Category: Purchasing a Home

In the U.S., most of the population lives in urban areas. But for some people, living in a rural or country area is more appealing. If you prefer rural living over city life, a program from the United States Department of Agriculture (USDA) can help you buy a home. Every year, the USDA uses its Rural Development program to invest about $20 billion in helping families across the United States buy and improve their homes. The program was created to boost rural economies and improve quality of life.

Below we’ve mapped out an overview of the USDA Rural Development Guaranteed Housing Loan Program, explaining how it works and if you’re eligible for loans.

Topics Covered

- What Is a USDA Loan?

- Types of USDA Loans

- Who Should Get a USDA Loan?

- Pros and Cons of a USDA Loan

- Who Qualifies for a USDA Loan?

- Other Mortgage Options

What Is a USDA Loan?

The USDA loan program is part of the department’s single-family housing program. It aims to encourage the purchase of homes in rural or suburban areas by making mortgages easier for borrowers to obtain. Compared to conventional loans and other types of government-guaranteed loans, USDA loans have lower down payment requirements and lower income requirements. The loans also have strict income and location requirements.

USDA loans fall into several categories, with some only available to borrowers with the lowest incomes. The loans can be directly from the USDA or offered by private lenders and guaranteed by the department. The USDA’s Rural Development program also offers grants to individuals who want to work on housing construction projects.

Although the goal of the USDA loan program is to make homeownership more available to a wider swath of buyers, there are certain requirements people need to meet before they are eligible for the loans. The USDA’s programs have income limits and often have credit score requirements.

USDA loans are sometimes known as Section 502 loans. The mortgages seek to provide very-low to moderate-income buyers with access to sanitary, decent and safe housing in eligible areas.

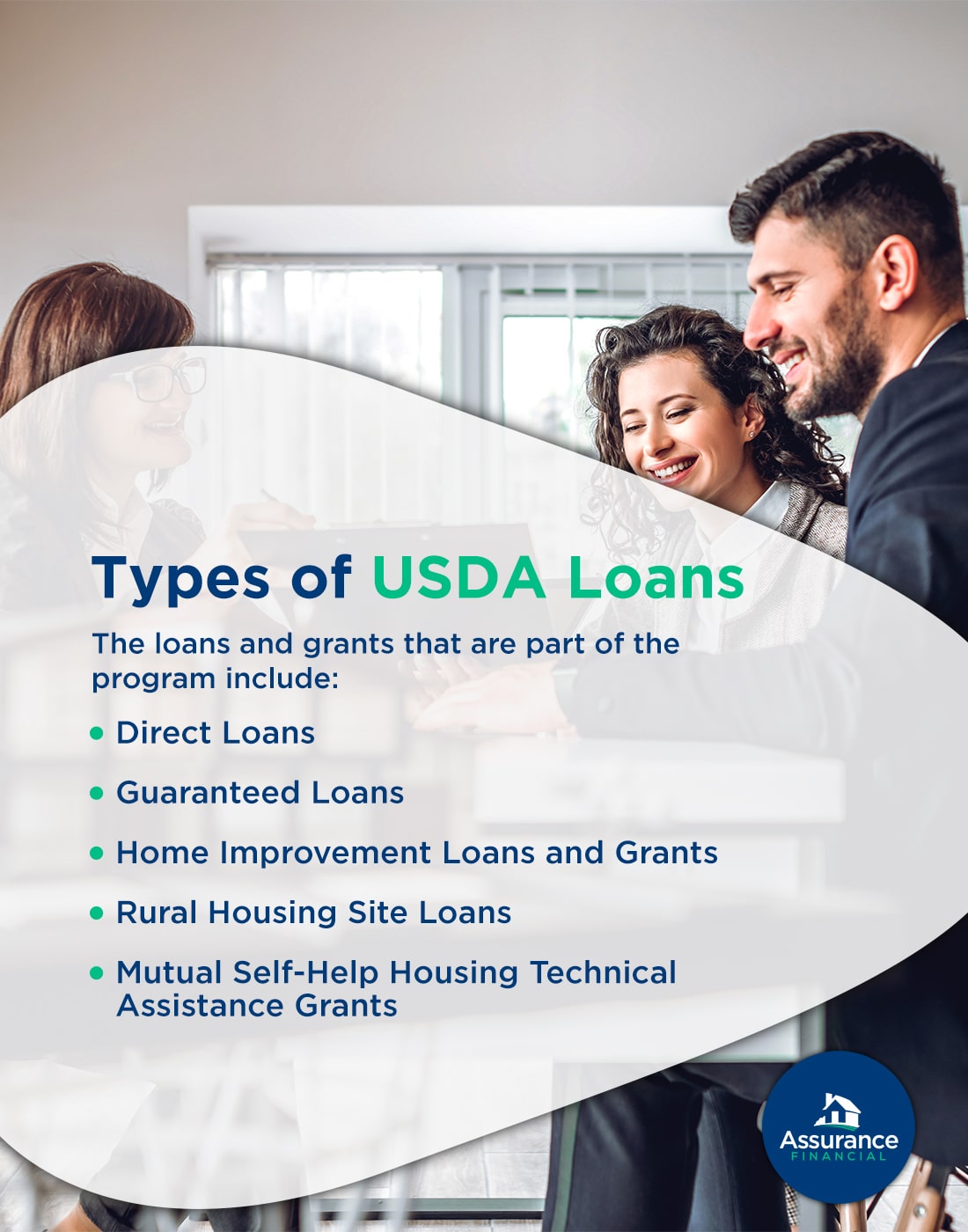

Types of USDA Loans

The USDA’s Single-Family Housing program includes several types of loans that are made directly to borrowers, in addition to grants and loans made to organizations that help lower-income individuals purchase or improve their homes. The loans and grants that are part of the program include:

1. Direct Loans

These mortgages are designed to suit low- to very-low-income applicants. The income threshold varies by region, and with subsidies, interest rates can be as low as 1%. Direct loans come from the USDA, not from a private lender.

To qualify for a direct loan, a borrower needs to:

- Have an income below the “low income” limit for their area.

- Be in need of safe and sanitary housing.

- Agree to live in the home as their primary residence.

- Be legally able to take on a loan.

- Be unable to get a mortgage through other means.

- Be a U.S. citizen or eligible non-citizen.

- Be allowed to participate in federal programs.

- Be able to repay the debt.

The house a person buys with a direct USDA loan needs to meet several requirements, too. As of 2021, it needs to be less than 2,000 square feet and should be situated in a rural area with a population under 35,000. The value of the house needs to be less than the loan limit for the area. It can’t be used for income-producing activities and can’t have an in-ground pool.

Borrowers who get payment assistance can end up with rates as low as 1%. The USDA allows people to get direct loans with 100% financing, meaning they don’t have to make a down payment. Although the repayment period is typically 33 years, there is an option to extend it to 38 years based on a borrower’s income eligibility.

Since loans in the direct loan program come straight from the USDA, people who are eligible and interested in applying for one should apply directly through their local Rural Development office. The loan program is open year-round.

2. Guaranteed Loans

While direct loans come from the USDA itself, guaranteed loans come from private lenders. The loans are backed by the USDA, meaning that it will step in and pay if the borrower defaults on the loan. The lending requirements for a guaranteed USDA loan are slightly looser than the requirements for a direct loan.

Borrowers need to be U.S. citizens or eligible non-citizens. They need to meet income requirements, but the maximum income allowed is higher than for the direct loan program. Eligible borrowers need to earn no more than 115% of the median income in their area. As with the direct loan program, people who get a guaranteed USDA loan need to live in the home as their primary residence.

Location requirements are a little looser for the guaranteed loan program, as well. The location should be a rural area, but some suburban areas also qualify. Potential borrowers can put their address into the USDA’s eligibility website to verify that it qualifies for a mortgage.

People who get a guaranteed loan from the USDA can get 100% financing, meaning no down payment is needed. The USDA will guarantee up to 90% of the loan amount. People can use the loans to buy, build or rehab a qualifying home.

3. Home Improvement Loans and Grants

The USDA loan program also includes loans and grants that help homeowners modernize, improve or repair their homes and grants that help older homeowners pay to remove safety and health hazards from their homes. Eligible homeowners need to earn less than 50% of the median income for their area.

As of 2021, the maximum loan amount is $20,000 and the maximum grant amount is $7,500. Homeowners who qualify for both a grant and a loan can combine them, receiving a maximum of $27,500. People who receive a USDA home improvement loan have 20 years to repay it. While the grants usually don’t need to be repaid, if a homeowner sells their property within three years of getting the grant, they will have to pay it back.

