Category: Purchasing a Home

What Is a Home Equity Line of Credit?

Homeownership comes with a wide range of benefits. One significant advantage is that you can build equity as you pay off your mortgage over time. You can leverage home equity to access cash for major purchases, alternative debt repayment, retirement plans or home renovations. You can also use it to obtain funds via a second mortgage like a home equity line of credit, or HELOC.

When you obtain a HELOC, you are securing it against your home equity value. As such, lenders may offer lower rates compared to other personal loans. At Assurance Financial, we offer HELOCs to homeowners who qualify.

What Does HELOC Mortgage Mean?

A home equity line of credit is a revolving fund source you can obtain when you have equity in your home. Your home equity is the difference between your home’s value and your current mortgage balance. For example, if your home is worth $200,000 and your current mortgage balance is $150,000, your home equity would be $50,000.

There are a few ways to build equity in your home, including refinancing, renovating, paying down your mortgage and making a sizeable down payment. Your home’s value may also increase with an upward trend in the housing market.

If you own your home and have already paid off your mortgage, you may also be able to obtain a HELOC. In this case, the HELOC will be your primary mortgage rather than a second mortgage. Like a credit card, you can access this source of funds as needed. You may have several different ways to do so, such as by writing a check, making an online transfer or using a credit card associated with your account.

A HELOC mortgage may have few or no closing costs and usually comes with a variable interest rate, though you may be able to get a fixed rate for a few years. A HELOC is not the same as a home equity loan, which is cash that comes to you in a lump sum. Homeowners are more likely to opt for a home equity loan for a one-time purchase or expense like a major renovation.

What Can You Use a HELOC For?

HELOCs are versatile because you can use yours however you want without restrictions. The following are some of the expenses you can use a HELOC for.

- Educational costs: If you want to return to college to get a degree, you can use a HELOC to cover your college expenses.

- Emergency funds: You can also use a HELOC to cover emergency expenses, such as damage to your home not covered by insurance, a medical emergency or the loss of a vehicle.

- Debt consolidation: Credit card debt can quickly become overwhelming, costing thousands every year in interest alone. You can use a HELOC to consolidate and pay off your debt.

- Home improvements: You can leverage your home equity to make improvements, such as renovating your kitchen or installing new windows. Remodeling projects are among the most popular uses of a HELOC.

How Does a Home Equity Line of Credit Work on Your House?

With a HELOC, your home equity is collateral. As such, a lender may be able to offer competitive interest rates comparable to rates for first mortgages. A HELOC will likely have an adjustable interest rate that rises and falls with market conditions. Your lender begins with an index rate to set your interest rate, and depending on your credit, will then add a markup. The better your credit, the lower your markup is likely to be. Before you sign for a HELOC, be sure to ask about this amount.

If you are still paying off your first mortgage, your HELOC will be a second mortgage, which is any type of loan borrowed against your home’s equity. You can borrow funds against your credit line whenever you want, and if you do not use funds, you will not owe interest.

You can repay all or a portion of what you draw from your line of credit each month. When you pay off the balance, you will have access to your full credit line again. For example, if you have a $40,000 line of credit and you spend $5,000, you will need to repay that $5,000 before you can access the full amount of $40,000.

If your lender does not require minimum withdrawals, a HELOC can be a source of emergency funds. For example, if you lose your job, you can take out a HELOC for extra cash as long as you have equity in your property. Your lender will specify how many years you can withdraw from your credit line while only paying back interest and how many years you have to repay the principal and interest.

There are two phases of a home equity credit line, which we’ll explain below.

Draw Period

The first stage of a HELOC is the draw period. During this phase, you can access the credit available to you as needed. You typically only need to make interest payments in the draw period. However, if you choose, you can pay extra and apply it toward the principal. In some cases, you can ask for an extension after the draw period is over. If you do not want an extension, your HELOC will move into the next stage.

Repayment

The second phase of a HELOC is the repayment period. During this stage, you cannot access additional funds. You will also be making payments of principal and interest rather than interest-only. You will continue paying until you have repaid your balance. Repayment options during this phase vary from lender to lender. Remember, payments in this stage could be much higher than they were during the draw period, so be sure to create a repayment plan and include this expense in your budget.

Do You Have to Pay Back a HELOC?

Yes, as with other forms of debt, you have to pay back a HELOC. When you repay a portion of your principal, these funds will return to your home equity line of credit. You must pay off the rest of your principal and interest during the repayment period.

Can You Repay Your Debt Early?

If you’re already making regular payments, you may want to repay your debt more quickly to pay less total interest. During the draw period, you can opt to make principal payments, even if the agreement’s terms only require you to make interest payments.

Review your budget to determine how much you can put toward repaying your HELOC each month. If you are concerned about how much interest you’ll be paying, you may want to look for opportunities to make additional payments toward the principal and lower your overall monthly payments.

Is There a Prepayment Penalty?

Some lenders charge penalties for paying off a HELOC early. Whether you want to get ahead or you’re planning to sell or refinance your home, prepayment penalties can throw your plans for a loop if you’re not expecting the charge. Before you pay back your HELOC early, be sure to ask your lender about these penalties. Typically, small amounts beyond your required monthly payment will not incur a prepayment penalty, but you should carefully review your agreement and terms before moving forward.

What Are the Advantages of a HELOC?

If you qualify for a HELOC, there are a few reasons you may want to apply for this line of credit. The following are some of the advantages of a HELOC.

- Skip the fees: While credit cards tend to charge cash advance fees, you likely won’t have these when you draw funds from your HELOC. If a lender charges a fee every time you draw money, you may want to look for another lender.

- Improve your credit: Two factors that affect your credit score are your credit mix and payment history. You can increase your credit score by securing different types of credit — such as loans and credit cards — and making consistent, on-time payments. Obtaining a HELOC may boost your score if you steadily pay off the loan.

- Get a low interest rate: Even when mortgage interest rates are higher, a HELOC typically has a lower rate. HELOCs often come with adjustable interest rates, and though these can fluctuate, there are limits on how much the rate can rise while you have your loan.

- Pay lower initial costs: Similarly, HELOCs tend to come with lower initial costs than credit cards. That makes a HELOC ideal for ongoing projects or debt consolidation.

- Get a higher credit limit: You can likely get a much more generous credit line from a HELOC than from a credit card. Remember, the amount you can receive depends on the equity in your home and your credit score.

- Convert to a fixed rate: You may be able to convert your adjustable interest rate to a fixed rate, which can make your payment and interest rate more consistent and predictable. Though this may happen automatically when your HELOC enters the repayment phase, you may be able to convert it to a fixed rate earlier.

- Pay low or no closing costs: While you likely have to pay closing costs for your first mortgage, when you get a HELOC, you may not have to pay any at all if you have good credit. Any required closing or appraisal costs are likely to be low.

- Borrow the funds you need: With a HELOC, you’ll use the funds you need when you need them. You can borrow cash as you go, and if you eventually need less than you anticipated, you will pay a lower monthly payment. This flexibility is one significant advantage for borrowers who apply for a HELOC.

- Use the funds as you see fit: A HELOC imposes few restrictions on how borrowers can use the loan. Though many homeowners renovate or update their properties, you don’t have to. You can put the money toward various expenses, such as travel, higher education or debt consolidation.

- Deduct interest on your taxes: According to the IRS, you can deduct interest payments if you use your HELOC to substantially improve, build or buy the home that secures your loan. There is a limit on how much you can deduct, combined with the interest on your first mortgage.

- Enjoy flexible options for repayment: Many HELOCs come with flexible repayment options, including the timeline and interest-only payments versus payments that include principal and interest. Your timeline for repayment can vary depending on your lender and the amount you borrow. You can likely make additional payments to lower your remaining balance.

What Are the Disadvantages of Home Equity Lines of Credit?

While there are many advantages to securing a HELOC, you may want to consider some drawbacks before you apply.

- Fees: While lenders make money from the interest you pay, you may also owe some fees, such as an annual fee, transaction fee, appraisal fee or a fee if you refinance or cancel your HELOC before the end of the draw period. Some lenders may also charge fees if you do not borrow a specific amount or maintain a given loan balance. Be sure to review these fees before moving forward with a HELOC.

