Finding out you’re pregnant can come with a whole litany of emotions. Especially if it’s your first baby, you know you’re embarking on a whole new chapter of your life. Another exciting new chapter of life is when you purchase a home.

When these major life events overlap, you may find that excitement is overshadowed by anxieties and stress. Buying a home while you’re expecting a baby or on maternity leave can be challenging, but it doesn’t have to be. Our guide will help you navigate through the process of applying for a home loan while pregnant or after you’ve recently welcomed a new baby.

There are many reasons why someone might be denied when they apply for a home loan. Lenders must feel confident that applicants will keep up with their payments. This requires taking a detailed look at an applicant’s current situation in order to predict their future ability to pay off their loan. However, for some, their current situation may be a special circumstance that doesn’t necessarily indicate what their future will hold. One example of this type of situation is a pregnancy.

This is not an issue if you’re purchasing a home with a spouse or partner who could get approved on their own. If that is the case, you could still choose to apply jointly or could allow your partner to apply on their own, which could simplify the process. However, if you depend on both your and your co-borrower’s incomes to qualify for a mortgage, or if you are applying for a home loan on your own, then it’s critical you know how a pregnancy or new baby might affect the process.

You may have heard that pregnancy could keep you from getting a home loan, so it’s easy to feel like the odds are stacked against you when you’re applying for a mortgage while on maternity leave. Fortunately, you cannot legally be denied a mortgage just because you are pregnant. However, the financial implications of pregnancy can create some challenges in the home loan application process that make it more difficult for lenders to predict your future ability to make payments. So, can you be denied just because you are pregnant? No. But, does pregnancy affect a mortgage application? Quite possibly.

Do You Have to Disclose Pregnancy When Applying for a Mortgage?

It is understandable if you are hesitant about telling a mortgage lender you are pregnant or on maternity leave, considering how this information could affect their decision. If you are on parental leave while you’re trying to obtain approval for a mortgage, one issue is that you likely aren’t receiving paychecks equal to what you would normally receive.

Additionally, it may be unclear exactly what your future employment situation will look like. Perhaps you’ll want to switch to part-time when you go back to work, for instance. All these factors can put mortgage lenders on the alert since they make it more difficult to predict whether you’ll be a reliable borrower.

Being pregnant in and of itself shouldn’t affect your application at all. In fact, there is no place on a loan application where you are expected to indicate whether you’re pregnant, so this information can be kept completely private.

A mortgage lender does not have the right to ask you whether you are pregnant or on maternity leave when you apply for a loan. You are under no obligation to tell them about your pregnancy or maternity leave. However, it is generally recommended that you do disclose this information because these life changes can have a significant effect on your household finances, which your lender needs to know about.

If you do tell your lender about your maternity leave, they are not permitted to operate under the assumption that you won’t return to work once your leave ends, which takes most of the risk out of telling them. In addition, if your lender contacts your employer to confirm your employment and income, your employer is free to inform them of your maternity leave status.

To better understand how maternity leave can affect the process, let’s take a moment to look at how maternity leave typically works.

Maternity Leave and Mortgage Approval

Parental leave looks different depending on factors like where you’re employed, how long you’ve worked there and your personal preferences. Most companies are required to provide up to 12 weeks of unpaid family leave to their employees, as long as the employee has been working there for at least a year and could leave for a while without causing the company serious financial harm. Parental leave ensures an employee’s job will still be there waiting for them when they return from their time with their new child.

Some companies may offer their employees paid parental leave. Mortgage lenders look more favorably on this type of leave. More frequently, however, employees use other forms of paid time off, such as vacation days or sick leave to cover part or all of the time they’re away.

For most parents who take time off to bond with their new child, the financial benefits come through a combination of paid time off benefits from work and short-term disability benefits through their employer-provided insurance. Some states require employers to offer this type of insurance coverage for temporary medical needs.

Regardless of what sort of parental leave arrangement you have, in the world of mortgage lending, maternity leave is considered a type of temporary leave, according to the U.S. Department of Housing and Urban Development (HUD), Fannie Mae and Freddie Mac. In any temporary work situation, there can be challenges to getting approved for a home loan, but our tips below could help you get approved.

How to Get a Home Loan While Pregnant or on Maternity Leave

To bolster your chances of getting approved for a loan while you’re pregnant or on maternity leave, you should focus on making yourself a strong candidate overall for a loan, choosing a loan you can afford and making the terms of your maternity leave completely clear to the mortgage lender. Consider these actionable tips, so you can start preparing to apply for a home loan today:

1. Obtain a Loan Before You Go on Maternity Leave

Since closing on a house while on maternity leave can be tricky, you’re better off to purchase a home before you go on maternity leave, if possible. This isn’t just so you’ll have an easier time obtaining a mortgage. It should also make for a smoother transition. Some couples may feel overwhelmed with preparing for the arrival of a baby and want to put off purchasing a home until after the baby is born, and they are on maternity leave, paternity leave or both.

The reality, however, is that this is a time of transition where most parents will have their hands full caring for their newborn, making this an especially challenging time to deal with applying for a home loan, going house hunting, and moving. If you know you plan to purchase a home, start searching early, or choose to wait until after you’ve had your baby and gone back to work. We understand, however, that there are situations when you may not have a choice but to apply for a loan while on maternity leave.

2. Cushion Your Savings Account and Minimize Debt

If you need to submit a loan application on maternity leave, you can boost your chances of getting approved by optimizing your financial situation outside of your temporary change in income. This means avoiding taking on any new debt and paying down any debt you have, as well as cushioning your savings account.

Lenders will factor in the money you have on standby along with your income to determine whether you can afford a loan, so if your income appears to be lacking, you can make up for this in the money you have saved. Since there are costs associated with giving birth and caring for a child, lenders may factor in these expenses, so having more money saved will show you’re prepared to make your payments, even with the added costs you’re soon to or already experiencing from having a baby.

3. Find Out the Details of Your Parental Leave Arrangement

As you near the end of your pregnancy, it’s always wise to talk with your employer to make sure you are on the same page and understand the terms of your upcoming maternity leave. Make sure you have a plan for how long you’ll be gone, what compensation you’ll receive while you’re away and what your schedule will look like when you return.

Determining the details of your parental leave is especially important when you’re seeking a home loan — the more information you can provide to your lender, the better. If you can demonstrate to your lender that your parental leave won’t mean a sudden stop in your income or an indefinite employment future, you may be able to set their mind at ease and secure a loan.

4. Determine What You Can Afford

When buying a home, it’s always critical to carefully assess your current and future financial situation to determine what mortgage payment you can afford. This is true no matter what stage of life you’re experiencing and whether a pregnancy is in the picture or not. You’re more likely to get approved for a loan that fits comfortably within your budget than one that pushes the limits of what you can afford, so it’s wise to make sure you don’t stretch yourself too thin. This is what lenders fear and what leads to foreclosures.

If you’re expecting an addition to your family, this can impact your future financial situation, so it’s especially important that you take the time to figure out what sort of mortgage payment you can reasonably afford. Deduct medical costs associated with a birth and checkups for your infant, child care, and whatever other new expenses you’ll incur. Your lender will be thinking about these expenses, too, so it’s helpful if you can show you’ve thoughtfully considered your budget and are asking to borrow a reasonable amount.

5. Choose the Right Home Loan

Another piece of advice that applies to anyone looking to get approved for a mortgage is to choose the right loan option. This may mean doing some research and shopping around with different lenders to compare quotes. A loan adviser can help apprise you of your options and help you make the right choice. Choosing the right loan is critical if you want to get approved.

In addition to conventional loans, there are special types of mortgages for veterans, people with low credit scores, people borrowing a lot, and other special circumstances. Find the right type of loan, an interest rate you’re comfortable with, and the best plan for paying back your loan. Typically, conventional loans are designed to be paid off in 10, 15 or 30 years. If you’re stretching a bit financially, you’ll likely want to go with a longer period, so each payment is lower and fits better in your budget.

If you apply for a home loan while pregnant, but before you go on maternity leave, you aren’t required to let your lender know, though they will likely ask whether you know of any upcoming changes to your household expenses, and the answer here would be yes. While you aren’t legally required to mention your pregnancy at all, if you’re applying for a home loan near the end of your pregnancy or just after you’ve had your baby, you’ll need to go the full disclosure route.