Both grants and home improvement loans come directly from the USDA, and availability can vary based on area and time of year. Eligible individuals can apply for a loan, grant or both at their local Rural Development office.

4. Rural Housing Site Loans

While direct and guaranteed USDA loans are available to individual borrowers, the department also has loan programs for organizations that provide housing to low-income or moderate-income homebuyers. Eligible organizations include nonprofits and federally recognized tribes. The loans have term limits of two years and either charge a 3% interest rate or a below-market rate, depending on the loan type.

5. Mutual Self-Help Housing Technical Assistance Grants

USDA technical assistance grants are given to nonprofits or federally recognized tribes that help very-low and low-income individuals build their own homes. The homes need to be located in eligible areas and the people who will live in the homes need to perform most of the labor of building the houses, with some assistance from the organization. The grant money can be used to help recruit people to the program and to provide supervisory assistance to families, but it can’t be used to fund the actual construction of the home.

Who Should Get a USDA Loan?

When you’re buying a house, you have a lot of decisions to make, such as the location of your new home, its size and its amenities. You also need to choose the type of mortgage you get. Whether a USDA loan is right for you or not depends on a few factors.

The loans are designed to encourage people to buy homes in rural areas. But the USDA’s definition of a rural area, at least for its guaranteed loan program, might be much broader than you think it is. Often, homes in suburban areas qualify for USDA loans. The only areas that are fully excluded are metropolitan or urban ones, so if you know you definitely want to buy in a city, the USDA loan program may be off the table for you.

Your income can also determine whether or not the USDA loan program is right for you. Buyers need to meet income limits, so as long as you qualify as a very low to moderate-income earner in your area, you may be eligible.

It can also be worth determining what other loans you qualify for, if any. Usually, USDA loan borrowers can’t get financing through other means, such as a conventional mortgage or FHA loan. If that describes you, it may be worthwhile to seriously consider a USDA loan.

Apply Now

Pros and Cons of a USDA Loan

While there are many benefits to a USDA home loan for the right applicant, these mortgages aren’t for all borrowers. Let’s take a closer look at the advantages and drawbacks of the loan program:

Pros of a USDA Loan

Some of the benefits of getting a USDA loan include:

- 100% financing available: Saving up for a down payment can be difficult, especially if a potential homebuyer earns just above or below the median income in their area. USDA loans let people get mortgages without putting any money down. The loans don’t have private mortgage insurance requirements, which can help buyers save more. Since the USDA guarantees 90% of the loan note, the risk to lenders is reduced.

- Open to very-low and low-income borrowers: Qualified borrowers need to earn 115% or less of the median income in their area to get a guaranteed USDA loan. The income limits for direct loans and home improvement loans and grants are even lower. The loans make it possible for people to buy a home who may otherwise struggle to get approved for a loan.

- Open to borrowers who can’t get other loans: In addition to opening up mortgages to people who don’t have high enough incomes, the USDA loan program makes it possible for borrowers who aren’t eligible for conventional or other types of home loans to buy a home. The loan program removes barriers such as down payments from the process.

- Fixed-rate interest: The interest rate on a guaranteed USDA loan is fixed for the life of the loan. The fixed-rate offers stability to borrowers.

- Long repayment period: USDA direct loans allow people 33 or 38 years to repay their mortgages. The 38-year term helps to ensure low-enough monthly payments for very low-income borrowers. Loans the USDA guarantees have a 30-year repayment term.

Cons of a USDA Loan

Some potential drawbacks of a USDA loan include:

- Restrictions on the location: USDA loans aren’t for people who want to live in cities or highly developed areas. The loans are exclusively for purchasing a home in rural or certain suburban areas. While the loans can’t buy homes in places like San Francisco, Philadelphia or New York City, the total area that does qualify for a USDA loan is likely larger than you think.

- Restrictions on housing type: USDA loans need to pay for a single-family residence. The direct loan program has more restrictions than the guaranteed loan program. Homes purchased with a direct loan need to be “modest in size” and can’t have in-ground pools. For both types of loans, the borrower needs to live in the house they buy.

- Loan limits may apply: Limits for a USDA loan are typically based on a borrower’s income and how much they can repay. For direct loans, the price of the home needs to be below the limit set for the area. The limit is often about $285,000but can be more in areas with a higher cost of living.

[download_section]

Who Qualifies for a USDA Loan?

Income limits to qualify vary by region and size of household. Consult the USDA map and table to find specific requirements for your location. The loan program only funds owner-occupied primary residences. You must be a U.S. citizen and have a dependable income to qualify.

Other qualifications include making a monthly payment that is 29% or less of your monthly income and good credit history. Metropolitan areas are excluded from the program. However, some suburban areas may qualify. Also note that you don’t have to be buying your first home to get a USDA loan.

Income Qualifications

You’ll need to provide proof of income to qualify for a guaranteed USDA loan. If you’re self-employed or work as a seasonal employee, you need to provide two years of income records. People who have full-time or part-time, year-round employment only need to provide proof of income for one year. The income limit varies based on your location and how many people live in your home.

Asset Qualifications

Since the USDA loan programs don’t require a down payment, you don’t have to show proof of assets like you would when applying for a conventional loan. You won’t have to verify that you have a down payment or that you have a sufficient amount of cash reserves when you apply for the loan.

Credit Qualifications

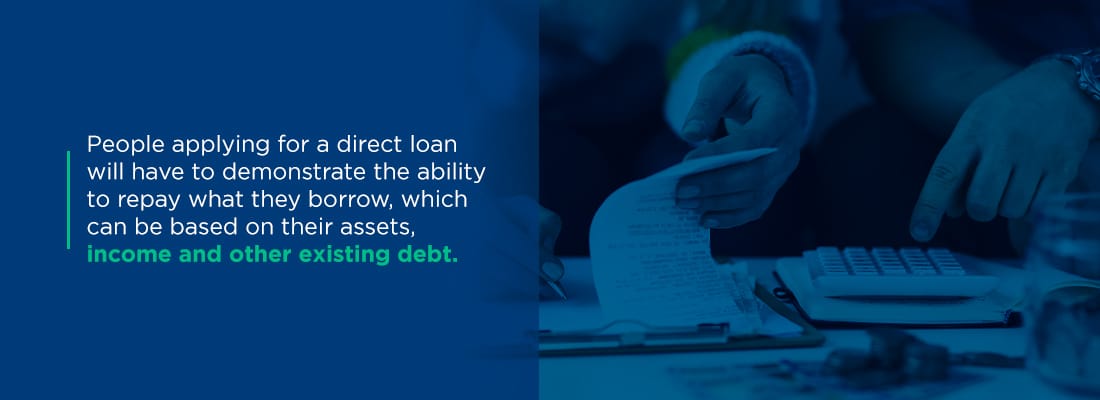

The USDA doesn’t outline specific credit qualifications for the guaranteed or direct loan programs. People applying for a direct loan will have to demonstrate the ability to repay what they borrow, which can be based on their assets, income and other existing debt.

People applying for a guaranteed USDA loan also need to demonstrate an ability to repay the loan. The individual lender might also require a certain credit score, but the USDA doesn’t outline any credit requirements.

In some cases, borrowers who don’t have traditional credit might be able to use alternative forms of credit to demonstrate their creditworthiness and ability to repay to a lender. Non-traditional credit options might include rental payment history, auto insurance payment history or utility bill payment history. If you’re considering applying for a USDA loan, your lender can provide you with more specific details about credit requirements.

Debt-To-Income Ratio

To keep people from borrowing more than they can comfortably afford to pay back, the USDA loan program has recommended monthly payment and debt-to-income limits for borrowers. If you get a USDA loan, the total amount of your housing payment shouldn’t be more than 29% of your income before taxes. For example, if you earn $2,000 per month, your housing payment should be no more than $600. Your housing payment is more than just the principal and interest on the mortgage. It also includes:

- Homeowners insurance

- Property taxes

- Homeowners association fees or dues

- Rural Development annual fee

Your total debt-to-income ratio needs to be low, less than 41%, to qualify for a USDA loan. Your total monthly debt might include:

- Student loan debt

- Credit card debt

- Car debt

If you earn $2,000 per month, no more than $820 of that should go toward debt payments, which includes your housing payments and any other loans you have.

Other Mortgage Options

For borrowers who meet income requirements and who want to buy in an eligible rural or suburban area, a guaranteed or direct USDA loan can be a great deal. It lets you become a homeowner without having to save up a hefty down payment and without having to have a high income.

