving: In some cases, it makes more sense to find and buy a new home or build a home from scratch than it does to remodel your existing property. Think about how extensive your renovations will need to be to make your home suit you before you decide to move forward with a renovation loan.

Can You Add Renovation Costs to Your Mortgage?

If you’re buying a home that needs some TLC, it can make sense to see if you can use some of your mortgage to pay for the cost of renovations. In some cases, you have the option of doing that. But you need to choose the right type of mortgage. Most conventional home loans can’t be used to cover the cost of renovations and the home’s purchase price.

To add the cost of remodeling to your home loan, you should look for a renovation mortgage. Then, when you apply for the mortgage, you borrow enough to cover the home’s purchase price plus the cost of the renovation.

When you close on the renovation mortgage, the lender will pay the seller the home’s sale price. The rest of the borrowed amount will go into an escrow account. For example, if your mortgage is $150,000 and the house costs $100,000, the seller will get $100,000, and the remaining $50,000 will go into an account.

The company performing the renovations will have access to the escrow account and will be able to pull payments from it as work continues on the project and milestones are reached. The lender will verify that work is completed before the contractor gets paid.

What Loan Is Best for Home Improvements?

The best way to finance home improvements depends on several factors, including your current homeownership status, the renovation project’s cost, and your credit score. Take a look at some of your loan options.

1. Construction Loan

While many people get a construction loan to cover the cost of building a home from the ground up, you can also get a construction loan to cover the costs of renovating an existing home. Although the application process is similar, a construction loan is slightly different from a mortgage. To get the loan, you need to provide proof of income and undergo a credit check. You’ll also need to make a down payment on the loan.

If you decide to get a construction loan to pay for home renovations, you might need to make a larger down payment than you would for a traditional mortgage. Usually, lenders expect borrowers to put at least 20% down when they finance renovations or new construction. Also, there interest rate on a construction loan might be higher than the interest charged for a conventional mortgage.

After the renovation is complete, a construction loan will typically convert to a mortgage. It can do that automatically, or you might have to go through the closing process again.

2. Fannie Mae HomeStyle Loan

The Fannie Mae HomeStyle loan is a conventional mortgage that also covers the costs of renovating a home. It’s not a construction loan. Instead, your lender will consider the cost of your renovation project when calculating the amount you can borrow. When you close the loan, the seller gets the purchase price, and the rest of the funds go into an account. To get access to those funds, the contractor you hire needs to submit plans for the remodeling project.

There are some benefits and drawbacks to using a Fannie Mae HomeStyle loan to pay for your renovations. One of the benefits of the loan program is that it allows you to buy and remodel a fixer-upper without making a large down payment.

A notable drawback of the HomeStyle loan program is that not every lender offers it. That can mean you need to hunt around to find the loan option. If you find a lender that offers it, you might not get the best loan terms.

3. USDA Home Repair Loan

The United States Department of Agriculture (USDA) offers a home loan program that helps people who want to purchase property in rural or suburban areas get a mortgage. The USDA also has a program designed to help borrowers pay for remodeling a home. Since USDA loans are intended for people who otherwise wouldn’t get a mortgage or loan, you need to meet specific requirements to qualify for the program.

First, the home needs to be in the right area. You can’t use a USDA loan to pay for renovations on a home in a city or urban environment.

Second, your household income needs to be less than 50 percent of the median income in your area. You also need to own and live in the home you’ll be renovating.

The maximum amount you can borrow through the USDA’s Home Repair loan program is $20,000 as of 2021. You can use the funds to repair or modernize the home or get rid of health and safety hazards.

4. FHA 203(k) Loan

The Federal Housing Administration (FHA) loan program helps people who might not have the best credit score or a big down payment to purchase a home. The FHA 203(k) program is similar but designed for people looking to buy a house to renovate.