- Upfront costs: Some lenders charge upfront costs to get a HELOC, such as an application fee, home appraisal, title search and real estate attorney fees. Consider these to determine whether a HELOC is the right option for you.

- Loss of equity: With a HELOC, you borrow against your home equity. If your home’s value drops with a dip in the housing market, you could owe more than your property is worth. When you have an outstanding HELOC, you may also be ineligible for other opportunities to borrow against your home’s equity.

- Payment increase: While the low payment during the draw period can be tempting, your minimum monthly payment will increase in your repayment period to include principal and interest. To avoid an unwelcome surprise, plan for your monthly payment to go from a small sum to hundreds of dollars.

- Limited draw period: Every HELOC has a draw period, which is the only time you can draw funds. After this phase, you will need to repay your HELOC.

- Variable interest rate: A HELOC often comes with a variable rate, so it can rise or fall depending on the market. Even if the HELOC has a low interest rate when you obtain it, that could go up when your HELOC enters the repayment period.

- Risk of overspending: Though overspending is not an inherent disadvantage of HELOCs themselves, you should be aware of the risk. Since you only need to make interest-only payments in the draw period, you can easily access more cash than needed, which could lead to financial ramifications.

- Minimum withdrawals: Some HELOCs may come with minimum withdrawal requirements, which means you’ll need to borrow a specific amount and keep your credit line open for a given period.

- Use of your home as collateral: Since you are using your home as collateral, you risk losing the house if you can’t repay your HELOC. That’s why it’s wise to only use a HELOC to increase your emergency funds or cover expenses that can help you accumulate wealth, such as home renovations and improvements.

If your income is not stable and you can’t make your monthly payments, a HELOC may not be the right option for you. Additionally, if you aren’t looking to borrow a large amount of money, you may want to opt for a low-interest credit card instead.

How Do I Get an Equity Line of Credit?

Once you’ve decided you want to obtain a HELOC, begin the application process. Follow the steps below to get an equity line of credit.

- Ensure you have sufficient home equity: Use a HELOC calculator or discuss your situation with our team at Assurance Financial to determine whether you have enough equity in your home to qualify for a HELOC.

- Review your credit score: You may be more likely to get approved for a HELOC and qualify for a better interest rate if you have a higher credit score. If you want to improve your credit score before you apply, you can plan to pay off some of your debts and make on-time payments. You can also review your credit report to ensure there are no errors you need to dispute.

- Speak to several lenders: Shop around at several lenders to make sure you can get the best terms and rate. Research lenders and ask about pre-qualification offers that may be available to you. At Assurance Financial, we offer historically low rates.

- Collect your application materials: Once you find your lender, you will need to provide your application materials — such as your identification, employment and salary information — plus your estimated home value and your outstanding mortgage balance.

- Provide verification documents: After you accept a HELOC offer, you will need documentation to verify the information you have provided. This paperwork may include tax returns, W-2s or pay stubs. The lender may also require an appraisal for your home and will complete a hard credit check, which will temporarily affect your credit score.

- Wait through the underwriting process: As with your first mortgage, you will have to wait for the underwriting process. For a HELOC, the underwriting is less extensive.

- Receive your funds: Finally, you will sign your paperwork and receive your money, which you can then start drawing from. The amount of time between approval and funds disbursement will depend on your lender.

Apply for a HELOC Loan With Assurance Financial Today

When you apply for a HELOC loan with Assurance Financial, we only need your asset information, proof of income, two most recent tax returns, proof of identification and credit score. We can review your application faster when you use our secure bank connector, and you can take a simple snapshot of a pay stub as proof of income. On the other hand, if your employer uses ADP, all you’ll need is your payroll login.

Contact us at Assurance Financial if you want to learn more about getting a HELOC or apply for a HELOC loan with Abby, our virtual assistant that can help guide you through the loan process.

Potential homebuyers, especially first-time homebuyers, often wonder how much money they should save to purchase a home. There are a number of costs associated with the process, including a down payment and closing costs. Fortunately, 100% financing options are available for home loans that may allow you to purchase a home with no money down. If you are looking for a home loan with 100% financing, meaning a home loan that doesn’t require a down payment, we cover what you need to know.

What Is a 100% Financing Home Loan?

A 100% financing home loan is a type of mortgage loan that allows you to finance the entire purchase price of a home without making a down payment. With this type of loan, you don’t need to put any money down, which can make it easier for you to purchase a home if you do not have a large amount of savings or want to keep your savings for other purposes.

There are a few different types of 100% financing home loans available, including United States Department of Agriculture (USDA) loans and Veterans Affairs (VA) loans. These loans are backed by the government and are designed to help make homeownership more affordable and accessible to a wider range of people.

While a 100% financing home loan may appeal to some borrowers, this option may also come with higher interest rates and fees. Carefully consider your options and work with a reputable lender to ensure you are getting the fairest loan terms possible.

What Options Are Available for No Money Down Home Loans?

There are two government-backed home loan options that do not require a down payment — a USDA loan and a VA loan.

USDA Home Loan

This type of mortgage loan is guaranteed by the United States Department of Agriculture (USDA). A USDA home loan is designed to help low- to moderate-income borrowers in rural areas purchase a home or make home repairs. USDA loans typically offer favorable terms, including low-interest rates and zero down payment requirements. They are also available to borrowers with lower credit scores than other types of loans.

To qualify for a USDA loan, the property you plan to purchase or renovate may need to be located in a designated rural or suburban area as defined by the USDA. Additionally, you may need to meet certain income limits based on the area you are buying in and your household size. USDA loans are administered by approved lenders, and since the USDA guarantees these loans, lenders are protected from losses if you default on your loan.

VA Home Loan

This type of mortgage loan is guaranteed by the U.S. Department of Veterans Affairs (VA). A VA loan is designed to help current and former members of the U.S. military and their qualifying surviving spouses buy or refinance a home. VA loans typically offer favorable terms, such as no down payment requirement and no private mortgage insurance requirements, making them an attractive option for eligible borrowers.

To qualify for a VA loan, you may need to obtain a Certificate of Eligibility (COE) from the VA. The COE verifies that you meet the VA’s service requirements and are eligible for the loan. Like USDA loans, VA loans are administered by approved lenders, and the guarantee from the VA protects lenders from losses if you default on the loan.

Benefits of 100% Financing for Home Loans

Receiving 100% financing for home loans, also known as zero-down payment loans, can offer you several benefits. The following are some of the potential benefits:

- Increased flexibility: If you have saved up a down payment, you can use these funds for other expenses, such as home renovations, moving costs or emergency expenses.

- No down payment required: With 100% financing, you are not required to come up with a large down payment to purchase a home, which can be a significant financial burden.

- Faster path to homeownership: With 100% financing, you can achieve your dream of homeownership sooner.

- Affordable monthly payments: With no down payment, the loan amount is higher, but the monthly payments may still be manageable, especially with competitive interest rates.

100% financing may not be available for all types of home loans, and we recommend that you carefully consider the terms and conditions of any loan before making a decision. Additionally, you may be required to have strong credit scores and income to qualify for this type of loan.

How to Buy a House With No Money Down

Buying a house with no money down is possible, but it may require careful planning and a good understanding of your options. The following are some potential ways you can buy a house with no money down:

- Gift funds: If you have friends or family who are willing to help you purchase a home, they can give you a monetary gift that you can use as a down payment.

- Negotiate with the seller: In some cases, you may be able to negotiate with the seller to cover some or all of the down payment as part of the sale agreement.

- Apply for a VA loan or USDA loan: If you are a current or former member of the U.S. military or a qualifying surviving spouse, you may be eligible for a VA loan, which requires no down payment. If you are looking to buy a home in a rural area, you may be eligible for a USDA loan, which also requires no down payment.

- Down payment assistance programs: Some state and local governments offer down payment assistance programs to help you buy a home with little or no down payment if you are a low- to moderate-income earner.

Keep in mind that even if you are able to buy a house with no money down, you may still be responsible for other costs associated with the home purchase, such as closing costs and appraisal fees. Carefully consider all of your options and speak with a qualified mortgage professional to help you navigate the homebuying process.

What if I Don’t Qualify for 100% Financing for a Home Loan?

If you don’t qualify for 100% financing for a home loan, you may have some other options, such as applying for a conventional loan, applying for an FHA loan, applying for down payment assistance, applying for closing cost assistance or saving for a down payment.