Let your lender know the details of your maternity leave, and let them know you’ve thought ahead and have calculated all your expenses, so you aren’t spreading yourself too thin with the loan you plan to take out. Within 10 days of closing on your home, your lender can call your employer to make sure you are still employed there and to verify your salary, so make sure your employer is prepared for this call and that there are no surprises for your lender if your employer states that you’re currently on leave.

How to Report Maternity Leave Discrimination

A mortgage lender will likely ask for proof of employment and income, especially if you’re on leave from your job for maternity reasons or otherwise. While mortgage lenders want to make loans, they must be careful about who they grant loans to. All mortgage lenders sell their loans, which means they need to be certain the loan will be purchased by an investor after the loan is made.

Because selling loans to investors can be a tenuous process, some lenders are quite conservative about who they select for loans. In particular, some lenders will be less flexible about lending to a borrower on any sort of leave, including maternity leave. Some mortgage lenders can cross the line from being cautious to discriminating against pregnant women.

Although it is normal for the loan qualification process to involve jumping through some extra hoops, a lender should never require a pregnant woman to end her maternity leave and return to work in order to receive mortgage loan approval. In fact, the U.S. Department of Housing and Urban Development (HUD) has deemed doing so a violation of the Fair Housing Act.

Still, the HUD has received complaints from borrowers about being discriminated against by mortgage lenders due to being on maternity leave. In response to these complaints, the HUD has fined many mortgage companies millions of dollars over the years, including large organizations like Wells Fargo Home Mortgage. If you feel a mortgage lender is violating your rights and breaking the law, you can file a complaint with the HUD online, over the phone or through the mail. The HUD will investigate your claim and issue a determination on the case at no cost to you.

[download_section]

What You Need to Get Approved

There are some important documents you’ll need to get approved for your home loan. Some of these documents are common to all applicants, and some are unique to applicants on maternity leave. When you’re applying for your mortgage, be prepared to submit the following documents:

Tax returns: Tax returns provide lenders with a detailed history of your income, which can help them predict how consistent your income will be in the future. Lenders may ask for one or two years’ worth of tax returns. Pay stubs can show what your current income is, but tax returns give a bigger picture to your lender of what your income looks like over the course of a year or two.

Proof of income: To show your current earnings, you’ll need to provide some sort of proof of income. This will commonly come in the form of pay stubs, but it may look different if you are self-employed or receive alternative sources of income. For example, you could provide a record of direct deposits into your bank account of 1099 forms.

Bank statements: Bank statements show your lender how much money you have on standby to cover a down payment and to provide some cushion to help you pay your mortgage even if you have some unexpected expenses come up. You may also need to provide documentation of other assets, such as life insurance.

Gift letter: If you’re fortunate enough to have a family member or friend who wants to help you purchase a home by giving you a financial gift, then you’ll need them to write a gift letter, letting the lender know the money is from them and is not a loan. Lenders check to see how long money has been in your account, so if they see a large sum show up seemingly out of nowhere, they’ll want it to know about it.

Maternity leave verification: If you’re on maternity leave, it’s critical that you have your employer compose an official, signed letter on the company letterhead that confirms the details of your leave. It should, at the least, state when you plan to return to work and whether there will be any change to the number of hours you work.

Having these documents ready to go will streamline your application process and will enhance your chances of getting approved, assuming your finances are in a state that will allow you to afford to purchase a home, even if you are temporarily on leave.

Lending Discrimination Laws

The Fair Housing Act is meant to prevent discrimination in housing over the basis of things like ethnicity, religion, sex, and more. One type of prohibited discrimination specified by the act is discrimination based on familial status — this includes women and couples who are expecting a baby.

Another law to be aware of is the Family and Medical Leave Act. This is the law that entitles most employees to time off without worrying about their job security for qualified medical and family reasons, which includes having a baby. The only exceptions are if you have newly been employed by a company, if the company is extremely small or if your salary is in the very top tier of the company, which indicates that your absence will have significant consequences for the company.

Eligible employees are entitled to 12 workweeks of leave over the course of a 12-month period, as long as those 12 weeks are within a year of their child’s birth. Most parents choose to take off just before or at the time of birth and use most of the leave for bonding with and caring for their new baby. This law is not gender-specific, so both mothers and fathers are entitled to parental leave.

Taking both of these laws into account, new parents are well within their rights to take time off to have a baby and to buy a house during this time. If a mortgage lender doesn’t want to approve your application simply because you have a new baby or a baby on the way, this is technically a violation of the Fair Housing Act. However, it isn’t always so simple. This is because mortgage lenders are allowed to reasonably evaluate whether you are a reliable or a high-risk borrower based on your financial history, current situation, and future.

Banks are often leery of granting loans to pregnant mothers because of the financial risks associated with this stage of life — this is why hedging your bets in every way possible to show you are a reliable borrower is crucial. If you think you have been discriminated against purely on the basis of pregnancy, you may want to seek legal counsel or simply try another lender.

Apply for a Home Loan With Assurance Financial

Does being on maternity leave affect mortgage applications? Yes. Does it mean you are automatically disqualified from buying a home? Absolutely not. Make sure you work with an understanding and attentive lender to work through the mortgage application process, so they see the full picture of your financial situation and not just a glaring risk.

At Assurance Financial, we care about our customers, no matter their stage of life. We work with you to help you find the best loan option for your budget and your preferences, so you can focus on welcoming your new baby into your family instead of stressing over the complicated process of buying a home. We have experts licensed in 43 states to guide you to the best, customized option for your life stage. You can also apply online with Abby in just 15 minutes. Get started today to get one step closer to owning a home perfect for your whole family.

The amortization schedule is a record of your loan payments that shows the principal amounts and the interest included in each payment. The schedule shows all payments until the end of the loan term. Each payment should be the same per period — however, you will owe interest for the majority of the payments. The bulk of each payment will be the loan’s principal. The last line should show the total interest you paid and your principal payments for the full term of the loan.

The process of obtaining a mortgage can feel overwhelming, especially for first-time homebuyers. Many of the mortgage-related terms may be new to you, such as conforming loans, non-conforming loans, fixed interest rates, adjustable interest rates, and loan amortization schedules.

The amortization schedule for a mortgage is an essential component to understanding the breakdown of your payments during the term of your mortgage.

Still have questions or need more information? Below is an overview of what this article covers!

What is loan amortization? Loan amortization is the schedule of periodic payments for a loan and gives borrowers a clear picture of what they’ll be repaying in each repayment cycle. You’ll have a fixed, consistent repayment schedule over the entire period of your loan term.

1. Loans That Get Amortized

Amortization schedules are typically used for installment loans with known payoff dates, fixed interest rates and fixed monthly payments, such as:

Mortgage loan: Most conventional home loans are 15-year or 30-year terms with a fixed interest rate. Though many homeowners may not keep their mortgage that long, such as if they sell their home or refinance, the loan functions as if you are going to keep it for the entire 15-year or 30-year term.

Car loan: Many car owners obtain an amortized auto loan for a term of five years or less. Some drivers decide whether they can afford a car based on what their fixed monthly payment will be.

Personal loan: A personal loan you can obtain from a credit union, bank or an online lender also tends to be amortized. Typically, personal loans are given for a term of three years at a fixed interest rate with a fixed monthly payment. Personal loans are generally used for debt consolidation or small personal projects.

You will pay these loans off with consistent payments until the balance is zero.

2. Loans That Don’t Get Amortized

Not every type of loan is amortized. The following are examples of loans that don’t get amortized:

Mortgage loan: Most conventional home loans are 15-year or 30-year terms with a fixed interest rate. Though many homeowners may not keep their mortgage that long, such as if they sell their home or refinance, the loan functions as if you are going to keep it for the entire 15-year or 30-year term.

Car loan: Car owners typically get an amortized auto loan for a term of five years or less. Some drivers decide whether they can afford a car based on what their fixed monthly payment will be.

Personal loan: A personal loan you can obtain from a credit union, bank or an online lender also tends to be amortized. Typically, personal loans are given for a term of three years at a fixed interest rate with a fixed monthly payment. Personal loans are generally used for debt consolidation or small personal projects.

If you apply for any of these types of loans, don’t expect an amortization schedule.

3. Composition of an Amortized Loan Payment

Payments for your loan go toward:

Principal: This portion of your payment goes toward reducing the balance of your loan.

Interest: This portion of your payment is what you pay your lender for loaning you money.

