Category: Purchasing a Home

There are many factors to consider when selling a home, and you may be wondering what happens to your mortgage when you move. After all, the 2018 American Community Survey found that the median length of time homeowners stayed in their homes was 13 years, a shorter length of time than most mortgage terms.

Recent data from the Pew Research Center found that at the end of the fourth quarter of 2020, the rate of American households that owned their own home increased to around 65.8%. With so much homeownership throughout the country, mortgages are an imperative topic. If you’re one of the many Americans that own a home with a mortgage, you should know your options when it comes time to sell.

Here’s a comprehensive guide to what happens if you sell your house and still owe money.

Topics Covered

- Should I Pay Off My Mortgage Before Selling My House?

- What Happens to My Mortgage When I Sell My House?

- Selling Your Current Home Before Buying Another

- Buying a New Home Before Selling Your Current One

- How to Get a Mortgage on a New Home

Should I Pay Off My Mortgage Before Selling My House?

If you plan to move and already have a mortgage on your current home, your first thought may be to pay off your mortgage early, so you’re free of your monthly payments. Though it isn’t necessary to pay off a mortgage before you sell your house, it may be a viable option depending on your situation. This option requires some planning, but you can make it happen.

There are several benefits to paying off a mortgage early:

- Saves interest fees: Over the life of a 15- or 30-year loan, interest can stack up and sometimes double what homeowners pay, despite their original loan amount. When homeowners decide to pay their loan off early, they get to eliminate some of the interest they would pay in the future and save themselves years of payments.

- Frees up monthly funds: This process also opens up more funds in your monthly budget, giving you greater flexibility with that cash later in life. When your mortgage payments are gone, you could contribute that money into your emergency fund, retirement account or other investments, or save up for that vacation you always planned.

Many variables can factor into your decision, so it’s essential to crunch the numbers and examine your financial situation individually.

Here are two of the most common strategies to pay off your mortgage early:

1. Higher or More Frequent Payments

One of the simplest ways to decrease the life of your mortgage is to make payments more often. Although bi-monthly payments will cost the same amount as your previous mortgage payments, they’ll use the weeks of the year to give you an additional annual payment. When multiplied over several years, one extra yearly deposit can lead to a considerable amount of savings.

Consider increasing your monthly payments, consistently paying more on your mortgage than the minimum requirement. Manually adding extra is a flexible option that allows you to contribute any amount you choose. Add $100 more, $50 more or any variable amount you decide to contribute over your loan’s life.

2. Refinancing

Some homeowners choose to fix their loan for 30 or 40 years but may later decide to pay it off sooner. By refinancing your mortgage, you can refigure your loan for a shorter timeframe, increasing your monthly payments and decreasing your interest.

However, refinancing may not be the best idea when you’re looking to move. Some homeowners may want to refinance to put the money they would have spent on interest payments toward their savings for a down payment. If your savings don’t add up before your planned move, a refinance could cost you more money than it’s worth. Use Assurance Financial’s refinance calculator to determine whether a refinance is right for you.

Ultimately, choosing to pay off a mortgage before you move may not be your best option. Depending on your timeframe and your other investment opportunities, you may decide to keep that cash and set it aside for a new down payment. Whatever you choose, weigh your choices and consider which is in your best interest.

What Happens to My Mortgage When I Sell My House?

According to Freddie Mac, almost 90% of American homeowners finance their homes with a 30-year mortgage. Still, many homeowners will move to another house before that timeframe ends. This situation is common, so you can follow standard practices for selling a home with a mortgage attached.

If you’re selling your house before the mortgage term is up, you can take one of two avenues:

1. Traditional Home Sale

In a traditional home sale, the seller lists the house for a price that will cover the following costs:

- The mortgage’s remaining costs

- Existing home equity loans or home equity lines of credit (HELOCs), if applicable

- Mortgage prepayment penalties, if applicable

- Closing costs, including agent commissions, taxes and other fees

After taking care of the above expenses, whatever amount is left over is the seller’s profit. To pay for the rest of the mortgage, the closing manager sets up an escrow account into which the buyer will deposit their payment. Then, the title company will distribute the final mortgage payment to the lender. As a result, the seller no longer has that mortgage.

If you’re unable to sell your home for enough money to cover the associated costs, you’ll have to pay them out of pocket, wait until you can sell the house for more or request a short sale. In an ideal situation, the seller can cover the remaining balance of their loan, pay for closing costs and put a down payment on their next home from the sale price. This scenario requires good home equity — which is the homeowner’s financial stake in their house — to warrant a high enough price.

A home’s equity is comprised of the following elements:

- The original down payment

- The home’s gains in market value

- Mortgage principal payments

- The cost of renovations or improvements the seller made to the house

Getting a quote for your mortgage payoff when selling your house helps determine the price you need to sell your home. A mortgage payoff shows you the total amount you need to pay to settle your mortgage debt, including your interest and other unpaid fees. If you tell your lender about your plan to sell your home, they’ll provide you with a mortgage payoff quote.

2. Short Sale

When your house has too little equity to pay for your mortgage, it has negative equity. Without enough cash to cover your remaining mortgage balance, plus the closing costs, a short sale may be your only option. In a short sale, the buyer purchases the home for less than the seller’s debt against the property. These sales require approval from your lender because they leave the mortgage company at a financial loss.

The approval process for a short sale usually takes longer than for a traditional sale since the seller has to convince the lender they can’t pay off their loan. To convince the lender, the seller must either show that the housing market dropped, so their home is worth less than their debt, or prove they’re incapable of keeping up with their payments. Because the lender is trying to recoup as much of their losses as they can, the process may take a while.

Another negative aspect of short sales is they remove the seller’s negotiating power. This entire process depends on the lender’s approval, including the sale of the house. Even when the buyer and seller agree on a price, the lender may end up declining the buyer’s offer to hold out for a higher one. Ultimately, short sales negatively affect a seller’s credit score and make it more challenging to get a home in the future.

Selling Your Current Home Before Buying Another

If you’ve examined all of your options and want to go ahead with the sale of your home, you may want to know whether you should sell it before or after buying a new one. This answer could be as simple as establishing how much you have in savings to spend on a down payment. Most sellers find that selling their current home opens up their home’s equity so they can use that profit for their next home.

Pros of Selling First

By selling first, you can enjoy the following benefits:

- More negotiating power: When you buy a new house before selling your current one, you put more pressure on yourself to sell quickly and at a high price. Depending on what strategy you use to purchase a new home while still responsible for an old one, you may feel compelled to accept the first offer you receive. However, selling first allows you to negotiate with buyers and wait to sell until you get the offer you want.

- Less pressure: Buying a new home before someone purchases your old one puts you on a crunched timeline to get rid of your current home as fast as possible. Waiting for the right buyer while paying for two properties can be a lot to handle. If you sell first, you can take your time considering sales strategies and making any renovations or repairs.

- Total equity for future purchases: Perhaps one of the most compelling reasons to sell before buying another house is the potential to tap into your current home’s equity when you make your next purchase. If you pocket a considerable profit, you may be able to pay a larger down payment and take out a smaller mortgage on your next home. With a high enough profit, you may even be able to offer cash, which is very appealing to sellers.

For the above reasons, selling a current home before buying another is usually the most straightforward course to take. When stepping into the market to purchase a new home, the lack of pressure on your time and funds can help you make the best decision regarding a sale and give you more money to put toward your next home.

If you’re in a seller’s market, selling before buying can be even more profitable. In a seller’s market, sellers have the upper hand in negotiations because there are fewer homes than potential buyers. This situation gives sellers the ability to keep their asking price high or even raise it. Because there’s such high demand, homes usually sell quickly in a seller’s market.

Cons of Selling First

However, selling before buying could also cause some logistical concerns. If you sell your home quickly, you might have to find temporary housing before purchasing your new home. When there’s a lot of competition in the housing market, a seller could reject your offer, and the property could go to another buyer. Should that happen unexpectedly, you might need to move your belongings into a rental unit or pay for storage until you can move somewhere else.

Before deciding when to sell, calculate the costs involved and whether you may experience a time crunch when going to buy. There may be a situation where timing forces you to move in with a friend or sublet an apartment for a while. That said, the cost of moving twice and storing your furniture and belongings until you buy a new house generally won’t outweigh the benefits of selling before buying a new home.

[download_section]

Buying a New Home Before Selling Your Current One

Sometimes, buying first can be appealing when you can afford to buy without recovering the equity in your old home or you’re in a buyer’s market and have negotiated an excellent deal for a house. This option may require some extra steps and additional help with financing the purchase. If you’re unable to pay for a new home out of pocket, you have several options for financing:

1. Home Sale Contingency

A home sale contingency is a clause you can include in your offer to purchase a house. This clause tells the seller you need to find a buyer for your own home before closing on the purchase. A sale and settlement contingency gives you the legal right to exit a contract if you don’t receive an offer for your current home in time. A settlement contingency protects you if an offer on your old home falls through.

A significant drawback to a home sale contingency is that it could make your offer less competitive to sellers. If the seller sees you can’t make a firm offer, they could pass over you in favor of a committed buyer when negotiating a deal. If you’re only able to make less competitive offers, buying a home could take longer. However, if the seller accepts your offer, you’ll be able to keep the home you want under contract while you wait for a buyer.