Apply for a Conventional Loan

This type of mortgage loan is not guaranteed or insured by a government agency like the U.S. Department of Veterans Affairs (VA) or the Federal Housing Administration (FHA). Conventional loans are backed instead by private lenders and investors. Typically, conventional loans come with stricter credit and income requirements than government-backed loans. They are often a good option for borrowers who have good credit scores and sufficient income to qualify for a loan.

Conventional loans can be conforming or nonconforming. Conforming loans are those that meet the guidelines set by Fannie Mae and Freddie Mac, the two government-sponsored enterprises that buy and sell mortgage loans. Nonconforming loans, also known as jumbo loans, exceed the conforming loan limits set by Fannie Mae and Freddie Mac.

Conventional loans typically require a down payment of at least 3% of the purchase price, although some lenders may want a larger down payment depending on your credit score and other factors. You may also be required to pay private mortgage insurance (PMI) if you make a down payment of less than 20%. Conventional loans are a popular option for homebuyers who meet the credit and income requirements and want to avoid the mortgage insurance requirements of government-backed loans.

Apply for an FHA Loan

This type of mortgage loan is backed by the Federal Housing Administration (FHA), a government agency that belongs to the Department of Housing and Urban Development (HUD). An FHA loan is designed to help lower-income and first-time homebuyers who may have difficulty qualifying for a conventional mortgage loan. The FHA insures the loan, which means that if you default on the loan, the lender is protected against losses.

FHA loans typically have more lenient credit and income requirements than conventional loans, and they may require a lower down payment. The down payment for an FHA loan can be as low as 3.5% of the purchase price, although you may be required to make a down payment of at least 10% if your credit score is lower than 580.

One of the key benefits of an FHA loan is that it allows you to qualify for a loan with a lower credit score than would typically be required for a conventional loan. Additionally, FHA loans may offer lower interest rates and more flexible repayment terms than conventional loans. However, FHA loans may also require you to pay an upfront mortgage insurance premium (MIP), as well as an annual MIP that is added to the monthly mortgage payment. The MIP is used to fund the FHA loan program and protect lenders against losses.

Apply for Down Payment Assistance

Down payment assistance (DPA) is a type of financial assistance that is designed to help homebuyers cover the upfront costs associated with purchasing a home, specifically the down payment and closing costs. Down payment assistance programs are often administered by state and local housing agencies and nonprofit organizations.

Down payment assistance can take many forms, such as grants, loans or forgivable loans. The funds can be used to cover all or a portion of the down payment and closing costs, depending on the program’s guidelines and your qualifications. DPA programs are typically targeted at low-income homebuyers and first-time homebuyers who may struggle to save for a down payment. They can also be available to certain groups, such as first-time homebuyers, veterans or teachers.

The goal of down payment assistance is to make homeownership more accessible and affordable to a wider range of people. By reducing the upfront costs of buying a home, DPA programs can help you get into a home faster and with less financial strain. Down payment assistance programs may have specific requirements and qualifications that you may need to meet to be eligible. Carefully review the guidelines of any DPA program you are considering to ensure that you meet the qualifications and understand the terms of the assistance.

Apply for Closing Cost Assistance

Closing cost assistance is a type of financial assistance that can help you cover the closing costs associated with purchasing a home. Closing costs are expenses that are incurred during the homebuying process, such as lender fees, appraisal fees and title fees. Closing cost assistance programs are often administered by state and local housing agencies and nonprofit organizations. The assistance can be used to cover some or all of the closing costs.

Closing cost assistance is typically targeted at low- to moderate-income homebuyers who may struggle to cover the upfront costs of buying a home to make homeownership more accessible and affordable. Check if there are any closing cost assistance programs available in your area.

Save for a Down Payment

Trying to save for a down payment on a home can be a significant challenge, especially if you’re starting from scratch. However, there are several strategies that can help you save money more effectively and reach your down payment goal faster, such as:

- Reduce debt: Pay off high-interest debt, such as credit cards, as quickly as possible. This will free up more money for savings.

- Create a budget: Make a budget that takes into account your income and expenses and look for areas where you can cut back on spending. Consider reducing discretionary expenses like eating out, entertainment and subscriptions.

- Set a savings goal: Determine how much you need to save for a down payment and set a specific savings goal. This will help you track your progress and stay motivated.

- Consider a side hustle: Look for ways to earn extra income, such as freelancing, tutoring or selling items you no longer need. Put this extra income directly into your down payment savings account.

- Automate your savings: Set up automatic transfers from your checking account to a savings account each month. This will help you save money consistently and avoid the temptation to spend it elsewhere.

Saving for a down payment can take time and discipline, but if you don’t qualify for 100% financing, this can be an important step toward achieving homeownership.

Where to Start

Every homebuyer has different needs, which is why we offer so many different home loan options at Assurance Financial. We can help regardless of your life stage or homebuying goal, whether you are:

- First-time homebuyers.

- Vacation homebuyers.

- Experienced homebuyers.

- Self-employed homebuyers.

We can also assist if you’re downsizing your home, remodeling or building a home, or investing in real estate. Use a 100% financing mortgage calculator to determine how this mortgage may impact your finances.

Apply for a Loan Today With Assurance Financial

At Assurance Financial, we have been servicing the loan industry since 2001. We combine superior customer service with technology-focused solutions to bring you the most seamless homebuying experience possible. We handle the entire home loan process in-house, so you can rest assured that the process will go smoothly. If you are seeking 100% financing for a conventional loan or another type of home loan, apply for a loan with us at Assurance Financial today.

Key Takeaways

- In a seller’s market, buyers face significant disadvantages and have limited leverage to negotiate for concessions, contingencies, or repairs, requiring focus on what matters most.

- Getting pre-qualified for a home loan is essential to demonstrate you’re a serious buyer capable of securing financing for a specific amount.

- Strategic planning and financial readiness are critical to compete effectively with other buyers in competitive markets.

During home shopping, most homebuyers want to know whether the current housing market is a seller’s market or a buyer’s market, along with how to get a good deal in a seller’s market. Though certain seasons tend to be busier, fluctuations in the housing market are more likely influenced by supply and demand than the season. As such, it’s essential for buyers to be aware of the state of the housing market and whether the area is currently experiencing a seller’s market or a buyer’s market.

To help you navigate the homebuying process, we cover how to identify whether you’re shopping in a buyer’s or seller’s market, what the current housing market is in 2024 and how to negotiate buying a house in a seller’s market.

Buyer’s vs. Seller’s Market

The housing market is either a buyer’s market or a seller’s market. These terms mean that the market either favors buyers or sellers.

What Is a Buyer’s Market?

When the supply of properties exceeds demand, this is known as a buyer’s market. When many homes are available for purchase yet there is a low number of interested buyers, buyers have an advantage. A buyer has leverage over the seller because there is less competition over a home.

In a buyer’s market, homes are on the market for longer periods and real estate prices drop. Essentially, sellers are competing with one another to attract buyers. A seller may be forced to drop their asking price to make the sale, and they may be more open to negotiating offers.

When you’re home shopping, a buyer’s market is the ideal time to buy. You can take your time, visit as many homes as you want before making an offer and negotiate with the seller to bring the price down. In a buyer’s market, sellers need to make repairs, market their property and price it competitively.

What Is a Seller’s Market?

On the other hand, when demand for homes exceeds supply, this is known as a seller’s market. Though many individuals are interested in purchasing a home, the inventory of available properties is low. Sellers have an advantage in this housing market since the lack of available homes creates more competition among buyers. Homes sell more quickly in a seller’s market, and because buyers are competing over the same properties, sellers can increase asking prices.

With this price increase, buyers may need to be willing to spend a greater amount of money on a property. When there are many parties interested in a home, buyers rarely have negotiating power and may need to accept a property as-is. A housing shortage can lead to a bidding war, and the competing offers can drive the price above the seller’s asking price. Sellers can take time to carefully consider their offers and only consider pre-qualified buyers.

Even though sellers have an advantage in a seller’s market, you can still succeed as a homebuyer and find the home of your dreams in this market.

