Tag: home loan

The most common type of home loan is the conventional loan. These loans are perfect for borrowers with a strong credit history and the funds for a more substantial down payment. Conventional loans offer the ability to avoid the costs of mortgage insurance while also giving borrowers the option of fixed or adjustable rates.

- What are conventional loan limits?

- Is a conventional loan suitable for you?

- What are the down payment requirements?

- What is Private Mortgage Insurance?

- What are the interest rates on a conventional loan?

- What credit score is needed for a conventional loan?

- Other requirements for a conventional home loan

- How do conventional loans compare to other options?

- Can first-time home buyers get a conventional loan?

The Basics of a Conventional Mortgage

The length of most conventional loans is 15, 20 or 30 years. To qualify, you will need a good credit score. The minimum score to be approved can vary from lender to lender, but a score of 620 is usually what you will need to be approved, and a score of 740 will help you secure the best rate possible.

Unlike other loans, a conventional mortgage could require a significant down payment. Most other loans require an initial payment of about 5%, but you can expect to put down up to 20% with a conventional loan. The amount varies and depends on your credit history. You will also be responsible for origination fees, appraisal fees and mortgage insurance.

[download_section]

Loan Limits

There are two types of conventional mortgage loans — conforming and non-conforming.

Conforming loans follow guidelines set by Fannie Mae and Freddie Mac. The rules for these loans are based on the size of the loan. In 2021, home loans for single-family homes were limited to $548,250, while higher-cost areas held limits up to $822,375.

Non-conforming loans are suitable for borrowers who don’t qualify for a conforming loan because the amount is more than what can be backed by Fannie Mae or Freddie Mac. Most lenders charge higher rates for non-conforming loans since they typically carry other fees and insurance requirements.

Is a Conventional Loan Suitable for You?

A conventional loan is an excellent choice for people who plan on living in their homes for many years and want to know what their monthly payments will be for the duration of their loan. The other side of the coin is adjustable-rate mortgages (ARMs). ARMs offer a lower interest rate for a short term during the first few years of the term — usually from 3 to 10 years, after which the interest rate can change. If you intend to own your home for a brief period, you could save money with an ARM at today’s low rates. If you plan to stay in your home longer, a fixed rate could be your best option.

A conventional loan is a mortgage that isn’t received from a government agency. It is the most common type of loan, requiring acceptable credit and reasonable down payment. Most borrowers find this loan attractive because of its two different rate options and lower interest rates than government loans, such as those guaranteed by the Federal Housing Association and the Department of Veterans Affairs. As a long-term option for most homebuyers, conventional loans offer fixed and adjustable-rate options. Depending on your situation, one may work better than the other. However, a significant draw for most is the option to choose their rate in general.

Let’s take a closer look at conventional home loans.

Down Payment Requirements for a Conventional Loan

In many cases, the more you can afford to put down when buying a home, the better off you will be. Making a sizable down payment reduces the amount of money you borrow, making your mortgage more affordable. Putting down at least 20% of the home’s price when you buy also eliminates the need for private mortgage insurance, which means your mortgage costs less each month.

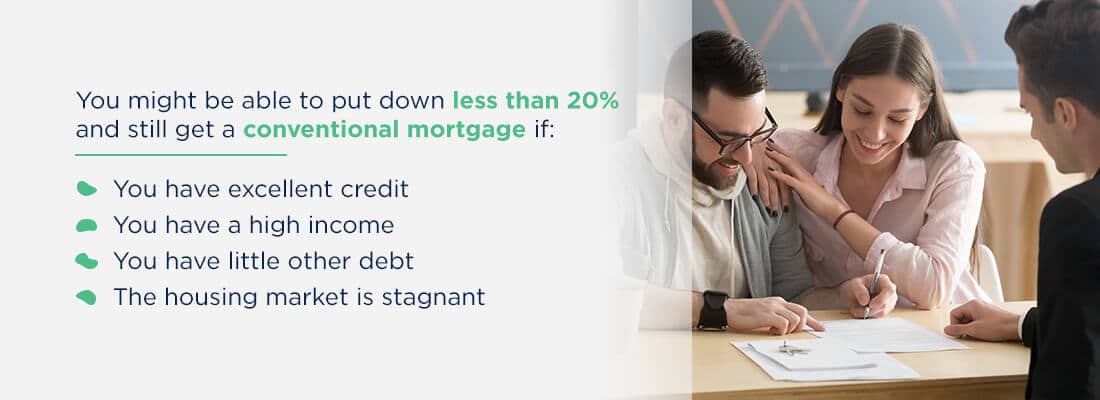

While a 20% down payment is often recommended, it’s not always required. A lender will look at the big picture when evaluating your mortgage application. Depending on your specific situation, you can put down as little as 3% when taking out a conventional mortgage. You might be able to put down less than 20% and still get a conventional mortgage if the following are true:

- You have excellent credit: A higher down payment reduces risk to the lender, but having a high credit score can put a lender at ease.

- You have a high income: Having a steady employment history and a high income compared to the amount you’re borrowing can also make a lender more comfortable with a smaller down payment.