2. Bridge Loan

Another option for financing a purchase is taking out a bridge loan. These are short-term loans designed to bridge the time between when a homebuyer needs financing and when it becomes available. With a bridge loan, you can access the resources you need to pay for your current mortgage and make a down payment toward your new house.

These loans can be a simple way to get financing quickly. Note that you’ll need to make monthly payments on the bridge loan while also paying for your existing mortgage. However, when you sell the old home, you can use your profit to pay off the bridge loan. If your home takes a while to sell, you could be paying two mortgages on top of the bridge loan payments as you wait.

3. Two Mortgages

If you can afford it, carrying two mortgages may be the least complicated option for financing a home. Maintaining two mortgages while you wait for your old house to sell can keep you from entering into another loan like a bridge loan.

However, carrying two mortgages at once probably doesn’t sound enjoyable. The cost of two mortgages can become steep, so you may not be interested. Still, it could give you greater freedom to make an offer without being tied to a home sale contingency.

How to Get a Mortgage on a New Home

Whether you’ve already sold your old home or are just beginning the house-hunting process, you’ll need a mortgage before closing on a new house. Here are the steps you need to take to be ready to make that purchase and move into your next home.

1. Save for a Down Payment

The down payment may look different depending on whether you’ve already sold your old home. With the profits from your old home in your pocket, you can use it for a down payment along with any other funds you saved. Because a larger down payment means a smaller loan size, choosing to save the money you would have spent on your morning later can go a long way.

If you’re buying a home without the benefit of your previous home’s equity, you may qualify for a conventional loan with a down payment of only 3-10%. There are also mortgage programs that require as little as 0% down, like United States Department of Agriculture (USDA) loans and Veterans Affairs (VA) mortgages. With certain qualifications, you can reduce the amount you need for a down payment and avoid paying for private mortgage insurance.

2. Explore Mortgage Options

Before applying for a loan, consider which loan types are most beneficial for you in your financial situation. Some homebuyers choose to go with a conventional mortgage with 15-, 20- or 30-year loan terms. Special considerations — such as your credit score, veteran status or location — can qualify you for other loan types. With some careful research and the help of our dependable loan advisors, you can find the best mortgage type for your needs.

Also, think about what features you want in a house and what you’re willing to sacrifice. It may be best to buy a smaller or less updated home to keep your mortgage debt lower or concentrate your monthly debt payment on loans with higher interest rates, such as school or credit card payments. On the other hand, you may be comfortable buying at the higher end of your price range if you have few or no other debts.

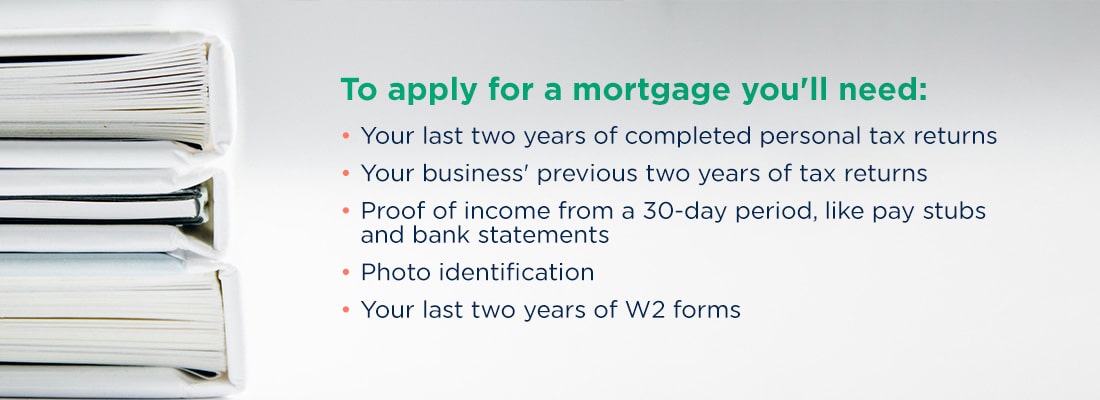

3. Complete an Application

Once you’re ready, you’ll want to apply for the mortgage of your choice. To apply, you’ll need some paperwork, including:

- Your last two years of completed personal tax returns

- Your business’ previous two years of tax returns, if applicable

- Proof of income from a 30-day period, like pay stubs and bank statements

- Photo identification like a driver’s license

- Your last two years of W2 forms

Once you have your forms in order, you can apply online, and your lender will look over your financial information to give you an estimated interest rate. With the online application at Assurance Financial, you can submit all of this documentation in as little as 15 minutes and get pre-qualified for a loan within 24 hours.

4. Wait for Processing and Underwriting

Once you’ve found the home you want and the seller has accepted your offer, your lender sends your financial information over to a loan processor, who double-checks all of the details and will contact you if they need any clarification.

After processing, your lender will likely order a home appraisal to determine the value of the property you intend to buy. Once an appraiser looks over your home, a loan underwriter will review your credit score and application once more to make the final approval. This stage finalizes the amount of your loan and your interest rate.

5. Head to Closing

When your loan is cleared, you can begin the final steps in your journey to homeownership. The title company will set up a closing day with you, and you can sign many of your closing documents online beforehand.

On closing day, you’ll bring your down payment in the form of a cashier’s check, plus any other fees and closing costs you may be required to pay. Alternatively, you can choose to set up a wire transfer for the funds. After you sign the last bit of paperwork, you’ll get the keys to your new home.

Get Started With Assurance Financial

If you’re looking to get a mortgage for your new home or refinance an old mortgage, Assurance Financial is ready to help. We provide complete support at every step of your loan application, and our licensed loan officers are experts at getting the home loan that best suits your needs. With a variety of loan types and competitive rates, we provide mortgage solutions for homebuyers at any stage of life.

At Assurance Financial, we understand you want a smooth mortgage process that leads you to your dream home. To get started and discuss your mortgage options, find a loan officer today and see why Assurance Financial stands out from other online mortgage lenders.

Linked Sources:

- https://assurancemortgage.com/paying-off-mortgage-early/

- https://assurancemortgage.com/calculators/should-i-refinance-my-mortgage/

- https://myhome.freddiemac.com/blog/homeownership/20190815-mortgage-options

- https://www.consumerfinance.gov/ask-cfpb/what-is-a-payoff-amount-is-my-payoff-amount-the-same-as-my-current-balance-en-205/

- https://assurancemortgage.com/everything-you-need-to-know-about-usda-rural-loans/

- https://assurancemortgage.com/5-things-know-va-loans/

- https://assurancemortgage.com/what-is-a-conventional-mortgage/

- https://assurancemortgage.com/apply/

- https://data.census.gov/cedsci/table?q=duration%20of%20homeownership%202018&tid=ACSDP1Y2018.DP04

- https://www.pewresearch.org/fact-tank/2021/03/08/amid-a-pandemic-and-a-recession-americans-go-on-a-near-record-homebuying-spree/

Purchasing a new home is an exciting step in life and requires a lot of time, research and planning. Before signing the final papers, there are many factors to consider and scenarios to prepare for to secure your home financing solution. In today’s market, you will likely have to take out at least one type of loan to help you pay for the house in a manageable way.

In some cases, you may have to take out several loans or pay for something called private mortgage insurance (PMI). Read on to learn more about how private mortgage insurance can allow you to purchase a home, even if you don’t have enough resources to make a standard down payment.

Table of Contents

- What is PMI?

- What is Mortgage Insurance on a Home Loan?

- Is PMI Good or Bad?

- Types of Private Mortgage Insurance

- Ways to Avoid Paying Mortgage Insurance

- How Much is PMI per Month?

- Does PMI Decrease Over Time?

- Does PMI Go Away if Home Value Increases?

- Find a Loan Officer

What Is PMI?

PMI stands for private mortgage insurance (PMI), which is a type of insurance for mortgages if you have a conventional loan. PMI is an additional payment on top of your standard monthly mortgage. The fee varies by situation and property value and gives your lender added security. The PMI payment protects your lender with a safety net of funds in the event of mortgage default and foreclosure.

In short, PMI lowers the risk for lenders who give money to people who lack the funds necessary to make a standard down payment on a house. While PMI protects the lender, it can add a costly monthly fee to your house payments. Luckily, there are ways to expedite the payment process and pay off enough of your home to eliminate the need for PMI.

What Is Mortgage Insurance on a Home Loan?