With an FHA 203(k) loan, you can finance up to 110% of the appraised value of the property or the cost of the property plus the cost of the remodel, whichever is less. To get the loan, you need to work with an FHA-approved lender that offers 203(k) loans. Not all FHA lenders offer 203(k) loans.

Like typical FHA loans, the FHA 203(k) loan program provides funding to borrowers who might not qualify for conventional mortgages or construction loans. The credit score requirement is lower than for conventional loans, and you can put down as little as 3.5%. You will need to pay mortgage insurance for the life of the loan, which can be a drawback for some borrowers.

5. Refinance Loan

If you’ve been living in your home for a while, already have a mortgage and want to make some home improvements, refinancing your current home loan can be one way to pay for your renovations. When you refinance, you can tap into the equity in your home and use it to cover the cost of your project.

With a refinance, you trade one mortgage for another. The new mortgage might have a lower interest rate than your current one or it might be for a higher amount than your current home loan.

For example, when you first purchased your home, you took out a $200,000 mortgage and put down 20% on a $250,000 home. You had $50,000 in equity from the start. Now, you’d like to spend $50,000 on a home renovation project. You currently have $180,000 left on your mortgage.

To get the $50,000 you need for the home renovation, you refinance your existing mortgage to one worth $230,000. The $180,000 goes toward paying off the first loan and you get $50,000 in cash to pay for your renovation.

Refinancing might be a good option but it’s not always the best choice. When you refinance, you do have to pay closing costs all over again, which can add to the cost of your renovation project. Also, depending on when you refinance, you might end up paying a higher interest rate on your new mortgage.

6. Home Equity Loan

As you pay down your mortgage, you build equity in your home. The lower your mortgage is compared to the value of your home, the more equity you have. If you decide to sell your home, you get to pocket the equity from the sale and use it to buy a new home or reach other financial goals.

You can also use your home’s equity to finance renovations. One option is to refinance your loan, as described above. You can also borrow against your home’s equity, either by taking out a line of credit or getting a separate home equity loan.

Similar to your mortgage, a home equity line of credit or loan is backed by your home. If you have trouble repaying the loan or lien of credit, there is a risk of losing your property.

How much you can borrow against your home’s equity depends on the type of loan you get. With a home equity loan, you receive the payment in one lump sum. You then repay it over time, in equal monthly installments.

You can borrow as needed during the draw period with a home equity line of credit. If you repay the amount, you can borrow more. A home equity line of credit is similar to a credit card in that way. Once the draw period is over, though, you’ll need to start repaying it and won’t be able to borrow more.

7. Personal Loan

A personal loan is an unsecured loan that you can use for pretty much any purpose. Since there’s no collateral behind a personal loan, it will most likely have a higher interest rate than a mortgage or home equity loan. But you also have more freedom when it comes to using the loan money. The process of applying for and receiving a personal loan can also be more straightforward and cheaper than the process of getting a mortgage.

Whether you decide to get a personal loan or not depends on how much equity you have in your home and the size of your renovation project. If you’re just making a few small repairs or minor upgrades, it can make more sense to use a personal loan for your project. But if your renovations will be extensive, a construction loan, refinance or home equity loan might make more sense.

[download_section]

Can You Use a Credit Card to Pay for Home Renovations?

In some cases, it can make sense to use a credit card to pay for a home remodel. But before you do so, it’s important to know the drawbacks.