It could be that you’re not eligible for a USDA loan due to your income or where you want to live. In that case, you still have plenty of options available:

- Conventional mortgage: You do have to make a down payment with a conventional mortgage, usually between 3% and 20%. If you put down less than 20%, you also have to pay private mortgage insurance premiums. Conventional mortgages tend to have stricter lending requirements than other options, meaning you typically need to have a very good or excellent credit score to get approved and to get the best rates.

- FHA loan: An FHA loan is another type of government-backed mortgage. It’s designed to help people with smaller down payments and less-good credit buy a home. You can put down between 3.5% and 10% to get an FHA loan, and you’ll need to pay mortgage insurance for the duration of the loan.

- VA loan: Like USDA loans, VA loansoffer 100% financing, meaning no down payment is needed. The loans are backed by Veterans Affairs and are only available to former or current members of the armed services and their widows.

Choosing the right mortgage is as important as choosing the right home. The right lender can help you weigh the pros and cons of each mortgage option so you choose the one that works best for you.

Apply for a USDA Loan With Assurance Financial Today

Does a guaranteed USDA loan seem like the right choice for you? Start your application with Assurance Financial today. Our online application streamlines the paperwork process, so there’s no need to scramble to find the right documents. Get started today!

Linked Sources:

- https://www.rd.usda.gov/programs-services/single-family-housing-direct-home-loans

- https://www.rd.usda.gov/programs-services/single-family-housing-guaranteed-loan-program

- https://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do?pageAction=sfp

- https://www.rd.usda.gov/programs-services/single-family-housing-repair-loans-grants

- https://www.rd.usda.gov/programs-services/rural-housing-site-loans

- https://www.rd.usda.gov/files/RD-SFHAreaLoanLimitMap.pdf

- https://assurancemortgage.com/conventional-loans/

- https://assurancemortgage.com/fha-loans/

- https://assurancemortgage.com/va-loans/

- https://assurancemortgage.com/apply/

Many homebuyers make a list of the things they’d like in their new home — including the number of bedrooms, the types of amenities and the size of the yard, to name a few. When shopping for a home, it’s just as important to make a list of things you’d like from your mortgage — including the length of the loan, the interest rate and the repayment terms.

You have lots of options when choosing a mortgage. Some home loans are designed for people who meet specific criteria, and others for people who might not qualify for another type of loan. Take a look at some of the different types of mortgages available and what they offer to find the best mortgage for you.

Table of Contents

- What is a Mortgage?

- What Mortgage Do I Need?

- Fixed-Rate Mortgages

- Adjustable-Rate Mortgages

- Other Mortgage Options

- Programs to Help You Get a Mortgage

- Apply with Assurance Financial Today

What Is a Mortgage?

A mortgage is a type of loan you acquire to purchase a home. When you apply and are approved for a mortgage, the lender agrees to let you borrow a sum of money that is usually less than the home’s value. You need to repay the mortgage according to the terms of the loan. Most mortgages require you to make monthly payments of principal, interest and other fees, such as private mortgage insurance (PMI).

When you have a mortgage, the home acts as collateral. If you stop making payments and don’t work something out with the lender, they can foreclose on the home. Since the home is collateral, many mortgages have lower interest rates than unsecured loans, such as personal loans or credit cards.

When choosing a mortgage, there are several things to pay attention to:

- The length of the loan term:30 years is a popular mortgage term, but 10, 15 and 20-year mortgages are also available.

- The size of the interest rate: The market influences your interest rate, as does your credit score, income and loan size.

- The type of interest rate: Your rate can be fixed, meaning it will stay the same throughout the life of the loan or adjustable.

- The type of fees, such as PMI, lender’s fees and other fees: You’ll most likely need to pay an assortment of closing costs and may need to pay fees such as PMI premiums each month.

- The loan size:The amount you borrow depends on the size of your down payment, the cost of the house and what you can afford.

What Mortgage Do I Need? The Best Type of Mortgage to Get

How do you know which mortgage is right for you? It helps to consider your financial stability, your employment situation and your credit history. Two broad categories of mortgages exist, private loans and government-backed loans. Private loans often have stricter requirements, while government-backed loans are guaranteed by various federal agencies or departments and have looser requirements.

Your lender will let you know which mortgages you qualify for and help guide you to the one that best meets your needs. Get to know some of the most common mortgage options:

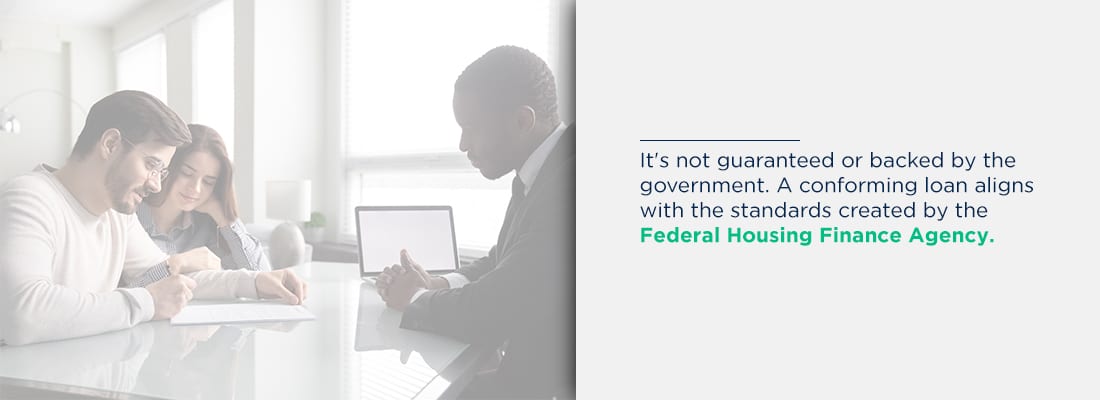

1. Conventional Conforming

A private lender makes a conventional mortgage. It’s not guaranteed or backed by the government. A conforming loan aligns with the standards created by the Federal Housing Finance Agency. One of those standards is a loan limit for all loans that Freddie Mac and Fannie Mae purchase. As of 2021, the limit for a conforming loan is $548,250* for a single-family home. The limit in areas with a high cost of living and higher-than-average housing prices is $822,375*.

You need to meet stricter requirements to qualify for a conventional loan. One of the requirements is a higher credit score. While you might get approved for a conventional loan with a score around 620, to get the best possible terms, including the lowest possible interest rate, it’s better to have a score in the mid-700s or higher.

The down payment requirements for a conventional loan are typically different than for other mortgage types. The standard advice is to put down at least 20% to get a conventional mortgage. But your lender might be willing to approve you if you have a smaller down payment. If you put down 5% or 10%, you can expect to pay PMI premiums in addition to your monthly principal and interest payments. How long you need to pay for insurance depends on how long it takes you to pay off at least 20% of the home’s value.

Once the loan-to-value ratio is 80% or less, you can ask the lender to remove the PMI premiums. The lender should automatically cancel your PMI premiums when the loan-to-value ratio falls to 78%.

A conventional conforming mortgage offers you a fair amount of flexibility. You can choose the mortgage term and the type of interest rate, such as fixed or adjustable. Some conventional loan programs even allow you to put down just 3% of the home’s value, making homeownership potentially more attainable and affordable.

Are you eligible for a conventional loan? Review these requirements to determine whether you qualify for this mortgage loan type and whether it’s right for you:

- Your credit score is above average. A higher score can potentially result in a lower interest rate, especially for those with a score over 740.

- You have a reasonable or low debt-to-income ratio. The ratio of your financial obligations to your monthly income should not exceed 43%.

- You have saved up enough for a down payment between 3% and 20%. Keep in mind that with a smaller down payment, you will most likely need to buy private mortgage insurance.

2. Conventional Non-Conforming

Some homes cost way more than the conforming loan limits set by the Federal Housing Finance Agency due to the home’s size, amenities or location. You can still get a mortgage for an expensive home, but the type of mortgage you get will be slightly different from a conventional conforming loan.

Conventional non-conforming mortgages are also called jumbo loans due to their size. As a general rule, lenders consider jumbo loans to be riskier than conforming loans. The borrower is borrowing more from the lender, so there is a slightly higher risk of default. For that reason, jumbo loans traditionally have slightly higher interest rates than conforming loans. They also usually have stricter eligibility and down payment requirements.

For example, while you might get a conventional conforming loan with as little as 3% down, you can expect to put down at least 20% to get a jumbo loan. You also need a higher credit score to qualify for a jumbo loan. Usually, the minimum score a lender will consider is 700. The higher your score, the more likely you are to get approved and potentially get a lower interest rate.