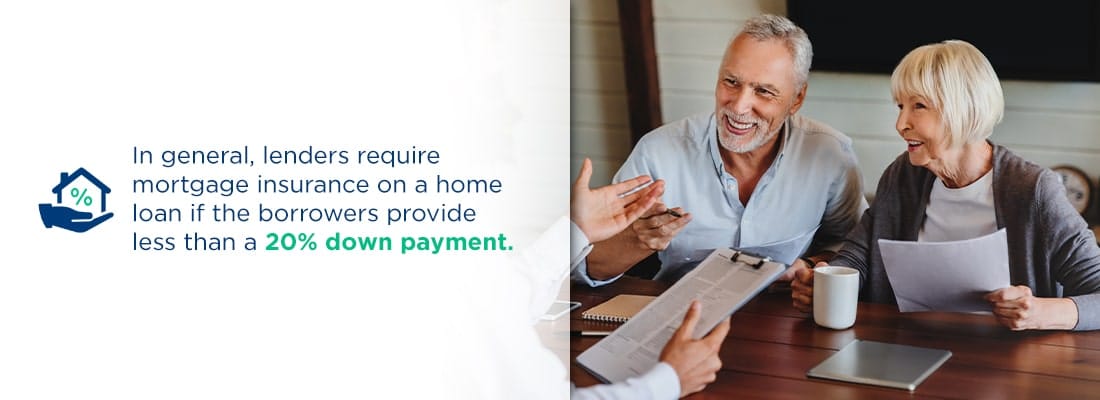

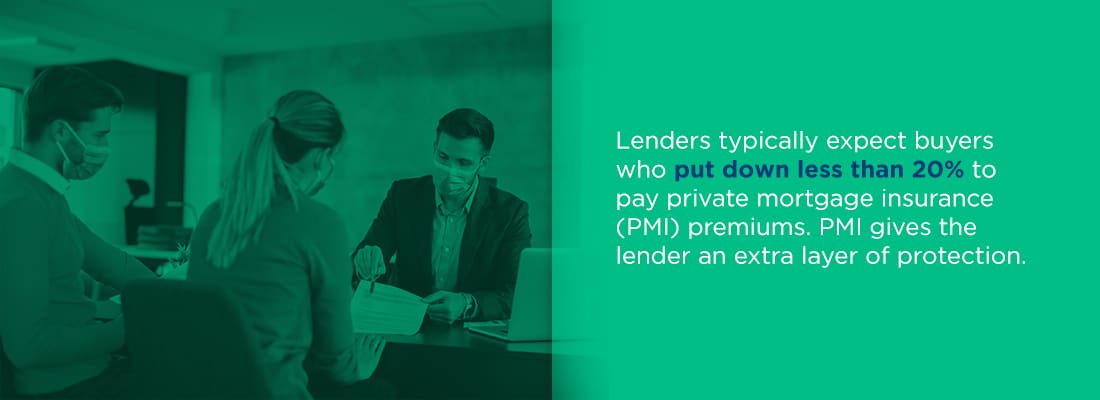

Whether you’re buying a home for the first time, refinancing or looking to purchase a house in the future, you may be wondering whether you’ll need to use private mortgage insurance. With PMI, you can still have your home loans approved even with less than a 20% down payment.

In general, lenders require mortgage insurance on a home loan if the borrowers provide less than a 20% down payment. Usually, the less money you can submit as a down payment, the higher your PMI monthly payment will be. To determine if you’ll need PMI on your home purchase, you first need to understand what PMI is and how it works.

Why Lenders Require PMI on a Home Loan

If you’re looking to buy a home, you should typically plan to save at least 20% of the purchase price for a down payment. If you do not have the standard 20% prepared, your lender will likely require you to pay private mortgage insurance premiums. To understand why lenders require PMI in these situations, consider what happens when someone defaults on their mortgage.

A mortgage default occurs when the homeowner misses at least three consecutive monthly payments, generating a loss of income for the lender. However, many states have laws that delay eviction, and the lender may have to wait two or more years before reclaiming a home.

By the time the house is sold in foreclosure, the lender could have accrued losses from months of missed payments plus years of potential property damage or neglect. The average loss a lender takes during the foreclosure process is about 20%, which is why the standard down payment is 20%. PMI payments help cover the lender’s losses in the event of default and foreclosure.

How Is Credit Score Related to PMI on a Home Loan?

A credit score gives lenders a numerical score for how creditworthy you are — essentially, this is a determination of the likelihood you’ll repay your loans on time. The higher your credit score, the more creditworthy you appear to banks and lenders. Higher scores may come with benefits, such as lower interest rates and higher loan approval rates.

Your credit score can make a significant impact on what you pay in monthly mortgage insurance premiums. PMI premiums are adjusted based on the creditworthiness of the borrower. A good credit score indicates a high level of creditworthiness and can reduce your monthly payments.

The difference in premiums can vary greatly depending on your credit score. You could save thousands of dollars in mortgage insurance payments throughout your loan with a high credit score.

Is PMI Good or Bad?

Mortgage insurance can improve your ability to purchase a home even if you don’t have the funding that’s traditionally required. In short, PMI makes low down payments possible.

In this way, PMI can benefit many homebuyers. With PMI, mortgage lenders make low and zero down payment home loans more accessible, making homeownership possible for buyers from various backgrounds. Borrowers with mortgage insurance also have the possibility of canceling PMI payments after acquiring enough equity through regular, timely payments.

While no one likes the idea of making payments on top of their regular mortgage, PMI can be an asset to homebuyers who want to purchase a house without a standard down payment. Since mortgage insurance doesn’t require a full 20% down payment upfront, PMI can get you in the home of your dreams sooner.

Everyone’s situation is different, and mortgage insurance provides an alternative so you can buy a house right away without saving the traditional 20%.

Types of Private Mortgage Insurance

As the borrower, you can choose between several options for how you want to make PMI payments. The two most primary categories are borrower-paid and lender-paid mortgage insurance. There are also several less common payment methods, including single-premium and split-premium mortgage insurance.

Understanding the differences between each payment option can help you make an informed decision and select the best type for your specific situation.

Borrower-Paid Mortgage Insurance

This is the most common PMI payment method. Borrower-paid PMI is paid monthly as part of your standard mortgage payments.

With this payment method, you generally make payments until you’ve reached a substantial equity level of your home. Generally, once you’ve reached about 20% of your home’s value, you can request your lender stop PMI payments. It can take years to get to the point where you’re able to cancel your borrower-paid mortgage insurance.

Lender-Paid Mortgage Insurance

Lender-paid PMI is another common payment method. It differs from the previous mortgage insurance because, as the name implies, the lender makes the payments instead of you. To compensate, you’ll pay a higher interest rate on your mortgage.

You typically won’t see the added expense on your mortgage payment, but you will pay more than you would without mortgage insurance.

Lender-paid mortgage insurance is more permanent than borrower-paid. You can’t cancel a lender-paid policy even when your equity is worth more than 20% of the purchase price. The best way to eliminate the extra costs associated with lender-paid mortgage insurance is to refinance your mortgage.

Even with refinancing, there is no guarantee you will find a better deal.

Single-Premium Mortgage Insurance

A single-premium PMI, also called single-payment, requires just one payment upfront. While less common than the previous payment types, this method allows you to get a lower monthly payment while still letting you qualify for a mortgage without a full 20% down payment.

Single-payment mortgage insurance is a nonrefundable payment that you generally pay at closing. However, if you choose to sell your home or refinance in the future, you won’t get your single-premium payment back.

This payment is less common than others because if you don’t have the funding to make a 20% down payment, you might not have enough to pay the insurance premium upfront. You can choose to finance the payment into the mortgage, in which case you’ll pay interest on it until you pay off your loan.

Split-Premium Mortgage Insurance

This final method is very similar to single-premium mortgage insurance. Instead of paying for everything upfront, you split your lump sum into two, paying part at closing and dividing the rest into monthly payments. The upfront portion is typically between 0.5% and 1.25% of the total loan.

The primary benefit of this payment method is you don’t need as much money upfront during closing as you do with single-payment mortgage insurance. You also avoid increasing your monthly payments in comparison to a more traditional buyer-paid mortgage insurance.

The premium paid at closing is nonrefundable. However, you may be able to request that your lender cancel monthly premiums after you’ve reached a substantial level of equity.

[download_section]

Ways to Avoid Paying Mortgage Insurance

If the idea of tacking on an extra fee to your monthly mortgage doesn’t appeal to you, you’re not alone. Luckily, there are several ways to avoid paying private mortgage insurance premiums. Take a look at the following options to determine if one of these alternatives could work for your situation.

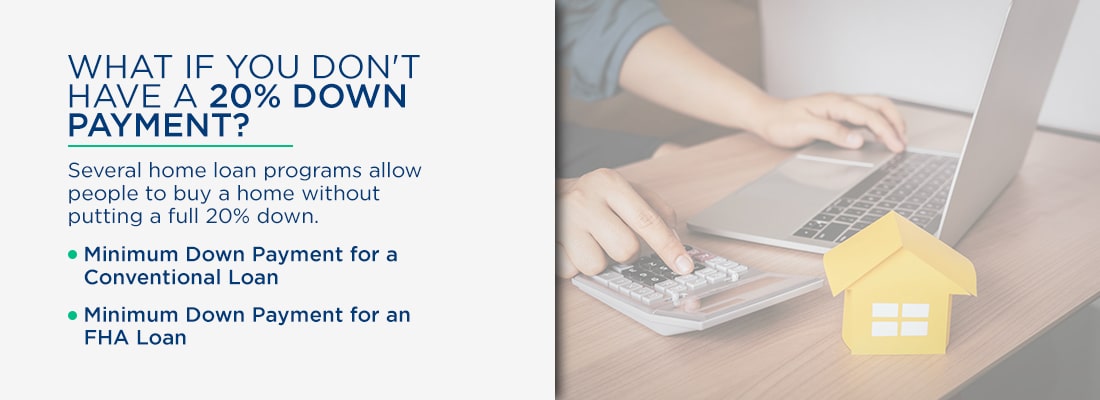

1. Secure a 20% Down Payment in Advance

The simplest way to avoid private mortgage insurance is to save up well in advance to make the entire down payment of at least 20% of the purchase price. A larger down payment can also help you get a lower interest rate on your mortgage and reduce the number of fees you’ll pay.