- You have little other debt: Lenders will look at your total debt and debt-to-income ratio when deciding how much to lend you and how risky you are as a borrower. A debt-to-income ratio under 43% makes you more likely to qualify for a conventional mortgage. You might also be able to make a smaller down payment with a lower debt-to-income ratio.

- The housing market is stagnant: The housing market also plays a part in determining how much you’ll need for a down payment. In a seller’s market, when more people are looking to buy a home than people selling, you might find it more challenging to get approved for a loan or to successfully put an offer on a home with a smaller down payment. In a buyer’s market when there are plenty of homes available to purchase, you’ll likely be fine with a small down payment.

What Is Private Mortgage Insurance?

Private lenders issuing loans to borrowers who make smaller down payments take on more risk than lenders who only accept 20% down. To mitigate that risk, lenders usually add private mortgage insurance (PMI) to a borrower’s loan. PMI guarantees the loan, offering the lender financial protection if the borrower stops making payments.

If you have PMI, you have to pay a monthly insurance premium when you pay your mortgage. The premium is built into the overall mortgage payment and not something you need to pay separately. The premium size depends on the size of your down payment, the cost of the home and the insurance provider. You can expect a higher premium with a smaller down payment.

One thing that’s important to note about PMI is that it’s a protection for the lender, not the borrower. If you have trouble paying your loan, you still risk foreclosure or losing your home, even with PMI. PMI isn’t permanent. You no longer have to pay the premiums once the balance on your mortgage reaches 80% of the home’s value.

Interest Rates on a Conventional Mortgage

When you take out a mortgage, you’ll need to pay interest on the amount you borrow. Several factors determine the amount you pay in interest. Some factors are out of your control, such as market conditions. Others you have some say over, such as your credit history and the home price. Usually, the better your credit, the lower your interest rate. Buying a less expensive home can also mean a lower interest rate.

The length of the loan also influences the rate. Usually, longer-term mortgages, such as 30-year loans, have higher interest rates than shorter-term loans, such as 15-year mortgages.

The size of your down payment can also affect the interest rate a lender offers. With a bigger down payment, you’re likely to get a better interest rate. A smaller down payment can mean more risk to the lender, translating into a slightly higher interest rate.

You have two options when it comes to the type of interest rate your mortgage has:

- Fixed rate: The interest rate on a mortgage with a fixed rate will remain the same throughout the life of the loan, even if interest rates rise or fall with the market. For example, if you have a 30-year loan with a 4% fixed rate, it will be 4% on day one and the last day of the loan. A benefit of a fixed-rate loan is that you can lock in a low rate for many years if rates are low when you take out the mortgage. If rates are high when you purchase your home, you could be stuck with a high rate for years unless you refinance.

- Adjustable rate: The interest rate on an adjustable-rate mortgage changes from time to time. Often, ARMs have an introductory rate, which can remain the same for several years. After the introductory period is over, the rate changes on a fixed schedule, such as every year. Depending on the market when the rate adjusts, it can increase or decrease, rising or lowering your monthly mortgage payment.

Credit Score Needed for a Conventional Mortgage

No matter how much you have to put down, lenders will look at your credit score when deciding whether or not to approve your mortgage loan. A credit score gives a lender an idea of how likely you are to repay your loan. Usually, a higher score means you have a history of repaying your loans on time. Lenders often consider borrowers with higher scores to be lower-risk.

The Basics of a Credit Score

Several types of credit scores exist, and each scoring system is slightly different. Generally, scores range from 300 to 850. To get approved for a conventional mortgage, you’ll likely need a credit score of at least 620.

When calculating a credit score, the companies that do the math look at several aspects of your credit history:

- Payment history: Whether you pay your bills on time or have missed or late payments affects your score. Missing payments can lower your score.

- Amount of debt: How much debt you have already also contributes to your score. A lot of debt can reduce your score.

- Types of debt: The mix of debt you have plays a small part in determining your credit score. A variety of debt types, such as a car loan and a credit card, are preferable over multiples of the same type of debt.

- Length of credit history: How long you’ve had and used credit also contributes to your score — the longer your credit history, the higher your score, usually.

- The number of new accounts: Opening several new accounts at once can cause your score to drop.

- Amount of credit used: How much of your available credit you use, such as your credit card balance, can affect your score — usually, the lower your credit utilization, the better.

Other Requirements for a Conventional Home Loan

As you go through applying for a conventional mortgage, the lender is likely to ask you to provide proof of income and verify the value of the home. Some common loan requirements include:

- Income: You need to show proof that you earn enough to afford the monthly mortgage payment, in addition to any other debts you have. Your lender might ask you to provide tax returns from the most recent tax year, as well as pay stubs or bank statements to demonstrate that you earn what you say you earn.

- Assets: A lender will also likely want verification that you have enough in the bank to make a down payment on the home and that you have some extra money to afford closing costs and other costs associated with homeownership. You might have to provide bank and investment account statements to the lender. If people are giving you money to help you afford the down payment, they might have to write a letter to the lender explaining that.