A lender will also carefully consider your debt-to-income ratio before approving you for a jumbo loan. The more existing debt you have, the less likely you are to get approved for the loan. There is a limit to jumbo loans. Usually, the maximum amount you can borrow to buy a single-family home is around $1 million.

Are you eligible for a jumbo loan? Review these requirements to determine whether you qualify for this mortgage loan type and if it’s right for you:

- Your credit score is above average.

- You have a debt-to-income ratio below 36%.

- You have saved up a hefty down payment, at least 20% of the home’s price.

- You need to buy a home that costs more than the conforming loan limit.

[download_section]

3. FHA

Government-sponsored mortgage programs aim to help people who might have difficulty qualifying for conventional loans purchase a home. The first type of government-backed mortgage is an FHA loan. The FHA loan program dates back to 1934. The government created it to ease credit requirements, allow for smaller down payments and reduce closing costs, making it possible for people to buy their first homes.

Usually, FHA loans allow borrowers to put down between 3.5% and 10% of the home’s value. How much you need to put down depends on your credit score. FHA loans allow borrowers to have slightly lower credit scores than conventional mortgages. To get an FHA loan with a 3.5% down payment, your score must be at least 580. If your score is at least 500, you’ll need to put down 10%.

Although FHA loans are government-backed, the mortgages themselves don’t come from the government. Instead, private lenders issue them with the understanding that the government will step in and cover the cost if the borrower defaults or stops making payments on the loan. The government guarantee protects the lender from losing too much money on a potentially risky loan.

In exchange for the government’s backing, you need to pay mortgage insurance if you decide to take out an FHA loan. FHA mortgage insurance is slightly different from the PMI premiums you pay on a conventional mortgage. First, the mortgage insurance is for the entire term of the loan if your down payment is under 10%. Unless you refinance an FHA loan to a conventional loan at some point, you’ll be responsible for premiums from the first payment until the last. You’ll also have to pay a mortgage insurance premium upfront, along with a monthly premium.

FHA loans can have terms of 15 or 30 years. The interest rate is fixed, meaning it stays the same throughout the entire term. An FHA loan might be a good option if you’re having trouble qualifying for a conventional loan due to a lower credit score or lower income.

Are you eligible for an FHA loan? Review these requirements to determine whether you qualify for this mortgage loan type and whether it’s right for you:

- You have a FICO credit score in the range of 500 to 579 with a down payment of at least 10%.

- You have a FICO credit score of at least 580 with a down payment of at least 3.5%.

- You’ve been employed for the past two years.

- You can verify your income with pay stubs, bank statements and tax returns.

- Your FHA loan will be used for your primary residence.

- Your property is appraised and meets property guidelines.

- Your monthly mortgage payments won’t be more than 31% of your monthly income. Some lenders may allow up to 40%.

4. VA

VA loans are available to people who are veterans or who are currently serving in the armed forces. Similar to an FHA loan, a VA loan is government-backed. In this case, Veterans Affairs guarantees the mortgages, which private lenders issue.

VA loans have two distinct advantages over conventional and FHA loans. The first advantage is that they don’t require a down payment. They are one of the few types of mortgages available that allow for 100% financing. Unlike conventional or FHA loans, you don’t have to pay mortgage insurance premiums on a VA loan, even if you put down 0% upfront.

VA loans also offer reduced closing costs. If you take out a VA loan, you need to pay the VA funding fee, which ranges from 1.4% to 3.6%, depending on the size of the down payment and whether you’re buying your first home or not. Other closing costs can be negotiated with the seller, meaning you might be able to get the seller to agree to pay for a portion of the costs.

Since VA loans come from private lenders, the lender might have its own requirements when deciding who to approve for the mortgage. A lender can determine what credit score you need, for example. It might also have certain income requirements.

If you’re a current or former member of the U.S. armed forces, a VA loan might offer the best value for you when buying a home. Spouses and widows of former or current service members can also qualify for VA loans.

Are you eligible for a VA loan? Review these requirements to determine whether you qualify for this mortgage loan type and whether it’s right for you. You may qualify for a VA loan if:

- For 90 consecutive days, you served in active service during a time of war.

- For 181 days, you served in active service during a time of peace.

- For 6 years, you have been an active member of the Reserves or National Guard.

- You are the spouse of a service member who died during active service or from a disability related to their service.

5. USDA

The United States Department of Agriculture (USDA) loan program aims to help borrowers who want to buy homes in rural areas and don’t have high incomes. Like FHA and VA loans, USDA loans are guaranteed by the government — in this case, the USDA. Private lenders issue the mortgages.

To qualify for a USDA loan, you need to meet several requirements. Your income can’t be higher than 115% of the median household income in the area. The home you want to buy needs to be in a rural area or a qualifying part of a suburb. Homes in cities or metropolitan areas don’t qualify for USDA loans.

Since one of the USDA mortgage program goals is to provide housing to people with the greatest need, it’s usually a loan program worth considering if you don’t qualify for other types of mortgages and want to live in a rural area. Though the loan program targets people with low to moderate incomes, you still need to prove a steady income, such as at least two years of stable employment, to qualify. You can get a USDA loan with a lower credit score, but you are likely to get a better interest rate and terms with a score of at least 640.

Like a VA loan, you can get a USDA loan with as little as 0% down. To further assist you with the homebuying process, USDA loans allow sellers to contribute to your closing costs.

Are you eligible for a USDA loan? Review these requirements to determine whether you qualify for this mortgage loan type and whether it’s right for you:

- You have a relatively low income in your area. You can check the USDA’s page on income eligibility to determine whether you qualify.

- You’ll be making the home your primary residence, or for a repair loan, you occupy the home.

- You must be able to verify that you’re able and willing to meet the credit obligations.

- You must either be a U.S. citizen or meet the eligibility requirements for a noncitizen.

- You must be purchasing a property in an eligible area.

What Are Fixed-Rate Mortgages?

An additional thing to consider when choosing the right home loan is the type of interest rate the loan has. A variety of factors influence the rate a lender offers you, including your credit score, income and the loan size.

Another factor that comes into play is whether the rate is fixed or adjustable. A fixed-rate mortgage has an interest rate that stays the same throughout the term of the loan. One advantage of a fixed-rate mortgage is that it lets you lock in a low interest rate, provided rates are on the low end when you buy the home.

A potential drawback of a fixed-rate mortgage is that it can confine you to paying a high interest rate, even after rates have dropped. If you’d like to lower your interest at some point due to a drop in interest rates overall or an improvement in your credit score, you’d need to refinance, taking out an entirely new mortgage.

A mortgage with a fixed rate might be right for you if you plan on staying in your home for the long term and rates are low when you apply for the loan and buy the house. With a fixed-rate loan, you have some reassurance that your principal and interest payment will stay the same throughout the loan term, allowing you to create a steady budget and have a good idea of what to expect when it comes to your housing costs.

What Are Adjustable-Rate Mortgages?

The interest rates on an adjustable-rate mortgage (ARM) fluctuate throughout the life of the loan. Often, ARMs offer an introductory rate that stays the same for several years. For example, you might get a 5/1 ARM, which has a five-year introductory period. After the first five years, the rate changes based on what’s going on in the market.

After the introductory period, your rate can increase or decrease. If it increases, your monthly mortgage payment will also increase. If it drops, your monthly payment will also drop. When the introductory period is over, the interest rate will adjust based on a set schedule. In the case of a 5/1 ARM, the rate adjusts every year.

ARMs often have a rate cap, which keeps the interest rate from increasing too much and helps you avoid a monthly payment beyond your reach. The cap can be on each adjustment, as well as a lifetime cap on interest increases. For example, your ARM might have an adjustment cap of 2% and a lifetime cap of 5%.

One feature that makes ARMs appealing is a low interest rate when you take out the mortgage. The rate you’re offered on an ARM will often be lower than the rate on a fixed-rate mortgage. For that reason, it can make sense to choose an ARM over a fixed-rate loan if you’re not planning on staying in the home for the long run. If you anticipate selling before the end of the introductory period, you can enjoy several years of reduced interest.

Another potential benefit of an ARM is that your rate could fall even more in the future. If you feel that interest rates will keep falling, getting an ARM can help you take advantage of lower rates without the need to refinance your mortgage.

It’s important to note that adjustable rates aren’t offered on all types of mortgages. You can choose a conventional mortgage, FHA loan or VA loan with an adjustable rate.

Other Mortgage Options

In addition to conventional mortgages and government-backed loans, there are several other home loan options for borrowers who might be in unique situations. If you already own a home, it’s possible to get another mortgage on the property, for example. You can also get a loan to build your home.