These factors allow you to gain home equity faster, reducing the amount you’ll have to pay back over time.

2. Consider a Piggyback Loan

A piggyback loan allows you to purchase a house with two loans that usually cover 90% of the purchase price. This type of loan helps ease the upfront costs of buying a home without locking you into private mortgage insurance.

You still take out a standard mortgage for 80% of the purchase price with a standard piggyback loan. Then, you take out another, smaller loan that’s typically about 10%, allowing you to pay only 10% upfront as a down payment instead of the standard 20%. This type of loan is also called an 80-10-10.

Another common way to split the mortgage is in a 75-15-10 ratio, in which you’d take out a mortgage for 75% and a loan for 15% and still pay 10% at closing.

Piggyback loans can offer an effective alternative to PMI when you don’t have 20% of your purchase price for a down payment.

3. Find a Loan That Won’t Require PMI

Depending on your circumstances and with a little extra digging, you may be able to find a lender that doesn’t require mortgage insurance. If you’re a veteran, you could qualify for a home loan supported by Veterans Affairs (VA). These loans do not require PMI and eliminate the need for a down payment.

The United States Department of Agriculture (USDA) offers similar home loan programs without mortgage insurance requirements. Your location or situation may qualify you for a USDA home loan.

Other lenders provide specialty loan programs that don’t require PMI, including additional compensating factors to cover a smaller down payment.

4. End Your PMI Early

If you find that paying PMI is unavoidable or the best option in your situation, you can still minimize its financial impact on you by canceling it as quickly as possible. If you have borrower-paid or split-premium PMI, you should monitor your loan balance and payments and request your lender cancels your PMI payments immediately after your equity is at or above 20% of your home’s original value.

Consider making extra payments when you can toward your principal so you can cancel your PMI even faster. Ensure you make your payments on time to increase the likelihood your lender will cancel your mortgage insurance when the time comes.

How Much Is PMI per Month?

Private mortgage insurance payments can vary significantly depending on your unique circumstances. In general, you should expect to pay between 0.5% and 1.5% of the total loan amount each year. For example, on a $300,000 loan, you may pay anywhere from $1,500 to $4,500 every year. This works out to $125-$375 per month.

These rates will typically remain the same throughout your mortgage insurance payments. However, numerous factors can raise or reduce the total percentage you’ll pay annually in mortgage insurance premiums.

The following factors can influence your yearly required mortgage insurance payments, affecting how much you’ll pay per month for PMI:

- Your mortgage loan size: One of the most significant determining factors in your mortgage insurance’s cost is the total loan amount. The larger your loan is, the greater your monthly mortgage premiums will be. For this reason, it’s important to stay within a reasonable budget based on your income and funding.

- The down payment size: Since one of the greatest factors in determining your monthly PMI payments is the size of your mortgage loan, one of the simplest ways to reduce your premium is to increase the size of your down payment. Even if your funding does not support putting the full 20% down at closing, you can pay as much as possible upfront to avoid costly PMI payments.

- Your credit score: Another crucial contributing factor to your monthly PMI premium is your credit score. This component is essential to remember since you can have a great credit score even if you don’t have a lot of cash. Building strong credit habits over time can help you save thousands of dollars in the long run on mortgage insurance.

- The type of mortgage you have: Different types of loans can influence your PMI rate. For example, on a conventional mortgage issued by a bank, you may have a higher PMI than you would on a Federal Housing Administration (FHA) loan. This is because FHA loans are designed to accommodate first-time homebuyers and people with low-to-moderate income levels.

- Property appreciation potential: If you are moving to an area where home values are appreciating, you may receive a lower PMI premium. If your home’s value increases enough, you could even stop PMI payments completely. You can have your home appraised again, and if the value has risen over 20%, you could request the cancellation of your PMI.

Does PMI Decrease Over Time?

Your mortgage insurance rate will usually remain consistent throughout your payments. However, if you’re eager to save money on monthly payments and cancel your PMI early, there are several ways you can get rid of your mortgage insurance premiums.

The following methods are ways you can ditch your PMI and get greater financial freedom:

- Take advantage of final termination: Your lender is usually required to end PMI automatically after you’ve reached the halfway point of your loan’s amortization schedule, regardless of how much equity you’ve acquired. This means if you have a 40-year loan, your lender will terminate your mortgage insurance after 20 years as long as you’re current on your payments.

- Reach equity of 80% or higher: When your equity reaches 20% or more of the original property value, you have the right to request that your lender cancel your mortgage insurance. If you have extra funding, making additional payments is one way to free yourself of PMI faster. As long as you’re up-to-date on payments, the lender should cancel your PMI after you own 20% in equity.

- Refinance your mortgage: If you notice a drop in mortgage rates, you may want to consider refinancing your mortgage to reduce your monthly payments and save money on interest costs. This process could let you eliminate your PMI if your new mortgage is less than 80% of your home’s value. Before committing to refinancing, be sure to consider added closing costs to ensure the transaction is worthwhile.

- Have your home reappraised: The market can make sudden changes to your home’s value. If your property appreciates enough, you could eliminate your PMI with the increased value. If you think this is possible, have your home reappraised. If the value increases by more than 20%, you may be able to cancel your PMI.

Does PMI Go Away if Home Value Increases?

Your property’s fluctuating value can affect your private mortgage insurance. While your PMI won’t magically “go away” if your home value appreciates, you may be able to request that it be canceled if it reaches a certain threshold.

In most cases, if your home increases in value by 20% or more, you can terminate your mortgage insurance premiums. As long as you’ve owned the property for a minimum of five years and your mortgage is no more than 80% of the new appraisal value, you can ask to cancel your mortgage insurance

To start this process, you have to schedule a new appraisal of your home. Keep in mind that most appraisals cost between $312 and $407, with an average of $349. Some lenders may accept a broker price opinion, which can be a cost-effective alternative.

You can help increase the value of your property faster by renovating it or adding new amenities such as an extra room or a swimming pool.

Learn How Assurance Financial Can Help You With Home Financing Today

Assurance Financial offers resources and professional experience which can help make your home purchase easy. We are an independent, full-service residential mortgage banker with more than 20 years of experience servicing the public. At Assurance Financial, we can complete the entire mortgage process in-house with a simple, fully online application.

We are committed to providing quality, personalized service and operating with integrity and honesty. We offer every type of loan on the market and want to do everything we can to ensure you get the service you need.

With Assurance Financial’s support, you can pre-qualify for a loan in as little as 15 minutes. Apply online with Abby, our helpful virtual assistant, or find a loan officer near you to learn more.

Enjoy excellent service and custom competitive rates when you choose Assurance Financial. Contact us online today for a no-obligation quote.

Linked Sources:

- https://www.canr.msu.edu/news/5_facts_to_know_about_mortgage_insurance

- https://www.hgexperts.com/expert-witness-articles/broker-price-opinion-and-property-inspections-practices-and-procedure-for-the-mortgage-industry-18102

- https://www.forbes.com/advisor/mortgages/what-is-a-piggyback-loan/

- https://www.benefits.va.gov/homeloans/

- https://themortgagereports.com/24154/private-mortgage-insurance-pmi-cost-low-downpayment-return-on-investment

- https://eligibility.sc.egov.usda.gov/eligibility/welcomeAction.do

- https://wsecu.org/resources/what-is-private-mortgage-insurance

- https://www.scefcu.org/news-and-alerts/article/average-cost-home-appraisal

- https://assurancemortgage.com/apply/

- https://assurancemortgage.com/find-a-loan-officer/

- https://assurancemortgage.com/contact-us/

Additional Sources:

- https://themortgagereports.com/17948/private-mortgage-insurance-pmi-conventional-loans

- https://www.nerdwallet.com/article/mortgages/pmi-calculator

- https://myperfectmortgage.com/how-your-credit-score-affects-the-pmi-premium/

- https://www.bankrate.com/mortgages/removing-private-mortgage-insurance/

- https://www.investopedia.com/ask/answers/081214/average-what-can-i-expect-my-private-mortgage-insurance-pmi-rate-be.asp

Tiny houses are beloved for their cozy atmosphere, affordability, and mobility — with a tiny home, you can travel anywhere you dream. At 400 square feet or less, tiny houses are great for downsizing and finding out what really fulfills you in life. Whether you’re looking to take all the comforts of home on the road with you or you’re hoping to downsize and reduce your carbon footprint responsibly, joining the tiny house movement can be quite a worthwhile investment.

However, tiny houses can come with big challenges for financing since their small size makes them ineligible for many mortgage and insurance plans. From finding the right mortgage to finding a legal place to store your home, you must understand the unique financial demands of a tiny house and prepare for challenges ahead of time. Get ahead of the game and learn how to finance your tiny home with Assurance Financial.

Topics Covered

- What Qualifies as a Tiny Home?

- How to Finance a Tiny Home Build

- What Are the Challenges to Financing a Tiny House?