Signs of a Seller’s Market

Before you start home shopping, you may want to determine whether your local area is currently experiencing a seller’s market or a buyer’s market. The following are some signs of a seller’s market:

- Lack of price cuts: Sellers are more likely to drop their asking prices in a buyer’s market, so several price cuts to listed homes could indicate a buyer’s market. On the other hand, a lack of price cuts can indicate a seller’s market. Keep in mind, however, that sellers can have unrealistic expectations about the value of their properties, so look for a trend in pricing rather than a single occurrence.

- Sales over asking price: Check the recent sales of the property you’re interested in and homes comparable to it. If homes have usually been selling above the asking price, this may indicate a seller’s market. Homes selling below the asking price, on the other hand, may indicate a buyer’s market.

- Bidding wars: A bidding war occurs when multiple buyers present competing offers for the same property. Buyers attempt to outbid each other by gradually increasing their offer. If you keep getting into bidding wars or you know friends or family who are home shopping and getting caught in bidding wars, this could indicate that the housing market is currently a seller’s market.

- Market trends: One of the strongest indicators of the current housing market is determining whether home prices in your area have been decreasing or increasing. Look at market trend reports to review the homes in your local area to get information on the median sale price, the number of properties on the market and how the numbers have changed during the last year. Increasing prices and decreasing inventory often indicate a seller’s market.

- Shorter time on the market: How long a home sits on the market is another factor that could indicate whether the housing market is currently a seller’s or buyer’s market. In a seller’s market, homes sell faster than in a buyer’s market. So if you notice a lot of quick sales, this could indicate a seller’s market.

- Fewer houses on the market: Consider the homes currently for sale. If the inventory is large, your local area may be in a buyer’s market. However, if the inventory is limited, then your local area may be in a seller’s market. Divide the number of properties for sale by the number of properties that were purchased in the past month. If you come up with a low number, this could indicate a seller’s market.

Is It a Buyer’s or Seller’s Market in 2024?

The current housing market is a seller’s market. The pandemic has had a dramatic impact on the housing market and ushered in new rules and processes, such as virtual open houses and tours.

The typical seasonality of home buying has changed in the past couple of years. While spring and summer used to be the height of the home buying season and turn to a seller’s market, the pandemic has led to a highly competitive seller’s market that has endured and made buying a home challenging, even during the slower winter season.

Current Trends in the Housing Market

Keep the following trends in mind if you are buying in the current seller’s market:

Virtual Home Tours

Many real estate agents are conducting virtual tours and walkthroughs as the buyer’s first view of the home. As a buyer, you may encounter everything from a simple video walkthrough to a more immersive experience with 3D technology.

A virtual tour can save you time that you would’ve otherwise spent traveling to and from the property, especially if you looking to buy in a different city or state. Before the virtual home tour, make sure you download the appropriate app, charge your device and have a good internet connection. You should also ensure you’re in a quiet place where you can hear the real estate agent.

Take advantage of this opportunity to view the home virtually by asking the agent to zoom in on certain areas, open closet doors and describe specific features.

Increased Buying Activity

Buyers are showing continued interest in purchasing properties, even as mortgage rates and home prices steadily rise. While the number of homes for sale on the market hit a record low, sales and median home listing prices shot up.

A slight majority of buyers have owned a home previously, and those that have been renting before buying cite the desire to own a home as their decision for buying. Others want a larger property or want to move to be closer to family or friends.

Bids Above the Asking Price

With so many competitive buyers bidding on homes, many offers are coming in above the asking price. As we approach the spring and summer seasons, this flurry of homebuying activity is likely to only get more hectic. Buyers have been lining up to purchase homes for months, even in the winter, which has led to an unusually low real estate inventory and greater competition over homes.

This increase in demand drives up prices, and other buyers are likely to put in offers on the same property, so if you want to get your dream home, you may have to place a bid above the asking price.

How To Buy a House in a Seller’s Market

If you want to buy now, in a seller’s market, you should know how to navigate this housing market and get a good deal even when there is a limited supply of homes. Though you probably shouldn’t expect to negotiate for repairs or convince a seller to accept less than their asking price, you can utilize some methods and strategies to successfully compete in this ultra-competitive housing market. Follow these tips for buying in a seller’s market:

1. Be Aware of the Current Market

While home shopping and making an offer, keep in mind what kind of housing market you’re shopping in and know that you are at a disadvantage. In a seller’s market, you may not have the leverage to push for concessions, contingencies, repairs or a strict closing date. Be sure to focus on what matters most to you, and consider whether the stipulations you want to be included in the contract are worth losing the home over.

2. Get Pre-Qualified for a Home Loan

Getting pre-qualified for a mortgage means a lender is willing to lend you a certain amount for the purchase of a home. Though this isn’t a guarantee of a mortgage, it gives you a maximum loan amount to work with. Many sellers only want to consider offers from pre-qualified buyers, especially in a seller’s market. Apply to get pre-qualified with Assurance Financial when you’re ready.

[download_section]

3. Get Pre-Approved for a Mortgage

After getting pre-qualified, your next step is getting pre-approved for a mortgage. A pre-approval is based on an analysis of your finances. The pre-approval offers a more concrete number for a loan amount. The lender will review your completed mortgage application and conduct a credit check. Though pre-approval is also not a guarantee of a mortgage, it’s a more accurate estimate than pre-qualification.

4. Work With a Real Estate Agent

Whether you’re buying in a seller’s market or a buyer’s market, working with a real estate agent can ensure you navigate the current housing market successfully. Real estate agents can give you an advantage over other competitive buyers, as they have the skills and knowledge you need on your side. Real estate agents may also have connections allowing them to identify and view homes before they’re even on the market or before the final bids are considered.

To choose the right real estate agent, read their reviews, find out what their experience is and speak with buyers they’ve worked with. After you narrow down your list to a few options, there are a few important questions you can ask to choose the right agent for you:

- What are your fees?

- How familiar are you with this area?

- What’s the most difficult deal you facilitated?

- Do you have access to properties that aren’t listed yet?

- How can you strengthen my offer in a competitive seller’s market?

Your real estate agent can help you strengthen your offer by looking beyond price. Consider what else the seller values to give you an advantage, such as conveniences or contingencies. For example, if you can close earlier or you don’t need to move immediately and can give the seller more time to find their next home, this could give you an advantage when the seller is considering their offers.

5. Have Your Down Payment Ready

Be sure to save up enough for a down payment. If someone is giving you the money for your down payment in the form of a gift, discuss this process with your lender. The person giving you this money may need to write a gift letter that explains you don’t need to repay the money. Many lenders will also want to see the bank statements from the account with your down payment funds, and they may want to see that the funds have been in the account for a couple of months.

6. Look at Homes Under Budget

In a seller’s market, many sellers receive multiple offers on their homes. As a buyer in a seller’s market, you should look for homes that fall below your spending limit. Other buyers are likely to bid higher than the asking price, so you want to look at homes on which you can afford to bid higher than the asking price. With this strategy, you can afford to bid up without exceeding your comfortable spending limit or needing to dip into your savings.

7. Act Quickly

When you find your dream home in a seller’s market, it’s important to act quickly. Hesitating to make an offer on a home you know you love and want to purchase may mean losing your dream home. By the time you make your offer, the home may no longer be available. Ensure you get preapproved for a home loan before you start shopping so you can make an offer immediately.

8. Stay Patient

In a competitive seller’s market, it’s normal to lose out on homes you’re interested in. Try not to get discouraged, and stay patient. Inexperienced buyers could get frustrated, find themselves caught up in a bidding war and offer more on a home than they’re comfortable spending or more than the property is actually worth.

Keep in mind, though, that you don’t have to give up as soon as you sense someone could outbid you or has an all-cash offer. Deals fall through all the time, as your real estate agent can attest, so being the second-choice offer can still work out in your favor.

9. Widen Your Search

The most popular neighborhoods understandably come at the highest prices. If you want to own a home in a specific ZIP code but homes in the area are not within your budget, you may want to consider widening your search. Identify what you like about this neighborhood, such as the school, parks, public transportation or local businesses and restaurants. Once you determine what features you want in your neighborhood, you can try to find them in locations you haven’t explored or considered before.

10. Avoid Settling

When a homebuyer grows tired of losing out on homes, they may make an offer on a home they wouldn’t be interested in otherwise. Try to avoid this situation, and keep in mind that purchasing a property is a huge, long-term investment. You may be living in and paying for this home for decades, so don’t settle for a home you don’t love unless you need to move immediately.