- Employment: Lenders want you to be gainfully employed and likely to stay gainfully employed. Most will verify your employment status, usually by contacting your employer. If you own your business or are self-employed, you might have to provide documentation that proves your ownership and shows that your business is relatively stable.

- Home appraisal: A lender doesn’t want to lend you more than the home’s actual value. To confirm that the house is actually worth the sales price, they will order an appraisal before your loan is finalized. An independent appraiser will examine the home and determine its value.

How Conventional Home Loans Compare to Other Options

A conventional home loan is one mortgage option, but it’s not the only option available. Take a look at other types of mortgages and see how conventional loans stack up.

Conventional Loan vs. FHA Loan

The U.S. government created the FHA loan program to help first-time buyers and people who otherwise have trouble qualifying for a mortgage buy homes. Compared to a conventional home loan, an FHA loan typically accepts borrowers with lower credit scores. You can get an FHA loan with a small down payment, usually between 3.5% and 10%.

One notable difference between conventional and FHA loans is private mortgage insurance. You need to pay PMI on both types of loans if your down payment is under 20%. With an FHA loan, the mortgage insurance is for the life of the mortgage. With a conventional loan, you no longer need to pay PMI once your loan-to-value ratio is 80% or more. Another notable difference is that PMI is the same on an FHA loan, no matter your credit score. With a conventional loan, having a higher credit score can mean a lower PMI.

Conventional Loan vs. VA Loan

If you are a current or former member of the U.S. Armed Forces, a VA loan might be an option for you. VA loans are only available to veterans or current service members. They differ from conventional loans in a few ways. Perhaps the biggest difference between the two is that VA loans let you get a mortgage without putting any money down. Unlike a conventional loan, you don’t have to pay PMI on a VA loan. The Department of Veterans Affairs guarantees the mortgages.

Conventional Loan vs. USDA Loan

Depending on where in the country you want to buy a home, a USDA loan may be an option. You can get a USDA loan with little or no money down. The main criterion is that you need to purchase a home in a rural area that qualifies for the USDA loan program. If you want to buy in a city or a well-developed suburban area, a conventional loan is likely your better option.

Conventional Loan vs. Construction Loan

If you’re hoping to build a house from the ground up and need to finance the cost of construction, you will likely need to consider a construction loan. Construction loans cover the cost of building the home. Once construction is complete, the loan becomes due. You can convert it to a conventional mortgage at that stage.

Two types of construction loans exist. The first is a single-closing loan that automatically converts to a permanent, conventional mortgage after construction is finished. A two-closing loan has a separate closing process in the middle before the construction loan becomes a conventional mortgage.

Since conventional mortgages use the property you buy as collateral, and because there’s no property at the start of the construction process, you need a construction loan if you want to finance your new home purchase from the start.

Conventional Loan vs. Jumbo Loan

A jumbo loan is technically a conventional loan but has some features that make it different from other conventional mortgages. One key difference is the size of the loan. Jumbo loans are non-conforming loans, meaning they exceed the borrowing limits set by Fannie Mae and Freddie Mac.

Jumbo loans are higher-risk loans because of their size and because Fannie Mae and Freddie Mac won’t guarantee them. For that reason, they often have slightly stricter requirements compared to conforming conventional mortgages.

You’ll usually need a higher credit score, in the 700s at least, to qualify for a jumbo loan. A lender is also likely to want to see significant cash reserves and larger down payment. While you can qualify for a conforming conventional mortgage with a down payment of 5% or even 3%, you can expect a lender to want at least 20% down with a jumbo loan.

Another difference between conforming and non-conforming conventional home loans is the interest rate. Since the lender is taking on more risk by lending you more money, it’s also likely to charge you a higher interest rate, even if you have a down payment of 20% and an excellent credit score.

Can First-Time Home Buyers Get a Conventional Loan?

If you’re buying your first home, loan programs exist to make the process easier and more affordable to you. First-time homebuyer programs can help you buy a home with a smaller down payment and provide reduced PMI premiums. Depending on your needs and financial situation, a conventional mortgage might be the right option for you. You might also qualify for an FHA loan, VA loan or USDA loan.

Apply for a Mortgage With Assurance Financial Today

Assurance Financial offers home loans for all types of buyers, from first-timers to people looking to build a new home. You can apply online in just 15 minutes!

Sources:

- https://assurancemortgage.com/calculators/mortgage-calculator/

- https://singlefamily.fanniemae.com/originating-underwriting/loan-limits

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-debt-to-income-ratio-why-is-the-43-debt-to-income-ratio-important-en-1791/

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315/

- https://assurancemortgage.com/fha-loans/

- https://assurancemortgage.com/va-loans/

- https://assurancemortgage.com/usda-loans/

- https://assurancemortgage.com/how-to-finance-new-construction/

- https://assurancemortgage.com/jumbo-loans/

- https://assurancemortgage.com/first-time-home-buyer-loans/

- https://assurancemortgage.com/apply/

- https://singlefamily.fanniemae.com/originating-underwriting/mortgage-products/97-loan-value-options

Finding out you’re pregnant can come with a whole litany of emotions. Especially if it’s your first baby, you know you’re embarking on a whole new chapter of your life. Another exciting new chapter of life is when you purchase a home.