- How Long Can You Finance a Tiny House?

- Is It Cheaper to Buy or Build a Tiny House?

- Do Tiny Homes Depreciate?

- How Much Are Tiny Homes Worth?

What Qualifies as a Tiny Home?

Any home that’s under 400 square footage is considered a tiny home. Tiny homes have gained traction in the past decade as a pushback against the growing square footage and rampant financial appreciation of larger family-sized homes. Tiny homes allow their owners to save more money and work less, all while getting to customize their own unique living space. Today, thousands of people live in tiny homes both on and off the grid, and many people even take their tiny houses with them on the road.

There are two main types of tiny homes — those on wheels and those on foundations. Tiny houses on wheels (THOW) operate like a trailer and allow easy transportation and setup almost anywhere with the right access points. For insurance and financing purposes, THOWs fall under the umbrella of recreational vehicles (RVs) and covered as such. THOWs also come with many additional financial considerations, like parking fees, water bills, electricity costs and transportation costs.

Compared to THOW, tiny houses on foundations are easier to mortgage and insure. Mortgage companies only cover buildings on foundations since they are more protected from the elements. However, tiny homes on a foundation may come with additional costs due to the size of the lot they reside on and other property taxes.

The options for tiny house usage are endless. Tiny houses are perfect for people just starting their home-owning journey, those looking to downsize, those in retirement and those who want to live while traveling on the road. Many purchase tiny houses to be accessory dwelling units for parents, in-laws, in-home caregivers and adult children looking for an affordable place to stay. Tiny homes are also an affordable option for those looking to build an office or small business location in their existing yard.

How to Finance a Tiny Home Build

Tiny homes aren’t subject to the same financing, mortgage and insurance rules as traditional home loans. The average tiny home can cost buyers anywhere between $30,000 and $100,000 depending on the size, make and material of the tiny home, which means adequate financing is still a high priority. Financing and insuring a tiny home requires working with banks and lenders who may work exclusively with tiny homes and understand the unique challenges they bring to the table.

While many go into the tiny home buying process to lessen their debt, many buyers still need comprehensive financing packages to create or purchase their dream tiny home. With the backing of a major bank or credit union, you can finance your tiny home for up to 20 years for the promise of smaller monthly payments. Comparatively, many RV loans also allow you to finance THOWs.

Here are some of the best ways to finance a tiny house:

Traditional Mortgages

If you want to finance your tiny home with a traditional mortgage, it needs to be on a solid foundation on a plot of land. However, it can be pretty difficult to get a traditional mortgage on a tiny home. Traditional mortgages are usually only an achievable means of funding for those with large tiny homes on a foundation or those with expensive, luxury tiny houses with price points close to a traditional home.

Land Loans

Since many tiny homes don’t come with a plot of land, you may need to consider a land loan. Land loans operate similar to mortgages but have larger down payments and interest rates due to the lack of property collateral. To qualify for a land loan, you must have a great credit score and a significant portion of the total cost saved as a down payment. You must also have a detailed land development plan to convince lenders that you’re a good investment.

Construction Loans

If you’re building your own tiny home from the ground up, you may be eligible for a short-term construction loan that covers the cost of your customized tiny house. Construction loans are designed to help homeowners get started on building a custom home to then use a mortgage to pay off the home once it’s been completed. This method is one potential hack for those seeking a traditional mortgage who would otherwise be unable to secure one.

Tiny House Builders and Lenders

Many tiny house builders offer their own financing and lending programs, so you don’t have to complicate the financing process and go through anyone else. Today, there are hundreds of tiny house contractors to choose from located in every state. When you opt to finance your build through a tiny house building company, you’ll get to customize every square foot of your home while receiving financing.

Home Equity Loans

If you already own a home and are looking to add a new private tiny home space to your land, you may be able to tap into your existing home equity to get what you need. This strategy is perfect for those building additional living quarters or offices. Home equity loan amounts are determined by subtracting the amount of money you currently owe on your mortgage from your total property’s value. The more of your home you’ve paid off, the more you can tap into your home equity.

Home Equity Lines of Credit

While a home equity loan is ideal for those looking for a lump sum at a fixed interest rate, those looking to draw money as they need it should apply for a home equity line of credit instead. Home equity lines of credit frequently come with an adjustable interest rate and allow you to pay in interest-only installments. If you don’t need a substantial sum to invest in your tiny home, a home equity line of credit is probably a better choice than a home equity loan.

RV Loans

Tiny homes that are on wheels and lack foundations may be eligible for certification and financing through the Recreation Vehicle Industry Association (RVIA), which offers RV loans to tiny homes that are considered permanent residences. The RVIA ensures that tiny homes on wheels (THOW) are complicit with the U.S. Department of Transportation’s National Highway Traffic Safety Administration codes and the living quarters are sufficient. You can also obtain RV loans through many major banks and credit unions.

While RV loans can be difficult to obtain due to strict safety standards, many manufacturers specialize in creating built-out RVIA certified tiny homes so you can secure a low-interest RV loan.

Credit Cards

While it’s not always advisable, you can technically charge a tiny home on your credit card if you have a large enough balance and the savings to do so. When done correctly, this method can earn you an astounding amount of cashback and eliminates the need for a mortgage. However, many financial advisors would highly discourage this method due to the rapid pace at which it can rack up interest.

What Are the Challenges to Financing a Tiny House?

Attempting to finance a tiny house comes with a unique set of challenges that aren’t seen in the rest of the housing market. For example, most home loan companies only offer loans starting at $50,000. They require that tiny homes have permanent foundations, making financing tiny homes on wheels impossible to accomplish in the traditional lending market. Certain loans, like FHA plans, also don’t cover most tiny houses and require a 400-square-foot minimum.

Many banks choose not to invest in tiny homes because they understand they are depreciating investments. Banks like to invest in large structures that will outlast your time with them, making tiny homes seem like a gamble. Due to the small size of tiny homes, insurance companies may also see them as a liability that’s highly prone to damage from both weather and their time on the road.

Another potential challenge with financing a tiny home involves the extra money you’ll have to spend on permits, upkeep and transportation. Purchasing a tiny house comes with multiple additional costs you need to anticipate, including:

- Local building permits: Depending on where you live, your local building permit could cost as little as a couple of hundred dollars or over a thousand.

- Foundation materials: If you’re keeping your tiny home stationary, you must invest in a foundation. Having a foundation is also a prerequisite for most tiny home mortgage and insurance policies.

- Land/parking costs: Just because your tiny home is on wheels doesn’t mean that you won’t need a place to park. Whether you choose to invest in your own plot of land or live in a tiny house community, finding a place to park your tiny home is a difficult feat.

- Vehicle costs: If you’ve opted to purchase a tiny home on wheels, you’re going to need a vehicle that’s strong enough to endure traversing the country with thousands of pounds in tow. These vehicles also tend to be less fuel-efficient and may require expensive premium fuel.

- Utilities: Tiny houses on wheels require special utility accommodations for electricity, gas, and water that aren’t as easy to secure as traditional homes on foundations. Those who take their tiny homes on the road can end up paying extra for these essential utilities.

- Appliances: Since tiny houses don’t have the room or the hookups for standard household appliances, it’s unlikely that you can use the appliances you’ve already invested in. The appliances you choose must be energy efficient to accommodate the smaller energy grid your home has, and have a smaller footprint so you don’t have to sacrifice a whole living area for the fridge or stove unit.

- Laundry and storage accommodations: The small footprint of tiny homes means that many can’t accommodate a washer and dryer in the space. While laundromats are relatively inexpensive, frequent trips to wash your clothes can add up to hundreds of dollars a year. The smaller square footage also limits storage altogether, meaning you may need to invest in a storage unit if you have valuable possessions that don’t fit in your tiny home.

- Home insurance: Most insurance companies specify that a tiny home must be on a solid foundation to qualify for a policy, but many companies choose not to protect tiny homes at all due to their susceptibility to damage. If your tiny home is on wheels, you may have more luck getting it protected as a recreational vehicle than a tiny home.

How Long Can You Finance a Tiny House?

Unlike traditional mortgages, tiny houses have much shorter financing periods due to their size. Options like land loans and construction loans have to be paid off shortly after acquisition — usually in less than a handful of years — while home equity loans and lines of credit give you a greater period of time to pay back the money you owe. Overall, you should save a significant portion of the cost of your tiny home beforehand to secure a loan and get your home paid off.

[download_section]

Is It Cheaper to Buy or Build a Tiny House?

Whether purchasing or building a tiny house is the most cost-effective choice depends on several considerations and what you want out of your house. Are you looking for a short-term housing fix at an affordable cost, or are you trying to make a forever home and are ready to invest in it as such? Do you have experience with DIY construction, or are you looking for a ready-made solution?

Purchasing a tiny house is almost always more expensive than building your own, but certain ready-made tiny homes can also be quite cost-effective. While purchasing a ready-made tiny home may give you more bells and whistles, it can also cost you as much as a regular house, with some luxury ready-made tiny houses costing upwards of $100,000. However, purchasing a tiny house may save you plenty of money considering the reduced labor costs and pre-included add-ons such as plumbing, electricity, and dormers.