Similarly, try to avoid fixating on the first home you fall in love with. This can lead to a huge disappointment, or even worse, a bad financial decision made during a moment of desperation.

Contact Us at Assurance Financial to Learn More

As a mortgage lender, Assurance Financial is a home loan expert. We want to help you realize your dreams of owning a home, and our team can assist you through every step of the process, regardless of whether you want to buy a starter home or a vacation home. You have several different loan options for your mortgage, including conventional loans, FHA loans, VA loans and jumbo loans.

With our financial mortgage services, we can offer you a customized option for paying for your home. Contact us at Assurance Financial to learn more about how to find a house in a seller’s market and get the mortgage loan option that’s right for you.

Every year, your family enjoys a getaway in the mountains, at the beach or in a cabin in the woods. And, every year, you wonder if it’s finally time to buy a vacation property.

If you already have a primary residence, purchasing a second home can be an excellent investment. You have a guaranteed vacation spot each year and can rent the house out to bring in some extra income.

The process of buying a vacation home has some things in common with buying your first house. You want to put as much time and effort into finding your dream vacation spot as you did in finding the place you call home. There are a few differences between a vacation property and your primary home when it comes to financing a second property.

Why Buy a Vacation Home?

Buying a vacation home can make good financial sense for a few reasons. One reason is that it sets you up with a vacation spot for as long as you own the home. When you already own your vacation spot, you don’t have to pay for travel expenses such as hotels or rentals anymore, which can save you money over time.

Another reason is that buying a vacation home can give you a source of passive income. You can rent the home out to others when you’re not using it. Renting the property out can help you cover the cost of the mortgage or give you a little extra spending money.

Some people like to buy a property to use as a vacation home now and then move into the property full-time after they retire. If you dream of retiring to the beach or mountains, owning a property already gets you one step closer to achieving that dream.

Finally, you can look at a vacation home as an investment. Over time, the value of the home will likely increase. When your family is no longer interested in vacationing there, you can sell the property or continue to rent it out, generating an ongoing source of income.

Important Questions to Ask Before You Purchase a Vacation Home

Before you start the process of purchasing a vacation home, carefully weigh the pros and cons and ask yourself a few questions to make sure it’s the right option for you.

What’s Your Vacation Style?

Everyone has different vacation styles. Some people prefer to visit the same area yearly, such as the beach, woods or mountains. They like to build up traditions and enjoy the familiarity of staying in the same place.

Others prefer to see the entire world. They might spend a few weeks at the beach one summer, then head off to Europe for a backpacking vacation the next. These people prefer a varied, diverse vacation scene. They choose to visit all the popular vacation spots rather than stay in the same place.

If your vacation style is similar to the first one and you like to go to the same area every year, then buying a second home in that area can make sense. You won’t have to hunt around for a hotel or home rental every time you want to travel. If your style is closer to the second one, purchasing a vacation home might not be the best option for you at the moment.

Buying a vacation home can also make sense if you prefer to take longer vacations or if you want to go away several times during the year. When you own the property, you can easily spend a month or longer there. You can also visit whenever you want, provided you haven’t rented the space out.

Can You Afford a Second Home?

Two residences means two mortgage payments and two sets of property taxes. Buying a second property can stretch your budget depending on your current income and obligations.

Here’s what to look at when deciding whether a second home will work with your budget:

- Your current savings: Ideally, buying a second home won’t keep you from saving for retirement and other goals, such as your kids’ education. If you’re behind on saving for those milestones, waiting to purchase a second home can make sense.

- Your current mortgage: If you’ve nearly already paid off your mortgage, you may have the wiggle room in your budget to buy a second home. Similarly, if you have a lot of equity in your primary residence, you can borrow against it to buy a vacation home.

- Your income: You might have high expenses, such as a big mortgage payment, but at the same time, your income might be high enough to allow you to buy a second home without derailing your other financial goals.

Keep in mind that the cost of a vacation home can vary considerably based on location and size. If you’re comfortable buying a small property in a less popular vacation area, you might get a better price than if you purchased a home in a busier spot or wanted to buy a larger property.

Can You Rent Out the Home?

Unless you decide to make it your primary residence, a vacation home can provide a steady supplemental income stream. You can rent out the property during the weeks you don’t use it or during the low season to bring in some extra cash or help pay down the mortgage.

You’ll want to consider a few factors before you decide to rent out a vacation home, though. While renting the property out can help you pay down the mortgage, you might not want to rely on rental income to cover the second mortgage since you might not rent the property out enough to cover the costs.

Also, consider the effort involved in renting the property. If the vacation home is a considerable distance from your primary home, it can make sense to hire a property management company that’s closer to it. You want someone to be available to respond to the renters’ issues and take care of repairs as needed.

Who Will Take Care of the Home?

Similarly, it’s essential to think about who will care for the vacation home. Houses need regular upkeep. Otherwise, you might spend the first part of your vacation mowing the lawn or fixing leaking pipes.

A property management company can look after the house if you plan on renting it out. The management company charges you for its services and any repairs.

Another option is to hire a housekeeper or groundskeeper to look in on the property and take care of things as needed when you’re not there. The housekeeper can visit weekly during the off-season or when the home is unoccupied to ensure everything’s fine and clean surfaces or the exterior as needed. If you rent the home, the housekeeper can clean it between rentals.

What Are Property Taxes?

Along with paying for the property itself, buying a second home means paying another set of property taxes. Tax rates vary considerably based on location. It’s a good idea to look at taxes before you decide on an area.

The taxes in your dream spot might make owning a home there impractical. However, the taxes in the next town over or in a neighboring vacation locale might be much more reasonable.

How Will You Pay for the Home?

You have a few options for paying for your vacation home. If you have savings, you might pay for it in full, in cash. Another option is to refinance the mortgage on your primary home and use the proceeds from that to pay for a second home.

You can also take out a second mortgage, if you have the credit, a down payment and can afford the additional monthly mortgage payment. You might want to use the rental income from the property to cover the mortgage cost. A more reliable option is to ensure you can afford the mortgage without renting the property out. That way, you’ll always be able to pay the mortgage, even if no one is renting your vacation home.

Does Owning a Second Home Affect Your Taxes?

Buying a second home affects your taxes in a few ways. First, if you rent the property out, you’ll need to declare the rental income when you file your taxes. You might also be able to deduct expenses related to the rental, provided you meet the 14-day rule, meaning you don’t use it as a residence for more than two weeks or 10% of the number of days you rent it out.

Owning a second home can mean you can deduct the interest you pay on the mortgage, provided the total value of both mortgages is less than $750,000. You can deduct property taxes, too.

Benefits of Owning a Vacation Home

If it works for your budget, there are definite benefits to owning a vacation home:

- Better vacations: When you own a vacation property, your holidays can be longer and more affordable. Instead of spending $100 or $200 per night on a hotel or rental home, you’re building equity in your vacation property when you own the house. If you work remotely, you can easily spend the entire summer at your vacation home.

- You can swap: Owning a vacation property doesn’t limit your vacations to one geographic area. You might also sign up for a home exchange program that lets you swap homes with other vacation homeowners, giving you some variety.

- Additional income stream: Your vacation property can create an additional revenue stream for you, helping you build up a solid financial cushion. Just be sure to balance the cost of managing a rental property and the other tax responsibilities with the income it brings in.

- Improved quality of life: Owning your vacation spot can mean you see an improvement in your quality of life. If you’ve had a rough week at work, you can dash off to your cabin in the woods or your home by the shore for some much-needed relaxation.

- Greater financial security: A vacation home can be an investment that leads to greater financial security. You can sell the property later and enjoy a decent return on it. You can also use it as your primary home in retirement or pass it on to your children.

- Tax breaks: Owning two homes can mean more tax deductions, which can lower your tax bill and help you save more money.

How to Pay For a Vacation Home

If you’re not going to pay cash for your second home, you have a few options for financing a vacation property.

1. Cash-Out Refinancing

You can refinance your primary mortgage to either pay for your second home or come up with a down payment for your vacation home. When you apply for a cash-out refinance, you replace your existing mortgage with a larger one. The amount you can borrow is based on the market value of your home.