When these major life events overlap, you may find that excitement is overshadowed by anxieties and stress. Buying a home while you’re expecting a baby or on maternity leave can be challenging, but it doesn’t have to be. Our guide will help you navigate through the process of applying for a home loan while pregnant or after you’ve recently welcomed a new baby.

Topics Covered

- Can You Be Denied a Mortgage if You’re Pregnant?

- Maternity Leave and Mortgage Approval

- How to Get a Home Loan While Pregnant or on Maternity Leave

- How to Report Maternity Leave Discrimination

- What You Need to Get Approved

- Lending Discrimination Laws

Can You Be Denied a Mortgage if You’re Pregnant?

There are many reasons why someone might be denied when they apply for a home loan. Lenders must feel confident that applicants will keep up with their payments. This requires taking a detailed look at an applicant’s current situation in order to predict their future ability to pay off their loan. However, for some, their current situation may be a special circumstance that doesn’t necessarily indicate what their future will hold. One example of this type of situation is a pregnancy.

This is not an issue if you’re purchasing a home with a spouse or partner who could get approved on their own. If that is the case, you could still choose to apply jointly or could allow your partner to apply on their own, which could simplify the process. However, if you depend on both your and your co-borrower’s incomes to qualify for a mortgage, or if you are applying for a home loan on your own, then it’s critical you know how a pregnancy or new baby might affect the process.

You may have heard that pregnancy could keep you from getting a home loan, so it’s easy to feel like the odds are stacked against you when you’re applying for a mortgage while on maternity leave. Fortunately, you cannot legally be denied a mortgage just because you are pregnant. However, the financial implications of pregnancy can create some challenges in the home loan application process that make it more difficult for lenders to predict your future ability to make payments. So, can you be denied just because you are pregnant? No. But, does pregnancy affect a mortgage application? Quite possibly.

Do You Have to Disclose Pregnancy When Applying for a Mortgage?

It is understandable if you are hesitant about telling a mortgage lender you are pregnant or on maternity leave, considering how this information could affect their decision. If you are on parental leave while you’re trying to obtain approval for a mortgage, one issue is that you likely aren’t receiving paychecks equal to what you would normally receive.

Additionally, it may be unclear exactly what your future employment situation will look like. Perhaps you’ll want to switch to part-time when you go back to work, for instance. All these factors can put mortgage lenders on the alert since they make it more difficult to predict whether you’ll be a reliable borrower.

Being pregnant in and of itself shouldn’t affect your application at all. In fact, there is no place on a loan application where you are expected to indicate whether you’re pregnant, so this information can be kept completely private.

A mortgage lender does not have the right to ask you whether you are pregnant or on maternity leave when you apply for a loan. You are under no obligation to tell them about your pregnancy or maternity leave. However, it is generally recommended that you do disclose this information because these life changes can have a significant effect on your household finances, which your lender needs to know about.

If you do tell your lender about your maternity leave, they are not permitted to operate under the assumption that you won’t return to work once your leave ends, which takes most of the risk out of telling them. In addition, if your lender contacts your employer to confirm your employment and income, your employer is free to inform them of your maternity leave status.

To better understand how maternity leave can affect the process, let’s take a moment to look at how maternity leave typically works.

Maternity Leave and Mortgage Approval

Parental leave looks different depending on factors like where you’re employed, how long you’ve worked there and your personal preferences. Most companies are required to provide up to 12 weeks of unpaid family leave to their employees, as long as the employee has been working there for at least a year and could leave for a while without causing the company serious financial harm. Parental leave ensures an employee’s job will still be there waiting for them when they return from their time with their new child.

Some companies may offer their employees paid parental leave. Mortgage lenders look more favorably on this type of leave. More frequently, however, employees use other forms of paid time off, such as vacation days or sick leave to cover part or all of the time they’re away.

For most parents who take time off to bond with their new child, the financial benefits come through a combination of paid time off benefits from work and short-term disability benefits through their employer-provided insurance. Some states require employers to offer this type of insurance coverage for temporary medical needs.

Regardless of what sort of parental leave arrangement you have, in the world of mortgage lending, maternity leave is considered a type of temporary leave, according to the U.S. Department of Housing and Urban Development (HUD), Fannie Mae and Freddie Mac. In any temporary work situation, there can be challenges to getting approved for a home loan, but our tips below could help you get approved.

How to Get a Home Loan While Pregnant or on Maternity Leave

To bolster your chances of getting approved for a loan while you’re pregnant or on maternity leave, you should focus on making yourself a strong candidate overall for a loan, choosing a loan you can afford and making the terms of your maternity leave completely clear to the mortgage lender. Consider these actionable tips, so you can start preparing to apply for a home loan today:

1. Obtain a Loan Before You Go on Maternity Leave

Since closing on a house while on maternity leave can be tricky, you’re better off to purchase a home before you go on maternity leave, if possible. This isn’t just so you’ll have an easier time obtaining a mortgage. It should also make for a smoother transition. Some couples may feel overwhelmed with preparing for the arrival of a baby and want to put off purchasing a home until after the baby is born, and they are on maternity leave, paternity leave or both.