You make payments in regular installments of a set amount, though the ratio of interest to principal changes over the repayment period. This change in the ratio of interest to principal is detailed further in a loan amortization schedule.

What Is Amortization?

Amortization lowers the book value of a loan by spreading regular payments out over a set period of time. Amortization can also apply to an intangible asset, and in this case, works similarly to depreciation. You make consistent payments on a loan, gradually lowering its total value until the loan is completely paid off.

Getting a loan is much more appealing than having to save for the full price of a house or car, and amortization is the process of breaking up the loan, making it an accessible payment method. Calculating how long it will take to pay off the loan with amortization can help you forecast your monthly costs.

What Is an Amortization Schedule?

A table that shows periodic loan payments is referred to as an amortization schedule. You may also hear this referred to as a mortgage amortization schedule or mortgage amortization table. This amortization schedule includes the amount of principal and interest within each payment. Each monthly payment is listed to the end of the loan term, when the loan will be paid off. Each payment is the same throughout the amortization schedule.

Early in the amortization schedule, the payments are applied mostly to the interest of the loan, whereas the payments later in the schedule are applied mostly to the principal of the loan. The percentage of every payment that is paid toward interest continually decreases, while the percentage of each payment that goes toward the principal of the loan continually increases. This means the balance of the principal of your loan will not decrease much in the earlier part of your repayment schedule.

Though the amount of interest and principal you’ll be paying off differs each month, your total payment will be the same month to month. This makes budgeting easier for the years that you have the loan. You can also find the total of the principal payments and interest for your entire loan balance in the last line of your amortization schedule.

How Amortization Schedules Work

What is included in an amortization schedule?

Interest costs: For every payment, a portion goes toward paying off interest. The interest of each payment is calculated by multiplying the remaining balance of your loan by the interest rate.

Principal repayment: After applying the interest charge, the rest of the payment goes toward paying down the principal of the loan.

Scheduled monthly payments: Each of your monthly payments is listed individually for the entire duration of your loan.

The interest of a loan is calculated based on the loan’s most recent balance. When a payment exceeds the amount of interest, this payment reduces the principal. The interest rate is then applied to this new principal balance, and because the balance is lower, the amount of interest will also be lower. This is why the interest and principal in an amortization schedule have an inverse relationship. As the portion of interest in a payment decreases, the portion of principal in the payment increases.

The amortization schedule will generally contain seven columns:

Month: This is simply a number that denotes each month of your repayment period.

Beginning balance: This is the principal balance you have at the beginning of each new month before you make a loan payment.

Scheduled payment: This is your monthly loan payment. This number will be the same every month.

Principal: This is the amount paid toward your principal with every payment. Each month, this number will increase.

Interest: This is the amount paid toward your interest with each payment. Every month, this number will decrease.

Ending balance: This is the balance of your loan after you make your monthly payment.

Total interest: This column keeps track of how much you have paid toward interest so far. The final row will show you how much interest you’ll pay in total over the duration of the loan. Your amortization table may or may not include this cumulative interest amount.

The number of rows in your amortization table depends on the term of your loan. For example, if you have a 30-year mortgage, you’ll pay your loan off over the course of 360 months. This means your amortization table will have 360 rows.

Alternatively, the columns of your amortization schedule may be each month of your loan term, while the rows are your beginning balance, payment, principal, interest, ending balance and total interest.

When you calculate the amortization of your loan, you can create your own table with this information for the duration of your loan.

Use a spreadsheet to create an amortization table and analyze your loan.

Create an amortization table by hand.

If you want to set up your own amortization table, whether by hand or on a spreadsheet, you’ll need to know how to perform the calculations.

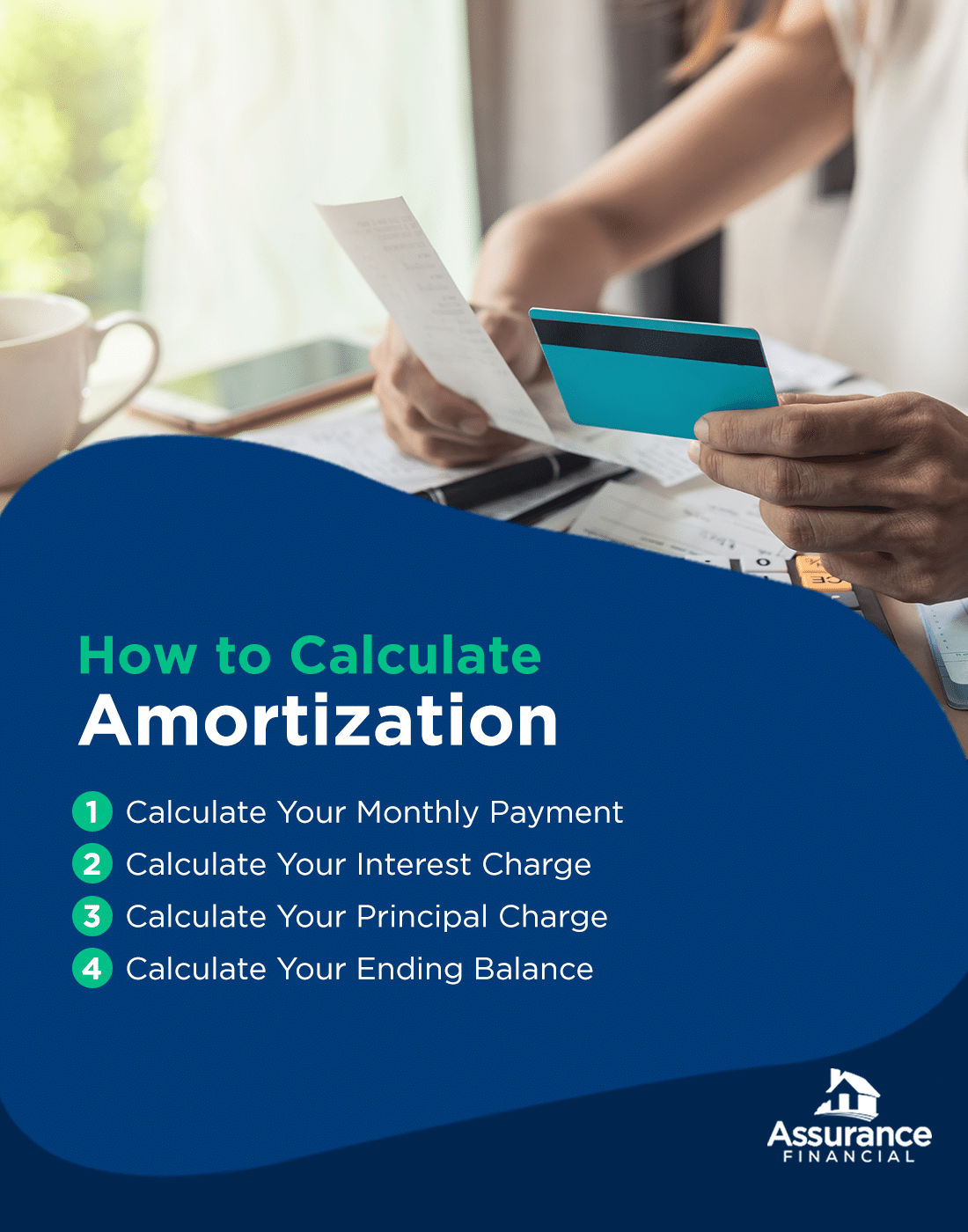

To calculate the amortization of your loan, follow these steps:

Calculate your monthly payment: This number will be the same every month.

Calculate your interest charge: To do this, multiply your beginning balance by your monthly interest rate. Your interest charge will decrease every month.

Calculate your principal charge: To do this, subtract your interest charge from the monthly payment. This number will show how much you’ll pay toward the principal that month.

Calculate your ending balance: To do this, subtract the beginning balance by the amount of principal paid that month. This number will be your ending balance for that month.

Repeat steps 2 to 4: Use the ending balance from step 4 as your beginning balance for the next month.

1. Calculate Your Monthly Payment

To calculate your monthly payment, you’ll need to know the amount of your loan, the term of your loan and your interest rate. These three factors will determine how much your monthly payment is and how much interest you’ll pay on the loan in total.

If you lower the principal or interest rate of your loan, you’ll also lower your monthly payment and save money. You can also lower your monthly payment by increasing the term of your loan, but you’ll ultimately pay more in interest.