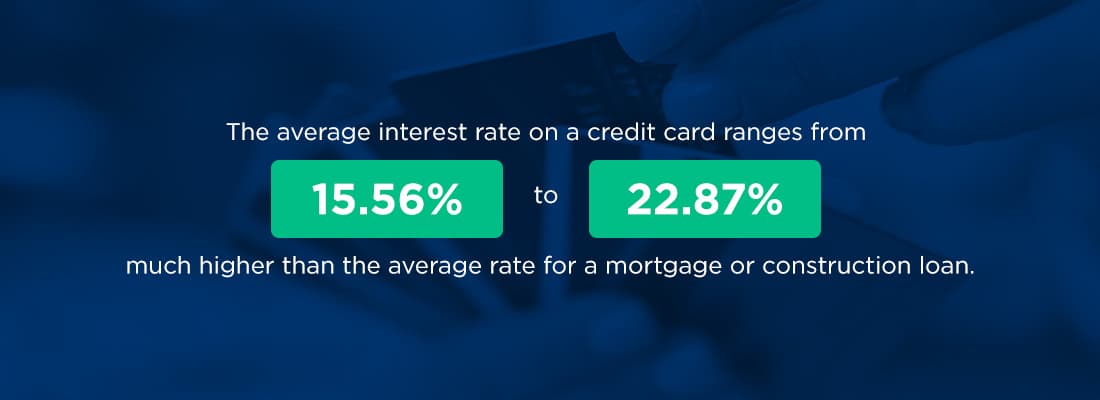

Perhaps the biggest disadvantage of using a credit card for a renovation project is the high-interest rate. The average interest rate on a credit card ranges from 15.56 to 22.87%, much higher than the average rate for a mortgage or construction loan. Credit cards also tend to have higher interest rates than personal loans. A higher interest rate means that you’ll end up paying much more in the long run if you use plastic to fund your remodel rather than a refinance or another type of home loan product.

There’s also your credit limit to consider. Many credit cards have credit limits that are much lower than what you can borrow with a construction loan or home equity loan. If your card has a $10,000 credit limit, you’ll either need to pay it off in full before using it again or use a different card to pay for the rest of your project.

There are some instances when using a credit card to pay for a remodeling project can make sense, though. If the project is small and you know you’ll pay it off quickly, a credit card can be the quickest and easier way to pay. Also, if you have a card that has a 0% interest introductory offer and you pay the project price in full before the introductory period ends, you can stand to save a considerable amount in interest.

Generally speaking, though, credit cards are best used for everyday or emergency purchases and shouldn’t be used to finance major projects such as a home renovation.

Apply for a Home Renovation Loan With Assurance Financial Today

If you want to remodel your home, you have options when it comes to paying for it. Assurance Financial can help you make sense of your home renovation loan options and choose the one that’s best for you. We offer construction loans and refinancing as well as USDA loans to qualified borrowers. Get started on your application today.

Linked Sources:

- https://assurancemortgage.com/construction-loans/

- https://assurancemortgage.com/how-to-finance-new-construction/

- https://www.rd.usda.gov/programs-services/single-family-housing-programs/single-family-housing-repair-loans-grants

- https://assurancemortgage.com/everything-need-know-fha-loans/

- https://www.hud.gov/program_offices/housing/sfh/203k/203k–df

- https://assurancemortgage.com/guide-to-cash-out-refinancing/

- https://assurancemortgage.com/is-refinancing-a-bad-idea/

- https://assurancemortgage.com/building-home-equity/

- https://money.usnews.com/credit-cards/articles/average-apr

- https://assurancemortgage.com/apply/

Finding a home that’s just right for you can be like looking for a needle in a haystack. The houses you visit might not be large enough, or they might be too big. They might not be located in a convenient area, or they might be in a place that’s too busy or noisy. The homes you view might not have the amenities you dream about or need to have in your residence.

If your house hunt is leaving you cold, you still have options. One option is to build your next home from the ground up instead of buying an existing house. Building a new home has many benefits. You can choose the style of the house, the number and type of rooms and the materials used.

Buying new construction is slightly different from buying an existing home in another way. The rules for loans and financing for new home construction aren’t exactly the same as they are for buying homes that already stand. Often, you’ll need to take out a construction loan first, which can convert to a mortgage once your home gets built. If you’re leaning toward building a new home, get all the details on the lending process.

Topics Covered

- FAQs About Home Construction Loans

- 1. How Do You Get Financing for a New Construction?