If you want to live in a tiny home but aren’t enamored with the idea of creating your own, purchasing a ready-made tiny home may be the most cost-effective option of the two. Purchasing a tiny home may also be easier to finance than building your own since many ready-made tiny homes already come with foundations or plots of land that make zoning and acquiring a mortgage easy.

If you love the idea of customizing your floor plan and interior at the most affordable rate possible, building your own tiny home is the right option. Building your own tiny house doesn’t have to be expensive, and it’s more than possible to build a tiny home for less than $10,000. The most important part of building your own tiny home is to go in with a detailed plan and stick to it. Building your own tiny home requires budgeting for costs including labor, materials, and potential overtime.

Do Tiny Homes Depreciate?

Most tiny homes are a form of personal property — like RVs and cars — and consequently, decrease in value over time. If your tiny home is built on wheels, it’s more akin to a recreational vehicle and has reselling prices more similar to RVs than homes. If you’re looking for an investment, you should carefully consider the depreciation of a tiny home’s value.

Tiny homes are best for those dedicated to changing their living situation while keeping their costs low — not those looking for a transitional space with high resale value. In addition to their depreciation, tiny homes can also be difficult to sell due to the fact that it’s cheaper for many buyers to create their own customized home than buy a used model.

There’s also a much smaller market for tiny homes than full-sized family homes since tiny homes don’t have the space to house a growing family. Tiny homes aren’t the right choice for those looking to grow their equity and appreciate their assets.

If you’re set on moving into a tiny home temporarily and are considering reselling it in the future, make sure to pick a model that’s high quality and customized in a way that a wide variety of people can enjoy being in it. Always make sure to properly maintain your home to keep its resale value from falling even more than it needs to. While attempting to resell a tiny home, it’s essential to keep it as clean and uncluttered as possible.

While the depreciation of tiny homes is tragic, it is a plus for those looking to move into a used tiny home. The supply of tiny homes may be small, but the equal demand tends to create a buyer’s market.

How Much Are Tiny Homes Worth?

Tiny homes fluctuate greatly in worth in accord with market demand, location, materials, and more. Tiny homes can range anywhere from $8,000 to $150,000, but they tend to depreciate quickly. Since tiny houses only appeal to a niche demographic of real-estate purchasers, they can be difficult to accurately appraise and find a buyer.

Due to the affordable cost of building your own tiny home, many buyers choose to customize their own home rather than buy a used model off of the market. While your tiny home might not appreciate in value, the lot that it’s located on may. Purchasing a land plot with your tiny home, while initially expensive, may result in better returns since land is a limited, and therefore valuable, resource.

Always make sure that a tiny home is worth your financial investment. Does owning a tiny house help you reach your long-term financial goals by helping you save money? Are you committed to the lifestyle changes that accompany investing in a tiny home? Can you take the financial risk of investing in an asset with a high likelihood of depreciation? Carefully consider your options from both a personal and financial perspective before deciding if a tiny home is worth it.

Home and Construction Financing From Assurance Financing

Assurance Financing has helped our clients turn their houses into homes for more than two decades. Our passionate, in-house team cares about servicing every loan from the beginning to the end. As an independent, full-service mortgage banker, we’re continuously growing our business to gain new state licenses across the country. After a quick pre-qualification process, we’ll work with you through the application, processing, and funding processes.

We offer both home loans and home construction loans. Whether you’re a first-time or experienced homebuyer, we’re excited to work with you. Learn more about our real estate financing options or talk to an agent today.

When you’re ready, let our helpful virtual assistant, Abby, guide you through the application process.

Linked Sources:

- https://www.hud.gov/sites/documents/SFH_POLI_APPR_PROP.PDF

- https://www.rd.com/list/costs-owning-tiny-home/

- https://www.rvia.org/about-us

- https://www.hud.gov/sites/documents/SFH_POLI_APPR_PROP.PDF

- https://www.businessinsider.com/how-much-does-tiny-house-cost-worth-it-2019-2

- https://assurancemortgage.com/first-time-home-buyer-loans/

- https://assurancemortgage.com/experienced-homebuyer/

- https://assurancemortgage.com/remodeling-construction/

- https://assurancemortgage.com/purchase-your-home/

- https://assurancemortgage.com/contact-us/

- https://assurancemortgage.com/apply/

Unlinked Sources:

The real estate market has fluctuated significantly over the past few decades, with a median sales price difference of $195,900 in the last 20 years alone. With these constant housing market shifts, it can be challenging to determine the best time to buy or sell a house.

The key to getting the best possible value for your money is understanding what’s happening in your local real estate market — whether you’re a buyer or a seller. You can do so by learning about the differences between a buyer’s and seller’s market, how to identify these market types, and effective tactics for navigating either.

Topics Covered

- What’s the Difference Between a Buyer’s and Seller’s Market?

- What Is a Buyer’s Market?

- What Is a Seller’s Market?

- How to Tell if It’s a Buyer’s or Seller’s Market

- Is It Bad to Buy in a Seller’s Market?

What’s the Difference Between a Buyer’s and Seller’s Market?

Buyer’s vs. seller’s markets are a matter of supply and demand. At its base, the housing market is relatively simple to understand, but there’s more that goes into it than these basic definitions. There are three primary differences between each of these market types.

Power Dynamic

The most considerable difference between a buyer’s and seller’s market is who has the power — the buyer or the seller. As you might have guessed, the power dynamic leans toward the buyer in a buyer’s market and a seller in a seller’s market. Why? Because in a buyer’s market, there’s more housing inventory and lower prices, giving power to the buyer. Conversely, seller’s markets enable sellers to ask for more money and encourage bidding wars, giving them the power.

Marketing Strategies

Marketing a home in a buyer’s market vs. a seller’s market requires different tactics. In a market that favors buyers, sellers and their realtors have to put in a much greater effort to make their homes stand out through means of social media, open houses, and advertisements.

Seller’s markets don’t require quite as many marketing strategies, though some level of promotion is still necessary to showcase their properties, such as professional photographs, deliberate staging, and fair pricing.

Buyer Expectations

Buyers have far different expectations when looking for a home in a buyer’s market than they do in a seller’s market. In a real estate market that benefits buyers, individuals expect to have plenty of housing options and get good deals. In a seller’s market, buyers expect a more competitive environment with higher pricing.

However, with more expensive homes, homebuyers often prefer that their end-purchases reflect their money, expecting high-quality properties like move-in-ready homes. In turn, sellers must offer houses that warrant their premium list prices.

What Is a Buyer’s Market?

A housing market where the supply exceeds the demand is called a buyer’s market. This means that though many properties are available, there’s a shortage of buyers interested in purchasing them. These market conditions give buyers the upper hand over sellers, compelling the market to respond accordingly.

In a buyer’s market, prices decrease and houses remain on the market for longer, forcing sellers to compete with one another and drop their asking prices to attract buyers in an environment where the clientele is limited. Sellers are much more willing and likely to reduce their prices in a buyer’s market to prevent them from losing a sale.

What Causes a Buyer’s Market?

A buyer’s market stems from changes in market conditions that advance homebuyers over sellers. In most cases, any situation that decreases a buyer’s urgency to buy and increases a seller’s urgency to sell will generate a buyer’s market. Some of the most common causes of buyer’s markets include:

- Economic recession: An economic recession occurs when economic activity declines significantly in a designated region for a prolonged period. This economic decline can cause homeowners to sell their houses if they can no longer afford to pay their mortgages, increasing housing inventory and shrinking the buyer pool.

- Job market decline: A dwindling job market may prompt homeowners to sell their houses and move to different locations with more job opportunities, creating a buyer’s market.

- Increased construction: Large influxes in new housing construction often result in buyer’s markets — just because homes are being built doesn’t mean there will be buyers interested in them. Real estate overdevelopment in an area often leads to an excess housing supply.

- Demographic shifts: How a certain demographic approaches the local real estate market can drastically impact supply and demand. For example, if younger people in an area decide to postpone homeownership, the buyer pool shrinks.

A prime example of one of these factors creating a buyer’s market was the financial crisis of 2007-2008. During this time, unsustainable mortgage rates caused many homes to go into foreclosure, resulting in significant price drops from homeowners desperate to sell. Supply increased drastically, but there were little to no buyers interested in purchasing properties.

Tips for Buying in a Buyer’s Market

If you’re a buyer looking to purchase real estate amid a buyer’s market, it’s the best time for you to be doing so. In a market that benefits the buyer, there are numerous tactics you can employ to negotiate a great deal and get the most value for your money:

- Take your time: You have the power in a buyer’s market. That means you can take your time browsing your options with minimal risk of losing a property you’re interested in. With a buyer’s market comes low demand for houses, so you likely won’t be competing with other interested parties and can therefore proceed without a sense of urgency.

- Weigh your options: As a buyer in a buyer’s market, you can relax and evaluate all your housing options to find a place that’s perfect for you. Knowing what’s on the local real estate market ensures that you find your ideal fit and gives you a greater ability to negotiate based on competing list prices.

- Pay attention to days on market: In a buyer’s market, real estate is likely to remain on the market for much longer than average. The longer a house stays on the market, the more you can negotiate with the seller to secure a more affordable price.