You can calculate your monthly loan payments using this formula: M=P[r(1+r)^n/((1+r)^n)-1)]. If this formula seems overwhelming, don’t worry. The calculation is actually pretty simple:

M: This denotes your monthly mortgage payment.

P: This denotes the principal amount of your loan. For example, if your loan is $100,000, this is the number you would plug in for P.

r: This denotes the monthly interest rate for your loan. The interest rate you’re given for your loan is an annual rate, which means you’ll need to divide this number by 12, as there are 12 months in a year. This will give you your monthly rate. For example, if your interest rate is 4.5%, your monthly rate is 0.045/12=0.00375.

n: This denotes the total number of payments you’ll make on your loan. For example, a 30-year mortgage will have 360 payments. You can calculate this number by multiplying the number of years for your loan term by 12, which is how many months there are in a year. 30×12=360.

The monthly payment for a $100,000 mortgage at an annual interest rate of 4.5% for a 30-year term is $506.69.

2. Calculate Your Interest Charge

The next step is calculating the interest charge. Multiply your beginning balance by your monthly interest rate. Again, to calculate your monthly interest rate, divide your annual interest rate by 12.

4.5%/12=0.00375

For the first payment of the above example, you’ll multiply $100,000 by 0.00375. This gives you an answer of $375.

$100,000×0.00375=$375

This is the interest you’ll pay the first month. Keep in mind that your interest charge will decrease every month.

3. Calculate Your Principal Charge

Then, to figure out your principal charge, subtract your interest charge from your monthly payment. For the above example, subtract your interest charge of $375 from your monthly payment of $506.69.

$506.69-$375=$131.69

This remainder of $131.69 is what you’ll pay in principal the first month.

4. Calculate Your Ending Balance

Finally, you’ll calculate your ending balance for that month. To calculate this ending balance, subtract the amount of principal you paid that month from the balance of your loan.

For the first month of the above example, subtract your loan balance of $100,000 by the principal charge of $131.69.

$100,000-$131.69=$99,868.31

This ending balance will be the beginning balance of the next month. Repeat steps two through four for each month of your amortization schedule. If you’re calculating your amortization table yourself, you can check your math with an amortization schedule calculator.

Amortization Schedule Uses

An amortization schedule can help you understand exactly how borrowing a loan will work and how it will impact your finances.

1. Figuring Out What Borrowing Will Truly Cost

An amortization schedule provides you with details about your loan. You’ll get a comprehensive picture of your loan beyond your monthly payment. You can track exactly how much of your payments are going toward principal versus interest and how much you’ll be paying for interest in total.

Though many consumers base the affordability of a mortgage or a car loan on the monthly payment, the interest expense is a better way to assess the true cost of what you’re buying. In fact, lower monthly payments can actually mean you’re paying more in interest.

For example, a $100,000 mortgage will have a higher monthly payment at a 15-year term than a 30-year term, but you’ll pay much more in interest for a 30-year term than a 15-year term. With an amortization table, you’ll know how much interest you’ve paid so far or during a certain year, along with how much principal you still owe. Additionally, an amortization schedule will also help you calculate how much equity you currently have in your home.

2. Making the Right Decision

Having the full picture of your loan will also help you decide which loan is right for you. You can compare different loan options and terms, such as how much you may be able to save if you obtain a lower interest rate.

With an amortization schedule for your mortgage, you can also calculate how much you might save by making early payments. When you pay off your debt early, you’ll save money by paying less in interest. You can also calculate how much more you’ll need to pay every month to pay off your mortgage early, such as in 20 years rather than 30 years.

Amortized vs. Unamortized Loans

For most borrowers, amortized loans are the better, more common option, though whether an amortized loan is right for you depends on your circumstances.

1. Pros and Cons of Amortized Loans

Amortized loans allow borrowers to pay principal and interest at the same time, so you’ll gain equity in your asset while you’re paying off your loan. You also know exactly how much you’ll be paying each month for the duration of the loan repayment period, which makes financial planning much easier. With an amortized mortgage schedule, you’ll know how much your mortgage will cost you every month this year, next year and 30 years from now.

Because borrowers pay both principal and interest at the same time, monthly payments can be higher. With an amortized loan, some borrowers may also be unaware of the loan’s real cost, as they focus more on the monthly payment and disregard the total interest the loan will cost them.

2. Pros and Cons of Unamortized Loans

Unamortized loans, on the other hand, are attractive to borrowers because of their interest-only payments, which tend to be lower than amortized loan payments of combined principal and interest. The monthly payments for unamortized loans are also easier to calculate since you only have to worry about the interest. These lower, interest-only payments allow borrowers of unamortized loans to save up enough to make a large lump sum payment.

For consumers who rely on lump-sum income, such as commission, bonuses or payment from contracts, unamortized loans tend to be a better financial option.

However, since you’ll be paying lower payments of interest-only, you’ll have to make a large payment toward the end of your repayment period, known as a balloon payment. This lump-sum payment will go toward the principal of your loan. Planning ahead with an unamortized loan is crucial to ensure you save up enough to make that large payment down the road. Additionally, because you aren’t initially paying any principal of the loan, you’re also not gaining any equity in your home or vehicle while making your interest-only payments.

For many borrowers, amortized loans are a better option. Home loans, car loans and personal loans tend to be amortized, but some mortgages, like balloon loans, can also be unamortized. Compare costs and take a good look at your personal finances to determine which is the right option for you.

Things to Keep In Mind About Amortization

Keep in mind the information that amortization tables don’t account for. This information includes:

Fees: An amortization table generally doesn’t include additional fees for your loan, such as closing costs on a mortgage or origination fees.

Additional expenses: Your amortization schedule doesn’t include every cost related to your home. You may also have to pay expenses such as property taxes or private mortgage insurance (PMI) that aren’t included in your amortization schedule.

Extra payments: A standard amortization schedule won’t account for extra payments. You can make an extra payment on your mortgage to pay your debt down early, but you may have to use your own amortization schedule to calculate the benefit of making an extra payment and how this will affect your remaining loan payments.

Though an amortization schedule breaks down your loan payments by month and illustrates exactly what you’ll be putting toward principal and interest in each payment, this amortization table may not provide a complete picture of how much your asset will cost you. When deciding how much home you can afford, for example, keep in mind that there are costs beyond monthly payments and interest to consider.

Amortization Schedules FAQ

Below are some commonly asked questions about amortization schedules:

1. What Is the Purpose of an Amortization Schedule?

Looking at individual payments will allow you to compare loan options more easily. You will be able to tell how much the accrued interest of each loan would cost each month. You will understand the interest rates of each type of loan better, and without having to visualize that information, you can select the option that works best for you.

Amortization schedules also help you stay on track for completing your payments once you secure a loan. They are handy if you ever need to refinance, and they continue to be useful for tax purposes, if needed.

2. What Does an Amortization Schedule Show?

The amount you borrow is the principal amount, and the interest is what the lender charges for their services. Your schedule should show both values, so you will see how much the interest costs. It’s easier to look at an amortization schedule than to estimate how much you will pay monthly or to calculate the numbers on your own.

3. How Do I Get an Amortization Schedule?

An amortization schedule will be provided when you close on a loan. You can also use an online calculator tool. With the right information, creating one yourself in Excel or a comparable program can save you some time when you’re still deciding on a loan.

Secure the Right Loan With Assurance Financial

Are you comparing your loan options? Want to make sure your loan is affordable over a long-term period? Find a loan officer who can help you create your ideal amortization schedule with Assurance Financial.

[download_section]

Webinar: Using Customer Data to Thrive as a Lender of the Future

“It’s time to get it right,” remarks Katherine Campbell, VP of marketing at Assurance Financial, during our webinar, How to thrive as a mortgage lender of the future. “Everybody has made a major investment in technology, and we now have to start figuring out some ROI.”

Watch as Campbell and Katy Keim of LQ Digital continue the conversation, discussing strategies for mapping the customer journey to modernize your lending experience while acquiring ideal consumers. Collectively, they present a compelling case for leveraging data to make informed decisions that align with your unique customer base.

Watch the webinar:

Updating the customer experience starts with knowing your customers. Build an ideal customer profile that incorporates information such as age, lifestyle, and features they’re looking for in a home. For example, are they first-time buyers or are they upsizing for their second home?

Once you know who they are, you’ll want to put yourself in the borrower’s shoes to understand their perspective. This will help you and your team glean what the borrower is looking for, which allows you to appropriately shape your communications. The messaging you use to interact with your customers is key to the new and improved journey you’re creating. Watch the webinar to dive deeper with Campbell and Keim and learn how to build out this journey.