Here’s an example. You purchased your first home 15 years ago for $150,000. You still have about $30,000 left on the principal. Since then, the home’s value has increased to $350,000. The vacation home you’re interested in purchasing costs $175,000. You decide to refinance your home, borrowing 80% of its current value ($280,000).

Since the amount you’re borrowing is more than you owe on the mortgage, you receive $250,000 in cash. You can then use that cash to purchase your vacation home.

A cash-out refinance might not always provide you with enough to cover the entire cost of a second home. For example, if the value of your home hasn’t increased by much since you bought it, you might not have enough equity in your home to get that much cash when you refinance. Instead, you might be able to get enough money to cover the down payment then apply for a mortgage on the vacation home.

There are some things to consider before you refinance. One is the cost of the refinance. You’ll have to pay closing costs when you refinance, which can be several thousand dollars.

Another is the interest rate on the refinanced loan. Interest rates are still pretty low but might not be lower than what you’re currently paying, based on when you took out your first mortgage. You might end up with a higher rate than you started with, which means you’ll spend more on your mortgage over time.

2. Home Equity Loan

Another way to tap into your primary home’s equity and use it to buy a second home is through a home equity loan. While a refinance replaces an existing mortgage with a new one, a home equity loan is a second loan in addition to your mortgage.

The loan size depends on the amount of equity in your primary home. For example, if your home is currently valued at $300,000 and you owe $150,000 on your mortgage, your equity is $150,000. You can choose to borrow against the equity, taking out a home equity loan for $100,000. You’ll get the $100,000 in a lump sum, which you can then use to make a big down payment on a vacation home.

If your home is worth enough and you have enough equity, you might be able to borrow enough to cover the full cost of a second home.

Usually, you can borrow up to 80% of the equity in your home. Similar to refinancing, you’ll have to pay closing costs on a home equity loan, which can add up. Closing costs vary based on your location.

One drawback of a home equity loan is losing your home if you fall behind on payments. You’re borrowing against your home, and a lender might foreclose on it if you can’t make the payments on either your home equity loan or your primary mortgage.

3. Second Mortgage

Suppose you don’t have much equity in your current home or don’t want to put your primary residence up as collateral for your vacation home. In that case, another option is to take out a conventional mortgage for your vacation home.

Getting a second mortgage is different from getting your first mortgage in many ways. A lender will want to check your credit, verify your income and ensure you have a down payment. Usually, the lending requirements are stricter for a second home than for your first, particularly if you’ll have two mortgages simultaneously.

If you have a down payment saved up, have an excellent credit score and don’t owe too much on your first mortgage compared to your income, getting a second mortgage can be the way to go.

Vacation Home Mortgage Requirements

Lenders consider vacation homes to be somewhat riskier than primary residences. A borrower is more likely to default on a second property than on their primary home if they lose their job or otherwise can’t afford payments. For that reason, vacation home mortgage requirements are usually a little stricter than for a first home.

Here’s what you’re likely to need to take out a second home mortgage.

1. Down Payment

How much you need to put down on your vacation home depends on how you plan on using it. If you live there at least some part of the year, the lender may consider the home as a second residence and may require a slightly lower down payment. If you plan on renting the property out for much of the year, a lender is more likely to consider it an investment property and might require a down payment of 20% or more.

2. Debt to Income Ratio

Your debt to income ratio (DTI) compares how much you owe to how much you earn. The lower your DTI, the less risky you look to lenders. Paying off your primary mortgage before borrowing for a second home can help you lower your DTI and increase your odds of being approved for a loan.

Lenders look at all your debts when determining your DTI. Paying off your credit cards and avoiding taking on more debt as you prepare to buy a vacation home will also increase your odds of approval.

3. Credit Score

Your credit score matters when you want to take out a mortgage for a second home. It might matter more now than it did when you got your first mortgage, as some mortgage programs, such as the FHA, VA or USDA loan programs, accept buyers with less than excellent credit scores.

4. Cash Reserves

You might not have needed to have much cash in the bank to buy your first home. With a second home, it’s a bit different. Lenders usually like to see cash reserves — money in a savings account — worth at least two months of mortgage payments. Having some cash reserves gives the lender a little peace of mind that you’ll keep paying even if you hit a financial rough patch.

In many cases, a lender will look at the big picture when deciding whether to approve you for a second home mortgage or when determining the interest rate to offer you. For example, having a credit score in the excellent range might make up for having a high DTI. A big down payment might make up for limited cash reserves or a good, but not excellent, credit score.

Apply for a Second Home Mortgage Today

Assurance Financial can help you find the financing that works for you if you’re thinking about buying a vacation property. We offer refinancing as well as conventional mortgages.

To learn more and see what you qualify for, start the online application process with us today.

Most people dream of owning a home, whether it’s a small one in the city or a rural one with a huge property. However, affording a home is difficult and saving up enough money can be challenging. Obtaining a mortgage is a big step, and you likely have many questions. One important thing you will need to know is how much of a mortgage you can afford based on your income. You can use a few different guidelines to discover what percent of your net income should go toward mortgage payments each month.

What Is Included in a Mortgage Payment?

The first thing you need to know is what exactly is included in the monthly mortgage payment. Your monthly mortgage payment is usually made up of four components:

- Principal amount

- Loan interest

- Property taxes

- Insurance

This means that your monthly payment may be more than you are expecting since it includes more than just your loan.

1. Principal

The principal is the portion of the mortgage payment that goes to the actual repayment of the amount loaned. Loans are structured so that the repayment of the principal is low at first but then increases in later years.

This means most of your money goes towards interest at the beginning of paying a mortgage. At the end of your mortgage term, the amount of principal paid will add up to the amount loaned. For example, if you purchase a $200,000 home and put $40,000 down, your total principal would be $160,000.

2. Interest

Interest is the price you must pay for borrowing money. At the beginning of your mortgage term, you will pay more towards interest than the principal.

When you’re in the process of getting your mortgage, you will be able to see how much interest you will end up paying over the course of your loan. This can end up being a lot of money, but that’s the cost of obtaining a loan. Interest rates vary but are typically between 3% and 5%, sometimes more or less, depending on different factors.

3. Taxes

You pay your property taxes to local governments to fund things like schools, firehouses, police departments and other public works. They are based on your property’s value and local tax rates.

While property taxes are calculated each year, you can usually include them in your monthly payments. The lender holds the funds in escrow until the taxes are due. This allows you to pay your taxes over time rather than paying a large sum all at once.

4. Insurance

You may have to pay two different types of insurance. If you pay less than 20% on the down payment, you may be required to purchase private mortgage insurance. Since loans with low down payments are riskier, lenders want to be protected. Private mortgage insurance protects the lender if you stop making payments. If you want to avoid an additional monthly cost on your conventional loan, you must put down 20% or more.

You will also need homeowners insurance. Most mortgage companies will not let you purchase a home without it. It protects your home and finances in the event of a natural disaster, fire or accident at the property. You should consider home insurance even if you are not required to.

Other Important Mortgage Terms

The mortgage process is often confusing, and it’s even worse if you don’t understand some of the terms. These are a few of the important mortgage terms to know:

- Amortization: The process of paying off a loan is called amortization.

- Annual Percentage Rate (APR): The APR is the cost of taking out a loan.

- Assessed value: The assessed value of a home is the value the local tax agency places on it, regardless of the selling price. Property taxes are based on the assessed value.

- Cash to close: This term refers to the amount of money you will need to bring with you to closing.

- Default: If you stop making payments on the loan or are paying less than required, you are defaulting on your mortgage. This can lower your credit score and cause the bank to foreclose on your home.

- Equity: As you pay off your principal, you are gaining equity in the home. Equity is the difference between the home’s value and the amount you owe.

- Foreclosure: If you default on your loan, the lender will take control of the property and try to get the money owed by selling the house.

- Title: The title is the record of who owns and has owned the property.