- 2. Is a Construction Loan a Mortgage?

- 3. What Does a Construction Loan Pay For?

- 4. What Type of Credit Score Do You Need?

- 5. How Much Can You Borrow?

- 6. What Are Interest Rates Like on Construction Loans?

- 7. What Percent Are You Asked to Put Down for a Construction Loan?

- 8. Do All Lenders Offer Construction Loans?

- 9. Is It Hard to Get a New Construction Loan?

- 10. Can I Build My Home Myself?

- Single-Closing vs. Two-Closing Transactions

- How to Finance New Construction: Types of Loans Available

FAQs About Home Construction Loans

Curious about the process of getting a construction loan? You likely have some questions. Let’s answer some of the most commonly asked questions about getting a home construction loan

1. How Do You Get Financing for a New Construction?

The process for getting a construction loan starts with an application. Most prospective home builders apply to several institutions to see what kinds of rates and loan terms are available to them. As you apply, you’ll provide detailed construction project information, including the contractor you’re working with, the building plans and timeline, and costs of materials and labor.

When approved for the loan, the borrower will place a down payment, or if they already own the land, they may be able to use the equity in their land as the down payment. The loan will finance the construction, and payment is due when the project is complete.

2. Is a Construction Loan a Mortgage?

Although a construction loan pays for the cost of building a home, it’s technically not a mortgage. A mortgage needs collateral, in this case, your home. When you are building a home, there isn’t anything to serve as collateral yet. Instead, a construction loan is a short-term loan that you either pay off once when the project is finished or convert into a mortgage.

3. What Does a Construction Loan Pay For?

Construction loans pay for most of the things involved in building a new home. The proceeds from the loan typically get paid to the contractor in installments or as certain building milestones are reached. The money can cover the cost of permits, materials and labor. The loan can also pay for the land purchased for the home.

4. What Type of Credit Score Do You Need?

Usually, borrowers need to have good credit with a score of at least 680 to qualify for a construction loan. The exact credit requirements can vary by lender and loan program. Some loan programs help people with lower credit scores purchase a new home and might be an option for you if your score is on the lower end.

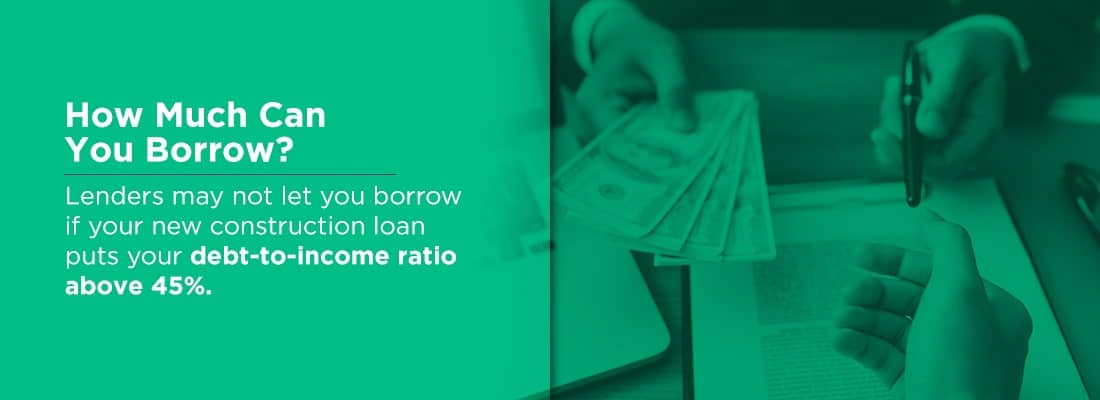

5. How Much Can You Borrow?

How much you can borrow to build a new home depends on your income, the size of the down payment, and any other debts you have. Lenders may not let you borrow if your new construction loan puts your debt-to-income ratio above 45%. In other words, the amount you owe per month, including rent, credit card payments, and your new construction loan, should not be greater than 45% of what you earn each month.