The reality, however, is that this is a time of transition where most parents will have their hands full caring for their newborn, making this an especially challenging time to deal with applying for a home loan, going house hunting, and moving. If you know you plan to purchase a home, start searching early, or choose to wait until after you’ve had your baby and gone back to work. We understand, however, that there are situations when you may not have a choice but to apply for a loan while on maternity leave.

2. Cushion Your Savings Account and Minimize Debt

If you need to submit a loan application on maternity leave, you can boost your chances of getting approved by optimizing your financial situation outside of your temporary change in income. This means avoiding taking on any new debt and paying down any debt you have, as well as cushioning your savings account.

Lenders will factor in the money you have on standby along with your income to determine whether you can afford a loan, so if your income appears to be lacking, you can make up for this in the money you have saved. Since there are costs associated with giving birth and caring for a child, lenders may factor in these expenses, so having more money saved will show you’re prepared to make your payments, even with the added costs you’re soon to or already experiencing from having a baby.

3. Find Out the Details of Your Parental Leave Arrangement

As you near the end of your pregnancy, it’s always wise to talk with your employer to make sure you are on the same page and understand the terms of your upcoming maternity leave. Make sure you have a plan for how long you’ll be gone, what compensation you’ll receive while you’re away and what your schedule will look like when you return.

Determining the details of your parental leave is especially important when you’re seeking a home loan — the more information you can provide to your lender, the better. If you can demonstrate to your lender that your parental leave won’t mean a sudden stop in your income or an indefinite employment future, you may be able to set their mind at ease and secure a loan.

4. Determine What You Can Afford

When buying a home, it’s always critical to carefully assess your current and future financial situation to determine what mortgage payment you can afford. This is true no matter what stage of life you’re experiencing and whether a pregnancy is in the picture or not. You’re more likely to get approved for a loan that fits comfortably within your budget than one that pushes the limits of what you can afford, so it’s wise to make sure you don’t stretch yourself too thin. This is what lenders fear and what leads to foreclosures.

If you’re expecting an addition to your family, this can impact your future financial situation, so it’s especially important that you take the time to figure out what sort of mortgage payment you can reasonably afford. Deduct medical costs associated with a birth and checkups for your infant, child care, and whatever other new expenses you’ll incur. Your lender will be thinking about these expenses, too, so it’s helpful if you can show you’ve thoughtfully considered your budget and are asking to borrow a reasonable amount.

5. Choose the Right Home Loan

Another piece of advice that applies to anyone looking to get approved for a mortgage is to choose the right loan option. This may mean doing some research and shopping around with different lenders to compare quotes. A loan adviser can help apprise you of your options and help you make the right choice. Choosing the right loan is critical if you want to get approved.

In addition to conventional loans, there are special types of mortgages for veterans, people with low credit scores, people borrowing a lot, and other special circumstances. Find the right type of loan, an interest rate you’re comfortable with, and the best plan for paying back your loan. Typically, conventional loans are designed to be paid off in 10, 15 or 30 years. If you’re stretching a bit financially, you’ll likely want to go with a longer period, so each payment is lower and fits better in your budget.

APPLY TODAY6. Be Transparent With Your Lender

If you apply for a home loan while pregnant, but before you go on maternity leave, you aren’t required to let your lender know, though they will likely ask whether you know of any upcoming changes to your household expenses, and the answer here would be yes. While you aren’t legally required to mention your pregnancy at all, if you’re applying for a home loan near the end of your pregnancy or just after you’ve had your baby, you’ll need to go the full disclosure route.

Let your lender know the details of your maternity leave, and let them know you’ve thought ahead and have calculated all your expenses, so you aren’t spreading yourself too thin with the loan you plan to take out. Within 10 days of closing on your home, your lender can call your employer to make sure you are still employed there and to verify your salary, so make sure your employer is prepared for this call and that there are no surprises for your lender if your employer states that you’re currently on leave.

How to Report Maternity Leave Discrimination

A mortgage lender will likely ask for proof of employment and income, especially if you’re on leave from your job for maternity reasons or otherwise. While mortgage lenders want to make loans, they must be careful about who they grant loans to. All mortgage lenders sell their loans, which means they need to be certain the loan will be purchased by an investor after the loan is made.

Because selling loans to investors can be a tenuous process, some lenders are quite conservative about who they select for loans. In particular, some lenders will be less flexible about lending to a borrower on any sort of leave, including maternity leave. Some mortgage lenders can cross the line from being cautious to discriminating against pregnant women.

Although it is normal for the loan qualification process to involve jumping through some extra hoops, a lender should never require a pregnant woman to end her maternity leave and return to work in order to receive mortgage loan approval. In fact, the U.S. Department of Housing and Urban Development (HUD) has deemed doing so a violation of the Fair Housing Act.