1. Construction Loan

This type of mortgage loan involves buying land on which to build a house. These loans typically come with much shorter terms than other loans, at a maximum term of one year. Rather than the borrower receiving the loan all at once, the lender will pay out the money as the work on the home construction progresses. Rates are also higher for this mortgage loan type than for others.

There are two types of construction loans:

- Construction-to-permanent: A construction-to-permanent loan is essentially a two-in-one mortgage loan. This is also known as a combination loan, which is a loan for two separate mortgages given to a borrower from a single lender. The construction loan is for the building of the home, and once the construction is completed, the loan is then converted to a permanent mortgage with a 15-year or 30-year term. During the construction phase, the borrower will pay only the interest of the loan. This is known as an interest-only mortgage. During the permanent mortgage, the borrower will pay both principal and interest at a fixed or variable rate. This is when payments increase significantly.

- Construction-only: A construction-only loan is taken out only for the construction of the house, and the borrower takes out another mortgage loan when they move in. This may be a great option for those who already have a home, but are planning to sell it after moving into the home they’re building. However, borrowers will also pay more in fees with two separate loans and risk running the chance of not being able to move into their new home if their financial situation worsens and they can no longer qualify for that second mortgage.

2. Second Mortgage

Second mortgages are taken out after a borrower’s first mortgage and are generally used for financing home improvements, consolidating debt or for covering enough of the first mortgage to avoid the requirement of paying the mortgage insurance. Second mortgages generally have terms that last only up to 20 years and can be as short as one year.

Programs to Help You Get a Mortgage

If you’re buying your first home, several programs exist that help simplify the process or make homeownership more affordable. First-time homebuyers programs are usually available on a state or local level. Some offer grants to help you afford a down payment, while others might help with closing costs or other fees.

Another thing to consider if you’re about to buy your first home is working with a financial counselor. A counselor can help you make a plan for saving for a down payment or help you work on improving your credit so you’ll get the best mortgage terms possible, whether you qualify for a conventional loan or a government-sponsored one.

One thing worth noting is that specific mortgage types aren’t limited to first-time buyers. You might qualify for a USDA or VA loan if you’re buying your second or third home, provided you plan on using the home as your primary residence. The same is true of FHA loans. While the loan programs expect you to live in the home as a condition of qualifying for the mortgage, they don’t require you to be a first-timer.

Another option is the Good Neighbor Next Door Program. It is sponsored by the U.S. Department of Housing and Urban Development and assists law enforcement, firefighters, teachers and emergency medical technicians with housing. The program offers a 50% discount on a home’s listed price in locations deemed “revitalization areas.” To be eligible, you must commit to living in the home for at least 36 months.

Your mortgage lender is also happy to discuss the different types of home loans available. They can work with you to help you choose a mortgage that works best with your current financial situation and that will help you achieve your goals in the future.

Apply for a Mortgage With Assurance Financial Today

Buying a home starts with getting the right mortgage. Assurance Financial has home loan options for every type of buyer, from first-time homebuyers to more experienced buyers. If you’re a veteran, we can help you get a VA loan. If you’re likely to buy in a rural area, we can help you with a USDA loan. Start your application today, or reach out to find a loan officer near you.

Linked Sources:

- https://singlefamily.fanniemae.com/originating-underwriting/loan-limits

- https://www.consumerfinance.gov/ask-cfpb/when-can-i-remove-private-mortgage-insurance-pmi-from-my-loan-en-202/

- https://assurancemortgage.com/jumbo-loans/

- https://www.hud.gov/buying/loans

- https://assurancemortgage.com/fha-loans/

- https://assurancemortgage.com/va-loans/

- https://www.va.gov/housing-assistance/home-loans/funding-fee-and-closing-costs/

- https://www.rd.usda.gov/programs-services/single-family-housing-guaranteed-loan-program

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/find-a-loan-officer/

- https://www.hud.gov/program_offices/housing/sfh/reo/goodn/gnndabot

- https://assurancemortgage.com/usda-loans/

- https://eligibility.sc.egov.usda.gov/eligibility/incomeEligibilityAction.do?pageAction=state

*Not a commitment to lend or extend credit. Restrictions may apply. Loan limits, information and/or data subject change without notice. All loans subject to credit approval. Not all loans or products are available in all states. Assurance Financial is committed to compliance with Section 8 of RESPA and does not offer free marketing services in exchange for referrals or the expectation of referrals.

Ready to take the first steps toward buying a home? If you’re going to finance your home purchase, one of the first things to do is figure out how to get a mortgage. You might have heard that getting a mortgage is a long and complicated process, with plenty of twists and turns along the way.

While it’s true there are several steps involved in applying and getting approved for a home loan, with a bit of preparation and attention, getting a mortgage doesn’t have to be complicated. Here’s what you need to know as you prepare to pursue your dream of becoming a homeowner.

10 Steps to Get a Mortgage Loan

What does it take to qualify for a mortgage? You can divide the home loan process into three major parts — the preparation period, the application period and the approval period. Depending on your timeline and preference, you can spend months or years in the preparation period before moving onto the other two phases. If you’re ready to learn more about how to get a loan for a house, take a look at the steps involved:

1. Save up for a Down Payment

The home loan process always starts with saving. The exact amount you need to save up for a down payment depends on the type of loan you choose, the market conditions and your financial situation. You might have heard a 20% down payment is ideal when you’re buying a home. That might be true, as putting down 20% allows you to avoid paying private mortgage insurance (PMI) premiums and can mean you get a better interest rate on your loan. But it can take many years to save up 20% of a home’s price, especially if you’re buying in a market with high housing prices.

Fortunately, there are other options available. You might qualify for a conventional mortgage with a 5% or 10% down payment. You will have to pay PMI premiums when you make your monthly mortgage payment, but those premiums will go away once you’ve paid at least 20% of the house’s value. If you meet certain requirements, you might qualify for a conventional loan with just a 3% down payment.

Certain mortgage programs, particularly government-backed loan programs, let you get a home loan with much less than 20% down, too. USDA Rural Development and VA loans accept 0% down. There are other factors to consider when deciding which loan to apply for as well.

Once you’re ready to start saving, there are a few ways to go about doing it. First, set a goal amount. If homes in your area cost an average of $250,000, and you want to save up 5%, for a down payment, you’ll need to save $12,500. Next, set a target date. Let’s say you want to have your down payment within 24 months. Once you know how much to save and how long you have to save, you can figure out how much to put aside each month. In this example, you’ll need to save around $520 monthly.

You might have to consider how you’ll come up with that $520 each month. One way to do that is to create a budget and to plan your expenses with care, so you have enough to save for your goal. To make the process of saving easy, set up an automatic transfer from your checking account to a designated savings account. That way, you’ll save without having to think about it.

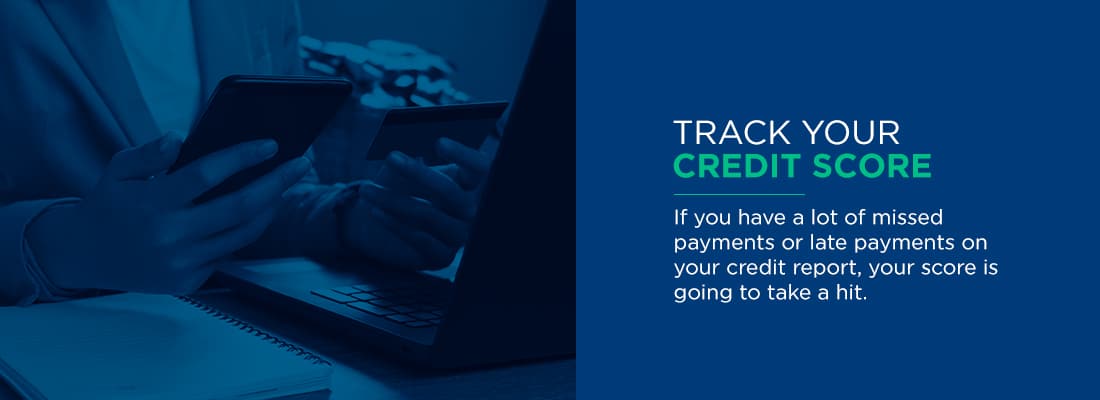

2. Track Your Credit Score

Having a good credit score makes the homebuying process a breeze! Before you start the buying process, get a copy of your credit report. You can request a free report from annualcreditreport.com. Your bank might also let you review your report for free. Some also give you access to your credit scores, which can give you a good idea of where you fall on the credit score range. Once you’ve examined your credit profile, you can begin taking steps to improve your credit score if need be.