6. What Are Interest Rates Like on Construction Loans?

The interest rate on a construction loan is likely to be slightly higher than the rate you’d pay on a standard mortgage. Once the loan converts to a typical mortgage, though, the rate might be more in line with what you’d pay to purchase an existing home.

7. What Percent Are You Asked to Put Down for a Construction Loan?

It depends on the construction loan you take out, but often, these loans require a higher down payment than other types of mortgages. If you apply for a conventional construction loan, you might be requested to put down between 20% and 30% upfront. With government-sponsored loans, a smaller down payment, such as 3.5%, is possible. Some construction loans have higher down payment requirements because lenders consider them higher-risk than standard mortgages.

8. Do All Lenders Offer Construction Loans?

Some lenders offer construction loans while others don’t. When looking for a loan, it’s a good idea to shop around. Luckily, Assurance Financial offers construction loans and can help you get started any time.

9. Is It Hard to Get a New Construction Loan?

In some cases, it can be harder to qualify for a construction loan than for a standard mortgage. But many loan programs make the process go smoothly and offer more accessible construction loans.

10. Can I Build My Home Myself?

Many construction loan programs require you to work with a licensed and insured contractor and ask you to submit plans before your loan is approved. If you’re a professional contractor, you might be able to build your own home. Otherwise, expect to work with a pro.

Single-Closing vs. Two-Closing Transactions

Two categories of construction loans exist — construction-only loans and construction-to-permanent loans. Construction-only loans are also called two-closing loans, as you will go through the closing process a second time should you need a mortgage once your home is built. A construction-to-permanent loan is sometimes called a single-closing loan, as it automatically converts to a mortgage after construction is complete.

Single-Closing Loan

A single-closing transaction requires less paperwork and can be less expensive than a two-closing loan. You don’t go through the closing process twice, so you only pay one set of closing costs. While you initially might pay less out of pocket for a single-closing loan, the interest rate you pay might be higher than if you were to apply for a traditional mortgage. The interest rate is typically locked in at closing.

Single-closing transactions can have strict underwriting guidelines. Your lender is likely to calculate the loan-to-value (LTV) using the appraised value or the acquisition cost, whichever is less. The LTV is the value of your loan compared to the value of the property. Lenders use it to assess risk, determine interest rates and see if you need to pay private mortgage insurance (PMI).

During the building process, the lender will make payments to the contractor on a set schedule. As the home is built, the borrower can either make interest-only payments or decide to defer payments until the loan converts to a permanent mortgage.

Once construction finishes, the loan turns into a permanent mortgage automatically. The borrower begins making principal and interest payments based on the term of the loan.

Two-Closing Loan

Two-closing transactions are the most common. They have a more flexible structure and more flexible underwriting guidelines. The LTV is calculated using appraised value, and equity is considered towards down-payment.

Unlike a single-closing loan, when you decide to get a two-closing or construction-only loan, you’ll go through the loan application process twice. Doing so has its benefits and drawbacks. An advantage of getting a construction-only loan is that it gives you more leeway when it’s time to apply for a mortgage. You can shop around for the best rate and terms and aren’t locked into the rate offered on the construction loan.

A drawback of a two-closing loan is that you will go through closing twice. That means you’ll need to apply for a mortgage once your home is ready, and you’ll sign a whole new set of documents. You’ll also pay closing costs twice.

Since you have the opportunity to get a better interest rate on your mortgage with a two-closing loan, you may save money in the long run, even though you pay closing costs again.

Construction-only loans are due as soon as the project is complete. Usually, the term of the loan is short — about a year, if not less. If a borrower has trouble finding a mortgage to pay the remaining principal on the construction loan, they might find themselves with a big bill after their home is move-in ready.

How to Finance New Construction: Types of Loans Available

Just as you have choices when buying an existing home, you have mortgage options when looking into buying new construction. Several loan programs offer construction loans as well.