The webinar explores ways to align your business practices with the various customer journeys you aim to serve. Learn how to:

Develop the ideal customer experience

Design communication flows that make sense for your customers

Define and evaluate metrics to reinvent the borrower journey

Share this post

If you’re looking to obtain a mortgage for your dream home, you’ve likely heard of loan officers. A licensed loan officer is required to obtain a mortgage, but what does a loan officer do? Why is working with a loan officer necessary, and what is their role in the mortgage loan process?

A loan officer can help you find the right loan type and mortgage terms for you. Because a loan officer is such a key player in the process of finding a mortgage, knowing how to choose a loan officer and what qualities to look for are essential in ensuring you get the best mortgage for you.

What Is a Loan Officer?

You may know that finding a loan officer is an important step in the process of obtaining your loan. Let’s discuss what loan officers do, what knowledge they need to do their job well, and whether loan officers are the best option for borrowers in the loan application screening process.

1. What a Loan Officer Does

A loan officer works for a bank or independent lender to assist borrowers in applying for a loan. Since many consumers work with loan officers for mortgages, they are often referred to as mortgage loan officers, though many loan officers help borrowers with other loans as well.

If you’re looking to borrow a loan, a loan officer decides if you’re eligible to proceed to underwriting. A loan officer will meet with you and evaluate your creditworthiness. If a loan officer believes you’re eligible, then they’ll recommend you for approval, and you’ll be able to continue on in the process of obtaining your loan.

2. What Loan Officers Know

Loan officers must be able to work with consumers and small business owners, and they must have extensive knowledge about the industry. Loan officers should know the rules and regulations of the banking industry, what lending products are available and what documentation is required for consumers to obtain a loan.

3. Why Loan Officers Are Better for Borrowers

Many would-be borrowers may find themselves facing discrimination when it comes to algorithms that work in place of a loan officer. If you can meet with or speak to a loan officer, you can make your case for loan approval to a human being rather than a machine. In short, working with a loan officer tends to get you better results than going through a bank or lender that automates the process with computer algorithms.

4. How Much a Loan Officer Costs

Some loan officers are paid via commissions. Mortgage loans tend to result in the largest commissions because of the size and workload associated with the loan, but commissions are often a negotiable prepaid charge. With all a loan officer can do for you, they tend to be well worth the cost.

While every loan officer is required to be licensed, part of the allure of this job is that the role tends to pay well without requiring a professional degree. It isn’t a job for everyone, though.

1. Duties of a Loan Officer

The duties of a loan officer include visiting loan applicants and completing lots of paperwork, especially for mortgages. Loan officers also possess comprehensive knowledge about the industry and excellent customer service skills. A loan officer is licensed with the necessary federal and state authorities and adheres to the regulations of the lending process. A loan officer will bring their expertise to the table when they work with you.

Loan officers know all about the many types of loans a lender may offer, and they can give you advice about the best option for you and your situation.

Discuss your needs with your loan officer. They can help direct you toward the best loan type for your situation, whether that’s a conventional loan or a jumbo loan. They can even help with reverse mortgages and construction loans.

2. The Role of a Loan Officer in the Screening Process

Your loan officer is your direct contact when you’re applying for a loan. They will research and review your financial history and assess whether you qualify for a mortgage. You won’t have to worry about regularly contacting all the people involved in the mortgage loan process, such as the underwriter, real estate agent, settlement attorney and others, because your loan officer will be the point of contact for all of the involved parties. This will alleviate you of the stress of trying to keep track of all the various representatives and their duties.

Because the process of a loan transaction can be a complex and costly one, many consumers prefer to work with a human being rather than a computer. This is why banks may have several branches — they want to serve the potential borrowers in various areas who want to meet face-to-face with a loan officer.

Meeting with a loan officer is your opportunity to prove your creditworthiness. You can take this chance to explain anything that may have a negative impact on your creditworthiness, such as:

A missed payment on your credit card

Gaps in employment

Drops in your credit score

Loan officer responsibilities also include answering a would-be borrower’s questions, so use this opportunity to ask your questions.

A loan officer will screen you to determine if you qualify for underwriting. They’ll factor in your annual salary, credit score, debt-to-income ratio and total debt amount, but the numbers aren’t the only important factors in your ability to qualify for a mortgage. If you can make a connection with a loan officer and explain the circumstances of your situation to a human being, you may have a better chance of successfully obtaining a loan.

3. The Role of a Loan Officer in the Loan Application Process

The mortgage application process can feel overwhelming, especially for the first-time homebuyer. But when you work with the right loan officer, the process is actually pretty simple. When it comes to applying for a mortgage, the process can be broken down into six phases:

Pre-approval: This is the phase in which you find a loan officer and get pre-approved.

Shopping for a home: This is the phase you’ve been looking forward to — shopping for your dream home.

Mortgage application: A lender reviews you application during this phase and provides you with a loan estimate.

Loan processing: During this phase, loan processors will verify everything on your application.

Underwriting: In this phase, the underwriter determines whether you’re a good loan candidate for the lender.

Closing: During this phase, you’ll sign all the final documents and pay for closing costs.

What is your loan officer’s role during these phases? If your loan officer approves you after the screening process, they will help prepare your application. During the loan processing phase, your loan officer will contact you with any questions the loan processors may have about your application. Your loan officer will then pass the application on to the underwriter, who will assess your creditworthiness. If the underwriter approves your loan, your loan officer will then collect and prepare the appropriate loan closing documents.

The amount of work this entails for the loan officer depends on what type of loan you’re applying for. Usually, a secured loan will require more documentation than an unsecured loan. Mortgage loans, in particular, are known for requiring a large amount of paperwork because of the several mortgage regulations at the federal, state and local levels.

A good loan officer can be a key player in ensuring that your loan application process goes smoothly.

Home buying can initially feel like an overwhelming, stressful process, but the right loan officer can pave the way for a smooth loan application process. So how do you choose the right loan officer for you?

To begin your search, start with lenders who have an excellent reputation for exceeding their customers’ expectations and maintaining industry standards. Once you’ve chosen a lender, you can then begin to narrow down your search by interviewing loan officers you may want to work with.

First, you’ll want to consider location when choosing a loan officer. A lender may offer branches across the nation, so you’ll want to find a branch that’s closest to you. We have several loan officers you can work with at Assurance Financial. You can use your zip code to search for loan officers near you.

When you have your search narrowed down to a few choices, you can ask helpful questions that can lead you to choose the right loan officer for you. The following are a few questions you may want to address in a discussion with a loan officer:

1. Do You Offer First-Time Homebuyer Loan Programs?

Does this lender offer first-time homebuyer loan programs? If so, find out what programs they offer and if you qualify for any of them. Learn what might be a good fit for your situation.

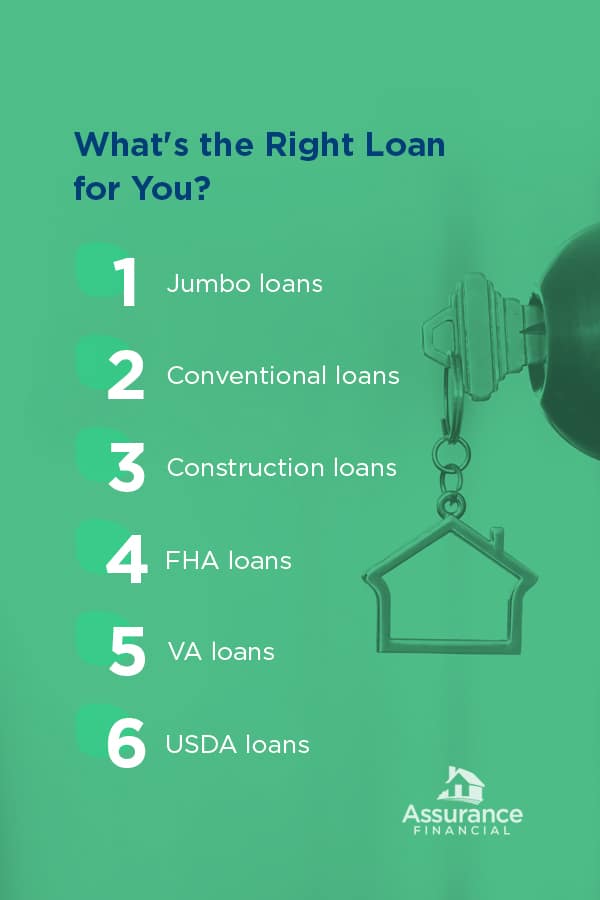

Loan programs offered to you may include FHA loans, USDA Rural loans and VA loans.