What should you look for when reviewing your credit history and score? First, it helps to understand what a credit score is and what makes one “excellent” versus “good” or “poor.” Scores range from 300 to 850. If your score is above 800, way to go! You have what most lenders consider an excellent score. Scores between 740 and 799 are usually “very good”, while scores between 670 and 739 are “good.” It can be difficult, but not impossible, to get a mortgage with a score below 670.

One factor that plays a significant role in determining your credit score is your payment history. If you have a lot of missed payments or late payments on your credit report, your score is going to take a hit. How much you owe also plays a big part in determining your score, so if you have several credit cards with high balances or owe a lot on a car loan or in student loans, your score might be lower than you want.

Fortunately, you can take action to improve your score. The first thing to do is get current on paying your accounts if you’ve fallen behind. If you aren’t behind, commit to staying caught up with your payments. The next thing to do is to focus on reducing how much you owe. Reducing your overall debt burden can also help you later on in the mortgage application process, as a lender will look at how much you currently owe when determining how much you can borrow for your home.

3. Explore Your Loan Options

Despite their sound advice, the loan program that worked best for your parents may not always be ideal for you. Take some time to research which loan program will fit your current financial situation. Everyone has a set of unique financial needs. With a little digging and help from our reliable loan advisors, you’ll be able to find the loan that best suits your needs.

Some mortgage options include:

- Conventional mortgages: A conventional mortgage is your standard home loan. It’s not guaranteed by the U.S. government, so a lender assumes the full risk of extending the loan to you. You might need to meet stricter requirements to get a conventional mortgage compared to other home loan options, such as having a higher income, above average credit, and a sizable down payment. Often, a combination of some factors, such as a steady employment history with a high income and an excellent credit score, can make up for missing other factors, such as only having a 5% down payment.

- Federal Housing Administration (FHA) loans: FHA loans are guaranteed by the U.S. Department of Housing and Urban Development (HUD), a government If a borrower stops paying their FHA loan, HUD will make payments to the lender. The guarantee from HUD means lenders are willing to approve borrowers with smaller down payments — as little as 3.5% — and lower credit scores for mortgages. In exchange, the borrower needs to pay PMI and an upfront mortgage insurance premium.

- VA loans: VA loans are for active-duty or veteran service members. They’re backed by the Department of Veterans Affairs and allow people to get a mortgage without a down payment.

- USDA loans: The USDA loan program is guaranteed by the U.S. Department of Agriculture. Its purpose is to encourage people to buy homes in rural or certain suburban areas. The loan program allows buyers to put zero down.

- Jumbo loans: A jumbo loan is also called a non-conforming loan. It’s a conventional mortgage that’s above the lending limits set by FreddieMac and FannieMae. If you’re looking to buy a large, expensive home, you might need a jumbo loan to do it. Often, you’ll need to have excellent credit and a hefty down payment to qualify for a jumbo loan.

[download_section]

4. Get Organized and Prepared

Congratulations, by this point, you’re nearing the end of the preparation period of the mortgage process. You’re now getting ready to actually apply for the loan itself. When you submit your mortgage application, you’ll need to hand over a few important financial documents to your lender. The exact documents you’ll need might vary slightly based on the lender you work with and your particular situation. The more prepared and organized you are, the better. Some of the documents you’ll want to have ready include:

- Tax returns: Have at least the past two years of tax returns handy before you meet with a lender to apply for a mortgage. Your lender might also ask you to complete and sign Form 4506-T, so it can pull your returns from the IRS.

- Pay stubs or other proof of income:Your lender will also want to verify your current income. If you are employed, you can present your most recent paystub or Form W-2. If you’re a freelancer or work for yourself, be prepared to show proof of income in other ways, such as Forms 1099, your tax returns or profit and loss statements.

- Bank statements:Your lender will want proof that you have enough saved up to make the down payment and cover closing costs. They might also want to see evidence of additional assets. Have all of your most recent bank statements, plus statements from any investment accounts you have, ready. Also gather up documents concerning other debts you have, such as credit card or student loan statements.

- Credit report: Your lender is going to pull your credit and won’t need you to show them the report. It’s a good idea to have it on hand so you can read it over and discuss any areas of concern to the lender. If there are mistakes on the report, contact the credit reporting bureaus before you meet with the mortgage lender to have the incorrect information removed from your report.

- Rental history: If you’re a renter, your lender might ask to see proof that you’ve paid your rent for the past year.

- Identification:You’ll need photo identification, such as your passport or driver’s license, when you apply for a mortgage.

5. Fill out a Mortgage Application

You’re prepped and ready, it’s time to start the process of applying for a mortgage. Gather up your financial documents and apply online.

The lender will review your documents to see how your income compares to your debts and to see how your credit stacks up. With this information, they’ll provide a maximum loan amount and let you know the interest rate you can expect to pay. At this point, if all goes well, you’re pre-qualified for a mortgage and can start the process of looking at homes.

6. Think About What Affordable Means to You

As you move into the application portion of the mortgage process, it can be useful to think about what you really want to spend on a home. Lenders consider your debt-to-income (DTI) ratio before pre-qualification. DTI compares your monthly income to the amount you owe each month. Your front-end DTI is how your projected total housing payment compares to your monthly income. The back-end DTI includes all your monthly debts. The ideal front-end DTI to back-end DTI ratio is about 25%/41%. Some conventional loans will allow a back-end of 50%, and FHA will even allow 56.99%.

While the “ideal” back-end DTI is about 41% and your lender might allow you to have a DTI of 50% or more, think carefully about whether that’s something you’re comfortable with. You might prefer to buy a less expensive house to keep your total debts low. If you have many other debts, you might want to buy less house so you can focus on paying off the more expensive debts. On the flip side, if you are going into the mortgage process without any other debts or financial obligations, you might feel comfortable purchasing a home at the upper end of your price range.

7. Start Looking at Houses

Once you’ve set a budget and know your price range, it’s time to get out there and start looking at homes. It takes time to find the right home. At the beginning of the house shopping process, make a list of the things you need to have in your future home. Some features to consider include:

- Number of bedrooms: Think about your family size now and in the future. If you’re single or have a partner, do you want to have kids someday? If so, do you want to continue to live in your current home? Another thing to think about when deciding how many bedrooms to have is whether you have guests frequently and whether you need a place to work from home.

- Number of bathrooms: A one-bathroom home might be fine for a couple or a single person, but it can be challenging for larger households. You might also want a half bath on the first floor for people to use when they visit your home.

- Kitchen size and layout: You might not need a big kitchen, but you probably want one that’s well laid out so it’s not difficult to get what you need when cooking. Another thing to consider is an open or closed layout. Some people like to see the rest of the living space from the kitchen, while others prefer a kitchen that’s separate from the rest of the house.

- Outdoor space: Do you want a yard? If yes, how big should the yard be? You might be happy with a concrete patio, or you might want a large backyard with a lush, green lawn.

- Location: Carefully consider where you want to live. How long do you want your commute to be, how important are quality schools to you, and how safe is the neighborhood overall?

Once you have a basic idea of what you want, book an appointment with a real estate agent and start touring homes in your desired area. Once you found one that works for you, put in an offer.

8. Get Ready for Loan Processing

After the seller has accepted your offer and the home has passed inspection, it’s time for the meat of the mortgage application process to start. At this stage, the lender is going to run all your documents, verify all your information and let you know whether you’re approved or not.

Your loan application gets sent over to the loan processors. Once it’s in their hands, they begin double-checking everything on your application. The processor will prepare and organize the file before it’s sent over to the bank or mortgage lender for approval. They will contact your employer to verify your job and the salary on your application. If there are any questions regarding the information on your application, they will have your loan officer contact you for details. Any mistakes you’ve made will arise during this stage, giving you a chance to make corrections before the file is handed off to the underwriter.

Keep your phone handy during this stage, as the processor is likely going to call you to verify information or correct details. They might call or e-mail you to ask you to send them even more paperwork, particularly if you’re self-employed.

9. Wait for the Underwriter’s Decision

Once your loan application passes the processing stage, it heads to the underwriter. The underwriter is the person who decides whether or not to issue the final approval on your mortgage application. To approve your application, they’ll pull your credit again and will review your job history and income.

Before the loan moves to the underwriting phase, the mortgage lender will likely require a home appraisal. During the appraisal, a third party will evaluate the home to determine its worth. They’ll use the prices of similar, recent sales in the area, the condition of your home and its size when determining its value. Ideally, the appraiser will decide that your home is worth as much as you’re paying for it, if not more. If the appraiser under-values your home, meaning they think it is worth less than the mortgage, your lender could deny your loan.