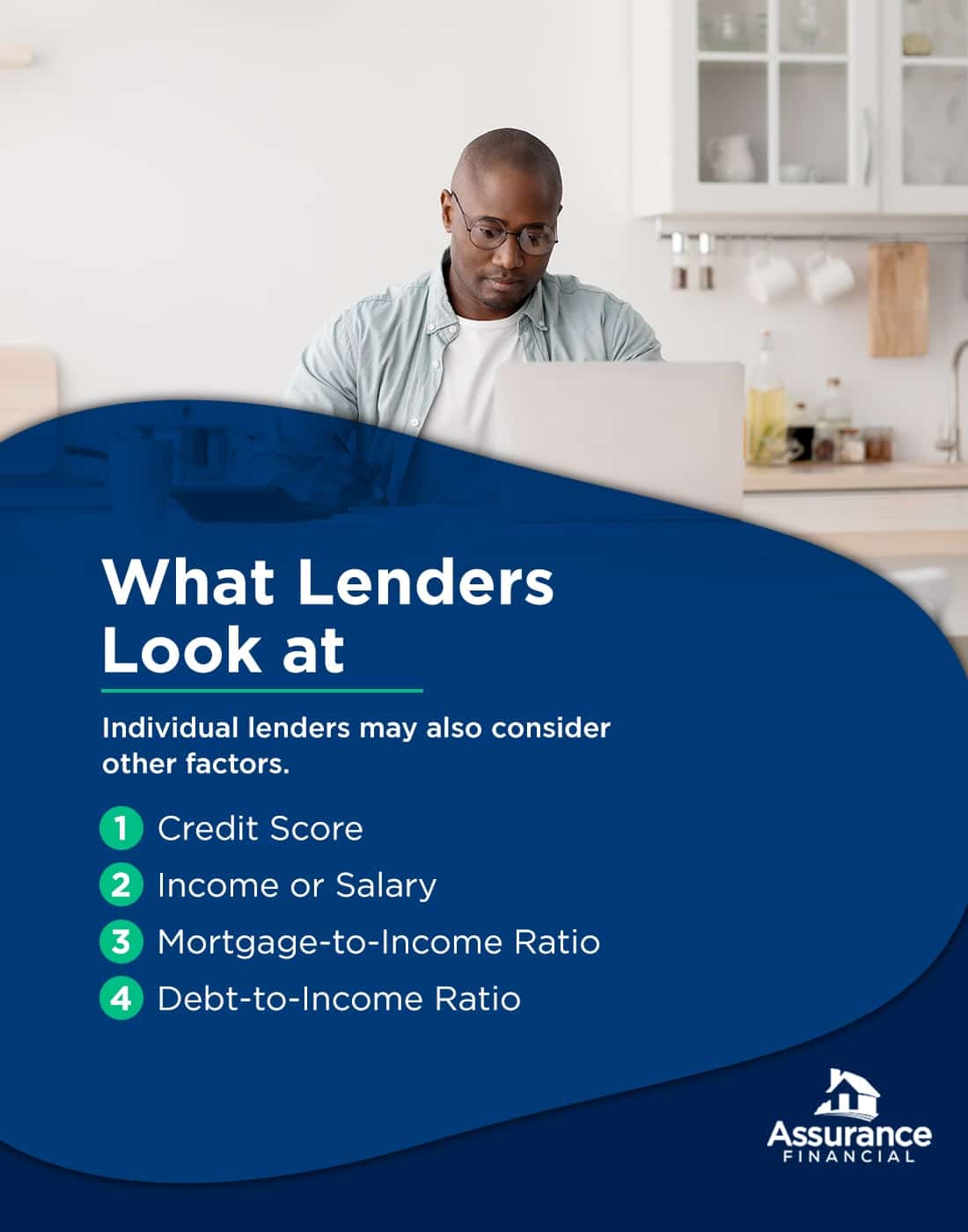

What Lenders Look at

Lenders look at more than just your income to determine what mortgage you qualify for. Your down payment, credit score and income will all be considered in relation to the amount of the loan you are seeking. Individual lenders may also consider other factors.

Credit Score

Many factors go into your credit score, such as how long you’ve had credit, the amount of credit you have access to, your repayment history and more. Lenders always check your credit score to determine if you are a responsible borrower who will pay off the loan.

A higher credit score will allow you to get better rates on your mortgage. Usually, a score of 740 or higher will help you get the best mortgage rates available. If your credit score is lower than 630, you may end up paying a much higher rate if you qualify for the loan. If your credit score is too low, you may not qualify for a conventional loan at all. Learn how to build your credit to get a mortgage loan.

Income or Salary

Lenders will need to know what your income is. They have to ensure you make enough money to pay the mortgage and all your other expenses. Of course, a higher income will likely help you qualify for a bigger mortgage.

Mortgage-to-Income Ratio

Your mortgage-to-income ratio, sometimes called the front-end ratio, will be calculated. This ratio is the percentage of your gross income that you have to put toward your mortgage payment. Most of the time, this should be below 28%. However, some lenders may allow it to be higher.

Debt-to-Income Ratio

Your debt-to-income ratio, sometimes called the back-end ratio, is also important. This ratio considers all your debt, like credit card debt, auto loans, child support, student loans and other debts in relation to your income.

How Much of Your Income Should Go Towards a Mortgage Payment?

When considering how much you can spend on a mortgage, you will need to calculate your income. Find your monthly gross income and monthly net income, as you will need both these numbers to help with these calculations.

It’s important to note that the amount of mortgage you can afford depends on more than just your income, so these are just guidelines to help. You’ll notice that the numbers will end up being different depending on which calculation you use.

28% of Gross Income

One calculation to calculate how much of your income can go towards your mortgage payment is the 28% rule. This rule says that you should not spend more than 28% of your gross income on your mortgage payment. Gross income is your income before any deductions or taxes are taken out. Find your monthly gross income by reviewing your recent paystubs. Then, multiply that number by 0.28 to find the maximum you should be spending on your mortgage payment.

For example, if you make $4,000 a month before taxes, you multiply that by 0.28 to get $1,120. The amount of $1,120 would be the max amount someone making $4,000 a month could spend on the mortgage payment. If you make $10,000 a month before taxes, you would be able to spend up to $2,800 on the mortgage payment each month. Income greatly affects the amount you can afford.

25% of Net Income

Another calculation you can use to find how much of your income you can spend on your mortgage payment is the 25% method. This method allows you to use your net income rather than your gross income. When you use your post-tax income, you use 25% instead of 28%. Find your monthly net income and multiply that number by 0.25. That number is the max you should be spending monthly on your mortgage.

For example, if you make $3,200 a month after taxes, you would multiply $3,200 by 0.25. Using these numbers, you would be able to afford a mortgage payment of $800 a month. This method can vary greatly because taxes are different depending on where you live.

35%/45% Debt Model

Another helpful calculation is the 35%/45% model. For this one, calculate your total monthly debts including, the mortgage payment. You will also need your pre-tax income and after-tax income amounts. If your other debts are fairly low, this method allows you to allocate more money to your mortgage payment. This method also provides a range your debts should fall in.

Multiply your pre-tax income by 0.35 and your after-tax income by 0.45. For example, let’s say someone makes $4,000 a month before taxes, which ends up being $3,200 after taxes. They would multiply $4,000 by 0.35, resulting in $1,400. Then, they would multiply $3,200 by 0.45, which is $1,440. This means this person’s monthly debts, including their mortgage payment, should be between $1,400 and $1,440.

Learn About Other Types of Loans

Most of these guidelines are in relation to conventional loans, but you may qualify for another type of loan. There are a few mortgage programs that allow people with low credit scores or savings to still purchase a home. VA loans and FHA loans have less strict requirements than conventional loans, so it’s worthwhile to look into them if you don’t think you will qualify for a conventional loan.

VA Loan

If you are a veteran, active-duty service member, member of the National Guard or Reserve, surviving spouse of a veteran or prisoner of war, you may qualify for a VA loan. VA loans have lower down payment requirements than conventional loans and FHA loans. You may not need to put down a down payment at all. There is also no credit score requirement, and lenders consider many factors before making a decision.

FHA Loan

To qualify for an FHA loan, you need to meet several requirements. You need a credit score of at least 500, and you will also need to put down a down payment. If you have a high credit score, you may be able to put down as little as 3.5%. If you’re approved, you will need to pay for mortgage insurance. Learn more about VA loans and FHA loans.

USDA Loan

If you are unable to get other types of loans, you may be able to get a USDA loan. There are many requirements, but they are designed for low-income borrowers. There are both direct loans and USDA guaranteed loans. Learn more about USDA loans.