Still, the HUD has received complaints from borrowers about being discriminated against by mortgage lenders due to being on maternity leave. In response to these complaints, the HUD has fined many mortgage companies millions of dollars over the years, including large organizations like Wells Fargo Home Mortgage. If you feel a mortgage lender is violating your rights and breaking the law, you can file a complaint with the HUD online, over the phone or through the mail. The HUD will investigate your claim and issue a determination on the case at no cost to you.

[download_section]

What You Need to Get Approved

There are some important documents you’ll need to get approved for your home loan. Some of these documents are common to all applicants, and some are unique to applicants on maternity leave. When you’re applying for your mortgage, be prepared to submit the following documents:

- Tax returns: Tax returns provide lenders with a detailed history of your income, which can help them predict how consistent your income will be in the future. Lenders may ask for one or two years’ worth of tax returns. Pay stubs can show what your current income is, but tax returns give a bigger picture to your lender of what your income looks like over the course of a year or two.

- Proof of income: To show your current earnings, you’ll need to provide some sort of proof of income. This will commonly come in the form of pay stubs, but it may look different if you are self-employed or receive alternative sources of income. For example, you could provide a record of direct deposits into your bank account of 1099 forms.

- Bank statements: Bank statements show your lender how much money you have on standby to cover a down payment and to provide some cushion to help you pay your mortgage even if you have some unexpected expenses come up. You may also need to provide documentation of other assets, such as life insurance.

- Gift letter: If you’re fortunate enough to have a family member or friend who wants to help you purchase a home by giving you a financial gift, then you’ll need them to write a gift letter, letting the lender know the money is from them and is not a loan. Lenders check to see how long money has been in your account, so if they see a large sum show up seemingly out of nowhere, they’ll want it to know about it.

- Maternity leave verification: If you’re on maternity leave, it’s critical that you have your employer compose an official, signed letter on the company letterhead that confirms the details of your leave. It should, at the least, state when you plan to return to work and whether there will be any change to the number of hours you work.

Having these documents ready to go will streamline your application process and will enhance your chances of getting approved, assuming your finances are in a state that will allow you to afford to purchase a home, even if you are temporarily on leave.

Lending Discrimination Laws

The Fair Housing Act is meant to prevent discrimination in housing over the basis of things like ethnicity, religion, sex, and more. One type of prohibited discrimination specified by the act is discrimination based on familial status — this includes women and couples who are expecting a baby.

Another law to be aware of is the Family and Medical Leave Act. This is the law that entitles most employees to time off without worrying about their job security for qualified medical and family reasons, which includes having a baby. The only exceptions are if you have newly been employed by a company, if the company is extremely small or if your salary is in the very top tier of the company, which indicates that your absence will have significant consequences for the company.

Eligible employees are entitled to 12 workweeks of leave over the course of a 12-month period, as long as those 12 weeks are within a year of their child’s birth. Most parents choose to take off just before or at the time of birth and use most of the leave for bonding with and caring for their new baby. This law is not gender-specific, so both mothers and fathers are entitled to parental leave.

Taking both of these laws into account, new parents are well within their rights to take time off to have a baby and to buy a house during this time. If a mortgage lender doesn’t want to approve your application simply because you have a new baby or a baby on the way, this is technically a violation of the Fair Housing Act. However, it isn’t always so simple. This is because mortgage lenders are allowed to reasonably evaluate whether you are a reliable or a high-risk borrower based on your financial history, current situation, and future.

Banks are often leery of granting loans to pregnant mothers because of the financial risks associated with this stage of life — this is why hedging your bets in every way possible to show you are a reliable borrower is crucial. If you think you have been discriminated against purely on the basis of pregnancy, you may want to seek legal counsel or simply try another lender.

Apply for a Home Loan With Assurance Financial

Does being on maternity leave affect mortgage applications? Yes. Does it mean you are automatically disqualified from buying a home? Absolutely not. Make sure you work with an understanding and attentive lender to work through the mortgage application process, so they see the full picture of your financial situation and not just a glaring risk.

At Assurance Financial, we care about our customers, no matter their stage of life. We work with you to help you find the best loan option for your budget and your preferences, so you can focus on welcoming your new baby into your family instead of stressing over the complicated process of buying a home. We have experts licensed in 43 states to guide you to the best, customized option for your life stage. You can also apply online with Abby in just 15 minutes. Get started today to get one step closer to owning a home perfect for your whole family.

Linked Sources:

- https://assurancemortgage.com/how-do-you-calculate-your-estimated-mortgage-payment/

- https://assurancemortgage.com/mortgages-explained/

- https://assurancemortgage.com/what-is-considered-a-good-mortgage-rate/

- https://www.hud.gov/topics/fair_lending

- https://archives.hud.gov/news/2014/pr14-124.cfm

- https://www.hud.gov/program_offices/fair_housing_equal_opp/online-complaint

- https://www.hud.gov/program_offices/fair_housing_equal_opp/fair_housing_act_overview#

- https://www.dol.gov/agencies/whd/fmla

- https://assurancemortgage.com/apply/

Is your dream home a little more expensive than most lenders will agree to? Well, have no fear, a jumbo loan is the best way to get the financing you need for your dream home. Jumbo loans were created to help people move into a dream home, even if it was more than most lenders would agree. Because of the amount of money involved, the risk of this type of loan is high. Jumbo mortgages typically exceed conforming loan limits to get buyers into luxury properties. More recently, jumbo mortgage rates have been historically low, which is attractive to people wanted to borrow large amounts. In addition to low rates, interest on jumbo loans — up to $1 million— can be tax deductible, but you’ll need to check with a qualified accountant. If you want a loan amount over the conforming limit, it is possible to use a non-jumbo conventional loan plus a second mortgage to make up the difference.