When your loan is in the underwriting phase, it’s important that you leave your credit and employment situation alone. Now’s not the time to change jobs or quit your job. It’s also not the time to start buying furniture for you new place or apply for credit cards or other loans.

10. Head to Closing

If all goes well with underwriting, the lender will approve your application and clear you for closing. You’re so close to being a homeowner at this stage!

On the day of closing, you’ll need to bring your down payment and any other fees and closing costs. Usually, you’ll need the money in the form of a cashier’s check, or you’ll need to arrange for a wire transfer of the funds. Your lender will let you know how much you need to bring with you, usually a few days in advance, so you have time to get the cashier’s check or set up the wire transfer.

At closing, you’ll sign a lot of paperwork, will likely pose for a few photos with your real estate agent and lender, and most importantly, will get the keys to your new home.

Start the Mortgage Application Process With Assurance Financial Today

Are you ready to start the process of getting a home loan? Assurance Financial can help. You can find a loan officer near you and set up an in-person visit to get the process started today.

Linked Sources:

- https://assurancemortgage.com/loan_process/

- https://assurancemortgage.com/ways-to-save-for-a-down-payment/

- https://www.annualcreditreport.com/index.action

- https://assurancemortgage.com/conventional-loans/

- https://assurancemortgage.com/fha-loans/

- https://assurancemortgage.com/va-loans/

- https://assurancemortgage.com/usda-loans/

- https://assurancemortgage.com/why-get-pre-qualified-before-looking-for-home/

- https://assurancemortgage.com/loan-options-self-employed-buyers/

- https://assurancemortgage.com/what-to-expect-during-a-home-inspection/

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/find-a-loan-officer/

Buying a home is a major commitment, both on the part of the buyer and the lender. As a buyer, you agree to take care of your new home and repay your mortgage based on the terms of the loan. The lender is taking a chance by providing you a significant sum of money upfront, with the expectation that you’ll pay it back with interest.

Lenders use several factors when deciding whether or not to lend money to an individual or group of people. One of those factors is the borrower’s credit history and credit score. Learn more about the importance of your credit history when getting a mortgage and what you can do to make the most of yours.

Table of Contents

- What is a Credit History?

- How Important is a Credit Score?

- How Does Your Credit Affect Interest Rates?

- What Happens to Your Credit After Approval?

- Other Factors to Consider When Buying a Home

- How to Improve Your Credit Score

- Apply for Home Loan Insurance Today

What Is a Credit History?

Your credit history is a snapshot of how you’ve used money and loans throughout your life. Generally, your credit history includes the following:

- The number of loans or credit accounts you have:Your credit history includes accounts that are currently open as well as closed accounts. Examples of closed accounts include a loan you’ve paid off or a credit card you canceled.

- The amount you owe on each account:Your credit history also reflects how much you owe on each account. For example, you might have a student loan with a principal balance of $15,000, and you might owe $2,500 on a credit card. If the account has a limit, such as a credit card with a limit of $7,000, that will also be part of your credit history.

- The types of accounts you have: Loans typically come in two forms — revolving and installment. Installment loans include personal, auto and student loans. Credit cards are common examples of revolving loans.

- Your payment history: Whether you pay on time, have made late payments or have missed payments will all be part of your credit history. If you have any loans that went into collection or that were charged off, those will appear on your credit history, too.

The information that makes up your credit history is contained in a credit report. There are three bureaus that put together credit reports. What gets reported by one bureau might not get reported by another, which can affect the accuracy of your credit history. In addition to details about your credit and loan accounts, your credit report will contain identifying information, such as your current address and a list of your previous addresses, your birthdate and your Social Security number.

How Do Lenders Use Your Credit History?

Lenders look at your credit history to get a sense of your relationship to loans and money in the past. If you have a very short credit history or don’t have one at all, a lender doesn’t have much to work with. They have no way of knowing whether you’re likely to pay your loan as agreed or if there’s a high risk that you’ll default on it.

If you have a history of on-time payments and a variety of loan accounts, a lender might feel more confident in letting you borrow money. Lenders also look at how much you owe when making a decision about you. If you have a lot of outstanding debt, they might be hesitant to offer you more credit. Along with approving you for a mortgage, a lender might also offer you a lower interest rate or let you borrow more money if you have a strong payment history and don’t currently owe a lot of money.

How Important Is a Credit Score?

Your credit history plays a significant role in determining your credit score, a three-digit number ranging from 300 to 850. If you’re interested in getting a mortgage, your credit score is important, as it lets a lender see at a glance how you’ve handled money and loans in the past. The higher your score, usually the better the terms you’ll get on a mortgage.

Certain parts of your credit history influence your score more than others. Usually, the following five factors determine your total score:

- Payment history: Your payment history has the biggest impact on your score, accounting for 35% of the total score. That makes sense, as a lender may hesitate to let someone who regularly misses payments or pays late borrow money.

- Amount you owe: How much you owe on existing loans also has a considerable impact on your score, accounting for 30% of the total. A lender is likely to be nervous about lending money to someone who already has a significant amount of debt.

- Length of history: The longer your credit history, the better, although the length of your history only accounts for 15% of your total score. If you’re interested in getting a mortgage one day, it may be a good idea to open up your first credit card or get another type of loan when you’re relatively young.

- Types of accounts: The type of accounts you have play a smaller part in determining your score. Credit mix accounts for 10% of your total score. While you don’t have to have one of every possible type of loan, it’s useful to have a variety of accounts in your history, such as a credit card and a personal loan, or a credit card and auto loan.

- New credit: New credit accounts for 10% of your score. Multiple new accounts on a credit report can be a red flag to lenders. They might wonder why someone opened several credit cards or took out multiple loans at once.

Your credit score has a part in determining how much interest you pay on a loan and can also play a role in the type of loans you’re eligible for.

What Is a Good Credit Score for a Home Loan?

If you’re going to pay for your new home in cash, you technically don’t need to worry about your credit history or score, as you aren’t borrowing money. But if you plan to get a mortgage to pay for part of your new home, your credit score is going to play a bigger role. The credit score you need to qualify for a home loan depends in large part on the loan you’re applying for and the amount you hope to borrow.

Conventional mortgages typically require higher credit scores than government-backed mortgages. A lender assumes more risk when issuing a conventional home loan, so it’s important for them to only lend money to people with strong credit scores. The minimum credit score for a conventional mortgage is around 620. But a borrower is going to get better rates and the best terms possible if their score falls in the “Excellent” range, meaning it’s above 740.

A borrower can qualify for certain government-backed mortgages, such as the FHA loan program or VA loans, with a much lower score. The FHA loan program may also accept borrowers with scores as low as 500, but those borrowers need to make a down payment of at least 10%.

How Does Your Credit Affect Your Interest Rates?

The higher your credit score, the lower your interest rate may be on a mortgage or any other type of loan. A lender will feel more confident issuing a mortgage to someone with a score of 800, for example, than they would approving a mortgage for someone with a score of 690. To reflect that confidence, the lender will charge less for the loan.

At first glance, the difference between the interest rate someone with a score of 800 is offered and the rate someone with a score of 690 is offered might not seem like much. For example, someone with a score of 800 might get a rate of 4%, while a person with a 690 score might be offered a rate of 4.5%. But over the 15-year or 30-year term of a mortgage, that half of a percentage point difference adds up to thousands of dollars.

Depending on the type of mortgage you apply for, you can qualify for a better rate with a lower score. For example, if you apply for an FHA loan with a score of 580, you’ll get a higher rate than someone who applies with a score of 700. But if the person with a score of 700 applies for a conventional mortgage, they are likely to get a higher rate on the conventional loan than on an FHA loan.

What Happens to Your Credit After You’re Approved for a Loan?

Your mortgage will appear on your credit reports and will affect your credit score. Overall, adding a mortgage to your credit history is a good thing. But there are a few things to note. One is that initially, your score might drop after you get approved for a mortgage and close on your home. When you get a mortgage, you add a significant amount to your total debts owed, which accounts for nearly one-third of your credit score. You also add new credit to your report, which accounts for 10% of your score.

Don’t panic if you see your score drop after taking out a mortgage. If you had a relatively high score to begin with, the drop is likely only to be a few points. You’re also going to improve your score relatively quickly. As you start paying off your mortgage, the lender that owns it will report your payments to the credit agencies. After a few months of on-time, consistent payments, you’ll have bolstered your payment history on your report.