- Offer less than the asking price: Sellers are much more willing to lower their prices to close a deal in a buyer’s market. When negotiating a price drop, think about how much you want the house, how much you’d expect it to go for and how happy you’d be with the house with or without a reduction.

- Seek seller concessions: In addition to offering a lower price for a house, you can also ask that the seller pay your closing costs, which can account for approximately 15% of a home’s purchase price. You may also be able to ask the seller to impose a more flexible closing date, including appliances in the list price or add bonuses like furniture.

- Request repairs: If you notice that the house has damage but is not meant to be a fixer-upper, you can ask the seller to make repairs.

Tips for Selling in a Buyer’s Market

As a seller in a buyer’s market, you may have to be a bit more strategic in your sales plan. However, that doesn’t mean you have to submit to every buyer’s whim. Consider these tips when selling a house in a housing market that benefits the buyer:

- Optimize your marketing: It’s vital that you market your property as professionally as possible to attract buyers. Try highlighting your home’s competitive advantages, taking high-quality photos, and implementing up-to-date decor to create a polished look.

- Price competitively: In a buyer’s market, it’s crucial that your house is priced similarly or lower than other homes in the area. Because buyers have the power, they won’t hesitate to move on to the next property if your price is too high.

- Make repairs: When buyers have more houses to choose from, they tend to be pickier about their options. That’s why it’s beneficial to hire someone to conduct a pre-inspection of the house so you can pinpoint and fix any problems before listing the property.

- Consider closing costs and concessions: In a competitive market, you may have to go the extra mile by paying for closing costs or including concessions to close the deal.

- Be open to negotiation: Perhaps the most important part of selling a house in a buyer’s market is being flexible. It’s easier to close a deal when you’re open to negotiation and prepared to compromise with buyers.

What Is a Seller’s Market?

A seller’s market occurs when the housing demand exceeds the supply, meaning there are many interested homebuyers but a shortage of real estate inventory. Because there are more buyers than available homes in these market conditions, sellers have the advantage.

In a seller’s market, houses sell faster than average, requiring more buyers to compete with one another to secure a property. This higher competition often makes individuals willing to spend more than they normally would on a house, enabling sellers to raise their costs at or above the original asking price — with little to no pushback from buyers.

These housing market conditions minimize the buyer’s power to negotiate and often lead them to accept properties as-is.

What Causes a Seller’s Market?

Like a buyer’s market, there are numerous factors that can cause the real estate market to fluctuate in favor of the seller. Some of the primary contributors to a seller’s market include:

- Low interest rates: When mortgages have lower interest rates, more individuals feel inclined to buy. With lower interest rates and limited houses on the market, more bidding wars will likely occur, and more buyers will be willing to pay above the asking price.

- Job market growth: A booming job market brings more individuals to local areas seeking jobs. This job market increase attracts more people to the region, causing a greater need for real estate.

- Population growth: Like growing job markets, significant population increases also raise the demand for housing. If few properties are available during this population growth, the demand can quickly exceed the supply, giving sellers the upper hand.

- Development limits: Sometimes, local governments will implement development limits that restrict how many new houses can be built in an area, resulting in a lower housing supply.

- Decreased home construction: Even if there are no development limits in an area, there may simply be a shortage of new home construction, resulting in decreased real estate inventory.

For example, the year 2010 marked significant growth in San Francisco’s technology sector, bringing throngs of people to the city in search of higher-paying jobs, creating an influx in housing demand. However, due to the local government’s development laws, the supply remained low. As a result of San Francisco’s job market growth and construction limits, sellers gained an extreme market advantage, with the home values rising by over 85% to the previous decade.

Tips for Buying in a Seller’s Market

If you’re preparing to buy a house in a seller’s market, you may have to take some extra precautions to get the best price:

- Act fast: If you find your dream home, it’s crucial to act immediately to minimize the risk of losing a listing. In a seller’s market, properties go fast — sometimes even the day they’re listed.

- Prepare for bidding wars: You should know that you likely won’t be the only buyer interested in a house and be prepared to engage in bidding wars with other parties. Determine the most you’re willing to pay for a home and consider how much you can realistically afford before placing a bid.

- Don’t push the envelope: As a buyer in a seller’s market, you can’t ask for too much or risk losing properties to individuals with fewer stipulations. Sellers can afford to be much pickier in a seller’s market, so you should keep your offers simple instead of requesting contingencies, concessions or repairs.

- Don’t settle: Though sellers have the advantage, that doesn’t mean you have to settle for a home you don’t love just because it’s cheaper. Buying a property is a major investment, so try not to make a decision that you won’t be happy with later.

- Get pre-approved: You can stand out among other buyers by getting pre-approved for a mortgage, showing sellers that you’re financially able to follow through with your offers.

Tips for Selling in a Seller’s Market

Being a seller in a seller’s market is grounds for celebration. Even though you may not need a strong strategy to sell, there are still things you can do to generate the best possible outcome:

- Get your house in shape: Though you’ll likely receive considerable interest in your property, you should still present it in the best possible light by cleaning and organizing it beforehand. Tidying your house may even encourage higher offers.

- Price fairly: Selling in a seller’s market doesn’t mean you should hike up your prices as high as possible. When you price your home fairly at market value, you’ll likely attract more interested buyers than sellers with unreasonably high list prices.

- Consider offers carefully: Keep in mind that the highest offer isn’t always the best offer. Buyers can’t always afford to pay what they offer, which is why you should evaluate a buyer’s financial qualifications before accepting an offer.

- Confirm pre-approval: A good way to ensure that a buyer can pay for your property is by confirming that they’ve been pre-approved for a loan.

- Avoid contingencies: You should be wary of offers that include contingencies, as any unmet stipulations can enable buyers to back out of their contracts.

[download_section]

How to Tell if It’s a Buyer’s or Seller’s Market

If you’re unsure how to tell if it’s currently a buyer’s or seller’s market, there are numerous indications you can look for to gain insights into current housing conditions.

Real Estate Inventory

You can quickly determine whether your area is in a buyer’s or seller’s market by evaluating real estate availability. If you find that your region has a high housing inventory, it’s likely a buyer’s market. Fewer available properties in the area may indicate a seller’s market.

You can get the most accurate inventory estimate by dividing the number of homes currently listed on the market by the number of homes that have sold over the last month. A quotient above 7 signals a buyer’s market, while results below 5 indicate a seller’s market. Numbers in between the two are considered neutral.

Pricing

One of the clearest indications of the real estate market is current asking prices. Sellers are likely to reduce their asking prices in a buyer’s market and raise them in a seller’s market. When looking at housing prices, make sure that you’re evaluating trends rather than single occurrences to get the most accurate idea of the current market.

You can also learn about market conditions by observing interest rates. Lower mortgage interests rates enable more buyers to enter the marketplace, resulting in an influx in demand that indicates a seller’s market. Higher interest rates cause individuals to back out of the real estate market, benefitting interested buyers.

Recent Sales

Checking how much money properties sold for in recent weeks and comparing them to your home’s value is a good way to gauge the housing market. Make sure the houses you’re examining are comparable to your own, considering factors like location, size, age and number of bedrooms. Then, determine if buyers purchased them at significantly higher or lower prices than your home’s value.

If real estate commonly sold for or above the asking price, you’re in a seller’s market. Houses that sold for less than the asking price point to a buyer’s market.

Days on Market

How long a house remains on the market is a strong indicator of current real estate conditions. Houses sell very quickly in a seller’s market due to high housing demand, while they remain on the market for much longer in a buyer’s market where demand is low. You can determine which market applies to your area by monitoring listings to see how long they stay on the local market.

Market Absorption Rate

Market absorption is the number of months it would take to sell every home currently listed on the market. You can use this rate to measure real estate demand.

To calculate absorption rate, divide the number of houses sold within a given period — typically a month — by the total number of homes currently available on the market. A market absorption rate greater than 20% indicates a seller’s market, while rates below 15% point to a buyer’s market.

Is It Bad to Buy in a Seller’s Market?

Though the best time to purchase real estate is in a buyer’s market, that doesn’t mean searching for a home in a seller’s market is out of the question. If purchasing a home now makes sense for your life and you’re setting your sights on properties you can afford, the current market shouldn’t stop you from pursuing your dream home.

As long as you’re financially prepared to navigate the competitive environment and follow our suggestions for buying a house in a seller’s market, you should be able to find a property within your budget.

Navigate the Real Estate Market With Assurance Financial Today

If you’re looking to buy real estate in the current housing market, the reliable loan advisors at Assurance Financial can help. We are an independent, full-service residential mortgage banker dedicated to helping homebuyers secure the loans they need to buy the homes of their dreams. We’ve spent over 20 years conducting business with integrity and honesty at our core. You can trust us to do what’s best for you and your needs.

Apply for a home loan today!