When & How are Jumbo Loans Helpful?

If you’ve heard the term “Jumbo Loan” before and have been confused as to what it means, that’s understandable. The “Jumbo” in “Jumbo Loan” doesn’t refer to the size of the house, rather, the price. A Jumbo Loan is a mortgage loan exceeding the loan limits established by government regulation. The jumbo loan limit is $424,100. However, it does go up to as much as $625,000 in more high-cost areas of the country. Jumbo loans do not fit the typical standards of mortgage loans, so they are a great way for qualified buyers to purchase a luxury home. The ideal bowers will have low debt-to-income ratios, high credit scores, and the ability to put down a large down payment. If you fit these requirements, you may find that a jumbo loan will get you into the house you desire. If this fits your situation, let us know. We’ll get you the financing you need at payments you can afford!

APPLY TODAY[download_section]

What Does My Credit Score Need to be to Qualify for a Jumbo Loan?

The higher, the better. Typically, to get approved for a Jumbo loan you need a credit score of 700 or above. However, this may vary with lenders. Typically, lenders will require a down payment of at least 20 percent. This price range is because there are no private mortgage insurance options for Jumbo loans. As with the mortgage, interest rates will vary depending on the lender. However, due to the amount involved, interest rates can exceed $1 million. The good news is that this amount is tax deductible. If the price of the home you want to buy is over $424,100, then this loan is for you. Anything above this range is beyond government regulations, so there are not private insurance options.

If your dream home required you to apply for a jumbo loan, contact one of our home loan experts today! We will help you get everything you need to get approved as quickly as possible.

The common myth that the mortgage loan process is a nightmare is just that…a myth. Though it is a process, it can easily be broken down into six key phases: pre-approval, house shopping, mortgage application, loan processing, underwriting, and closing. At Assurance Financial, our goal is to help you realize your dream home and our team of home loan experts are here to help you along the way. Let’s dive in and help you understand the six phases before you begin the process:

1. Mortgage Application

Before you start your mortgage application, obtain copies of your most important financial documents. Lenders review your application to see if you’re financially prepared to handle a mortgage and pay it back over time. Your application is examined by lenders seeking information about your sources of income, credit history, job history and self-employment income. If you are self-employed, they’ll need to see your last two tax returns to prove consistent income.

After you’ve completed the loan application, your lender will verify the information you’ve provided. Expect to receive a loan estimate and a commitment letter from your lender shortly after submitting your application.

2. Housing Payment/Debt-to-Income Ratio

Lenders also consider your debt-to-income (DTI) ratio before pre-approval. Dividing your projected total housing payment by your gross monthly income produces a figure known as a front-end DTI ratio. Including your current monthly liabilities along with the proposed monthly housing payment in the calculation generates your back-end or total DTI ratio. The ideal front-end DTI to back-end DTI ratio is about 25%/41%. More conventional loans will allow a back-end of 50%, and FHA will even allow 56.99%.

3. House Shopping

It takes time to find the right home. At the beginning of the house shopping process, you should make a list of the things you need to have in your future home. Start by considering how many bedrooms and bathrooms you’ll require and always take into account how your family may grow in the future. Will you need a large backyard for your children or pets to play? After considering the basics, take some time to determine what kind of neighborhood you’d like to live in. Gather details on local school districts, shopping centers, commute times, and any safety concerns.

4. Loan Processing

Next, your loan is sent over to the loan processors. Once it’s in their hands, they begin double-checking everything on your application. The processor will prepare and organize the file before it’s sent over to the bank or mortgage lender for approval. They will contact your employer to verify your job and the salary on your application. If there are any questions regarding the information on your application, they will have your loan officer contact you for details. Any mistakes you’ve made will arise during this stage, giving you a chance to make corrections before the file is handed off to the underwriter.

[download_section]

5. Underwriting

The underwriter will examine your application to determine whether you’re a risk to the lender. Your income, debt, and credit history are the greatest factors in the underwriting process. Your total monthly debt obligations, including the potential mortgage payment, shouldn’t be more than 43% of your pre-tax monthly income.

6. Closing

Once you’re approved, the realtor will complete a final walk-through to ensure all contingencies are met. Closing is next! Along with a representative, you’ll sign all the final documentation and verify the money from the sale is properly distributed. The closing officer will review the mortgage note and the mortgage document with you, then move on to the closing disclosure.

Next, they will review the deed and the commitment for title insurance. The final activity is the distribution of the money from the sale. The closing agent will issue checks to the sellers, the seller’s lender, the real estate agent, and any other person indicated on the closing disclosure. Once you’ve signed all the documents and made the appropriate payments, the closing is finished and the home is yours!