FHA loan: An FHA loan is backed by the Federal Housing Administration and is intended for borrowers who wish to finance a home with a small down payment but still obtain a low interest rate. Depending on your credit score, you may be able to put down as little as 3.5% on your home.

USDA Rural Development loan: A USDA Rural loan is backed by the U.S. Department of Agriculture and is intended for lower-income earners who wish to purchase a property in a qualifying rural or suburban area. You’ll need a higher credit score than for an FHA loan, but you also may be able to obtain a USDA loan with no down payment.

VA loan: A VA loan is backed by the U.S. Department of Veterans Affairs and is offered to eligible military members, veterans and surviving spouses. You can typically obtain a loan at a competitive interest rate, and you aren’t required to provide a down payment.

Ask a loan officer whether they offer any of these programs and what your options are.

2. Do You Offer Assistance Programs for Down Payments?

Some lenders may offer down payment assistance programs and closing cost assistance programs. If approved for an assistance program, you may be able to move into your new home more quickly, select a 30-year loan at a fixed rate or get discounted private mortgage insurance.

Down payment assistance programs usually come in the form of:

Loans to be repaid alongside your mortgage

Loans to be repaid when you sell, move or refinance

Grants that you don’t have to repay

Down payment assistance programs can be a particularly helpful option for first-time homebuyers who have little savings but don’t want to delay moving into their dream home until they save a 20% down payment. Since saving enough for a down payment can take years for many would-be borrowers, these assistance programs can make a big difference in your ability to obtain a mortgage for your dream home.

3. What Is the Best Type of Mortgage for Me?

Make sure to provide the loan officer with plenty of details about your situation and answer the questions they ask you. They may recommend certain loans for you, so ask for those options to be put in writing. This will help you learn about each type of loan and its strengths.

Ask about details you may not completely understand. If a number seems high or surprising, ask the loan officer to explain.

4. What Is the Cost Estimate for the Loans You Recommend?

Another question you may want to ask when determining which loan officer is the right candidate for you is what their cost estimate is for the loan options they recommend. A loan estimate gives you a breakdown of all the costs associated with a loan, including closing costs.

Though the estimates will be based on current interest rates that can change, they can still give you an idea of what you can expect in terms of the cost of the loan. Request these estimates all on the same day so they can be fair, comparable estimates.

Ask questions like these during the interview with a loan officer. The answers a loan officer provides and their willingness to answer your questions will indicate to you whether you want to move forward with your professional relationship with this loan officer.

The Qualities of a Good Loan Officer

A good loan officer will possess certain qualities. What can you expect a good loan officer to be like? What will they do for you? The following are some of the qualities you can expect in a good loan officer:

1. Bring Expertise to Your Loan Process

Among a loan officer’s skills is expertise in the industry. Loan officers are licensed with the federal and state authorities, and they adhere to the regulations of lending money. Because regulations are so strict, loan officers must be highly knowledgeable about the lending process and the banking industry.

The loan process, especially for mortgages, requires a lot of paperwork. While completing the necessary paperwork, you’ll likely have several questions. A loan officer can offer their expertise to answer your questions and help you properly fill out the paperwork. Issues with the paperwork can delay the process of applying for a mortgage, so having a lender to guide you can help prevent delays.

When you work with a professional who has comprehensive knowledge about the work they’re doing for you, you’ll know you’re in good hands and making informed decisions about your loan.

2. Tailor Loans to Your Personal and Financial Situation

Because the success of many loan applications boils down to numbers, loan officers can be the difference between you being approved or denied in the screening process. Your credit score, annual salary, debt-to-income ratio and total debt amount factor into the approval process, but these numbers don’t tell the whole story of your financial history nor can they predict your financial future.

Loan officers can go beyond these numbers to tailor a mortgage solution to your specific personal and financial situation. A mortgage is one of the most significant financial decisions a person makes, and the terms of your mortgage can have an effect on your financial stability and happiness for many years to come.

3. Possess Superior Customer Service Skills

One of the most important qualities for a loan officer to possess is superior customer service skills. Good loan officers strive to exceed customer expectations, provide advice and suggestions specific to a borrower’s needs and to be accessible and responsive to the borrower and everyone else involved in the process.

A good loan officer aims to understand a borrower’s needs so they can not only meet but exceed each client’s expectations. A loan officer should also be easy to contact, and they should keep an open line of communication with you. This will allow them to assist you through every step of the loan application process.

4. Provide Suggestions for Improving Qualifications

Though a loan officer can’t make any issues in your credit history disappear, they can offer suggestions for how you can improve your credit and other qualifications for loan approval. Advice a loan officer gives you could potentially be the difference between getting approved or denied for a loan.

Even if you aren’t approved for the loan you applied for, following a loan officer’s suggestions can improve your odds of being approved when you apply for a mortgage again. A loan officer knows the ins and outs of loans and what makes an applicant get approved or denied, so take their suggestions seriously and implement them to increase your odds of getting approved for a loan.

5. Communicates Well With Involved Parties

While a loan officer will advise you, crunch numbers and streamline your application process, their job involves a lot more than paperwork. A good loan officer will also communicate well with the other involved parties, such as the underwriter. They’ll act as your representative and stay in contact with everyone involved so you don’t have to.

As such, you may want a loan officer who understands and connects with you. They should understand the needs and personalities of you and your family. If your loan officer understands what you’re looking for, they can better help you find the best lending solutions.

Find a Loan Officer at Assurance Financial

At Assurance Financial, we have over 120 mortgage loan officers who work with our clients to find the best lending solutions. We service a loan from beginning to end, saving our borrowers time and making the entire process more convenient with the highest quality digital tools available. We’re an independent, full-service lender and we enable our borrowers to purchase their dream homes, whether it’s their first home, a vacation home or an investment property.

We bring integrity and honesty to our work and strive to do what’s best for our customers. We’re licensed in 39 states and housed in 20 locations. Find the perfect loan officer with Assurance Financial and get pre-qualified before you begin the search for your dream home. Apply for a loan in under 15 minutes with our digital loan assistant, Abby, today!

Share this post

Appraisals are an essential step in the home buying process. An appraisal informs the buyer, seller and lender about the value of a home and is intended to prevent buyers and lenders from overpaying for a property. Appraisers determine a home’s worth by considering a variety of factors, including the size, condition, location, number of rooms and comparable sales in the area.

The appraiser must be an impartial third party with no interest in the outcome, so the appraisal can be considered fair. As long as the appraiser determines the value of the home to be equal to or higher than the asking price of the home, the sale can continue. If the home is appraised at a lower value, this can slow or halt the process.

Understanding loan appraisals is key to recognizing and avoiding over-inflated estimates. In this guide, we’ll discuss the process of loan appraisals, who requests them, what red flag to look out for and more:

Who Requests Appraisals?

An appraisal can be requested by a seller, buyer, real estate agent, homeowner or lender, as all parties have an interest in determining the value of a home. However, each may have a different reason for requesting an appraisal:

The seller: The seller of the home may request an appraisal to determine the asking price of their home or to support their asking price before they put the home on the market. Though a seller isn’t required to have an appraisal conducted, an appraisal can be helpful if they’re uncertain about the home’s actual value.

The buyer: The buyer may request an appraisal if they’re hoping to negotiate a lower price for the home.

The real estate agent: The buyer’s real estate agent may also request an appraisal if they believe the home is priced unusually high when compared to similar sales in the area.

The homeowner: If a homeowner is looking to refinance their home, they may also request an appraisal.

The lender: Before a lender approves a loan, they will most likely request an appraisal, since the home is collateral for the mortgage. If the buyer can’t continue making payments on their loan, the lender will need to sell the home to recoup their costs, and if the property was initially overpriced, the lender won’t be able to get back the full price of the loan.

An appraisal may be requested more than once to negotiate the best deal. Though a home usually doesn’t need to be appraised more than once, any of the three parties involved may request an additional appraisal if they deem it necessary.

How Does the Appraisal Process Work?

Depending on the size and complexity of the home, an appraisal can take less than an hour or several. An appraisal is also one of the first steps that will take place in the closing process of a purchase-and-sale transaction. You’ll even need an appraisal for a house you haven’t built yet.