[download_section]

How to Lower Your Monthly Mortgage Payment

If your income is too low or your monthly debts are too high, you may have trouble obtaining a mortgage. However, there are a few ways to lower your monthly mortgage payments:

- Find a home for a lower price: If you find the mortgage payments will be too high, you may need to spend less on your home. Use an affordability calculator to find out the approximate value of the home you can afford.

- Choose a longer loan term: The longer the loan, the lower the payments. However, you will end up paying more interest. A 30-year loan is typical.

- Spend more upfront: When you make a bigger down payment, you are reducing the amount of the loan. If you put down 20% or more, you will also avoid costly private mortgage insurance.

- Find a lower interest rate: Shop around to find a lower rate for your mortgage. The interest adds up, so if you can find a better interest rate, you will be saving a lot of money over the term of the loan.

Choose Assurance Financial

Assurance Financial is an independent, full-service residential mortgage lender that can process your loan end-to-end. We have every type of loan on the market and the latest in application technology.

We make it easier than ever to apply for and obtain a mortgage you can afford. Use our affordability calculator to find out your front-end and back-end ratios and the value of the home you should aim for. Why wait to start living your dream? Apply online today in as little as 15 minutes at Assurance Financial. If you’d rather talk to a person, we do that, too!

Linked sources:

- https://assurancemortgage.com/mortgage-term-glossary/

- https://assurancemortgage.com/how-to-build-credit-to-get-loan/

- https://assurancemortgage.com/fha-vs-va-loans/

- https://assurancemortgage.com/what-is-a-usda-loan-how-to-apply/

- https://assurancemortgage.com/calculators/how-much-can-i-afford/

- https://assurancemortgage.com/apply/

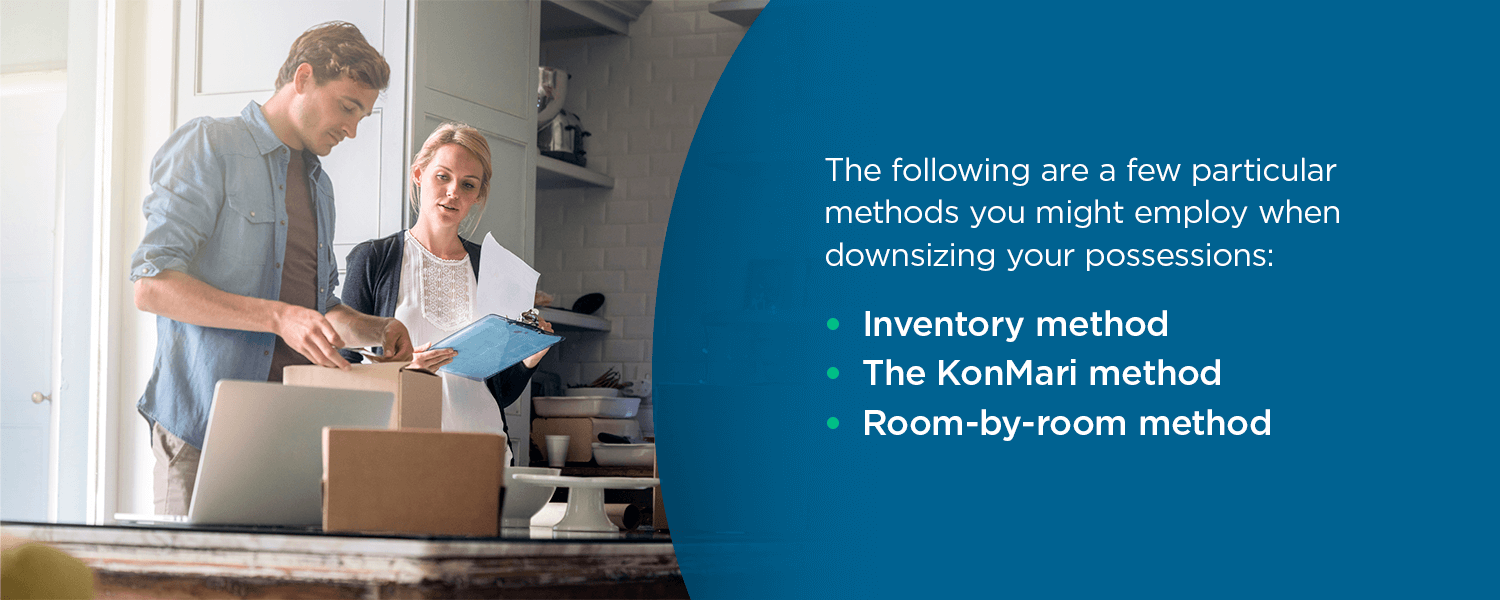

If you’re wondering when you should downsize your home, understand that it may be a lengthy process. While everyone’s timeline looks different based on their situation, downsizing involves a multistep process:

- Downsizing your possessions

- Preparing your home to sell

- Selling your home

- Finding and moving into a new house

If you have more space than you need, would like to save some money or plan to travel more, downsizing could be a great step to help you reach your goals. Discover the reasons and benefits of downsizing your home.

Should I Downsize My Home?

If you’re considering downsizing your home, you may be committing to a large, long-term project. Even if you have a short timeline — whether due to a sudden move or retirement — be sure to take the time to ensure downsizing is right for you. Reflect on why you want to downsize and what the process will involve realistically.

Some questions you may want to consider before downsizing your home include:

- What are my motivations for downsizing? If you want to downsize because you’re looking for a different layout for your home or to have different amenities, consider whether it might make more sense to reorganize or renovate your current home. Many homeowners whose needs change often decide to take out a second mortgage to fund their renovations.

- What do you love about your current home? During the process of buying a new home, you may be tempted to focus on the negatives of your current space. Instead, consider the aspects of your current house you love and use, and add those to your must-have list.

- What will my family or I gain from downsizing? Think about the activities and projects you will be able to accomplish with a smaller home. Perhaps it will allow you to travel more, or mean a safer environment for the children and older adults in your family.

- What are my primary concerns about downsizing? Most people’s main concern with downsizing is budget. You might also worry about missing out on storage, outside space and other amenities you enjoy in your current house.

- What is my timeline? Consider when you’d like to start your downsizing process, how long you want to take and when you ultimately want to complete the process and be in your new space.

- What are my current and future needs? When considering downsizing, think about what you need right now and how your needs might change in the future. Will you have kids moving out, parents moving in or other considerations you’ll want to account for in the downsizing process?

Reasons to Downsize Your Home

Everyone’s reasoning for downsizing will be unique to them, but there are a few important reasons many people choose to downsize. Most of these have to do with a person’s budget, living situation or dreams for the future. Take a look at six reasons why you should downsize your home:

1. Maintenance Costs

With larger homes and larger yards, you’ll confront higher costs of maintaining your spaces. Most homeowners should budget at least 1-4% of their home’s total cost to annual maintenance — you can budget less for newer homes and add more for older homes that may require more repairs. That means a 20-year-old house that originally cost $500,000 might need a budget of $20,000 each year, while a house for the same price that’s brand new may only need $5,000 for incidental maintenance and upkeep.

Smaller homes have lower price points in many cases, so the cost of maintaining them yearly is much less. With less square footage, you’ll spend less on things like flooring, roofing and heating and cooling costs. Downsizing also might mean a smaller or no outside space, resulting in little to no cost to maintain your yard.

2. Retirement

Most people begin thinking about downsizing while considering retirement. With a little more time on their hands, many envision traveling and participating in activities that make keeping up with a large home more difficult. When you reach retirement age, you may also begin thinking about the future and the potential challenges your current space might incur as you age.

Large homes with steps, steep driveways and other mobility challenges can be dangerous for older adults. Modifications, such as stairlifts, ramps and railings, may be simple and affordable to add to existing homes, but tasks like widening doorways, adjusting counter heights, leveling flooring and remodeling the shower or tub may prove more expensive than they’re worth. In most cases, downsizing is a better alternative as people reach retirement age and have less use for the space.

For many retired individuals and couples, condos and townhomes are attractive options when thinking about downsizing. They often provide on-site maintenance with staff handling outside work as well. Secondly, they also provide a community for older adults to gather together, a service that becomes incredibly important given the increased rates of loneliness in retired adults.

3. Unused Space