Purchasing a home is one of the biggest decisions an individual will make in their lifetime. No matter where you are in your life, it’s a process that requires experts and those interested in the best outcome for you. Our loan officers are here to help you find the best mortgage possible. Find a loan officer near you today!

So, you’re ready to buy a house, but you don’t know what type of loan you need. The type of loan you end up choosing shapes the future of your homeownership. Here’s a rundown of loan programs that are the most common:

Conventional Loans

Conventional loans are the most popular and economical loans available. A conventional loan is a mortgage that isn’t guaranteed or insured by any government agency. The loan typically includes fixed terms and rates. Borrowers typically need a pretty good credit score to qualify for a conventional loan along with a minimum of 3% down payment. The maximum loan amount for a conventional loan is $424,100. If the homeowner makes a down payment of less than 20% on the home, then lenders will require private mortgage insurance (PMI). PMI is configured by the lender and protects them if you stop making payments at any time. Once the loan-to-value ratio reaches 80% on a conventional loan, PMI is no longer required.

FHA Loans

An FHA loan is a mortgage insured by the Federal Housing Administration. These loans are popular thanks to high DTI (debt-to-income) ratio maximums, and many lenders approve borrowers with credit scores as low as 580. FHA loans typically require a down payment of at least 3.5% and offer low rates that usually sit about .25% lower than conventional loan rates. The national maximum loan amount for an FHA loan is $294,515 but varies by county/parish. In high-cost areas, county-level loan limits can be as high as $679,650. Lenders require two mortgage insurance premiums for FHA loans: The upfront premium is 1.75% of the loan amount, and the annual premium varies based on the length of the loan. The monthly mortgage premium is .85% of the base loan amount for the remainder of the loan.

USDA Rural Housing/Rural Development (RD) Loans

USDA loans are issued through the government-funded USDA loan program. The government designated these loans for homes in rural areas. The program focuses on improving the economy and quality of life in rural America. USDA loans typically offer lower rates than conventional loans and hold several similarities to FHA loans. The income limit for USDA loan recipients is $78,200 for a one to four person home and $103,200 for a household of five or more. Mortgage insurance for a USDA loan requires a 1% upfront fee of the loan amount, and a monthly mortgage insurance fee equal to 0.35% of the loan balance. As with the loan limits, income limits will also vary based on parish/county.

Veterans Affairs (VA) Loans

VA loans have helped more than 21 million veterans, service members, and surviving spouses achieve the dream of home ownership. This benefit – most praised by home buyers for offering $0 down, low rates, and removing the added cost of mortgage insurance – is made possible by the U.S. Department of Veterans Affairs guaranteeing a portion of each loan in case of default. Veterans who are eligible for a VA loan have what is referred to as VA loan entitlement, which is a specific amount that the Department of Veterans Affairs promises to guarantee. This entitlement is what gives lenders the confidence to extend VA loan financing with exceptional rates and terms. However, to be eligible for the VA loan, potential home buyers must first meet the basic service requirements.

The type of home, its location, and your situation are all factors that determine the type of loan that is right for you. If you need guidance, Assurance Financial’s loan officers are home loan experts who can help. Contact us today!

[download_section]

You may be wondering what creditors take into account when determining your credit score. There are five factors involved in calculating your credit score, each varying in importance and value to credit scoring models. Here are the five more common criteria of what determines your credit score:

1. Payment History (35%)

The most important factor in determining your credit score is whether you pay your bills on time. Credit scoring models examine all the credit you’ve already been extended, including credit cards, auto loans, installment loans and any other line of credit. Any late or missed payments are noted and may negatively impact your credit score.

2. Debt/Amounts Owed (30%)

The second most important determining factor is the balance-to-limit ratio on your credit cards. Models will examine how much of the total credit line you’re using on all of your credit cards. In general, you should try to keep your utilization rate below 30% to avoid lowering your credit score. Keeping your balance below 108 will help you achieve a higher score.

3. Age of Credit History (15%)

The credit score calculation also reviews the age of every account you hold. Scoring models favor users who show they’ve been able to handle several credit accounts over time without penalties, late fees or closures.

4. New Credit/Inquiries (10%)

Your credit score will also reflect how much credit you’ve received or applied for recently. Any credit you’ve applied for within the past three to six months or new inquiries from creditors are recorded and used during calculations. The scoring model doesn’t consider requests a creditor has made to review your credit file or score to build a preapproved credit offer. Nor does it account for any personal requests you’ve made for a copy of your credit history.

5. A mix of Accounts/Types of Credit (10%)

Creditors like to see you’ve been able to balance multiple tradelines of different types. The scoring algorithm examines the types of credit accounts you have, including revolving debt and installment loans.

The above are the most common factors determining your Credit Score. Be aware that your Credit Score is one of a number factors we consider when determining your home mortgage loan. The best way to know if you qualify, and for how much, would be to discuss your situation with one of our home loan experts. Contact an Assurance Financial Loan Officer now!

[download_section]