Linked Sources

- https://fred.stlouisfed.org/series/MSPUS#

- https://bungalow.com/articles/what-is-a-buyers-market#what-causes-a-buyers-market

- https://www.forbes.com/advisor/mortgages/closing-costs/

- https://sf.curbed.com/2019/12/16/21001096/san-francisco-housing-decade-review-2010-prices-bubble-crisis

- https://www.investopedia.com/terms/a/absorption-rate.asp

- http://www.homebuyinginstitute.com/news/still-a-sellers-market-in-2021/

- https://www.ramseysolutions.com/real-estate/housing-market-forecast

- https://assurancemortgage.com/apply/

Unlinked Sources

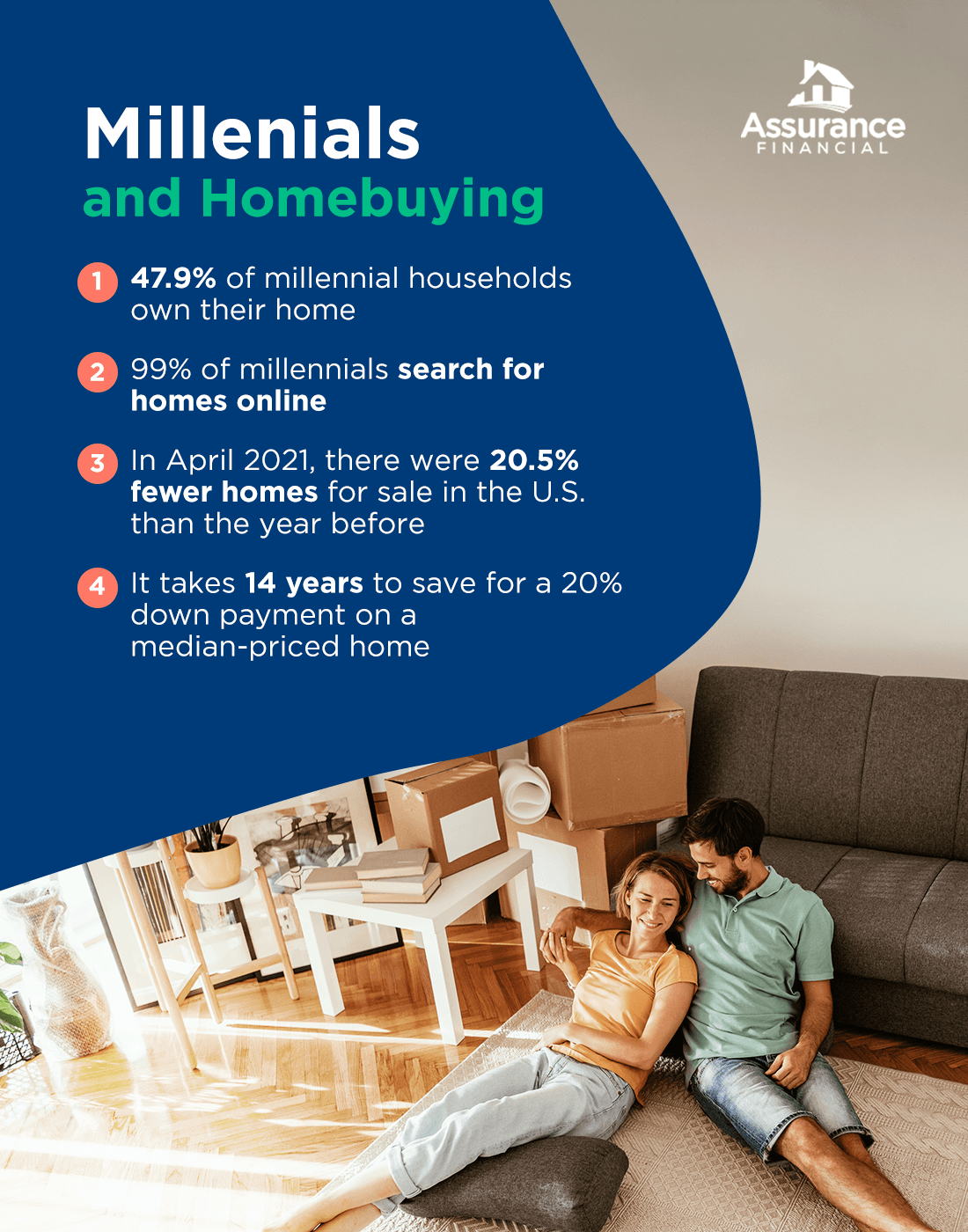

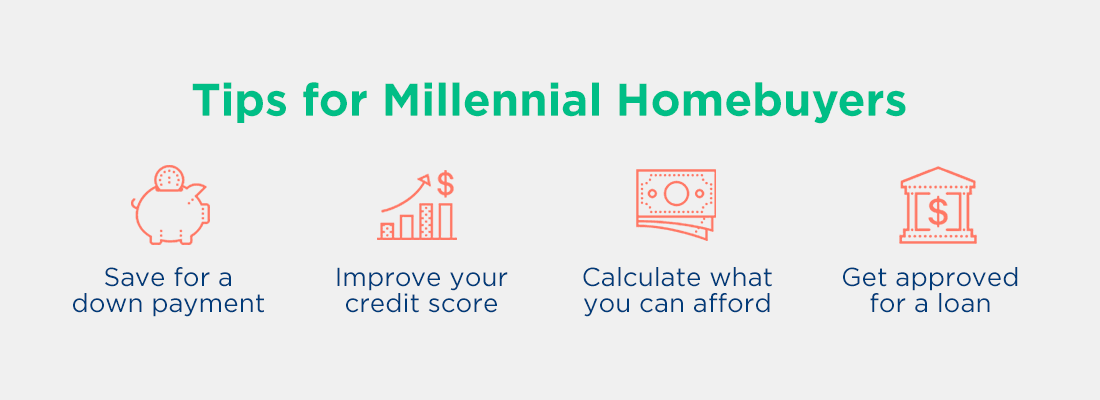

Millennials are now the nation’s largest generation. While the exact ages of “millennials” can vary from study to study, the millennial generation typically includes people born between 1981 and 1996, making them around 25-40 years old. The Pew Research Center also uses these years to define the millennial generation.

The youngest millennials are now reaching the age where they may be thinking about buying real estate. Many older millennials are wanting to buy a home if they haven’t already. Unfortunately, millennials have some unique challenges when it comes to buying a home. If you’re at this stage in life, you may have some questions.

What Percentage of Millennials Are Buying Homes?

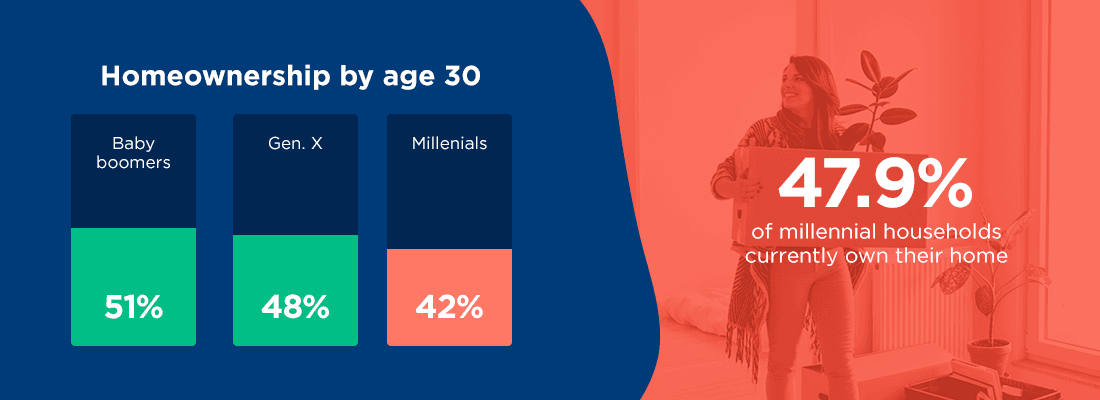

Currently, less than half of millennials own their homes. A study Apartment List published in February 2021 reported that 47.9% of millennial households own their home. This rate is below earlier generations, but it is growing as millennials increase in age.

The homeownership rate three years ago was only 40%. The current homeownership rate for Generation X is 69.1% and the rate for baby boomers is 78.8%. The millennial homeownership rate is increasing, but more slowly than it did for previous generations. Even so, millennials account for more than half of all new mortgages.

Comparing this rate another way shows that homeownership is generally decreasing. According to the 2021 Apartment List report, by age 30, millennial homeownership is only 42%. At the same age, Generation X was at 48% and baby boomers were at 51%. The previous year’s study reported that 35-year-olds in 1981 were almost 20% more likely to own their homes than 35-year-olds in 2016.

Many millennials are giving up on ever owning their own home. In 2018, 10.7% expected to rent forever. Then in 2019, the number rose to 12.3%. In 2020, the rate jumped to 18.2%. The majority of millennials cite affordability as one of the main reasons they can’t buy a home right now, but that’s not to say homeownership is unattainable. There are many loan programs designed to assist first-time homebuyers.

Why Should Millennials Buy a Home?

Buying a home has long been considered the “American Dream” and a sign of financial well-being. While some argue that millennials are killing the housing market, studies show that millennials do want to buy homes.

There are many reasons to buy a home instead of renting. Let’s go into detail about the main benefits:

1. Stability in Housing Costs

Owning your home means you’ll have more stability when it comes to your monthly housing costs. You won’t have to worry about lease terminations or rent increases. With a fixed-rate mortgage, you’ll have greater predictability in your costs year over year. While your property taxes and home insurance rates may fluctuate, the majority of your costs will not increase.

2. Forced Saving