FHA Loans

The original goal of the Federal Housing Administration (FHA) loan program is to make homeownership affordable for as many people as possible. FHA loans make getting a mortgage more accessible in a few ways. They typically have lower down payment requirements than other types of mortgages. If you want to get an FHA construction loan, you can put down as little as 3.5%. Credit requirements are also looser with FHA Loans. You can have a credit score in the 500s and still be eligible for a mortgage.

FHA loans are guaranteed by the Federal Housing Administration but don’t come from the government itself. Instead, you apply for the mortgage through an approved lender. The lender reviews your credit, income, and other documentation before deciding whether to approve you for the loan and how much interest to charge.

The type of FHA loan you apply for depends on the type of construction project you’re undertaking. If you’re building a home from scratch, you’ll apply for a single-closing, construction-to-permanent FHA loan. At the start of the process, the lender dispenses funds to the builder to cover the cost of construction. When the home is complete, the loan converts to a traditional FHA mortgage.

The other option is for people who are renovating an existing home. An FHA 203(k) loan covers the cost of rehabilitating a fixer-upper or other house that needs some TLC. You can use an FHA 203(k) loan to renovate your current home or to purchase and renovate a new home.

Two forms of 203(k) loans exist — standard and limited. The standard 203(k) is for larger projects that cost more than $35,000. The limited loan covers projects with a price tag under $35,000. One thing to remember if you’re considering an FHA loan is that the loan will require you to pay a mortgage insurance premium. You’ll pay a premium upfront and for the duration of the loan term.

VA Loans

The Department of Veterans Affairs offers VA loans to help veterans and current service members purchase homes. Like FHA loans, VA mortgages come from private lenders and are guaranteed by a government agency, in this case, the Department of Veterans Affairs. Also similar to an FHA loan, a VA loan lets you purchase a home with a limited down payment. In the case of a VA loan, you might be able to buy a house with zero down.

VA construction loans have relatively strict requirements. In addition to being a current or former member of the armed services, you may need to meet several other requirements before you can qualify. Not all lenders that offer VA loans offer VA construction loans, so you might be required to dig around before finding an eligible lender.

When considering applying for a VA construction loan, the first thing to do is to find a licensed, insured builder. You may be required to work with a professional builder if you want to use the VA program to buy your new construction home. The program doesn’t allow owners to build their homes. Next, you and the builder will work together to create plans for the home. You’ll submit those plans to the lender when you apply. You’ll also submit documentation about the building materials and the lot.

For you to qualify for a zero-down payment on a VA construction loan, the home needs to be appraised. The design of the house can’t be too unique or unusual, nor can the house be larger or more luxurious than others in the area. A home that is too “out there” will have a lower appraisal value than a house that’s more standard. Getting a low appraisal can mean you can’t qualify for a zero-down payment.

After closing on the loan and building your new home, the property will need to pass an inspection by the VA. If it passes inspection, the loan converts to a permanent mortgage.

USDA Loans

USDA loans are also backed by a government agency, in this case, the United States Department of Agriculture. The loans are traditionally meant to help lower-income households purchase a home in a rural or suburban area. Like VA loans, the USDA loan program offers 100% financing in some circumstances, meaning a borrower can buy a home with zero down.

It’s possible to get a construction-to-permanent loan as part of the USDA loan program, although it’s worth noting that the list of lenders who offer USDA construction loans is more limited than the number of lenders who offer USDA loans. If you decide to apply for a construction-to-permanent USDA loan, there are several things to keep in mind. First, you need to meet income requirements. The maximum household income you can earn varies based on location and the size of your household.

Second, you need to build your home in an eligible area. The new house isn’t required to be in a completely under-developed area, but it can’t be in a metropolitan or urban location. Some suburban neighborhoods are eligible for USDA loans, as are most rural areas. As with a VA construction loan, you need to work with an approved builder if you’re going to apply for a USDA construction loan. You can’t build the home yourself.