Another reason not to panic about an initial drop in your credit score is that your mortgage will boost your score over time, provided you continue to pay regularly. Mortgages are examples of installment loans. You borrow X amount and as you pay it down, the amount you owe decreases. That reduces the total amount owed that shows on your credit reports, ultimately improving your score.

A mortgage also gives you a more diverse credit portfolio. If you previously had mostly credit cards, adding a mortgage increases the variety of your credit mix, which can boost your score.

Other Factors to Consider When Buying a Home

While your credit score is important, it’s not the only factor that determines the interest rate you’re offered or whether a lender approves your application or not. A few other things that influence your mortgage include:

- Your down payment: How much you can afford to put down influences the interest rate you’re offered as well as the type of mortgage you qualify for. If you plan on taking out a conventional loan, your down payment can range from 3% to 20%, but only borrowers who meet certain requirements can qualify for a 3% down payment. Usually, the more you put down, the lower your interest rate.

- Market conditions: The overall market also influences the rate you get offered on a home loan. When rates are high, your interest rate will be higher, even if you have the best credit possible. When rates are low, you can qualify for a lower rate than you would otherwise. How competitive the market is also influences your mortgage options. It can be more challenging to qualify for a mortgage with a low down payment or lower credit score when there’s a lot of demand from buyers and few homes available for sale.

- Mortgage options: Depending on the type of mortgage you apply for, you might not need to have a credit score in the “excellent” or “very good” category. Certain government-backed loan programs are available to borrowers with less-than-stellar credit. If you have a lower score and don’t have much for a down payment, an FHA loan, for example, might be your best option. On the flip side, if you plan on buying a very expensive home and need to take out a jumbo mortgage to do so, you’ll need to have a higher-than-average credit score and a sizable down payment.

- The price of the home: How much the home costs compared to how much you want to borrow also influences whether or not you get approved for a mortgage. The pricier the home, usually the bigger the risk to the lender. If you’re buying an inexpensive property, you’re likely to get a better interest rate, especially if you’re able to put down a large payment upfront.

- Your income: A lender is going to ask you how much you earn and ask you to verify your income before they agree to lend money to you. They want to ensure you can pay back what you’ve borrowed. The higher your income and how it compares to your total debt influences how much a lender will let you borrow and the interest rate they charge.

- Type of interest: The type of interest rate your mortgage has is another thing to consider. Mortgages with adjustable rates have lower rates at first, but those rates can increase when they adjust. A fixed-rate mortgage might charge a slightly higher rate than an adjustable-rate loan, but you have reassurance the rate will remain the same for the life of the home loan.

- Length of the mortgage:How long you have to repay the mortgage also influences your rate. Mortgages with longer terms, such as 30 years, usually charge higher rates than loans with shorter terms, such as 15 years.

Your lender is likely to look at the big picture, taking your credit score, income, down payment and other factors into consideration before making a lending decision.

[download_section]

How to Help Improve Your Credit Score

If you don’t have a credit history, have limited credit or have a poor credit history, you’ll want to focus on improving your credit before you apply for a mortgage, even if you plan on applying for a government-backed loan. Fortunately, there are a few ways you can boost your credit.

If you don’t have a credit history at all, the first thing to do is open your first account. You have a few options for doing that:

- Get a secured credit card:Secured credit cards help people with limited credit histories or with poor credit boost their scores. When you apply for a secured credit card, you put down a deposit, such as $500. The deposit acts as collateral on the card, reducing the risk to the lender.

- Apply for a credit builder loan: Another option is to apply for a credit-builder loan from a credit union or bank. Credit builder loans are slightly different from other types of loans. In effect, it works backward. You don’t get the borrowed money upfront. Instead, you pay the lender each month, and it holds your payments in an account. Once you’ve paid off the full balance of the loan, you can receive the funds and use them as needed.

- Apply for a store credit card: If a credit-builder loan or secured credit card doesn’t appeal to you, another way to establish credit is to apply for a store credit card. Be cautious with this approach, though. You don’t want to charge so much on the card that you have trouble paying off the balance and end up with missed or late payments.

- Ask someone to co-sign with you:Finding a co-signer is another way to qualify for a loan with a limited credit history. Your co-signer is a co-borrower, meaning they are responsible for paying the loan if you fall behind. Make sure the person who agrees to co-sign with you understands the risks they are taking on before going forward.

If you do have a credit history but your score isn’t what you want it to be, there are things you can do to improve your score. It might take a while to get your credit where you want it to be, so it can be useful to check out your credit report months or years before you plan on buying a home:

- Pay on time:Remember that payment history is the big one when it comes to your overall score. If you’ve fallen behind on certain accounts, do whatever you can to make them current. Commit to paying every other account on or before the due date.

- Avoid new credit accounts: Try to avoid opening lots of new credit accounts, as doing so will cause your score to drop. It’s especially important to avoid new accounts while you wait for final approval on your mortgage, as opening a new credit card or taking out a different loan during that time can disrupt the approval process.

- Keep your debt balances low: How much you owe overall plays a major part in the calculation of your credit score. If you currently have a lot of credit card debt or student loans, try focusing on paying them off or significantly reducing the balance before you apply for a mortgage.

Apply for a Home Loan With Assurance Financial Today

Is your credit score where you want it to be? Even if it’s not, our helpful loan officers can help you decide the what’s best for your home buying goals. You can start the application process online with Assurance Financial. A loan officer will then get in touch to finalize your application.

Linked Sources:

- https://www.myfico.com/credit-education/whats-in-your-credit-score

- https://assurancemortgage.com/conventional-loans/

- https://assurancemortgage.com/va-loans/

- https://assurancemortgage.com/fha-loans/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/apply/

When you own your home, you can feel a sense of stability and security. You have a roof over your head and a place to raise a family if you choose to do so. You also get full control over how you decorate the home and any changes you make to it.

There’s another benefit to homeownership, and that’s the chance to build equity in your home. Many homeowners look at their property as an investment. If you live in the house for long enough and make enough payments on the mortgage, at some point, your property will be worth more than you paid for it. Another way that a home acts as an investment is through equity. The more equity you have in your home, the more homeowner advantages you can enjoy. Learn more about the value of building home equity and what you can do to maximize it.

Table of Contents

- What is Equity?

- Why is Building Equity Important?

- How to Build Equity in Your Home

- Work With Assurance Financial

What Is Equity?

Home equity is simply the difference between your home’s value and the amount you owe on the mortgage. If you own your home free and clear, your equity is the same as the property’s value. Here’s a quick example of how equity works. Suppose your home’s market value is $300,000. You have a mortgage on the home and still have $220,000 left to pay on it. In this example, the equity in your home is $80,000, or $300,000 minus $220,000.

For many homeowners, equity increases the longer they own their homes. As you make payments on your mortgage, the principal on the loan decreases. Meanwhile, the share of your equity grows.

Although equity usually goes up, it can drop. For example, perhaps you bought a home worth $300,000 and took out a $250,000 mortgage to do so. At the time of closing, your equity in the home was $50,000. Then, a recession happened and the value of homes in your area dropped. Your home now has a market value of $250,000 and you have $225,000 left on your mortgage. Even though you’ve paid off some of your loan principal, since the value of the property has fallen, you now only have $25,000 in home equity.

Why Is Building Equity in a Home Important?

Building equity in your home helps you establish financial freedom and flexibility. The greater your home equity, the better you may be able to weather financial hardships that come your way. Once you establish some equity in your home, you can use the cash value of the equity when necessary. There are two ways to tap into your home’s equity.

One option is to apply for a home equity loan. Just as your mortgage uses your home as collateral, so does a home equity loan. Usually, you can borrow up to 85% of the full amount of equity you have in your home. If your equity is $50,000, your home equity loan can be up to $42,500.

You can use the funds from the loan for pretty much any purpose. Some people use the loan to cover the cost of a home improvement project, while others use the loan to help pay for their children’s college education. Typically, you repay the loan in installments, making monthly payments until you’ve repaid it in full, plus interest. The amount of interest you pay depends on the market conditions, your credit score and how much you borrow.

The other way to tap into your home’s equity is with a home equity line of credit (HELOC). A HELOC is similar to a credit card. You have a credit limit and can borrow up to that limit. Once you repay the amount you’ve borrowed, you can borrow more, provided you’re still in the draw period.

The more equity you have in your home, the bigger your financial cushion if you need to borrow against it. It’s important not to go overboard when borrowing against your home’s equity. If you have difficulty repaying your home equity loan or HELOC, you do risk losing your home, just as you would if you can’t make payments on your original mortgage.