During this step, a professional appraiser will walk carefully around the property, examining the condition of both the exterior and interior with the intention of determining the fair market value or a fair range of values. They will make a note of any conditions that negatively impact the value of the property. If your home needs repairs, for example, this could negatively impact the property’s value. The appraisal value is what the property should sell for on the market.

For a purchase-and-sale transaction, the appraisal fee is generally paid for by the borrower and can cost several hundred dollars. An appraisal can also be requested in a refinance transaction to ensure the lender isn’t giving the borrower a loan of an amount higher than the property is worth.

An appraiser should be certified or licensed, familiar with the local area and impartial with no interest in the sale. An appraiser should have certifiable experience appraising similar properties in the area. To complete the process, an appraiser will consider:

Soiled carpeting

Water-stained walls

Persistent odors

Broken windows

Plaster cracks

Leaky faucets

Cracked ceilings

Damaged light fixtures

Code violations

Pests

Floor plan functionality

The square footage

The number of bathrooms and bedrooms

Comparable sales, known as comps

The condition of the home’s permanent features, including square footage, age, location, views and lot size

An appraiser is not looking at the condition of the furniture, the cleanliness of the home or the performance of the heating and cooling systems, though they will check that they exist and are working. Appraisers focus mostly on your home’s permanent fixtures and the condition of these features.

After the appraiser completes their evaluation of the property, they will then provide their conclusions and analysis based on their observations. In their report, an appraiser needs to include a sketch of the exterior, an explanation for the calculation of the home’s square footage, a street map that shows the appraised property and the comparable sales used for the appraisal, photos of the front exterior of every comparable property, and photos of the home’s front, back and street view.

The report should also include other relevant information the appraiser used to determine the fair market value of the home, such as public land records, market sales data and public tax records.

Sellers can often increase their home’s appraisal value by:

Patching up walls

Repairing broken windows

Fixing leaky faucets

Trimming hedges

Mowing the yard

Repairing or replacing broken garage doors

Informing the appraiser of positive updates to the neighborhood, such as a new school.

Writing down all the improvements and repairs you’ve made over the years, from a new roof to a new sink. Include when these updates were completed and the cost of each.

An appraisal should provide the true value of a home, which is why it’s such an important step in the process of buying a home and why the appraisal needs to be accurate. If a home is appraised at or above the asking price, the transaction can proceed as planned. If the appraisal is below or above the asking price, the transaction can get delayed or fall apart entirely.

If a home is appraised to be higher than the asking price, the lender will only issue a mortgage for the appraisal amount. This leaves the borrower to either cover the remaining cost on their own or return to searching for a home with a listed price that matches the appraised value. Appraisals are also used in estimating property taxes for a home, so this is an additional cost that could affect the homeowner.

If a seller wants to make a sale, their asking price needs to align with the appraisal value. If a buyer wants to purchase a home, the asking price and mortgage amount needs to align with the appraisal value. This is why an appraisal is so essential for everyone involved in the process and why avoiding over-inflated loan appraisals is crucial.

Over-Inflated Loan Appraisals

What is an over-inflated loan appraisal? What impacts does an over-inflated loan appraisal have on the home buying process?

An inflated loan appraisal determines an asking price that is much higher than the market value of the home. An over-inflated appraisal is a type of mortgage fraud that could cause a buyer to pay much more for a home than they should.

What Are the Causes of Over-Inflated Loan Appraisals?

Though no appraiser is perfect, they are highly-trained professionals with several years of experience and are required to continue their education throughout their careers. They have to prove all of their findings that factor into a home’s value and are heavily regulated. The consequences of doing their job poorly — by issuing a biased or intentionally misleading report — can be severe. Because of this, appraisers work diligently to make sure they keep their biases and personal judgments out of their work.

So why is appraisal fraud committed? Appraisal fraud is typically used to:

Help the seller make more money from selling the home.

Help the buyer be in a better position to finance mortgage payments.

Help the homeowner obtain better refinancing or a home equity loan.

Appraisers aren’t the only ones who can commit appraisal fraud. Sometimes buyers, sellers or homeowners will alter an appraisal using digital editing or bribery. Appraisers may also work with a real estate agent to increase a home’s purchase price to boost commission.

Appraisers can feel pressured to inflate a home’s price so the deal can work out between the buyer and seller. If an appraiser believes a home to be worth less than the asking price, a borrower may not be able to obtain a mortgage if the loan amount is higher than the lender’s limit. If a borrower needs to put 20 percent toward a down payment, for example, a higher home price could create conflict. A buyer may not be able to afford a home if it’s deemed more expensive, and an appraiser may not want to be the bearer of bad news.

To protect themselves against this fraud, lenders will request a separate appraisal, often with a preferred appraiser. This generally happens around the time of closing, so even if the buyer is ready to purchase the house, the lender may require the seller to lower the price, or they may not approve the loan.

A homeowner or buyer may also want to err on the side of caution and seek a second opinion if they’re making a decision using someone else’s appraisal.

How to Recognize an Over-Inflated Loan Appraisal or Appraisal Fraud

Despite strict regulations, appraisal fraud still occurs. If you can recognize these common scams and schemes, you may be able to avoid appraisal fraud. The most common red flags are:

An immediate resell for a profit: Appraisal fraud can sometimes occur with property flipping. If a home is purchased below market value and then immediately sold for a profit with the assistance of an appraiser who declares the property is worth much more than the initial estimate, this is a sign of appraisal fraud.

A property is undervalued for an investor: A property might be undervalued by an appraiser so an investor can purchase the property.

Other signs of appraisal fraud include:

The property listed for the appraisal is inconsistent with the property on the application.

The locations or types of comparable sales are inconsistent.

Photographs of the property don’t match the description in the appraisal

Loan Appraisals and Homebuyers

Are you a homebuyer who has been affected by inaccurate loan appraisals? Odds are, you don’t want the transaction to fall through, and neither does the seller. Generally, lenders don’t lend the total value of the home — depending on the borrower’s qualifications and the type of mortgage — so they definitely won’t lend more money than a home is worth.

Lenders want to take on as little risk as possible. If you can’t pay back your loan, they need to get their money back by selling the home. But if they gave you more money than the home was worth, they’re unlikely to make their money back. If you’re the buyer, this means you’re unlikely to get the loan you need to pay for your dream home.

Luckily, there are several things you can do as a homebuyer to if you think an appraisal is inaccurate:

Negotiate a Lower Price

If an appraisal determines the price of the home to be lower than the contract price, you may be able to use the appraisal to negotiate a lower price from the seller. The seller is likely motivated to sell, and at such a late point in the transaction, they may be willing to drop the price in order to close.

On the other hand, the seller may be dissatisfied with a low appraisal and believe it to be inaccurate. As such, they may not be willing to drop the price, or they may challenge a low appraisal. For example, if the appraisal value has been affected by foreclosures and short sales in the local area, the seller may be able to convince the appraiser that their home is worth more than the other properties because it’s in better condition.

Fortunately, if the owner can get the appraisal value up to the contract value, this will allow you to continue on with the process as planned.

Get a Second Opinion

Is an appraisal standing between you and your dream home? If so, you may want to consider getting a second opinion. You can request an appraisal to be performed by a different appraiser, who may assess the property at a different value. Appraisers are human, so mistakes can be made, and information can be overlooked.

Appraisers can also feel pressure from the people they work for to make a deal work. If they work for a lender, the appraiser may feel their livelihood is threatened if the numbers they provide don’t close the deal. An impartial appraiser is the key to an accurate estimate.

Make Your Case for a Higher Value

You can also speak with the initial appraiser and make your case for a higher value. If the appraiser agrees with you, they may revise their evaluation. This will allow you to continue forward with the transaction as planned.

You also may run into issues if you’re refinancing a mortgage and wind up with a low appraisal. To be approved for a loan when refinancing, your home needs to be at or above the loan amount you’re applying for. If the appraisal comes in under that amount, you won’t be able to qualify for the loan. An exception to this is if you have an FHA mortgage, you may be able to refinance your home without an appraisal.

When it comes to inaccurate loan appraisal, homebuyers have options. You can attempt to obtain a more accurate appraisal or use the appraisal to your advantage. Knowing how to improve this situation will ensure you come out of the appraisal process with the deal you wanted.