Like an FHA loan, you’ll be required to pay mortgage insurance when you take out a USDA loan. The insurance remains in place for the life of the loan. You might also pay a slightly higher-than-average interest rate on a USDA loan than on other types of mortgages.

USDA construction loans are usually hard to find. While many lenders participate in the USDA’s loan program, only a few participate in the construction loan program. Depending on your home-building goals, you might be better off choosing a different type of construction loan.

Conventional Loans

Although government-guaranteed loan programs can help people build and buy their homes, they aren’t the right choice for everyone. You might not qualify for government-backed loans, or you might want to buy a home in an ineligible area. While some loans, like FHA loans, make it possible to buy a home with a lower down payment, their mortgage insurance requirements can be a turn-off for some buyers.

Fortunately, it might be easier to qualify for a conventional construction-to-permanent loan than you think. Although many people believe that you need a large down payment to get a traditional mortgage, especially when you’re building a home, there are programs available that will accept a down payment as low as 3%. The size of your down payment depends on the appraised value of the home.

If you do put down less than 20% on a construction-to-permanent loan, you can expect to pay private mortgage insurance. However, unlike the mortgage insurance attached to an FHA loan, you can stop paying the premiums as soon as your LTV reaches 80% When your LTV reaches 78%, the mortgage insurance premiums will automatically terminate.

Your credit score is likely to matter more when you apply for a conventional construction-to-permanent loan than it does for a government-sponsored loan program. Ideally, you’ll want a score above 700, with a score over 740 being ideal. The higher your score, the less risky you look as a borrower. That can mean you get a lower interest rate and better loan terms from a lender.

Should you decide to go the conventional mortgage route, you have two options, depending on the value of your home. You can apply for a conforming loan, meaning the price of your home falls under the limits set by the Federal Housing Finance Agency. The conforming loan limit changes annually based on inflation. It is higher in areas with a higher cost of living and cost of homeownership.

If you’re planning on building a large, luxurious home, it’s likely that the cost of the project and the appraised value of the house will be above the conforming loan limit. In that case, you may be required to apply for a jumbo loan or a non-conforming loan. Jumbo loans can be up to $2 million. Since jumbo loans are above the limit, they don’t have the same protections as conforming mortgages. As a result, they often have higher interest rates and might require a larger down payment from the borrower.

Apply for a Construction Loan With Assurance Financial Today

Your dream home can be closer than your think. Assurance Financial offers several construction-to-permanent loan programs that will provide you with financing to build your home from the ground up.

We also offer an easy online application process. In just 15 minutes, you can see what your eligibility is. Get started today so you can begin your new construction project.

Sources:

- https://assurancemortgage.com/remodeling-construction/

- https://www.businessinsider.com/personal-finance/construction-loan

- https://assurancemortgage.com/fha-loans/

- https://www.hud.gov/program_offices/housing/sfh/203k/203k–df

- https://assurancemortgage.com/va-loans/

- https://assurancemortgage.com/usda-loans/

- https://www.rd.usda.gov/programs-services/single-family-housing-programs/single-family-housing-guaranteed-loan-program

- https://crsreports.congress.gov/product/pdf/RS/RS20530

- https://www.fdic.gov/consumers/community/mortgagelending/guide/part-1-docs/fannie-standard-97-percent-loan-to-value-mortgage.pdf

- https://assurancemortgage.com/appraisal-process-construction-financing/

- https://www.consumerfinance.gov/ask-cfpb/what-is-private-mortgage-insurance-en-122/

- https://www.consumerfinance.gov/about-us/blog/bad-credit-or-no-credit-when-you-want-buy-home/

- https://assurancemortgage.com/jumbo-loans/

- https://www.consumerfinance.gov/owning-a-home/loan-options/conventional-loans/

- https://assurancemortgage.com/apply/