How to Avoid Over-Inflated Loan Appraisals

How can you avoid over-inflated loan appraisals? Try the following tips to avoid an inflated loan appraisal:

Hire an Appraiser Yourself

One way you can avoid an over-inflated loan appraisal is by hiring your own appraiser. You’ll have to pay for an appraisal when you buy or refinance a home anyway, so using that money to give you the peace of mind you need is well worth it.

Ask for References

You can ask for references for an appraiser from banks. A bank is likely to hire an ethical, competent appraiser, so you’re likely to find one who is impartial and honest.

Understand the Appraisal Process

When an appraisal determines a home’s true value to be similar to the asking price, then an appraisal is simply a box to check off during closing. When a home appraisal is substantially different from the contract price, however, the transaction can come to a grinding halt. By understanding the ins and outs of the appraisal process, you can ensure it works in your favor and combat any problems that may arise.

If you can avoid an over-inflated loan appraisal, you can spare yourself and everyone involved the headache and heartache of a disrupted home transaction.

Seek Help From a Loan Officer

A loan officer can help buyers avoid getting the wrong appraisal. A loan officer evaluates and recommends approval for loan applications, so they’re on your side when it comes to financing your future home.

When you meet with a loan officer, you can present yourself as a worthy candidate for a loan. Demonstrate your creditworthiness and explain the issues that may come up on your credit history, like a missed payment on your credit card.

Sometimes, the process of applying for a loan can seem like it’s all about the numbers — your salary, your credit score, your debt-to-income ratio and your total debt. But loan officers can look beyond the numbers. After speaking with a loan officer, they can support you as a candidate for a loan and pass you along to the underwriting process.

A loan officer can help you along the process of financing your dream home and provide valuable insight to help you avoid an over-inflated appraisal. Since lenders want to avoid over-inflated home appraisals, a loan officer will be sure to work with you to get an accurate one.

[download_section]

Apply for a Loan From Assurance Financial

The process of appraising a home can be lengthy and complicated. Luckily Assurance Financial is here to help.

We are dedicated to providing the assistance you need to receive your loan hassle-free. Ready to get started? Apply online in 15 minutes or less!

Share this post

For many homebuyers, the process of purchasing a home and securing a mortgage can seem overwhelming, especially if you’re learning mortgage lingo for the first time — conforming loans, non-conforming loans, conventional loans, jumbo loans, fixed rates, adjustable rates and more. With so many options, how do you decide which is the right mortgage loan for you?

For many, the decision first begins with choosing between a conforming loan and a non-conforming loan, also known as a jumbo loan. To help you determine which might be the right loan for you, we’ve compiled a comprehensive guide of the similarities and differences between a jumbo loan and a conforming loan.

What Is a Jumbo Loan?

When your ideal home is more expensive than most, you may want to opt for a jumbo loan. Jumbo loans are large mortgages secured to finance luxury homes or homes located in competitive markets.

1. How Does a Jumbo Loan Work?

A jumbo loan can be financed for a single-family home that exceeds the Federal Housing Finance Agency’s maximum loan limit. A jumbo mortgage is not backed by Fannie Mae, Freddie Mac or any government agency.

The limit on conforming loans throughout most of the country is $484,350, though this limit does vary by location and can be much higher in competitive housing markets. In competitive markets like San Francisco and Los Angeles, you can secure a mortgage for over $700,000 without the loan being considered jumbo. States like Hawaii and Alaska also offer much higher loan limits than the rest of the U.S. If you want a loan that exceeds this limit, you may want to secure a jumbo loan.

The limit also varies by the number of units on the property.

Above $484,350 for a one-unit property

Above $620,200 for a two-unit property

Above $749,650 for a three-unit property

Above $931,600 for a four-unit property

You can use your jumbo mortgage to cover your primary residence, a second home, a vacation home or an investment property. If a large, expensive home calls to you and is within your price range, then a jumbo loan may be your best financing option.

2. What Are the Benefits of a Jumbo Loan?

Aside from being able to finance the home of your dreams, why should you get a jumbo loan?

Competitive interest rates: Though jumbo loans have historically come with higher interest rates, lenders have realized that borrowers of jumbo loans can be lower-risk and now offer interest rates that are competitive with those on conforming mortgages.

Fixed or variable rates: With a jumbo loan, you can decide whether you want a fixed interest rate or a variable interest rate.

No PMI payments: If you make a small down payment on a conforming loan, you will typically be required to make private mortgage insurance (PMI) payments. However, with a jumbo loan, you may be able to put down less than 20% without being required to pay PMI.

If you want to purchase a pricey home, a jumbo loan may be exactly the right mortgage option for you.

3. How Do You Qualify For a Jumbo Loan?

Jumbo mortgages tend to be riskier for a lender than conforming mortgages due to their hefty amount and their lack of backing, so qualifying for a jumbo loan can be more challenging than qualifying for other loan types.

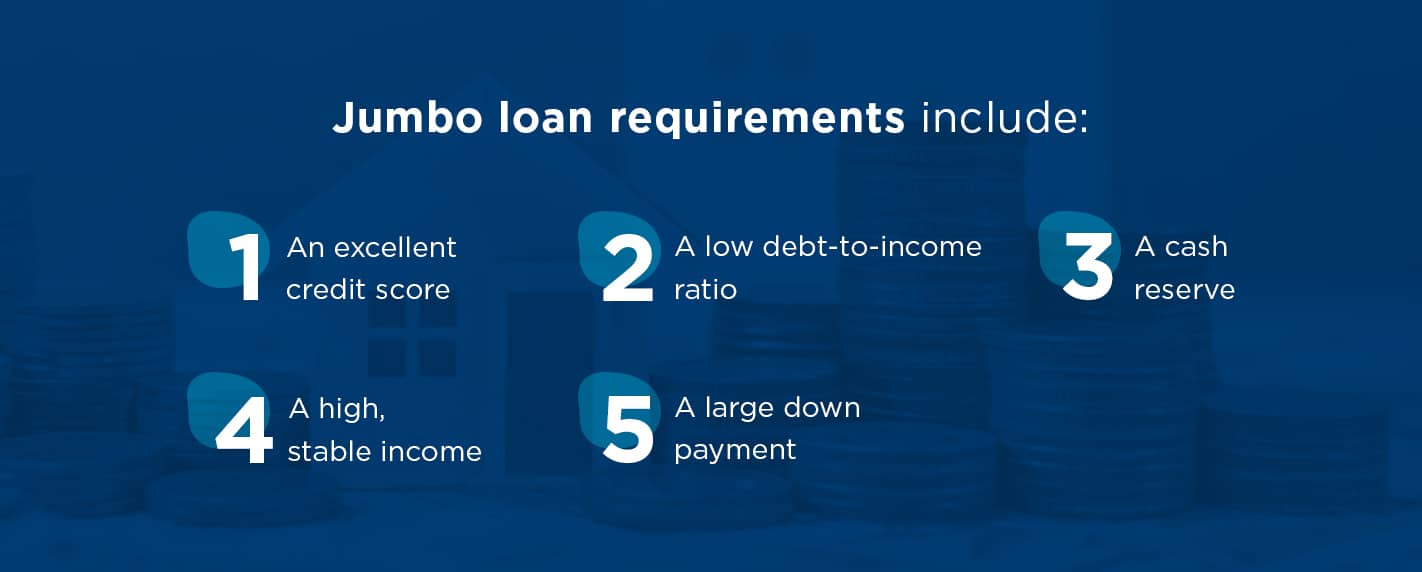

Jumbo loan requirements include:

An excellent credit score: Your credit score should be at least 700 to qualify for a jumbo loan.

A low debt-to-income ratio: This ratio should below approximately 36%. You can calculate your ratio by dividing your monthly debt payments by your monthly income.

A cash reserve: You may want to have about six to 12 months worth of monthly payments saved up to prove you have the resources to pay back your jumbo loan.

A high, stable income: You’ll want to gather 30 days of recent pay stubs and bank statements as well as W2 forms and tax returns from the past two years. A consistent, high income will give a lender more confidence in your ability to pay back your loan.

A large down payment: Many lenders will require a down payment of 20%, though it may be possible to put down only 10%. If you want to put down a small down payment, your credit, income and cash reserves will likely need to be even higher.

Lenders tend to be selective with the borrowers they approve for jumbo loans, so if you want to make sure you qualify, you may want to focus on building up your credit and assets.

4. Who Should Get a Jumbo Loan?